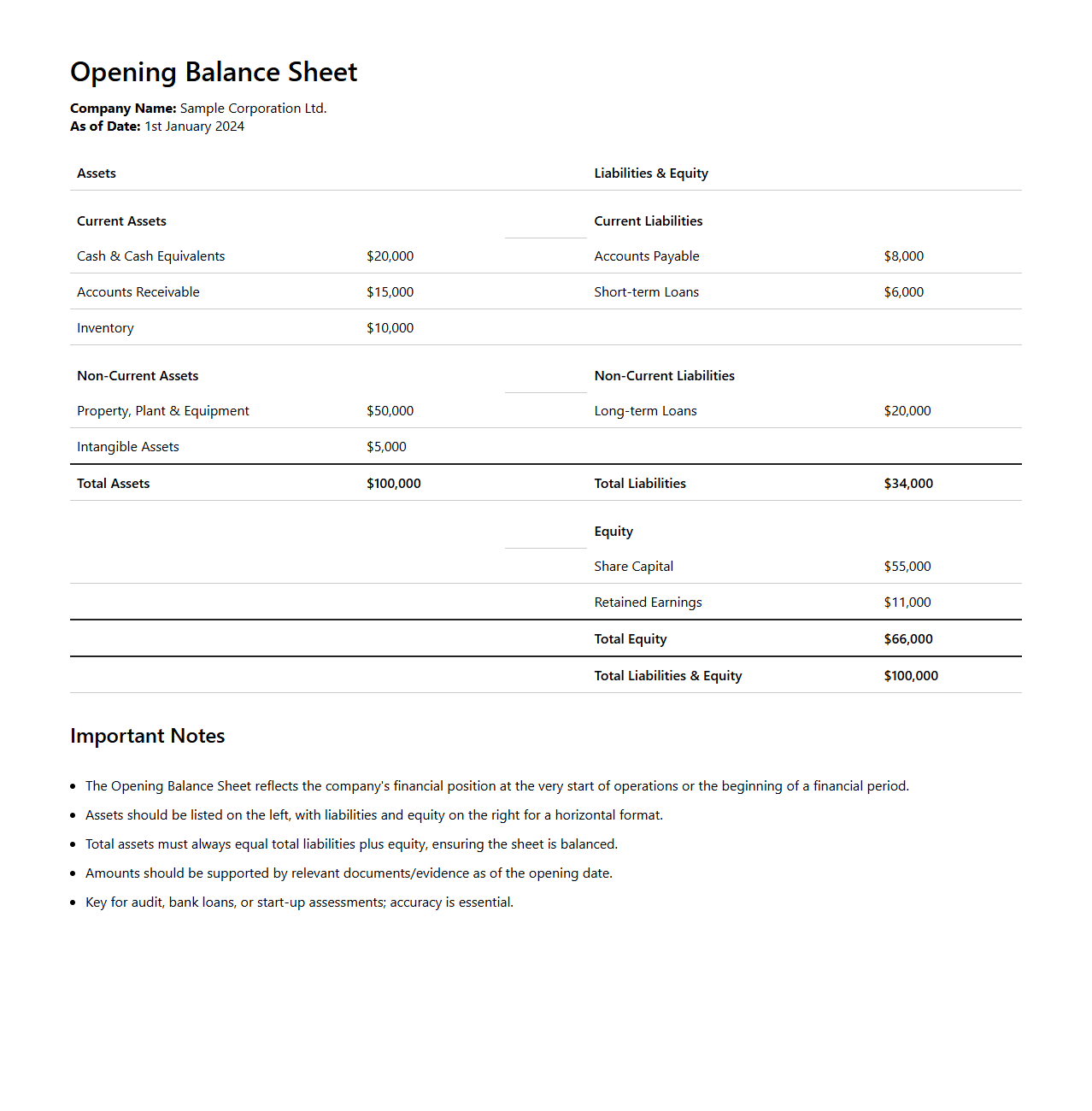

The format of the opening balance sheet for ledger includes a clear listing of all assets, liabilities, and owner's equity at the start of an accounting period. It serves as a foundational document to ensure accurate ledger entries and proper financial tracking. Accurate presentation of the opening balances supports consistent ledger management and financial reporting.

