The Format of Audit Opinion for Financial Review typically includes a clear statement on the scope of the review and the auditor's conclusion based on limited procedures performed. It emphasizes that the review provides limited assurance rather than the full assurance of an audit. The opinion is concise, focusing on whether anything has come to the auditor's attention that causes them to believe the financial statements are not prepared in accordance with the applicable financial reporting framework.

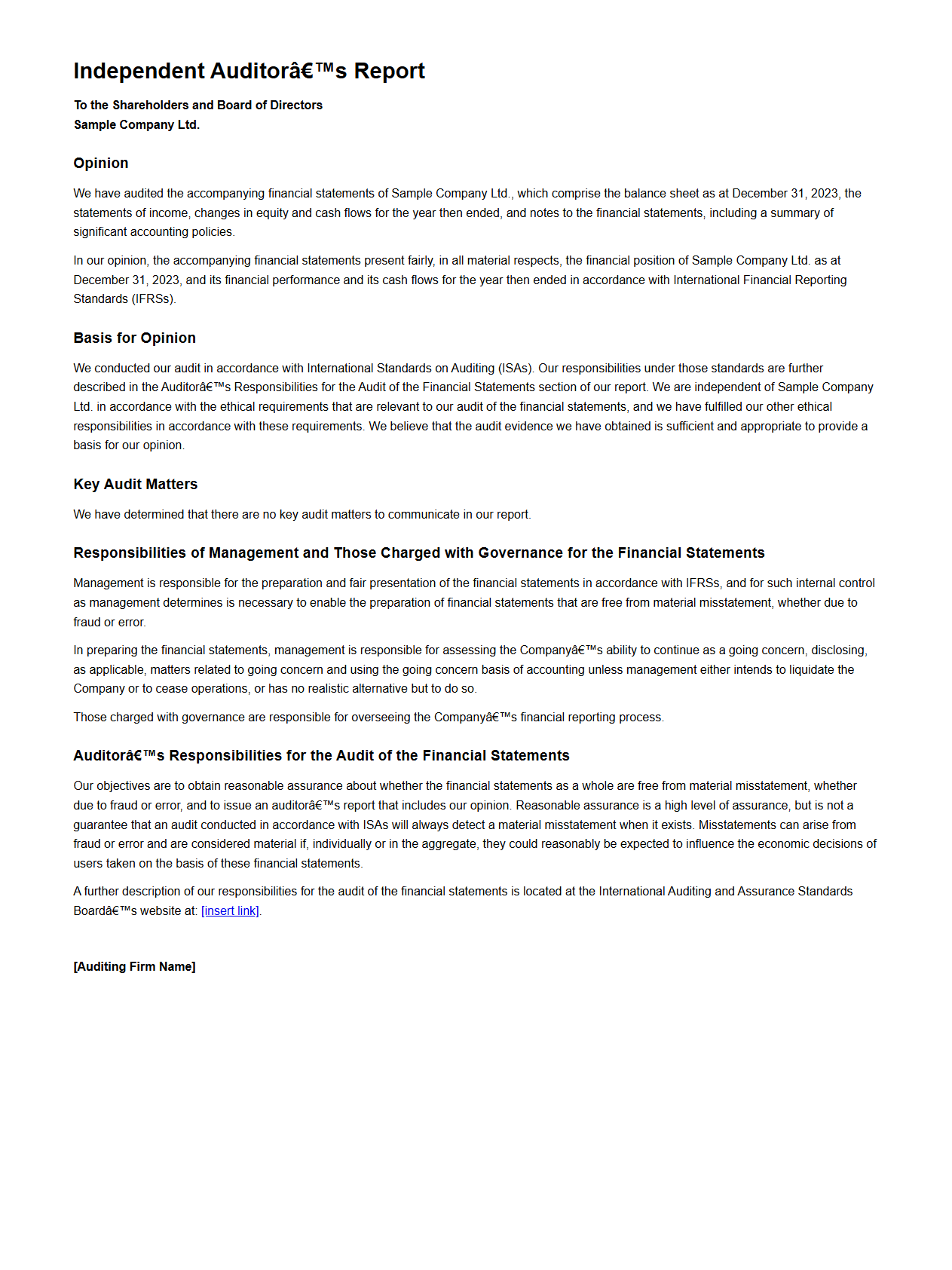

Standard Unqualified Audit Opinion Document Format

The

Standard Unqualified Audit Opinion Document Format is a formal report structure used by auditors to express an unqualified opinion, indicating that a company's financial statements present a true and fair view in accordance with the relevant accounting framework. This document typically includes key components such as the auditor's opinion, the basis for the opinion, management's responsibility, and the auditor's responsibility. Its standardized format ensures clarity, consistency, and compliance with regulatory requirements, facilitating stakeholders' trust in the audited financial statements.

