The Format of Net Profit Statement for Annual Accounts typically includes gross profit, operating expenses, and other incomes or losses to calculate the net profit or loss for the financial year. It begins with the total revenue, subtracts the cost of goods sold to derive gross profit, followed by listing all administrative and selling expenses. The statement concludes by adding non-operating incomes and deducting taxes to present the final net profit or loss, ensuring transparency and compliance with accounting standards.

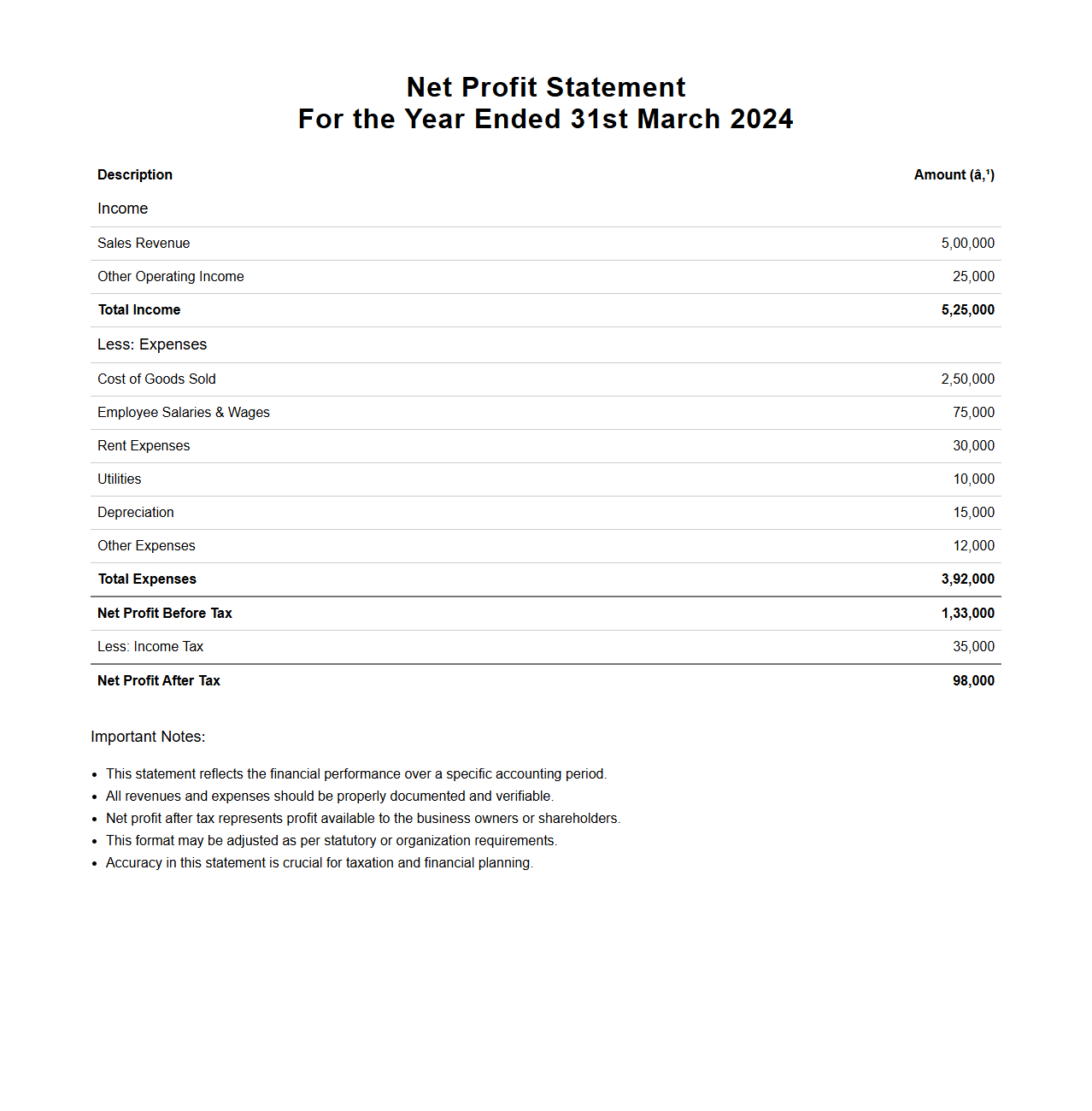

Standard Net Profit Statement Format

The

Standard Net Profit Statement Format document outlines a systematic approach to presenting a company's revenues, expenses, and net profit over a specific period. It includes key components such as gross income, operating costs, taxes, and other deductions, providing a clear snapshot of financial performance. This format is crucial for accurate financial analysis, compliance, and decision-making processes.