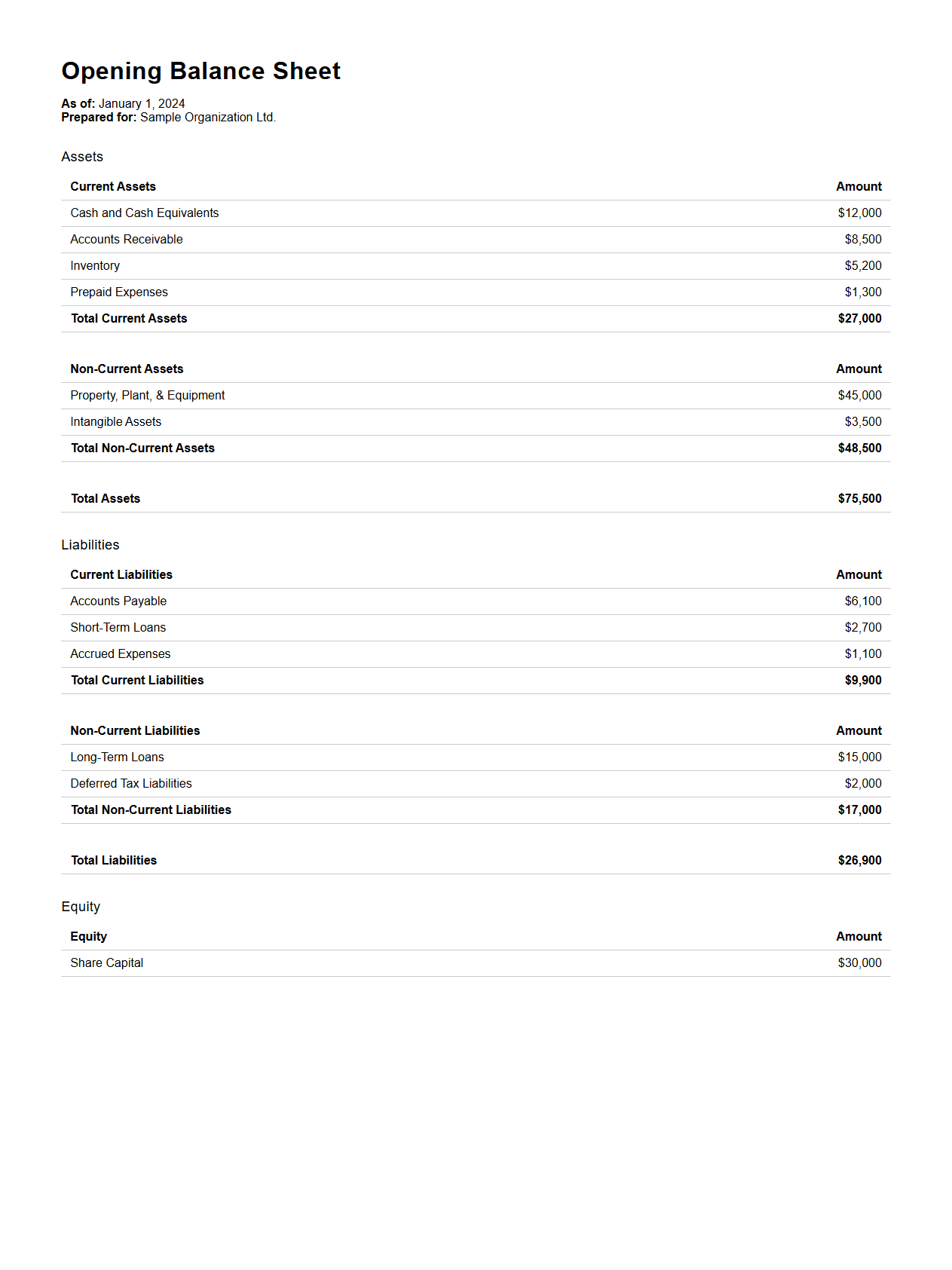

Standard Opening Balance Sheet Template

A

Standard Opening Balance Sheet Template document is a financial statement used to record a company's assets, liabilities, and equity at the start of a new accounting period. It helps businesses establish a clear financial position by listing all opening balances systematically, ensuring consistency and accuracy in bookkeeping. This template serves as a foundational tool for managing financial records and preparing subsequent financial statements.