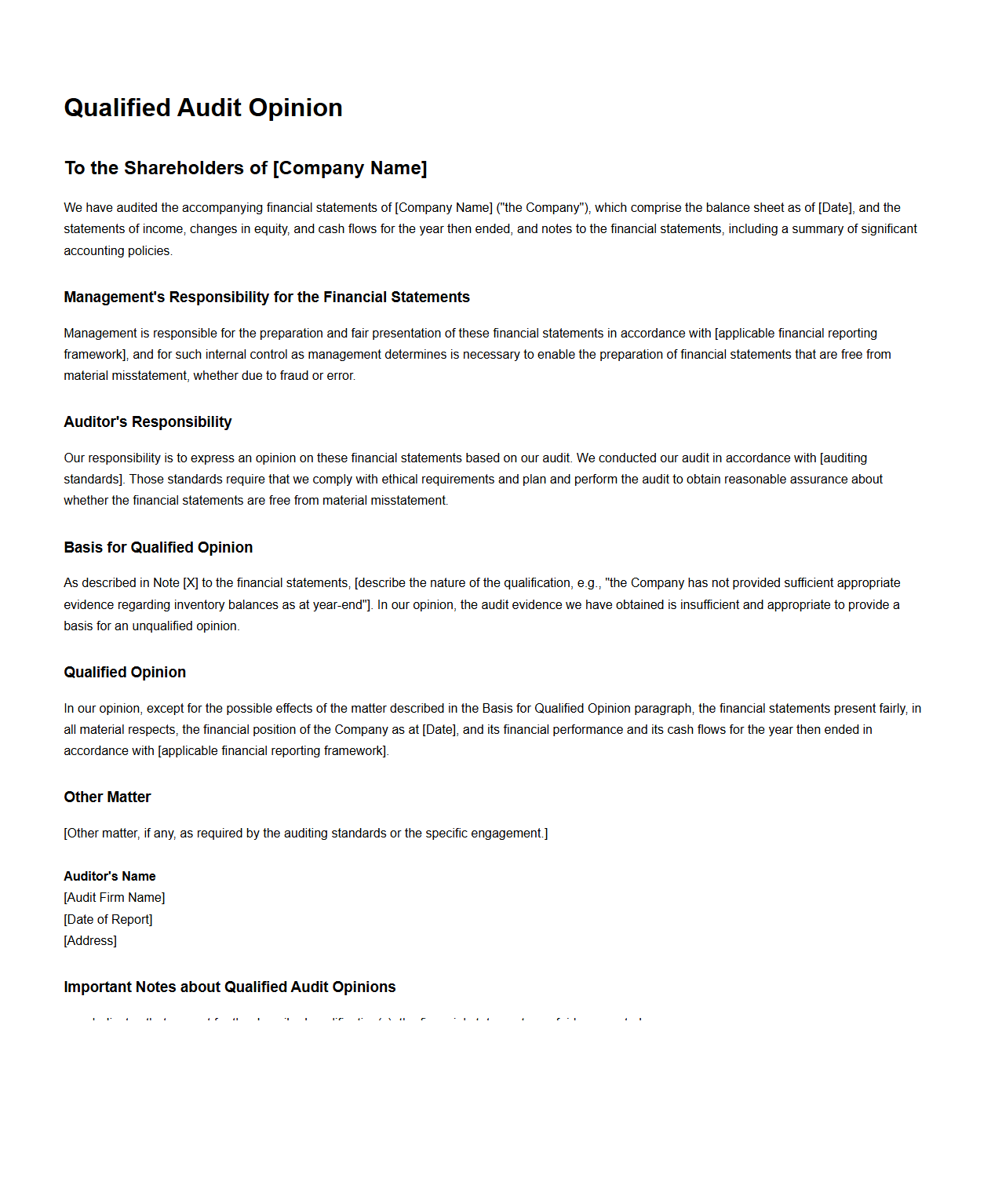

Qualified Audit Opinion Document Format

A

Qualified Audit Opinion Document Format outlines the structured template auditors use to report findings when financial statements contain exceptions or deviations from standard accounting principles. This document includes specific sections such as the auditor's opinion, reasons for qualification, and detailed explanations of the issues encountered during the audit. Using a standardized format ensures clarity, consistency, and compliance with regulatory requirements in communicating the qualified opinion to stakeholders.

