The Format of Engagement Letter for Statutory Audit typically includes the scope of the audit, responsibilities of both the auditor and the client, and the terms of remuneration. It clearly defines the audit objectives, compliance requirements, and the expected deliverables. This letter serves as a formal agreement to ensure mutual understanding and accountability throughout the audit process.

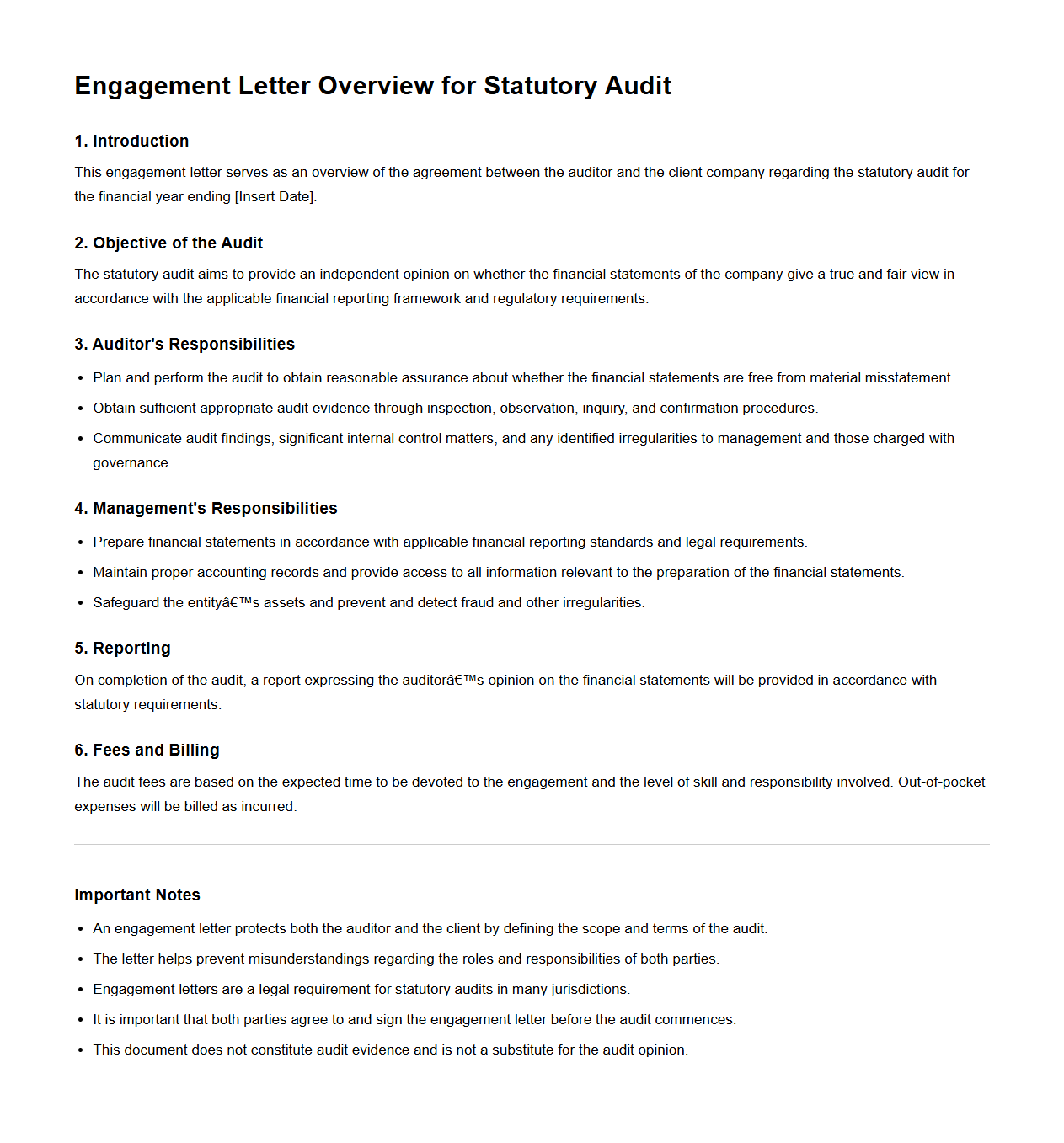

Engagement Letter Overview for Statutory Audit

An

Engagement Letter Overview for Statutory Audit is a formal document outlining the scope, objectives, and responsibilities of both the auditor and the client during the statutory audit process. It ensures clarity on audit timelines, deliverables, fees, and compliance requirements as per regulatory standards. This letter acts as a contractual agreement that establishes mutual understanding and minimizes disputes throughout the audit engagement.