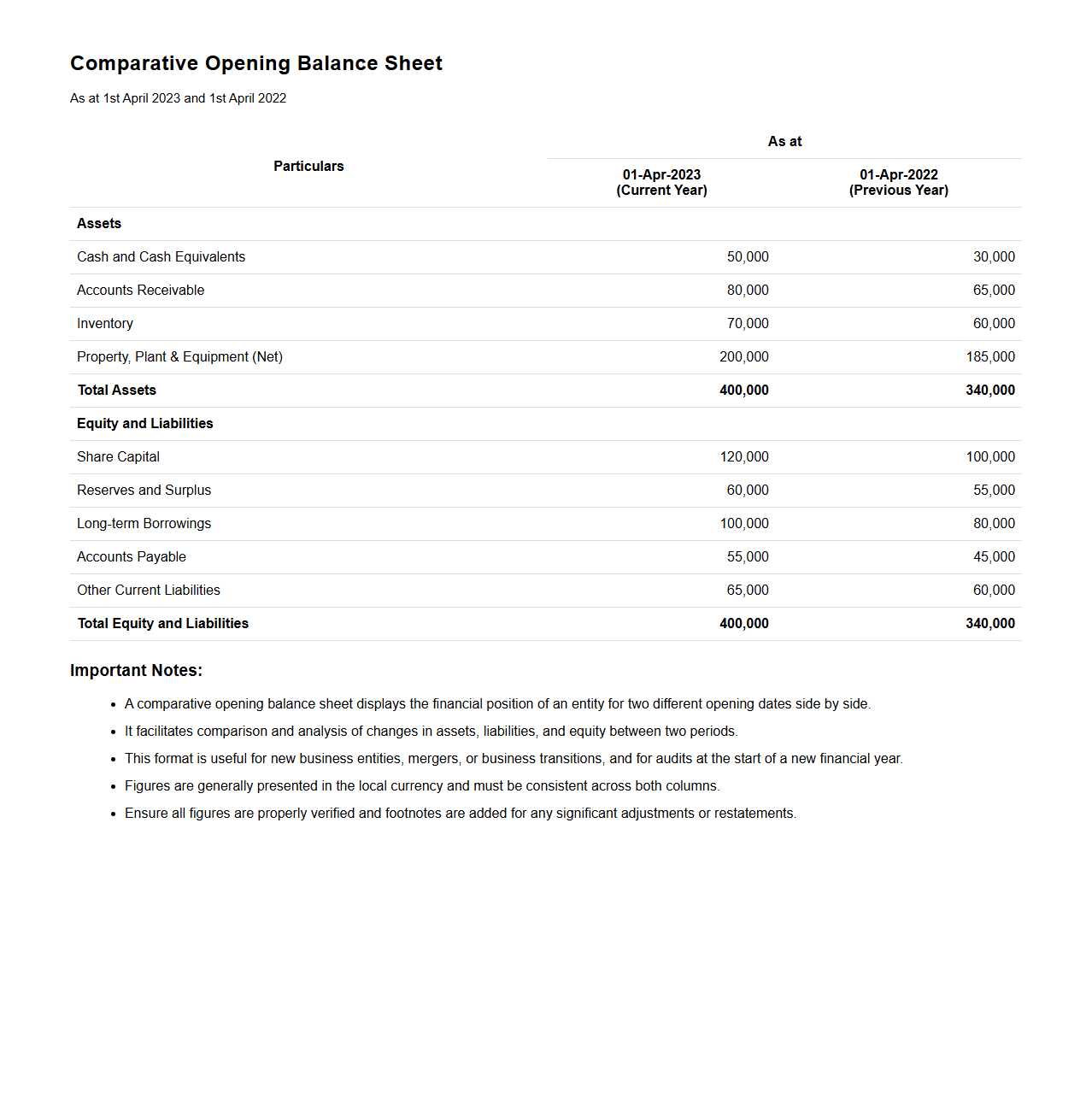

Comparative Opening Balance Sheet Format

The

Comparative Opening Balance Sheet Format document presents financial statements side-by-side, showing the opening balances of assets, liabilities, and equity for multiple periods. This format allows stakeholders to easily analyze changes and trends in financial positions over time. It is essential for auditors, accountants, and business managers to assess consistency and accuracy in financial reporting during transitions between accounting periods.

Multi-Column Opening Balance Sheet

A

Multi-Column Opening Balance Sheet document organizes financial data into multiple columns to present the opening balances of assets, liabilities, and equity accounts clearly. It allows businesses to compare various periods or accounts side-by-side, enhancing financial analysis and accuracy during the accounting period transition. This format supports streamlined data entry and improved visibility of financial positions at the start of the fiscal year.

Vertical Opening Balance Sheet Layout

The

Vertical Opening Balance Sheet Layout document organizes assets, liabilities, and equity in a single column format, facilitating clear and straightforward financial analysis. This layout enhances readability by presenting financial data from top to bottom, enabling easier comparison of account balances at the start of an accounting period. It is essential for maintaining accurate records and supports seamless integration with accounting systems.