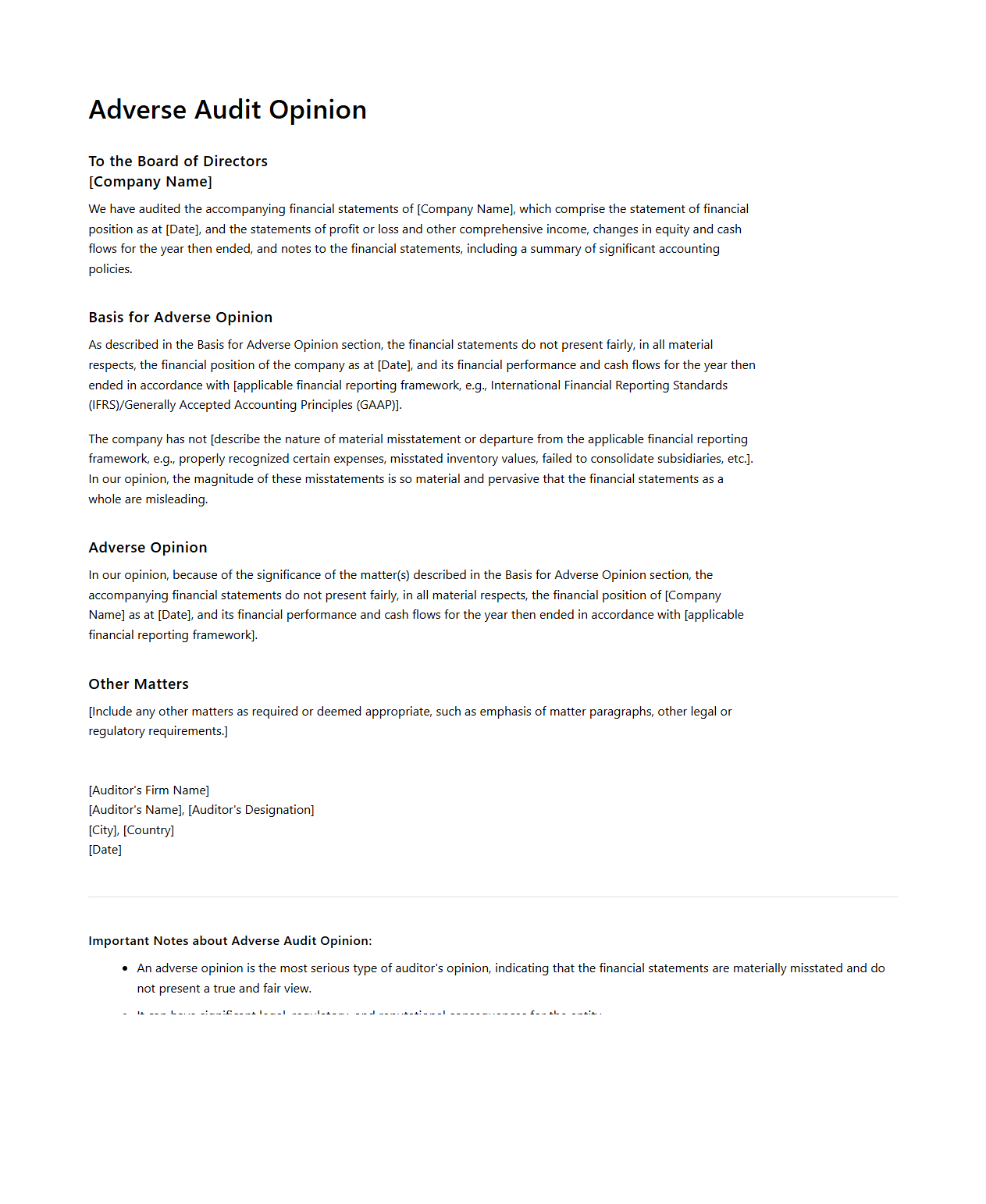

Adverse Audit Opinion Document Format

An

Adverse Audit Opinion Document Format outlines the structured presentation of an auditor's report indicating significant misstatements or non-compliance in financial statements. This document format includes sections such as the auditor's identification, basis for the adverse opinion, specific discrepancies found, and the overall conclusion stating that the financial statements do not present a true and fair view. Adhering to this format ensures clarity, transparency, and standardization in communicating the auditor's negative findings to stakeholders.