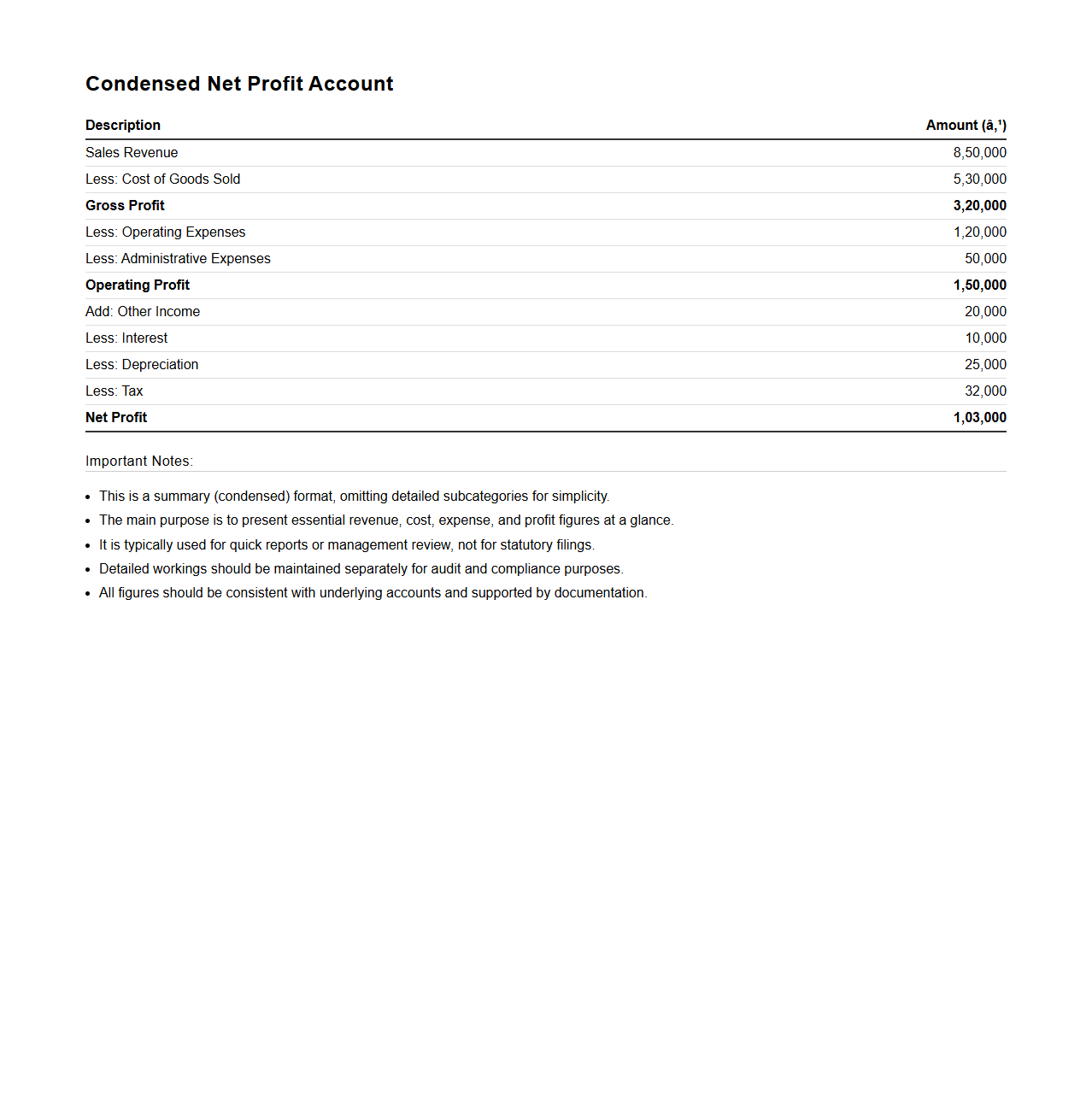

Condensed Net Profit Account Format

The

Condensed Net Profit Account Format document provides a streamlined summary of a company's profitability by detailing key revenue and expense items, resulting in the net profit or loss for a specific period. This format focuses on essential financial data, making it easier for stakeholders to assess operational efficiency and financial health without extensive line-by-line details. It serves as a critical tool for management, investors, and analysts to quickly evaluate business performance and make informed decisions.