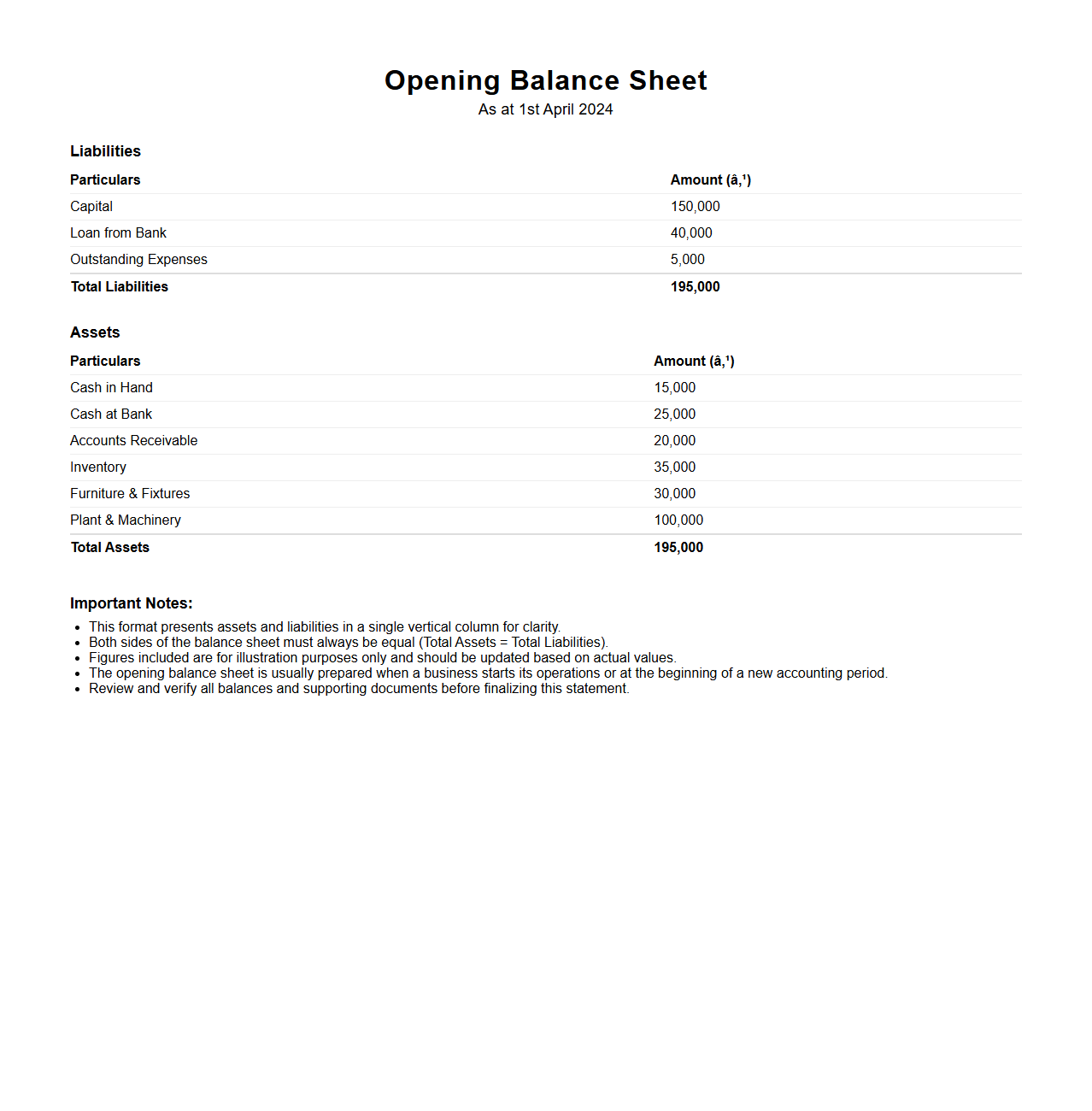

Horizontal Opening Balance Sheet Design

A

Horizontal Opening Balance Sheet Design document outlines the structured format for presenting financial position data, displaying assets, liabilities, and equity side-by-side in a horizontal layout. This design improves clarity by enabling easy comparison across different financial categories and periods, helping stakeholders quickly assess organizational financial health. It serves as a foundational blueprint for standardizing balance sheet presentation within accounting systems and reporting tools.