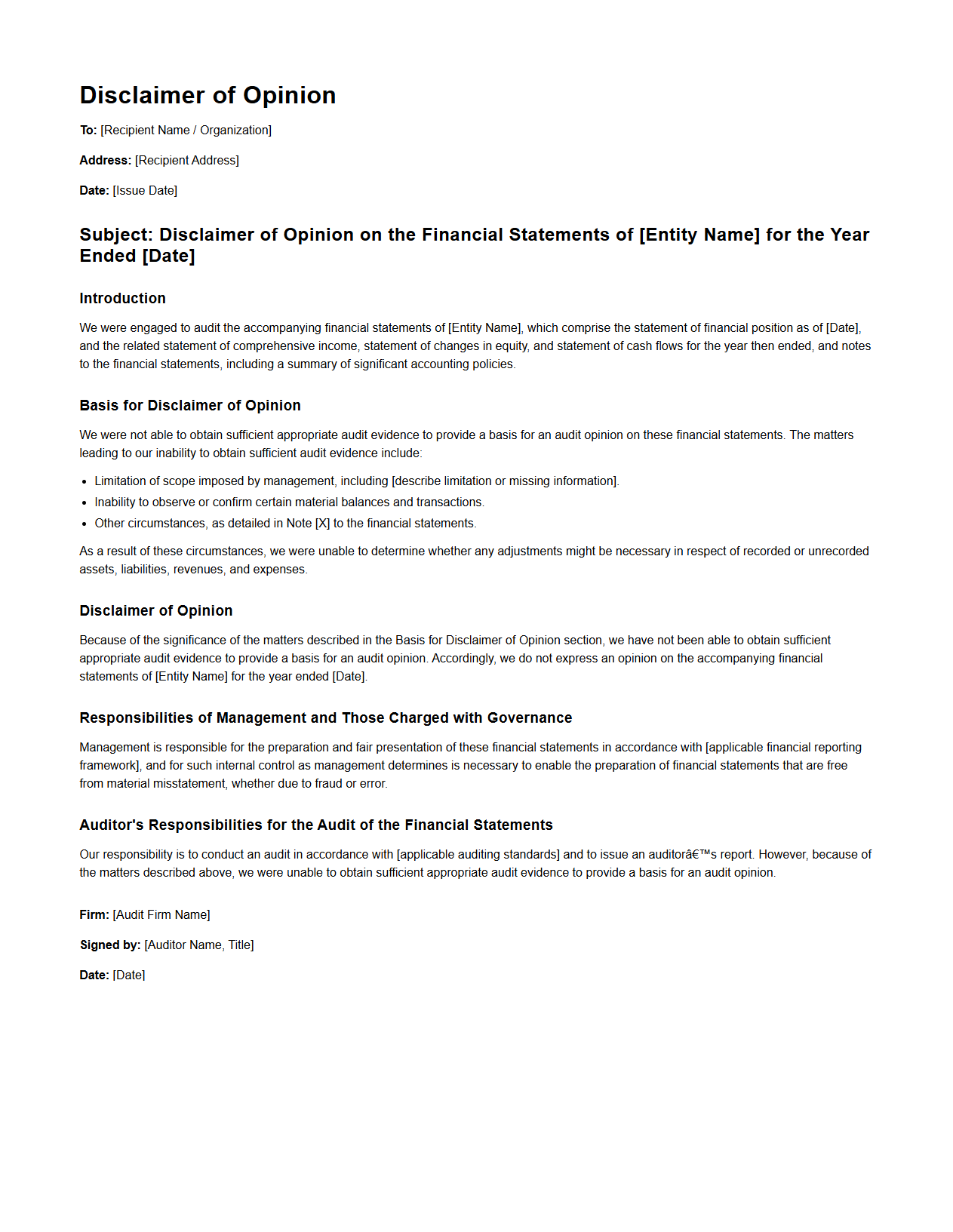

Disclaimer of Opinion Document Format

A

Disclaimer of Opinion Document Format is a structured template used by auditors to formally communicate their inability to express an opinion on a company's financial statements. This document outlines specific reasons for the disclaimer, such as insufficient evidence or scope limitations, ensuring clarity and compliance with auditing standards. It serves as an essential communication tool to inform stakeholders about the auditor's non-assessment of financial statement accuracy.

Emphasis of Matter Paragraph Format

An

Emphasis of Matter Paragraph in an audit report highlights important information that is fundamental to understanding the financial statements but does not modify the auditor's opinion. This paragraph is placed immediately after the opinion paragraph and clearly identifies the matter being emphasized along with a reference to the relevant note in the financial statements. Its purpose is to draw users' attention without affecting the auditor's overall conclusion on the financial position and performance.