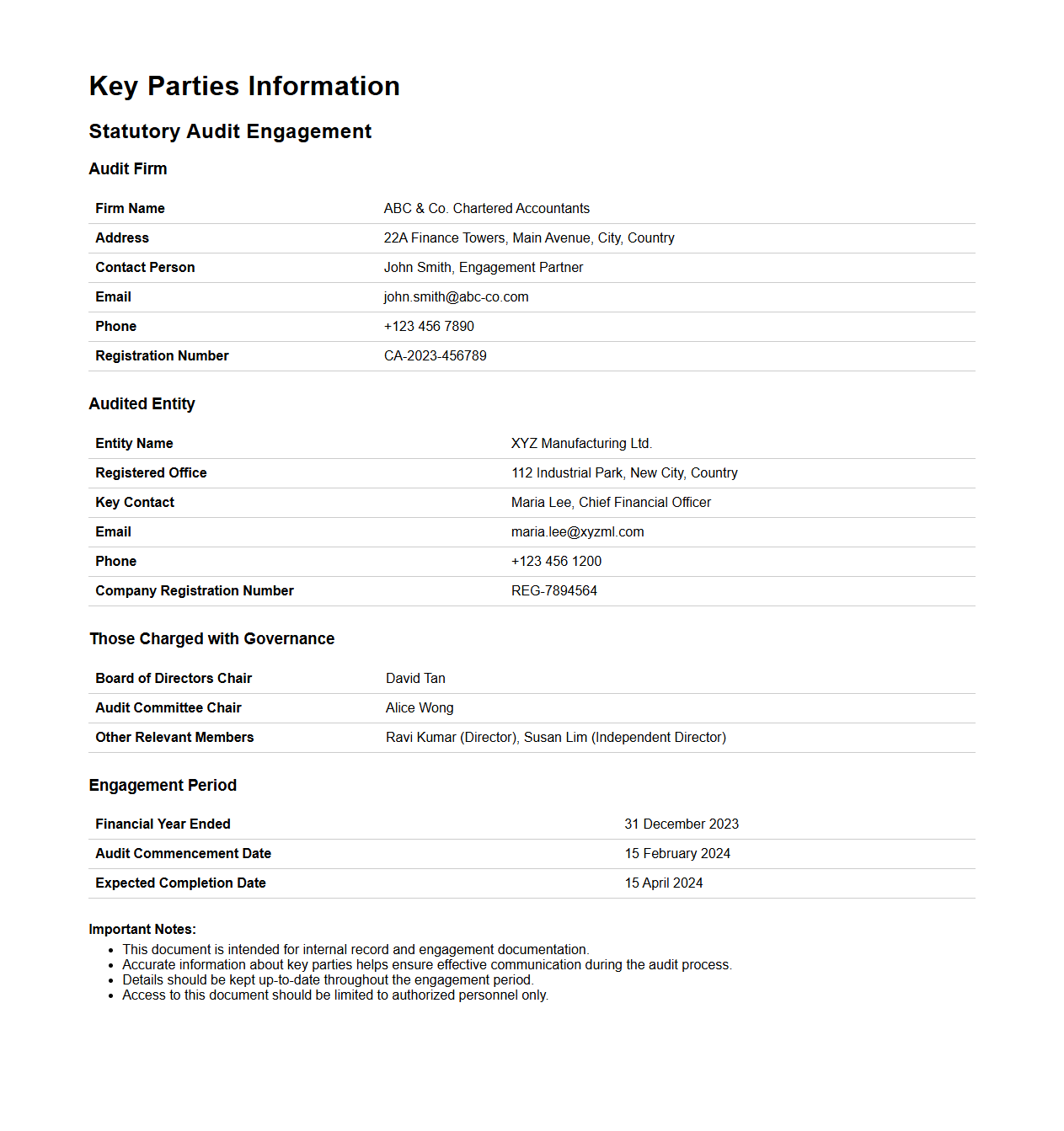

Key Parties Information in Statutory Audit Engagement

Key Parties Information in a Statutory Audit Engagement document refers to the detailed identification and roles of all significant individuals and entities involved in the audit process. This includes the client's management team, audit committee members, external consultants, and any third parties relevant to the audit scope. Maintaining accurate

Key Parties Information ensures clear communication, responsibility allocation, and compliance with auditing standards throughout the engagement.