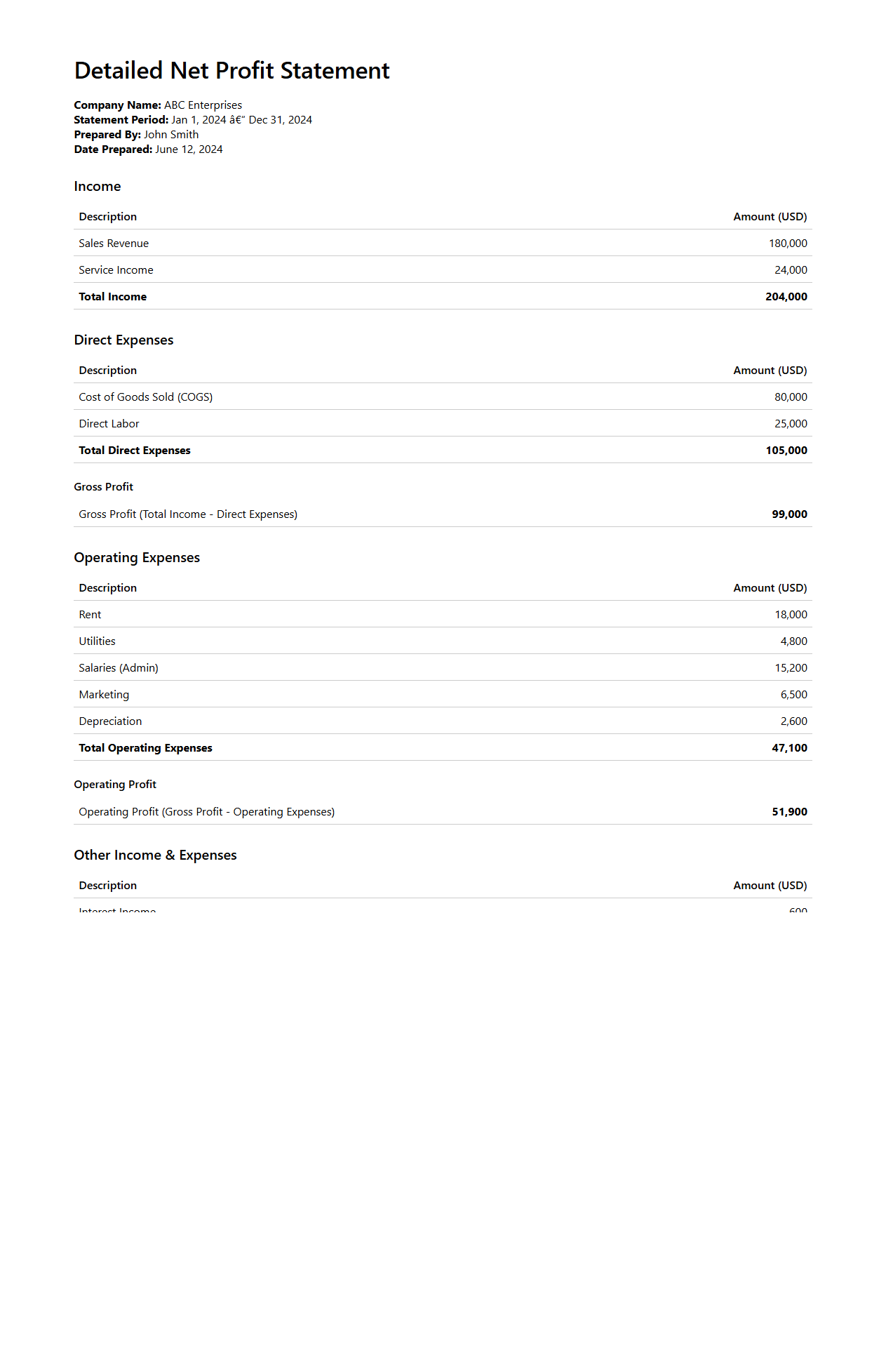

Detailed Net Profit Statement Format

A

Detailed Net Profit Statement Format document provides a comprehensive breakdown of revenues, cost of goods sold, operating expenses, and other income to accurately calculate net profit for a specific period. This format aids businesses in evaluating financial performance by highlighting key profit drivers and expense categories. Clear presentation of these financial metrics supports strategic decision-making and financial analysis.

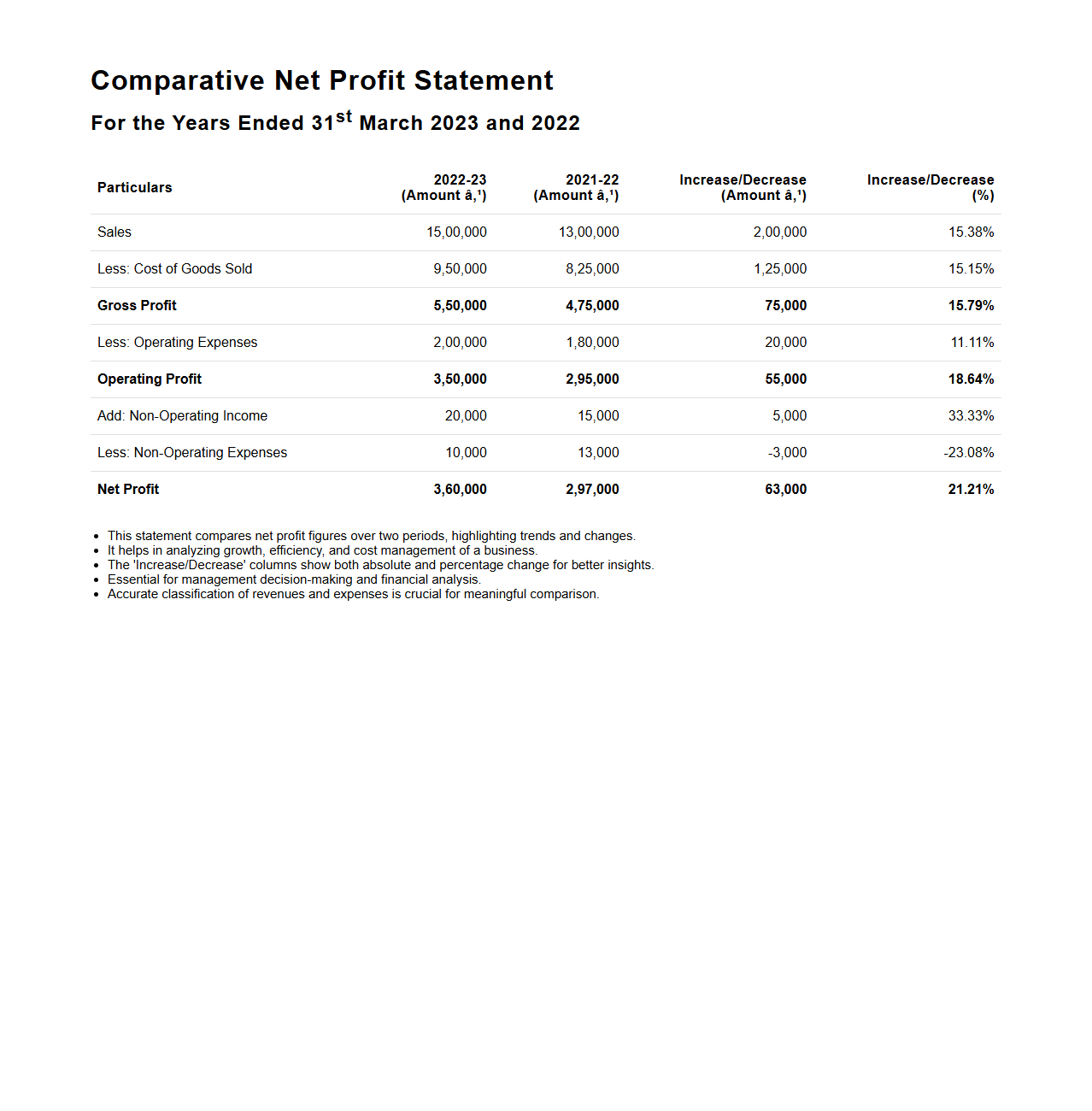

Comparative Net Profit Statement Format

A

Comparative Net Profit Statement Format document presents a side-by-side financial overview of net profits across multiple periods, facilitating performance analysis and trend identification. It highlights revenues, expenses, and net profit figures for each period, enabling businesses to evaluate financial health and make informed decisions. This format supports efficient comparison and aids in strategic planning by providing clear visibility into profit fluctuations.