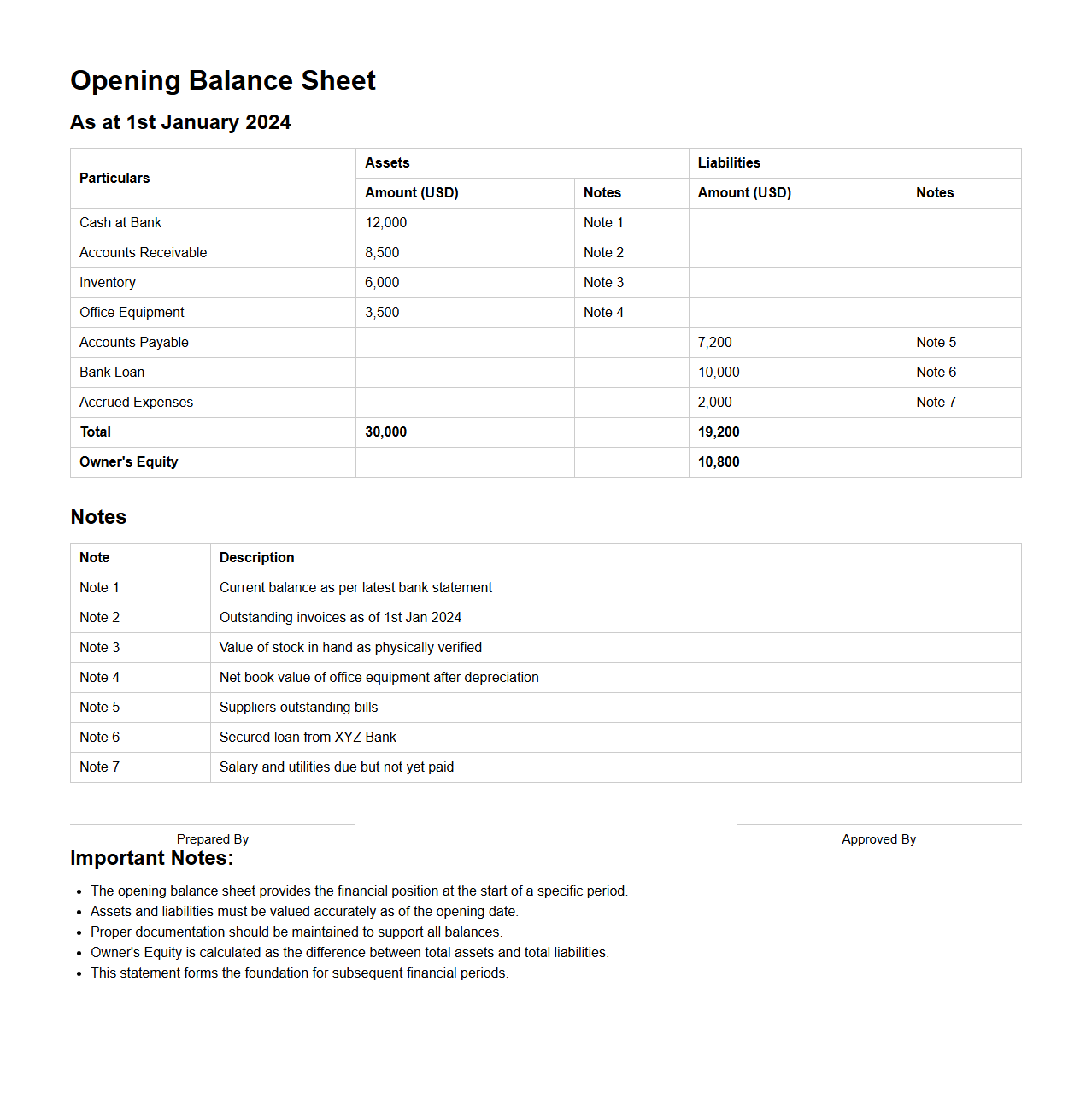

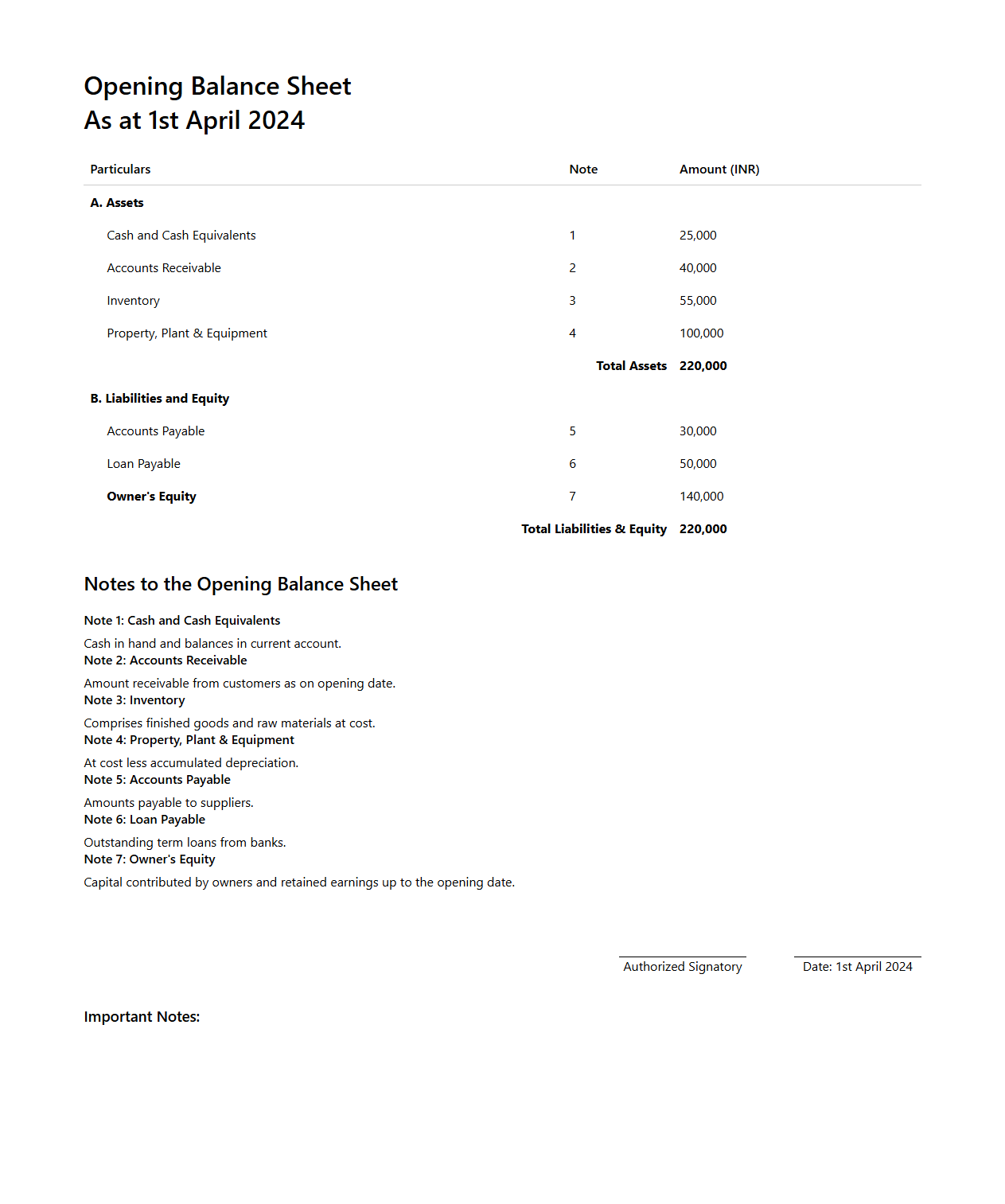

Opening Balance Sheet with Notes Format

An

Opening Balance Sheet with Notes Format document provides a detailed snapshot of a company's financial position at the beginning of an accounting period. It lists all assets, liabilities, and equity accounts with corresponding opening balances, accompanied by explanatory notes that clarify accounting policies, assumptions, and significant transactions. This format ensures transparency and facilitates accurate financial analysis and auditing for stakeholders.