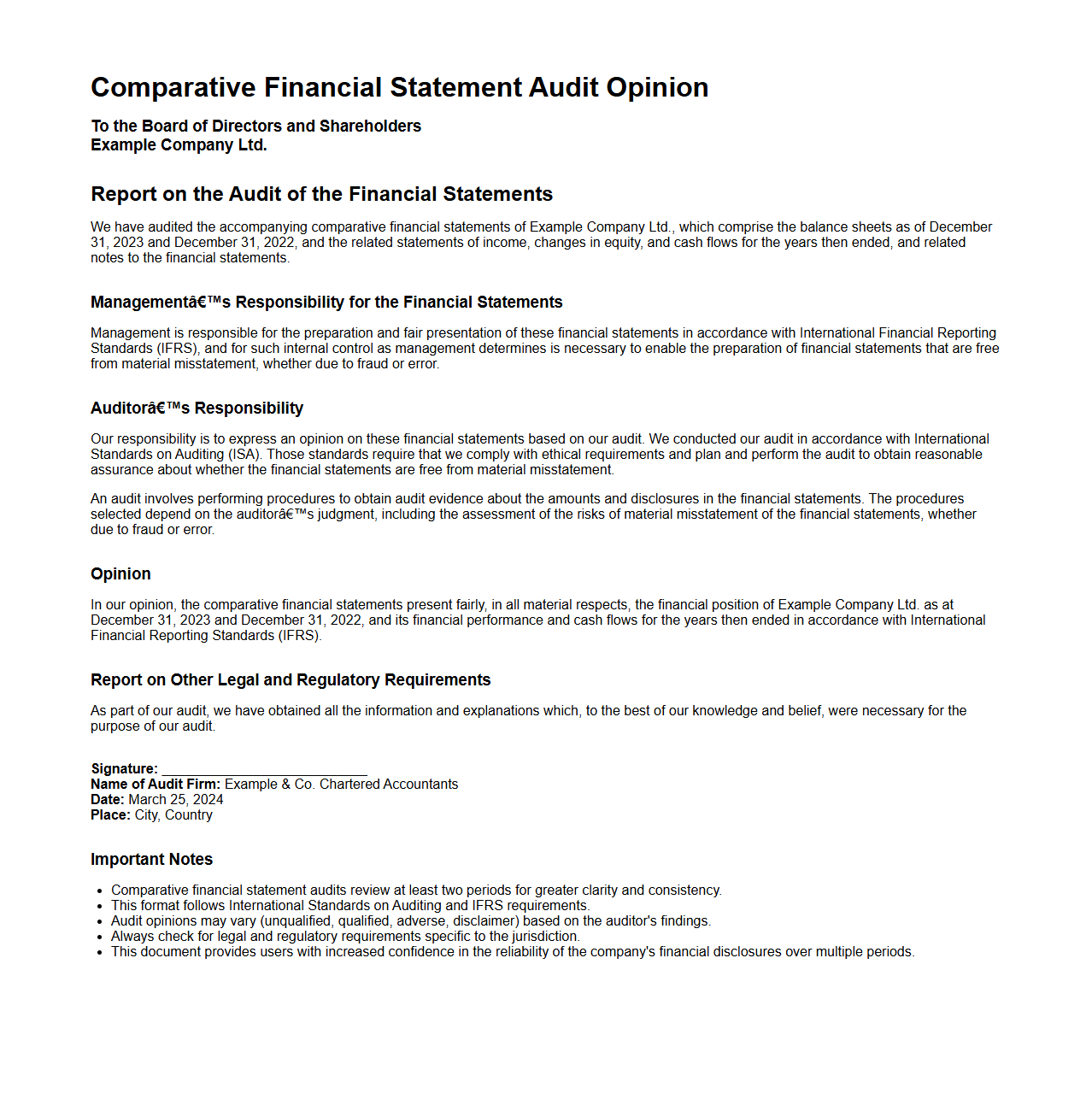

Comparative Financial Statement Audit Opinion Format

A

Comparative Financial Statement Audit Opinion Format document presents the auditor's evaluation of financial statements from multiple periods side by side, highlighting consistency and changes. This format helps stakeholders easily compare fiscal performance and compliance with accounting standards across years. It ensures transparency by clearly stating the auditor's opinion on the accuracy and fairness of the financial data for each comparative period.