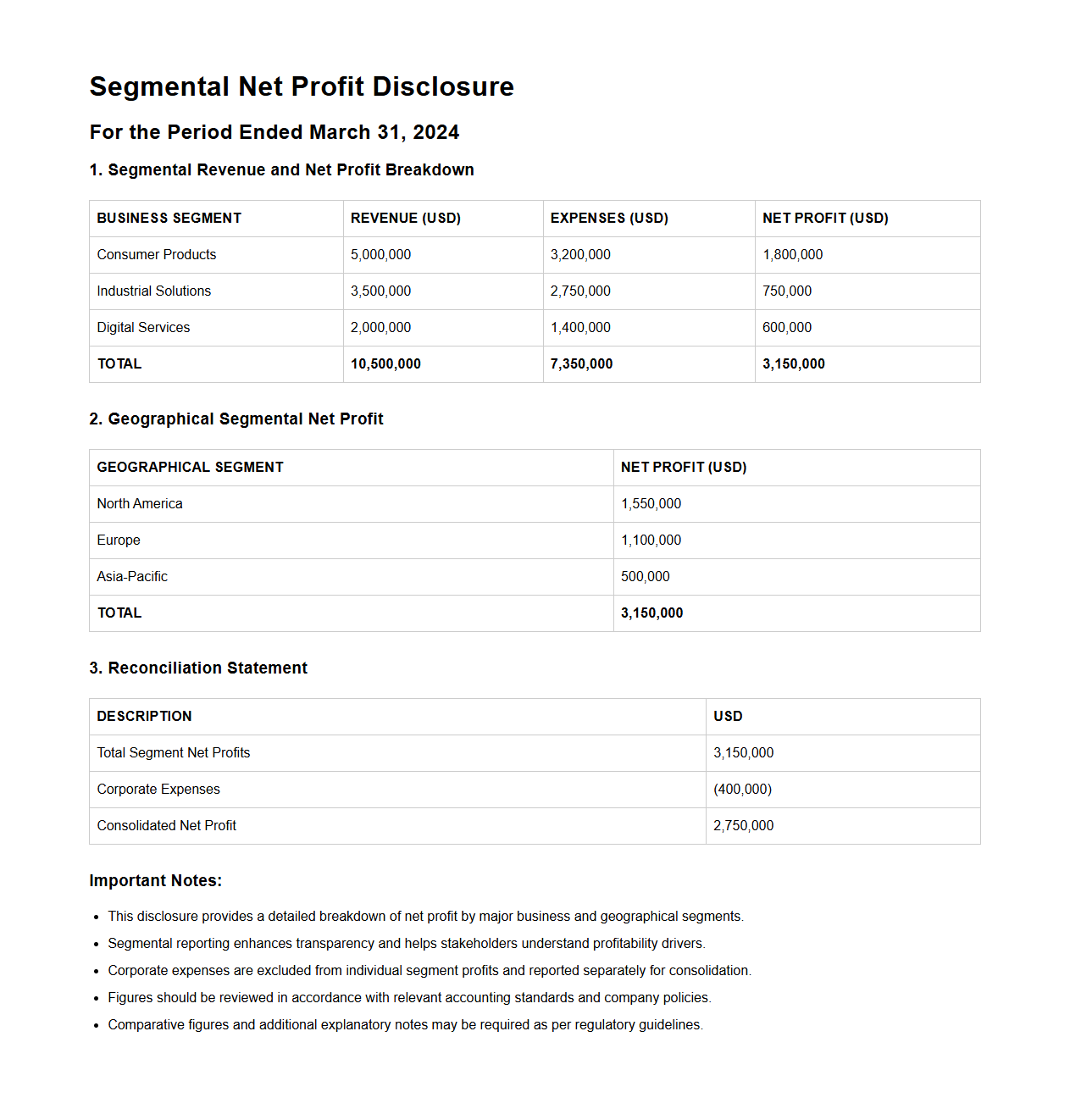

Segmental Net Profit Disclosure Format

The

Segmental Net Profit Disclosure Format document is a structured financial report that provides detailed insights into the profitability of different business segments within a company. It breaks down net profit figures by geographic regions, product lines, or business units, enabling stakeholders to assess performance variations and make informed strategic decisions. This format ensures compliance with accounting standards and enhances transparency in corporate financial disclosures.