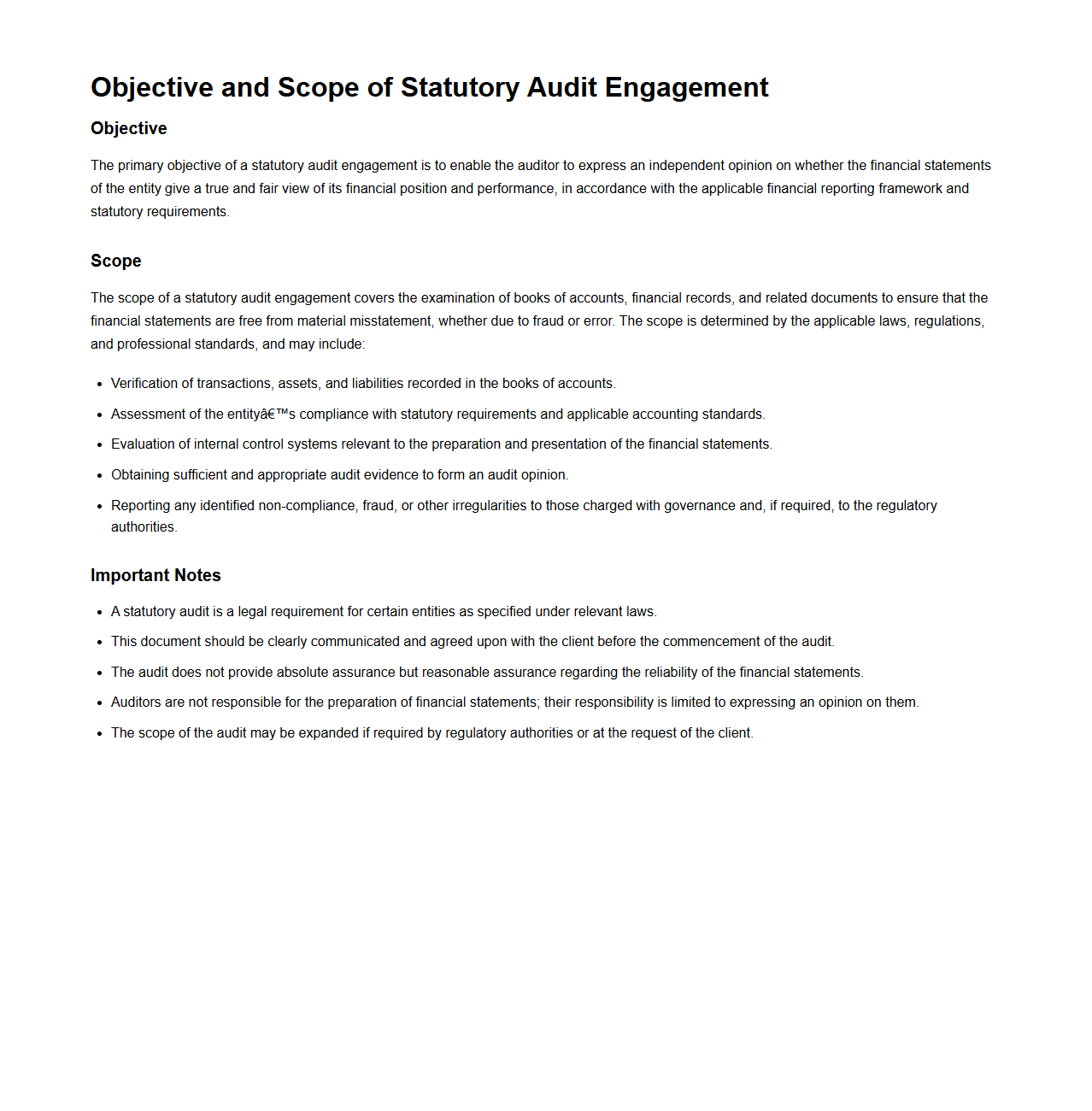

Objective and Scope of Statutory Audit Engagement

The

Objective and Scope of Statutory Audit Engagement document defines the purpose and extent of the audit process conducted to ensure an organization's financial statements comply with applicable laws and accounting standards. It outlines the responsibilities of the auditor, the financial areas to be examined, and the regulatory framework governing the audit. This document helps establish clear expectations between the auditor and the client, enhancing transparency and accountability during the statutory audit.

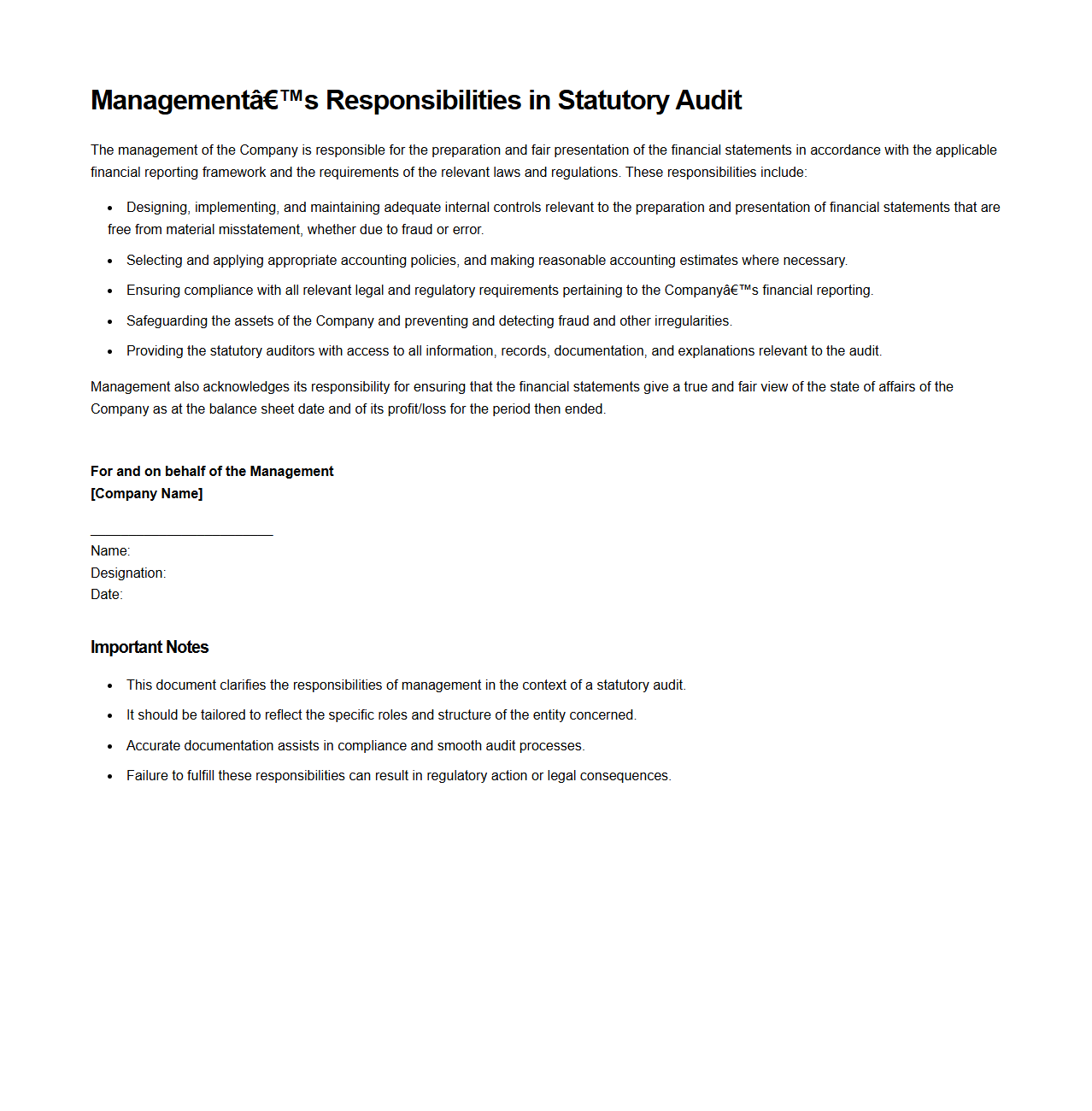

Management’s Responsibilities in Statutory Audit

Management's responsibilities in a

statutory audit document include preparing accurate financial statements in accordance with applicable accounting standards and regulations. They must provide access to all relevant records, documentation, and information necessary for the auditor to perform a thorough examination. Management is also responsible for establishing and maintaining effective internal controls to ensure the integrity of financial reporting.