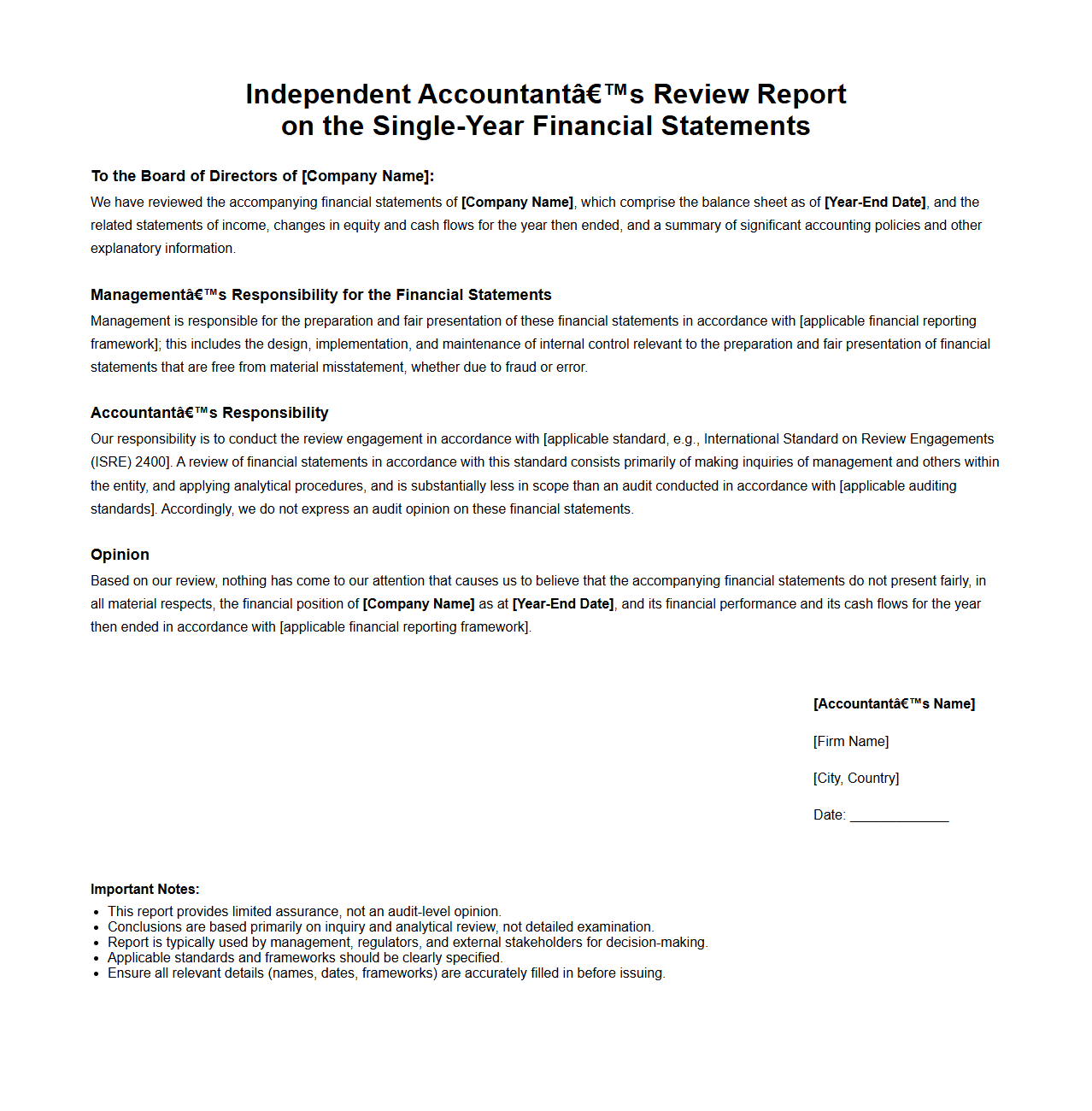

Single-Year Financial Review Opinion Format

The

Single-Year Financial Review Opinion Format document provides a structured template for auditors to express their professional opinion on a company's financial statements for a specific fiscal year. It includes sections detailing the scope of the review, the auditor's findings, and the conclusion about the financial statements' accuracy and compliance with accounting standards. This format ensures consistency and clarity in communicating the review results to stakeholders such as investors, management, and regulatory bodies.

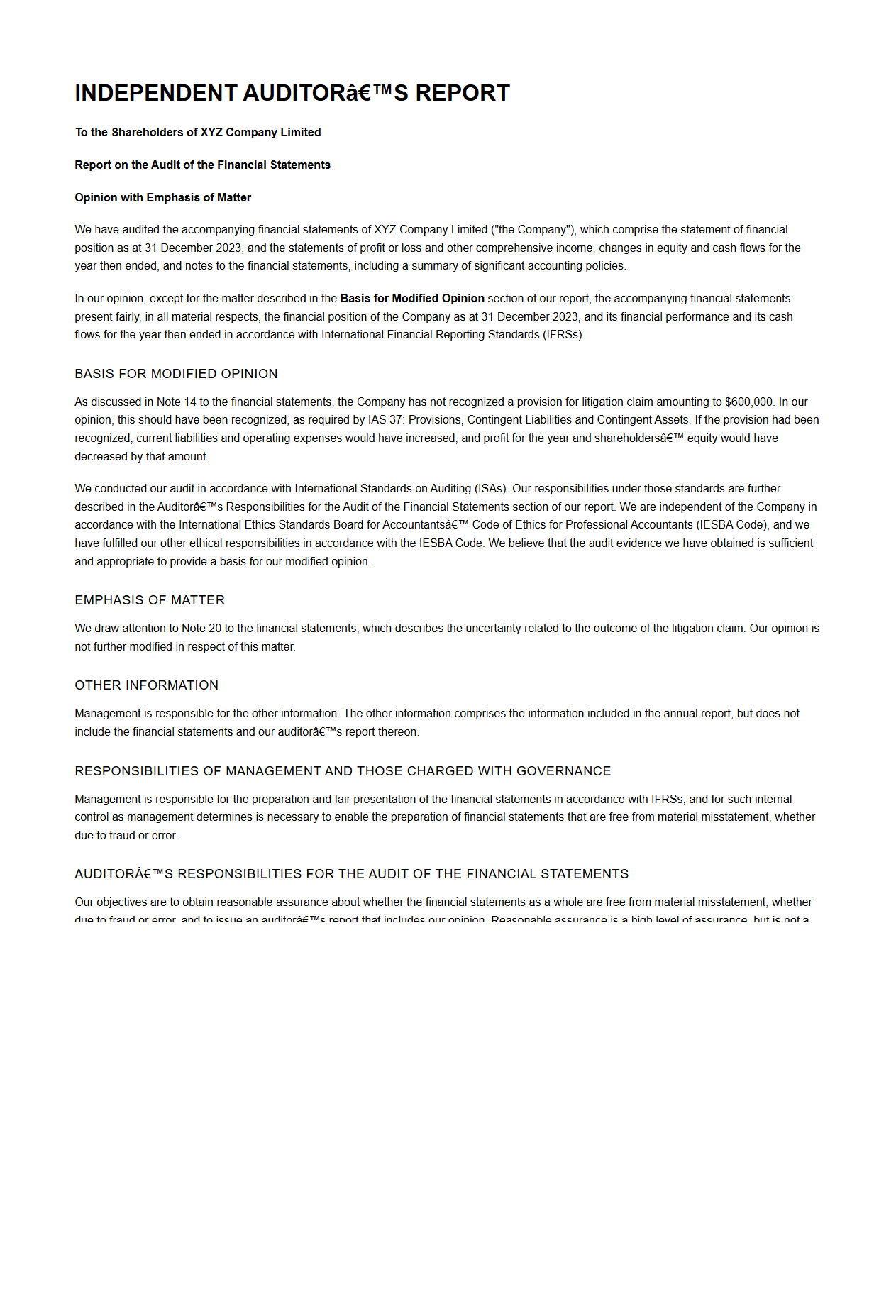

Modified Unqualified Audit Opinion Format

A

Modified Unqualified Audit Opinion Format document is issued when an auditor concludes that a financial statement is fairly presented except for a specific issue that does not overshadow the overall accuracy and compliance. This document details the auditor's reservations while confirming that the statements comply with Generally Accepted Accounting Principles (GAAP) except for the identified modifications. It is essential for stakeholders seeking a nuanced understanding of the audit findings without entirely discrediting the financial integrity of the entity.