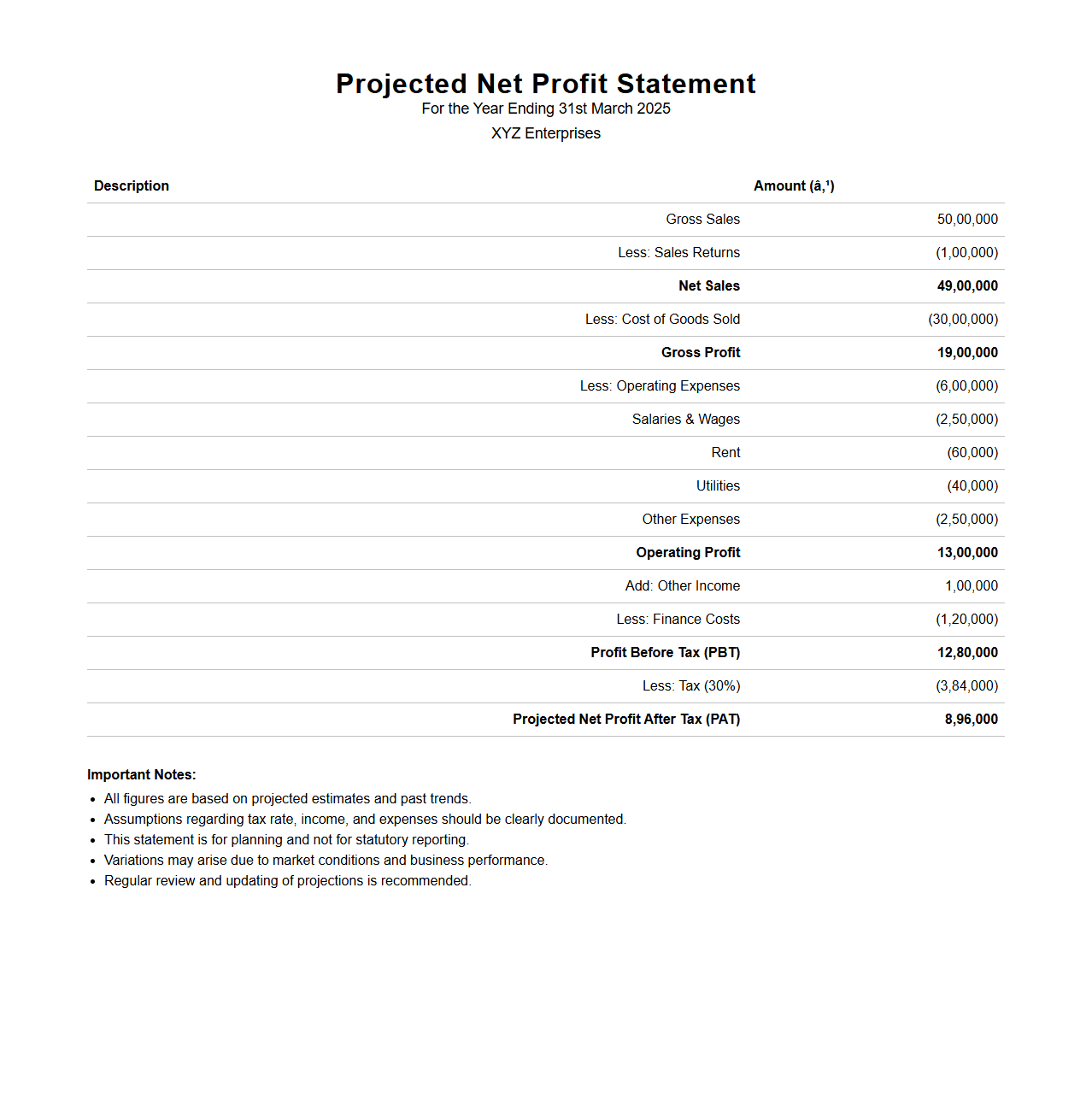

Projected Net Profit Statement Format

The

Projected Net Profit Statement Format document outlines the estimated financial performance of a business over a specific future period, detailing anticipated revenues, costs, and expenses to calculate net profit. It serves as a crucial tool for forecasting profitability, guiding budgeting decisions, and attracting investors by presenting expected financial outcomes. This format typically includes sections for sales projections, cost of goods sold, operating expenses, and net profit calculation, enabling clear financial planning and analysis.