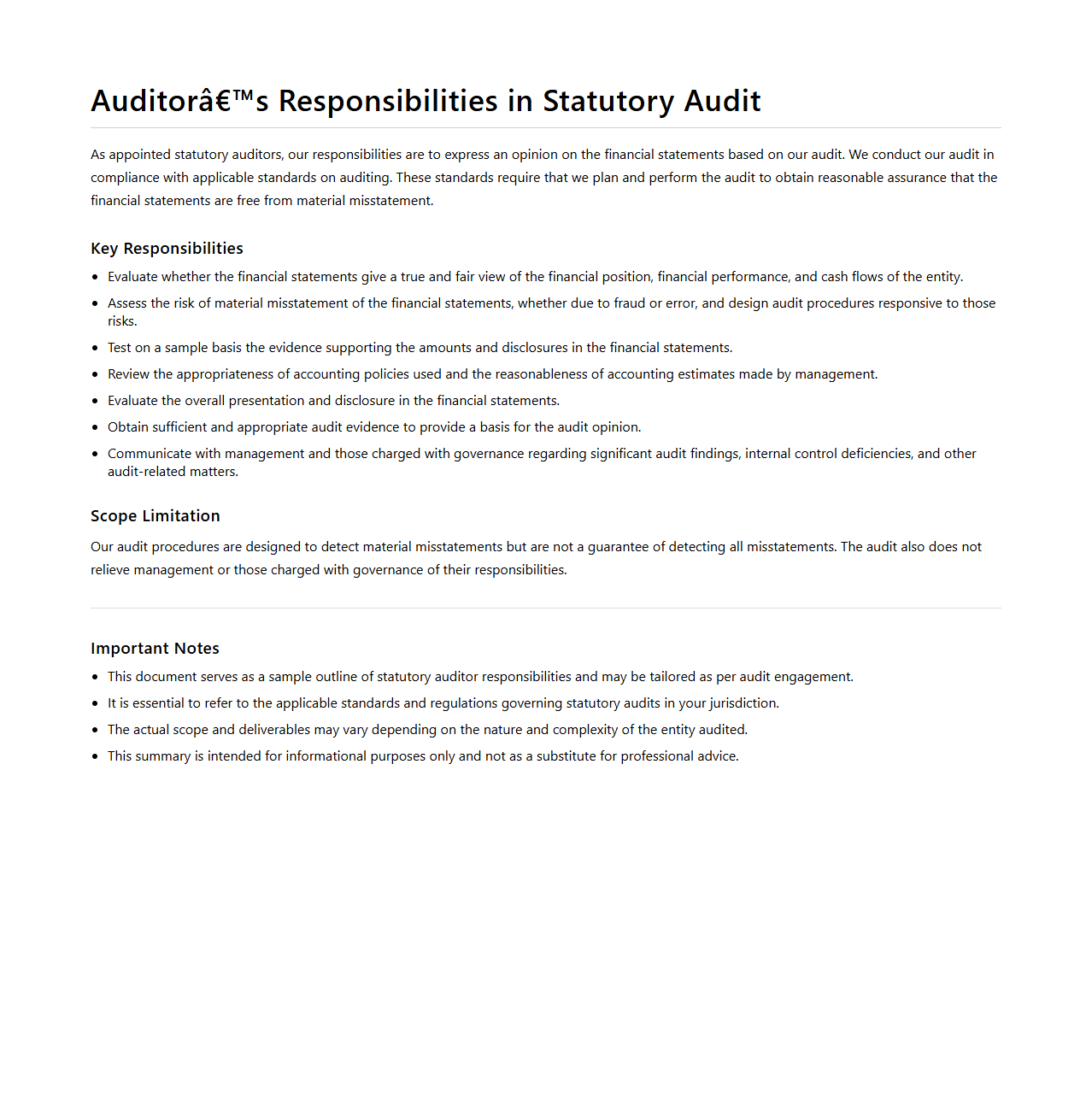

Auditor’s Responsibilities in Statutory Audit

An

Auditor's responsibilities in a statutory audit document include evaluating the accuracy and completeness of financial statements to ensure compliance with applicable laws and accounting standards. The auditor must obtain sufficient and appropriate audit evidence to form an independent opinion on whether the financial statements present a true and fair view of the entity's financial position. Responsibilities also involve identifying any material misstatements and assessing risks related to fraud or error during the audit process.