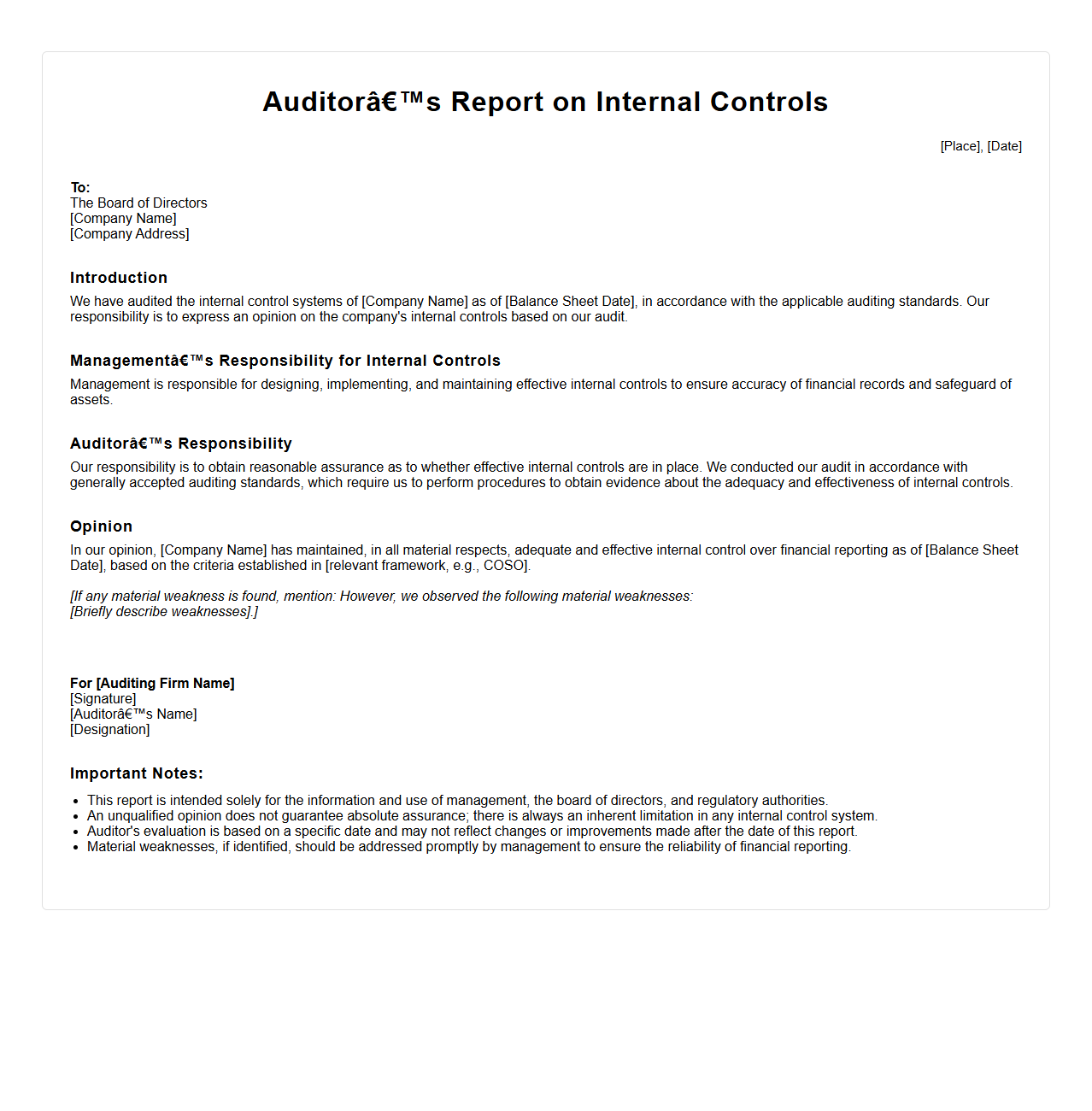

Auditor’s Report on Internal Controls Format

An

Auditor's Report on Internal Controls Format document outlines the standardized structure and key components auditors use to evaluate and report on a company's internal control systems. This format ensures consistency in presenting the auditor's assessment regarding the effectiveness of internal controls over financial reporting. It includes sections such as the scope of the audit, management's responsibility, the auditor's responsibility, and the audit findings or opinions.