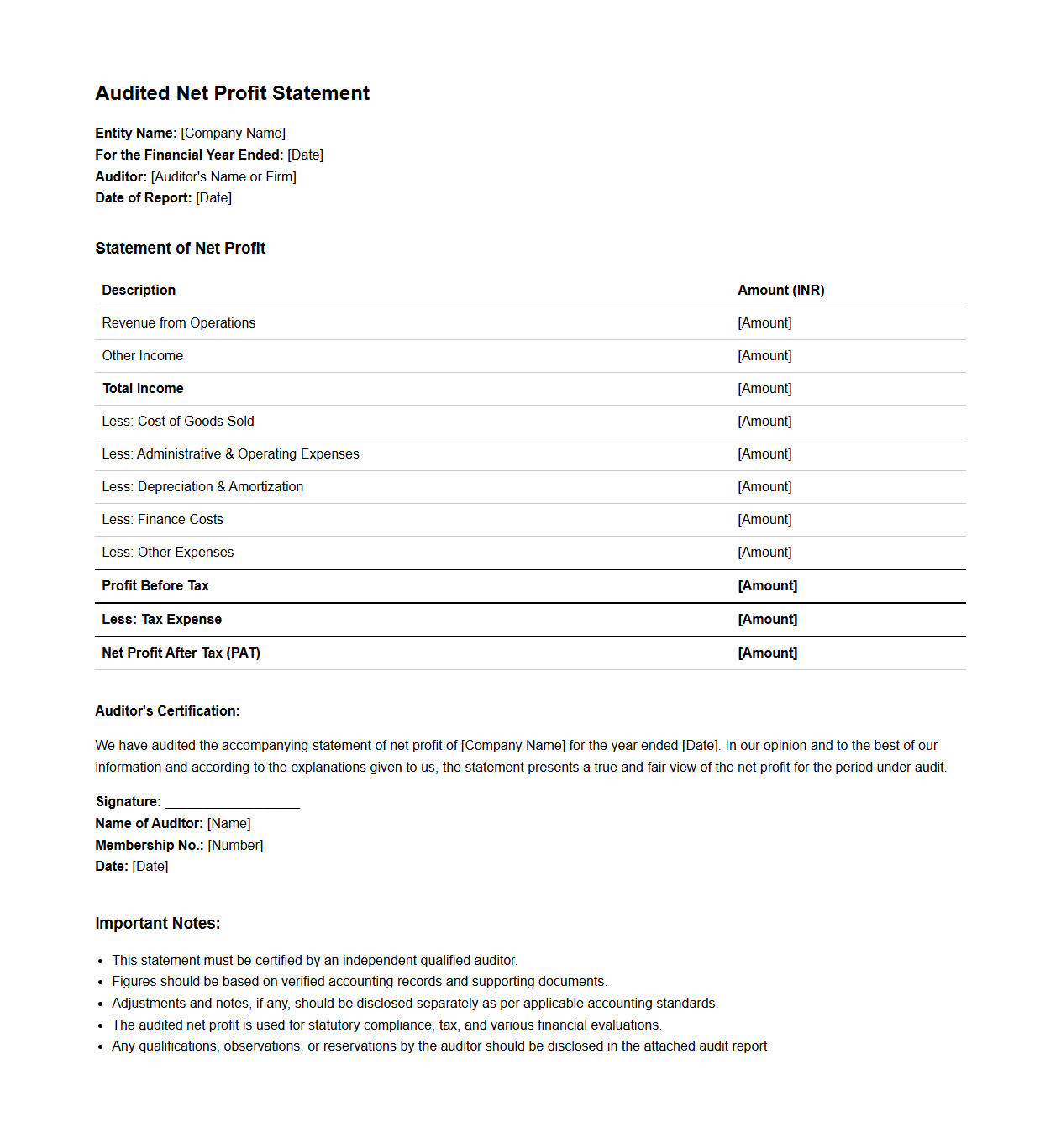

Audited Net Profit Statement Format

The

Audited Net Profit Statement Format document is a standardized financial report that presents a company's net profit after thorough examination by an independent auditor. It includes detailed revenue, expense, and tax data to ensure accuracy and compliance with accounting standards. This format is essential for stakeholders to assess the true financial performance and profitability of a business.