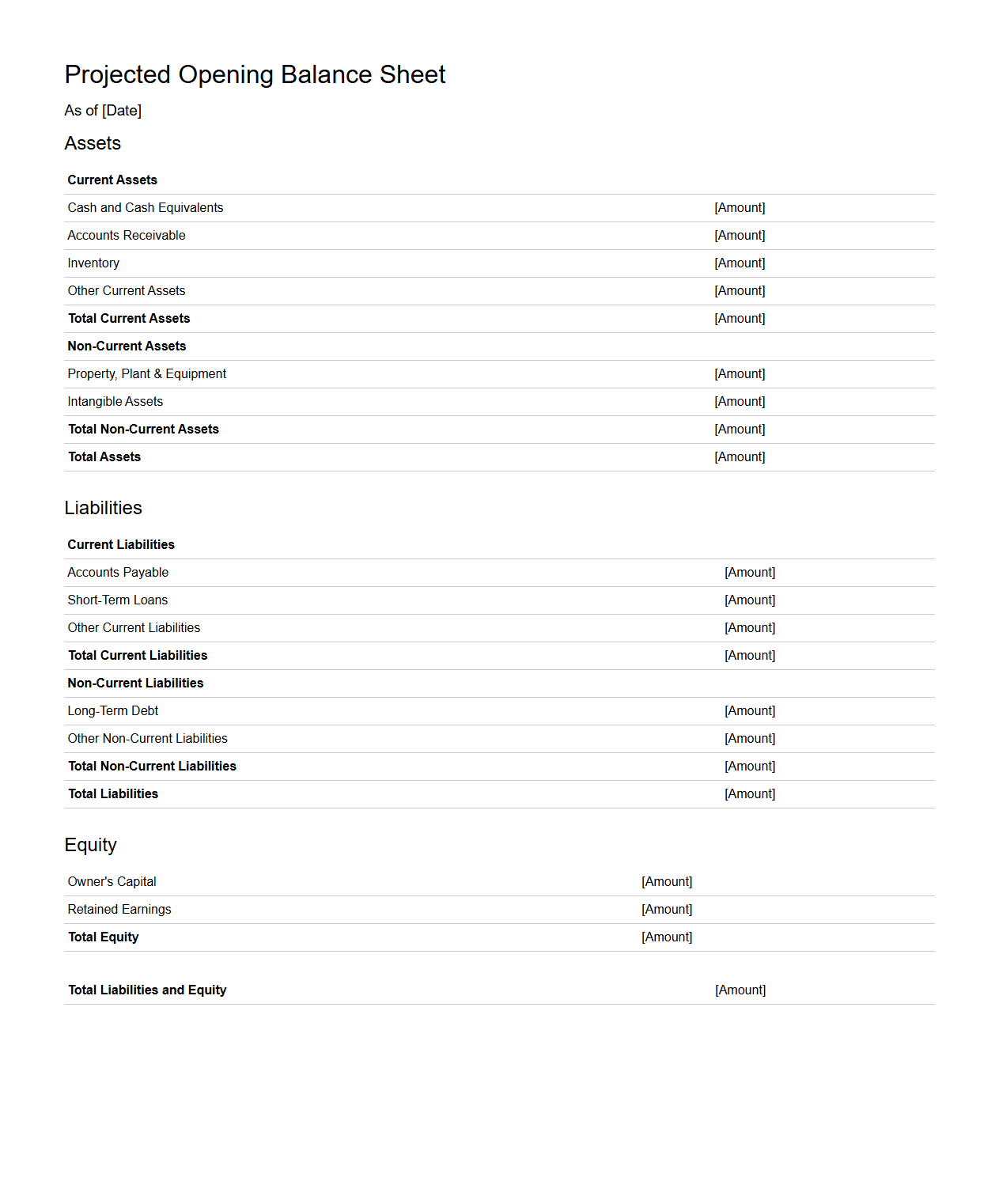

Projected Opening Balance Sheet Template

A

Projected Opening Balance Sheet Template document is a financial tool used to estimate the starting financial position of a business at the beginning of a new accounting period. It outlines anticipated assets, liabilities, and equity based on forecasts, helping organizations plan and make informed decisions. This template facilitates accurate budgeting, financial analysis, and strategic planning by presenting a clear snapshot of expected financial status.