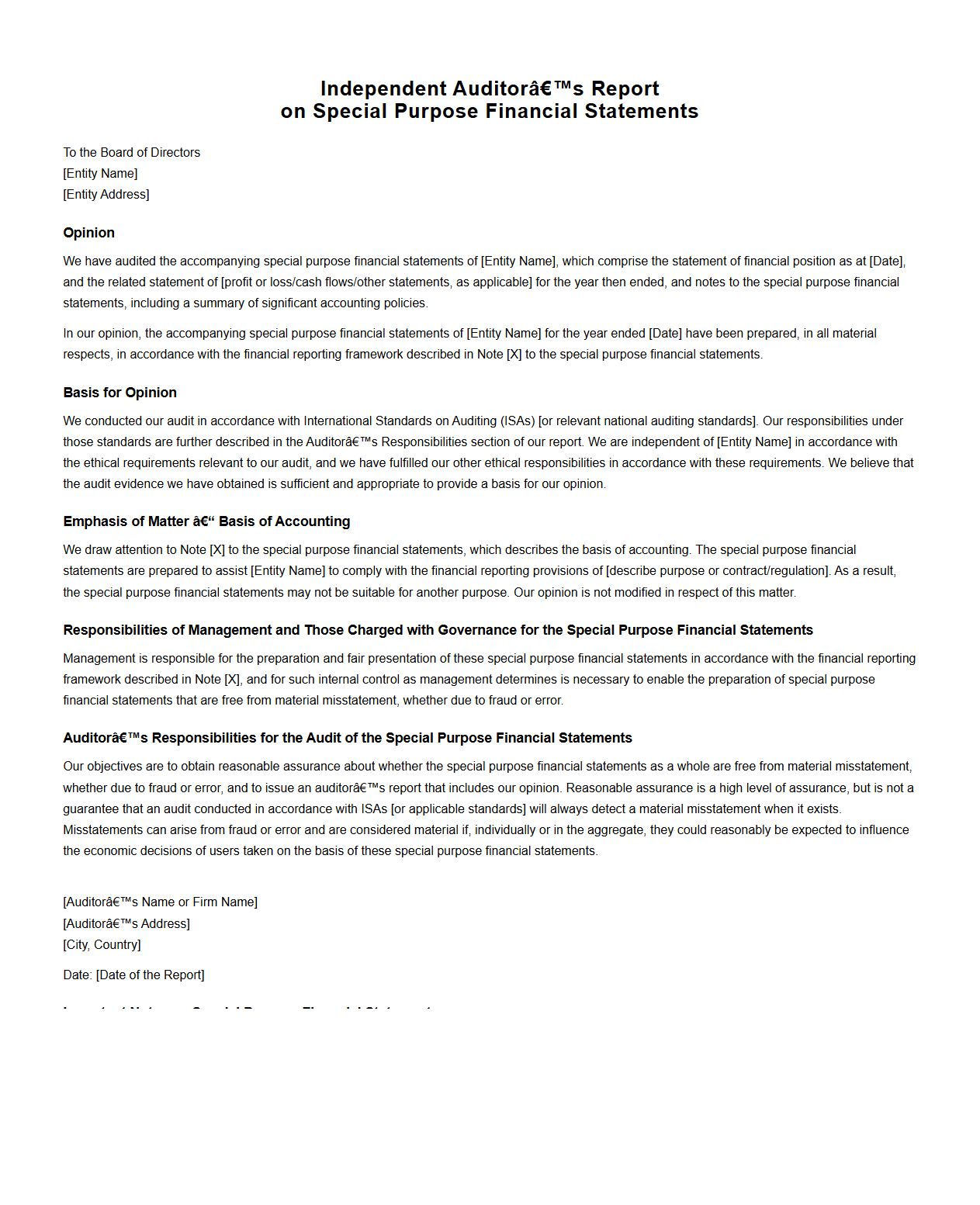

Special Purpose Financial Statement Audit Opinion Format

The

Special Purpose Financial Statement Audit Opinion Format document outlines the auditor's findings on financial statements prepared for a specific use, such as regulatory compliance or internal management. It details the auditor's conclusion on whether the financial statements present a true and fair view according to specified criteria or framework. This format ensures clarity and consistency in reporting audit results tailored to the unique requirements of the special purpose financial statements.

Specific Elements Required in the Format of an Audit Opinion for a Financial Review Engagement

The format of an audit opinion for a financial review engagement must include the title, addressee, and introductory paragraph clearly stating the scope of the review. It requires a management responsibility section, outlining management's role in preparing the financial statements. The opinion paragraph must express whether the financial statements are presented fairly in accordance with the applicable framework.

Structure of Emphasis of Matter Paragraphs in a Financial Review Audit Opinion Letter

Emphasis of matter paragraphs should be clearly labeled and placed immediately after the opinion paragraph to highlight significant uncertainties or events. They must describe the matter being emphasized without modifying the auditor's overall opinion. This structure ensures transparency while maintaining the clarity of the audit opinion.

Distinguishing the Format of a Modified Audit Opinion from an Unmodified One in Financial Review Letters

The primary distinction lies in the addition of a modification paragraph, which explains the reasons for qualification, disclaimer, or adverse opinion. Unmodified audit opinions express an unqualified view without reservations. Modified opinions explicitly highlight areas of concern, affecting the clarity and overall message of the report.

Industry-Specific Disclosures Mandated in the Audit Opinion Format for Certain Financial Reviews

Certain industries require specific disclosures integrated within the audit opinion to address regulatory compliance and sector-specific risks. These disclosures ensure the opinion is relevant and comprehensive for stakeholders within those industries. Failure to include such mandates can lead to non-compliance and reduced credibility of the review.

Concise Statement of Auditor's Responsibilities in the Conclusion Section of a Financial Review Audit Opinion

The conclusion section should succinctly state the auditor's responsibilities for conducting the review in accordance with applicable standards. It emphasizes the limited assurance provided, differentiating it from an audit's higher level of assurance. This clarity helps stakeholders understand the scope and limitations of the auditor's work.