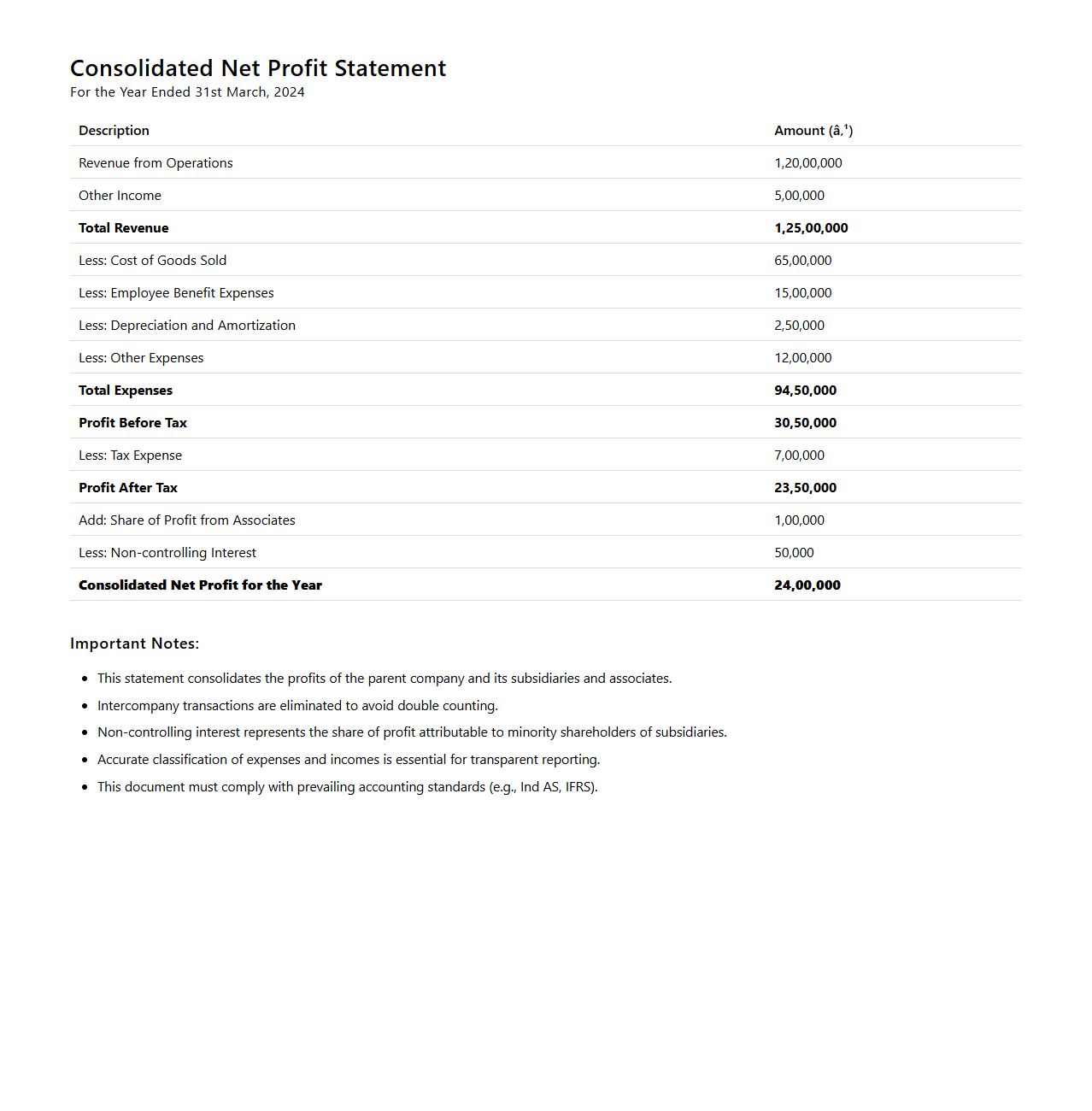

Consolidated Net Profit Statement Format

A

Consolidated Net Profit Statement Format document presents the combined net profit figures of a parent company and its subsidiaries, reflecting overall financial performance. It includes detailed revenue, expenses, and net profit calculations, ensuring accuracy and compliance with accounting standards such as IFRS or GAAP. This format is essential for stakeholders to assess the profitability and operational efficiency of the entire corporate group.

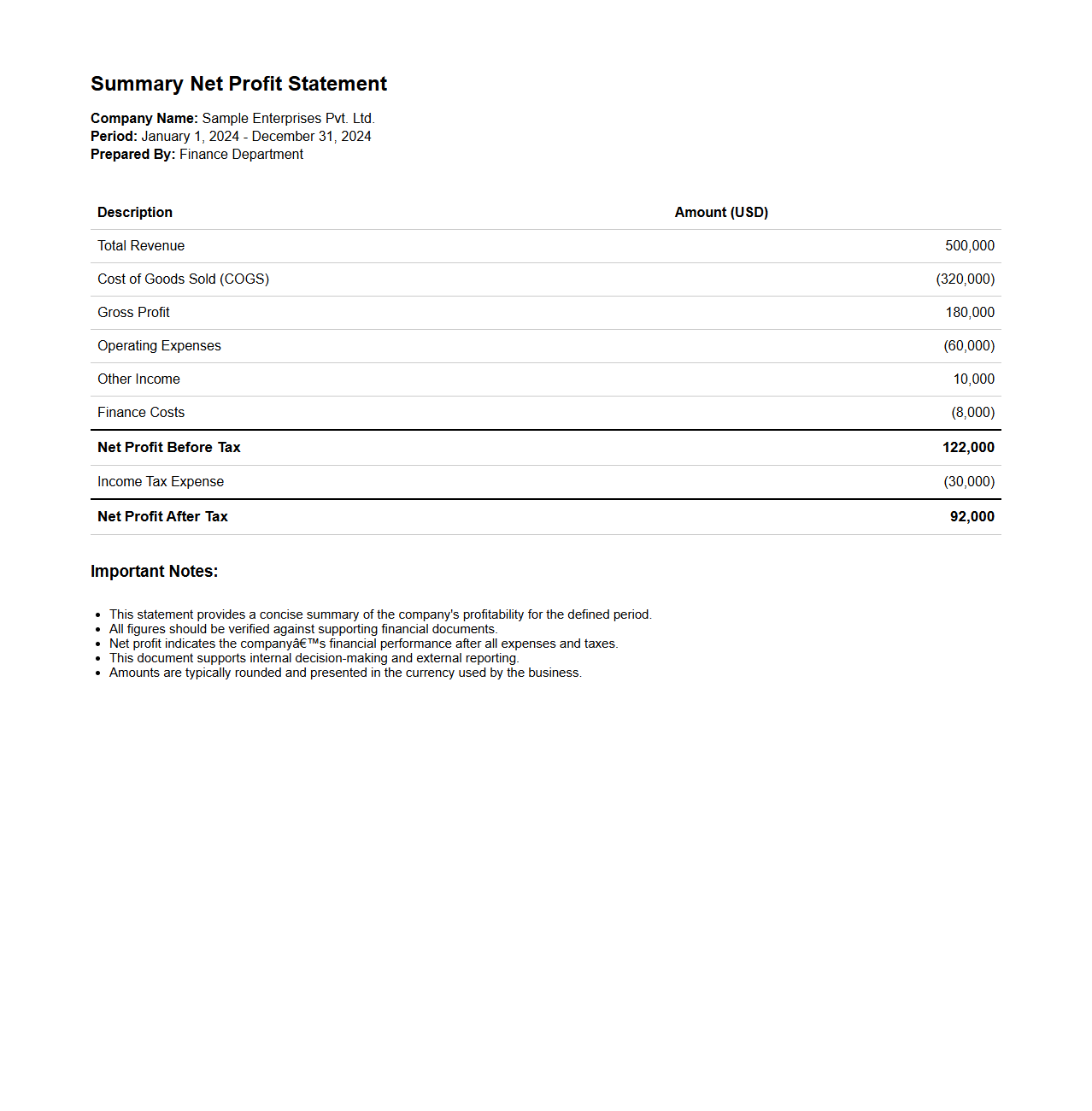

Summary Net Profit Statement Format

The

Summary Net Profit Statement Format document provides a clear outline of a company's net profit by summarizing total revenues and deducting total expenses within a specific accounting period. This format highlights key financial metrics such as gross profit, operating expenses, taxes, and net income, allowing for quick profitability analysis. It serves as an essential tool for stakeholders to assess financial performance and make informed business decisions.