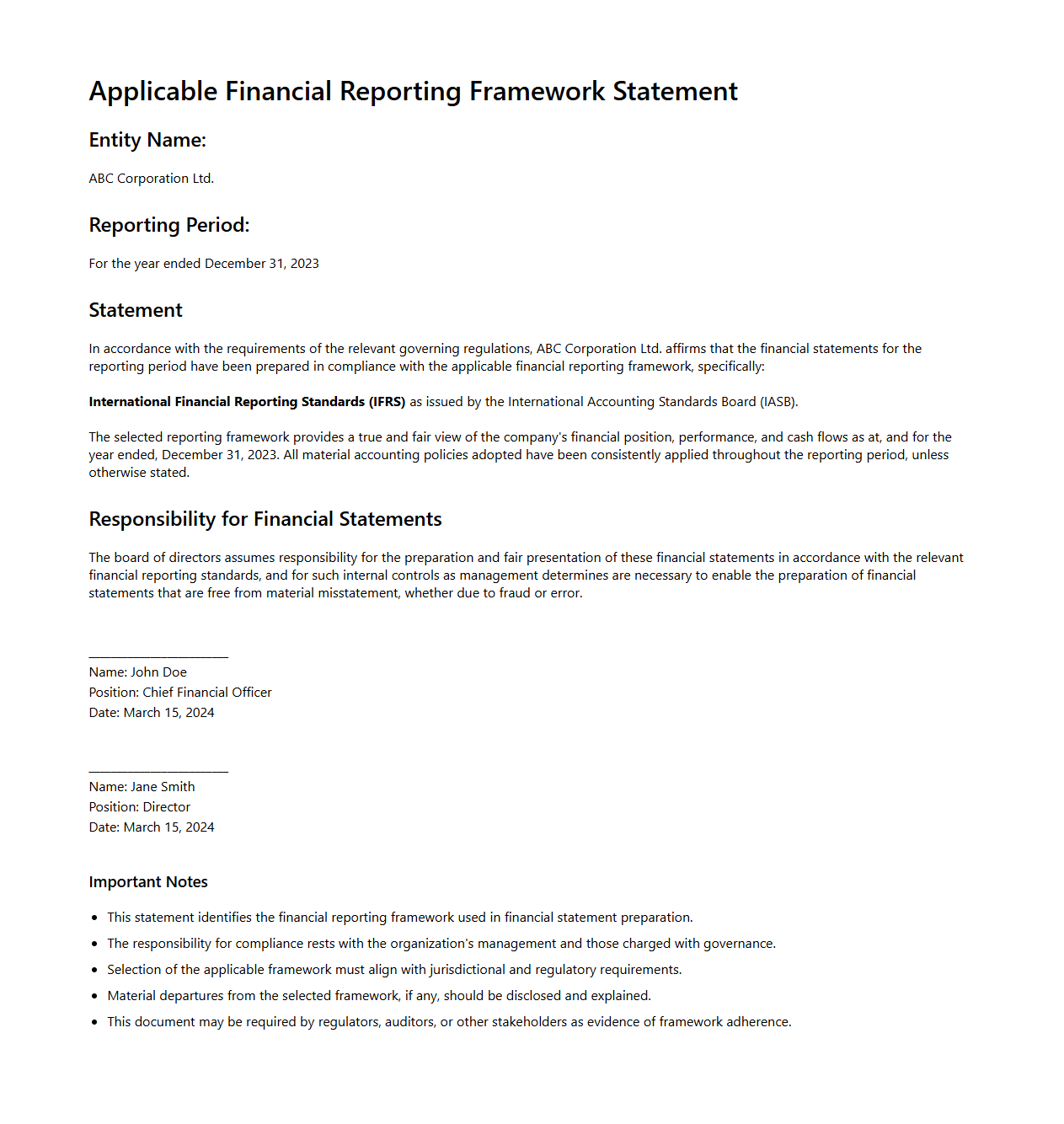

Applicable Financial Reporting Framework Statement

The

Applicable Financial Reporting Framework Statement outlines the specific accounting principles, standards, and regulations used to prepare financial statements. It ensures transparency and consistency by identifying frameworks such as GAAP, IFRS, or other statutory requirements. This document is essential for auditors, investors, and regulatory bodies to assess the accuracy and compliance of financial reporting.