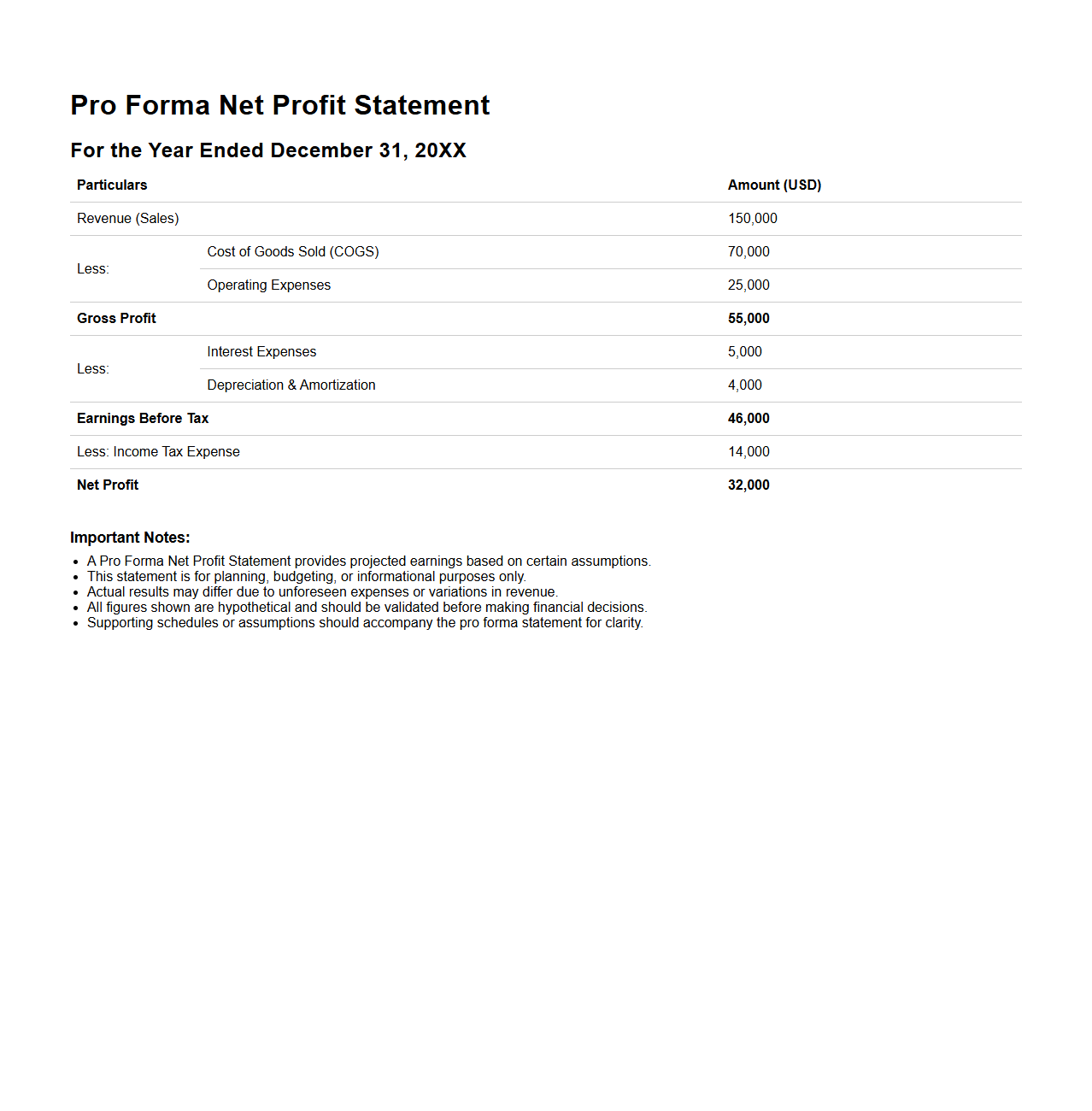

Pro Forma Net Profit Statement Format

A

Pro Forma Net Profit Statement Format document outlines projected profitability by estimating future revenues, expenses, and net profit for a specific period. It serves as a financial planning tool enabling businesses to forecast earnings, assess financial health, and support strategic decision-making. This format typically includes sections for sales, cost of goods sold, operating expenses, and calculates net profit to provide a clear view of expected financial performance.

What are the key components included in the Net Profit Statement format for annual accounts?

The Net Profit Statement format typically includes revenue, cost of goods sold, gross profit, operating expenses, and other income or expenses. It clearly outlines the total income generated and all deductions necessary to arrive at net profit. Additionally, it highlights interest and tax expenses to determine the final net profit for the period.

How is gross profit differentiated from net profit in the statement format?

Gross profit is calculated by subtracting the cost of goods sold from total revenue, reflecting the profitability from core operations. On the other hand, net profit accounts for all operating expenses, taxes, and extraordinary items in addition to gross profit. This distinction helps stakeholders understand operational efficiency versus overall profitability.

Which standard adjustments must be made to revenue and expenses in the annual Net Profit Statement?

Standard adjustments include the accrual of unpaid expenses and recognition of earned but unreceived revenues to comply with accrual accounting. Depreciation and amortization expenses must be expensed systematically to reflect asset usage. These adjustments ensure the reported net profit accurately represents the financial performance of the period.

How are extraordinary items and taxes presented and calculated in the Net Profit Statement format?

Extraordinary items are presented separately below operating profit to distinguish unusual gains or losses from regular business activities. Tax expenses are calculated on taxable income, which includes operational profit adjusted for extraordinary items. The clear segregation enhances transparency in the profit calculation process.

What layout and sequencing are required by accounting standards for the Net Profit section in annual accounts?

Accounting standards require a logical sequencing starting from total revenue down to net profit, following a standardized format. Income and expenses must be grouped and presented consistently for comparability across periods. Clear labeling and subtotaling are mandated to enhance readability and compliance with financial reporting norms.