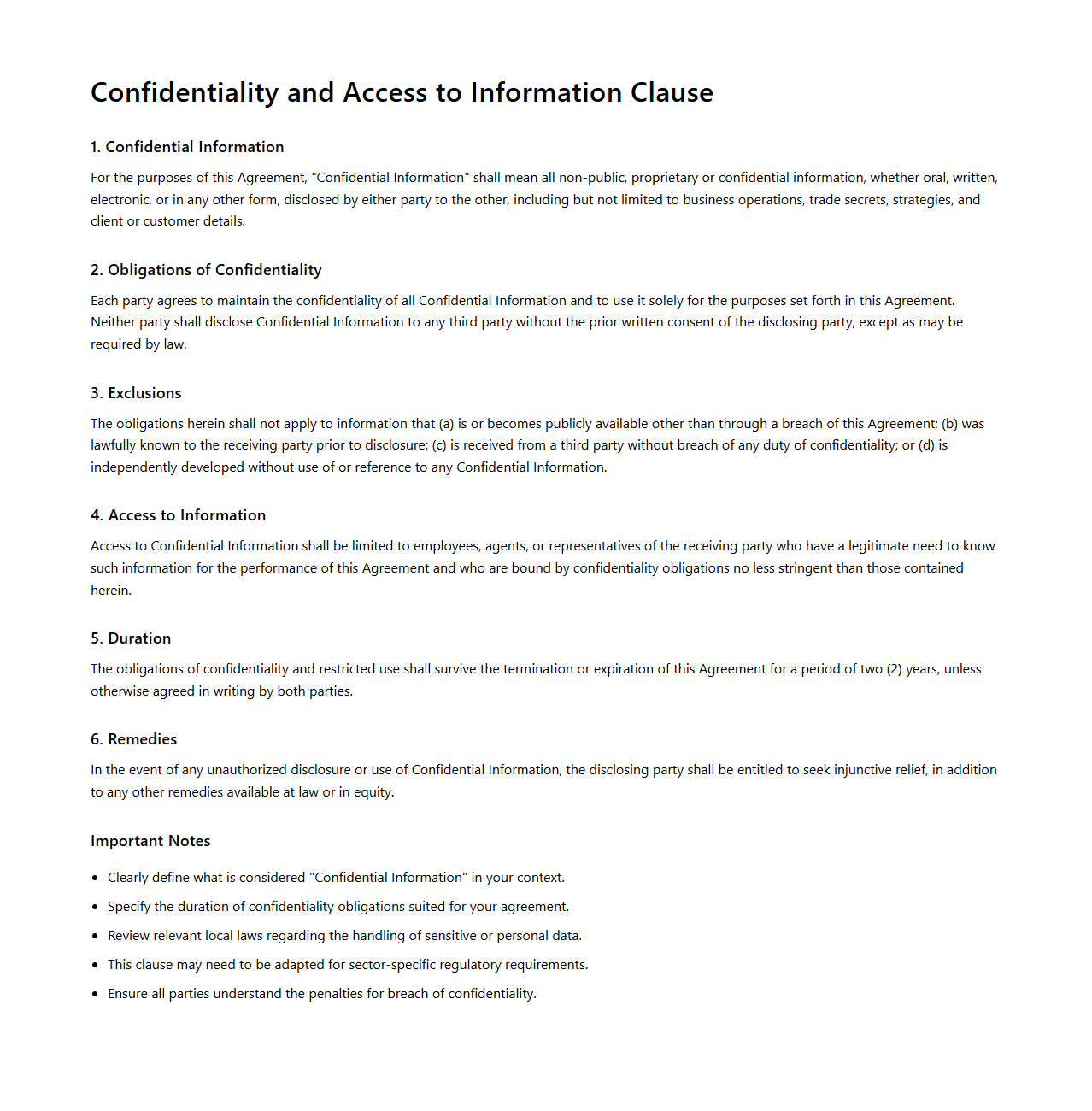

Confidentiality and Access to Information Clause

The

Confidentiality and Access to Information Clause document outlines the obligations of parties to protect sensitive information from unauthorized disclosure while specifying the conditions under which access to such information is permitted. It defines the parameters for handling confidential data, ensuring compliance with privacy laws and organizational policies. This clause is crucial in maintaining trust and safeguarding proprietary or personal information during business relationships.

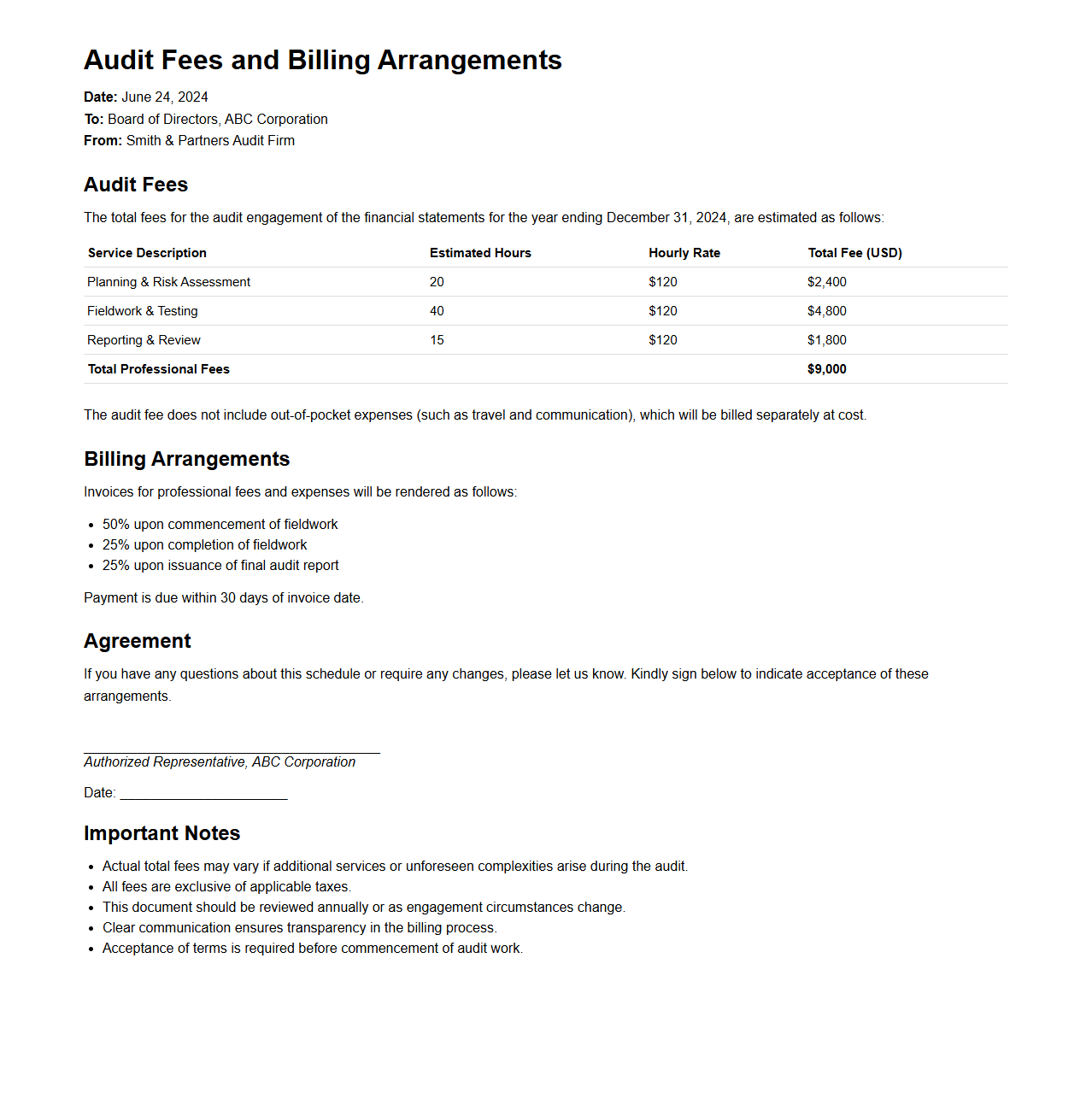

Audit Fees and Billing Arrangements

The

Audit Fees and Billing Arrangements document outlines the terms and conditions related to the costs and payment schedule for audit services provided by a professional firm. It specifies the fee structure, whether fixed, hourly, or contingent, and details the invoicing process along with acceptable payment methods and deadlines. This document ensures transparency and agreement between the auditor and the client regarding financial expectations and billing procedures.

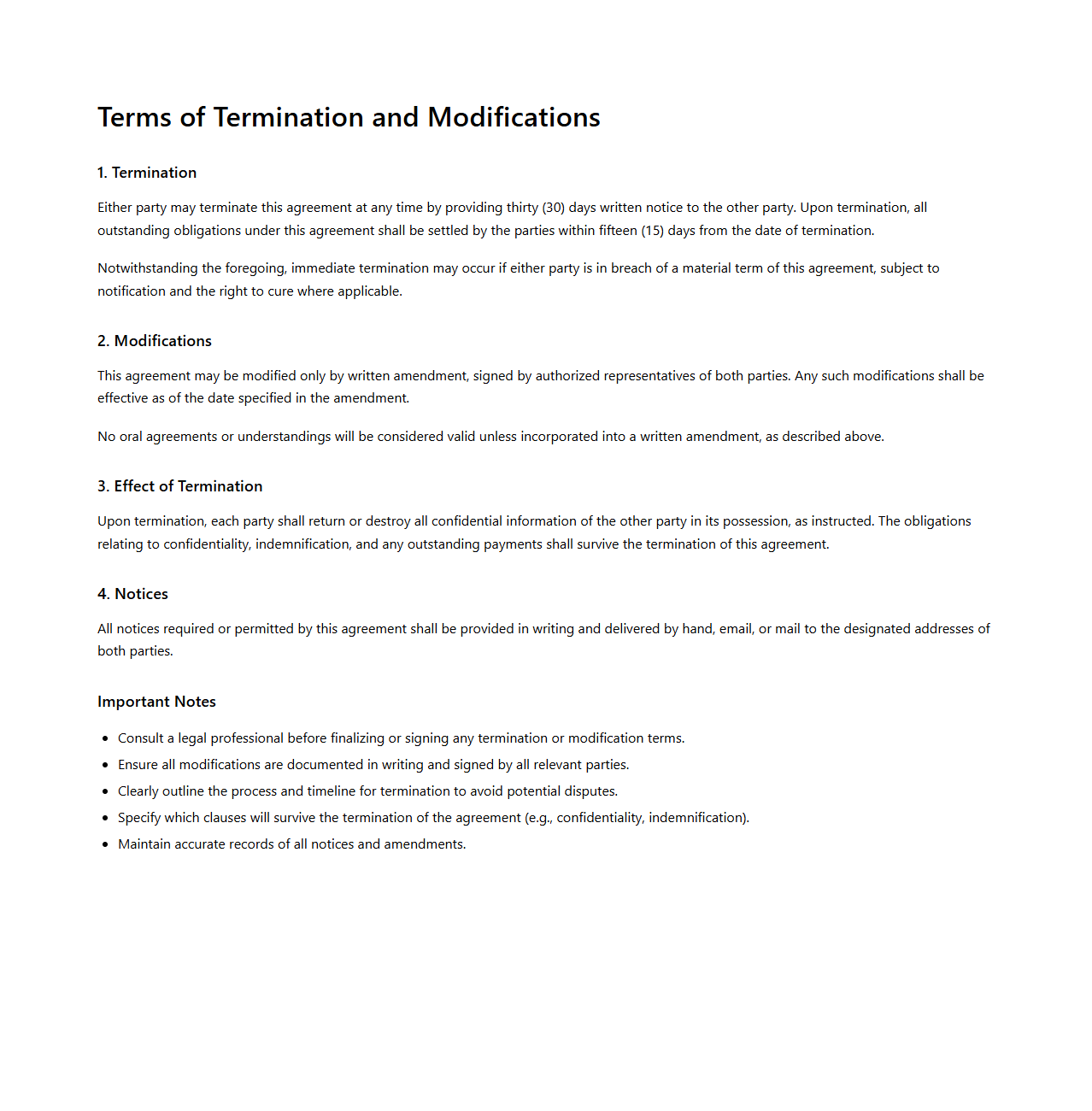

Terms of Termination and Modifications

The

Terms of Termination and Modifications document outlines the specific conditions under which a contract or agreement can be ended or altered. It provides clear guidelines on the processes, notice periods, and obligations required from all parties involved to ensure lawful and orderly termination or changes. This document safeguards the rights and responsibilities of each party, minimizing potential disputes during contract dissolution or amendment.

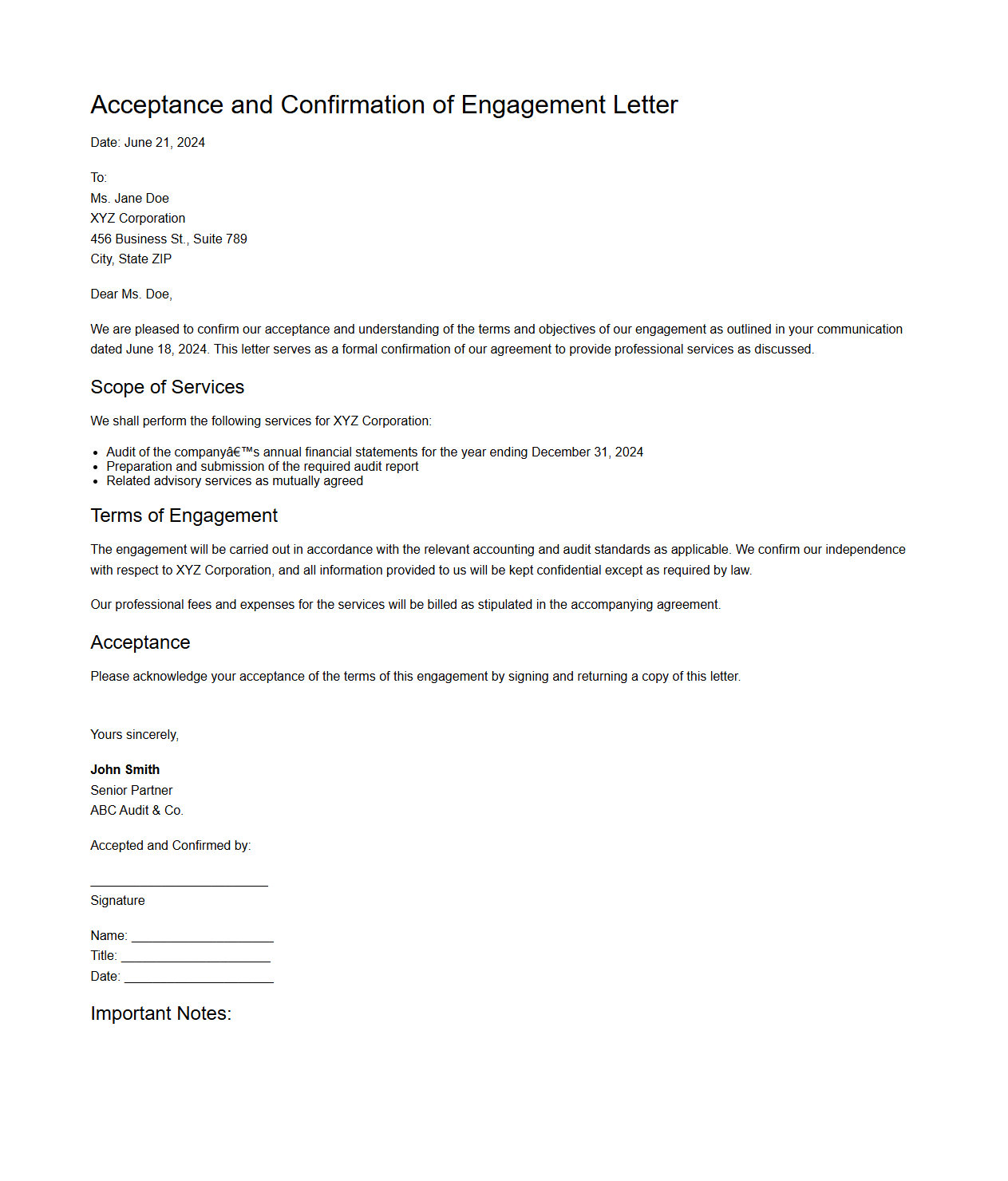

Acceptance and Confirmation of Engagement Letter

An

Acceptance and Confirmation of Engagement Letter is a formal document that signifies a client's agreement to the terms and conditions outlined by a service provider, typically in professional services such as legal, accounting, or consulting. This document ensures mutual understanding of the scope, fees, responsibilities, and timelines associated with the engagement. It acts as a binding agreement that protects both parties by clarifying expectations and reducing the risk of disputes during the service delivery.

What key clauses must be included in the engagement letter for statutory audit compliance?

The engagement letter for statutory audit compliance must include clauses outlining the purpose and objectives of the audit. It should specify the auditor's responsibilities and the client's obligations clearly to avoid misunderstandings. Additionally, clauses on the scope of work, limitation of liability, and fee arrangements are essential for compliance and transparency.

How should the scope of statutory audit services be articulated in the engagement letter format?

The scope of statutory audit services should be detailed precisely to define the extent and boundaries of the audit work. It must mention the financial statements to be audited and reference relevant auditing standards. Clear articulation ensures both parties understand what services are included, minimizing the risk of disputes.

What standard terms define the auditor's and client's responsibilities in a statutory audit letter?

The auditor's responsibilities typically include conducting the audit in accordance with applicable standards and exercising professional judgment and skepticism. The client is responsible for providing access to records, internal controls, and any necessary information. These terms establish mutual obligations critical for effective audit execution and compliance.

How is confidentiality addressed in the statutory audit engagement letter template?

Confidentiality clauses ensure that all audit information remains protected and undisclosed to unauthorized parties. The engagement letter should state that the auditor will maintain confidentiality except as required by law or professional standards. This safeguards client information and reinforces trust between auditor and client.

Are there recommended formatting best practices for the statutory audit engagement letter under local regulations?

Formatting best practices typically include a clear, professional layout with headings, numbered clauses, and logical flow for readability. Using formal language and including signature blocks for both parties enhances legal validity. Compliance with local regulations may also require including specific disclosures or disclaimers consistent with statutory requirements.