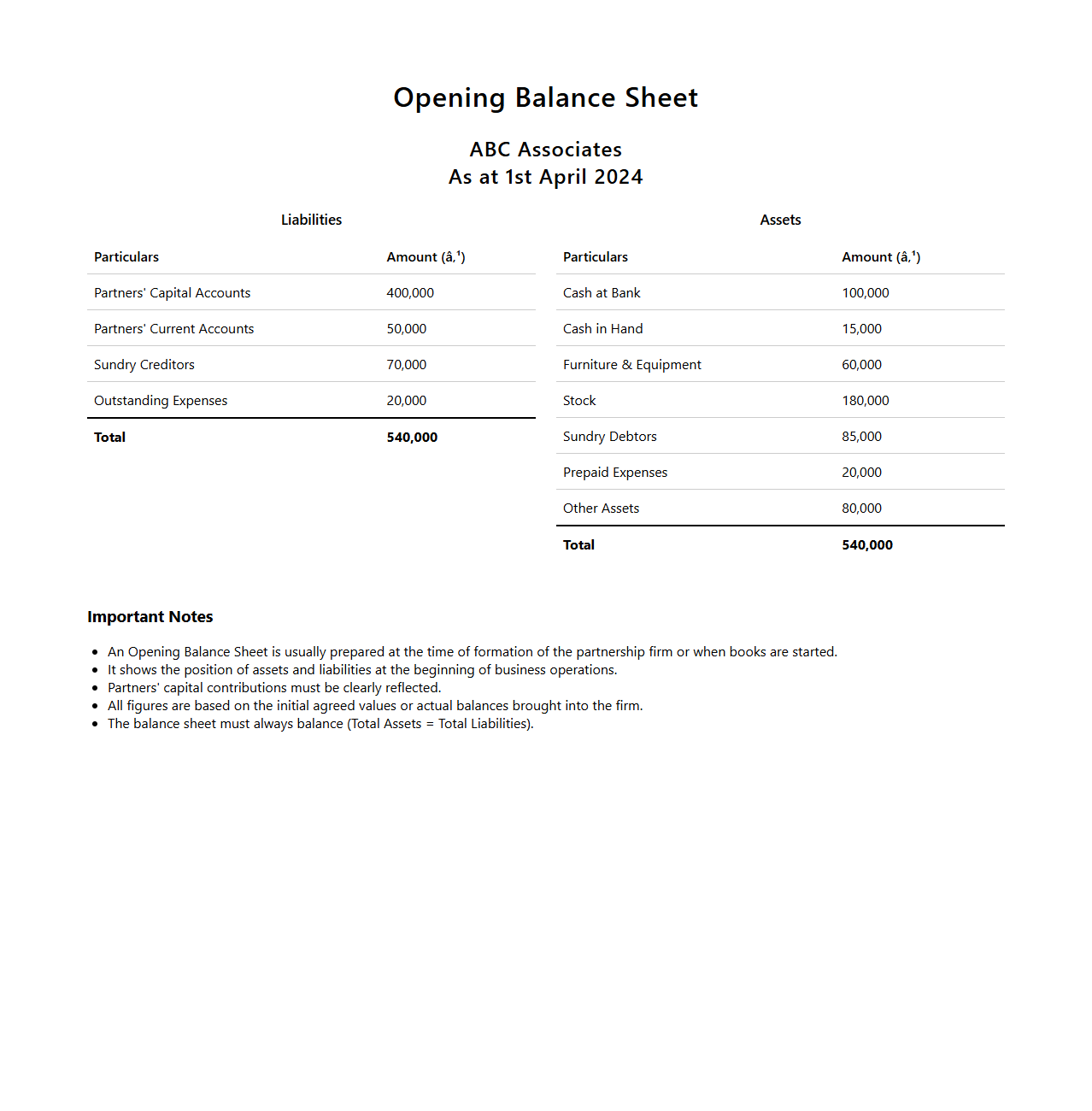

Opening Balance Sheet for Partnership Firm

The

Opening Balance Sheet for a partnership firm is a financial statement prepared at the inception of the partnership, detailing the assets, liabilities, and capital contributions of each partner. This document serves as a foundation for recording all future business transactions and is critical for determining each partner's equity in the firm. It helps in establishing transparency, accountability, and clarity regarding the initial financial position of the partnership.

Opening Balance Sheet for Sole Proprietorship

The

Opening Balance Sheet for a sole proprietorship is a financial statement that outlines the initial assets, liabilities, and owner's equity at the start of the business. This document serves as a baseline for tracking the business's financial progress and is essential for accurate bookkeeping and tax reporting. It provides a clear snapshot of the proprietor's investment and the company's financial position on the first day of operations.

Opening Balance Sheet in Excel Format

An

Opening Balance Sheet in Excel format is a structured financial document that records a company's assets, liabilities, and equity at the start of an accounting period. It serves as a foundational reference point for tracking financial progress and ensuring accurate accounting throughout the fiscal year. This Excel format allows for easy data entry, calculation automation, and customization to fit specific business needs.

What are the mandatory header elements in an opening balance sheet format for a ledger?

The mandatory header elements in an opening balance sheet include the company name, the title "Opening Balance Sheet," and the date or effective period.

These headers provide clear identification and time reference for the financial statements, ensuring accurate record-keeping.

A well-structured header enhances clarity and helps in distinguishing the opening balances from subsequent financial data.

How should assets and liabilities be structured in the opening balance sheet layout?

The opening balance sheet should present assets on one side and liabilities plus equity on the other, maintaining the accounting equation.

Assets are typically divided into current and non-current categories to showcase liquidity and long-term investments.

Liabilities must also be classified as current and long-term to reflect repayment timelines accurately.

Which line items must be included to comply with standard accounting principles in ledgers?

Standard accounting principles require the inclusion of key line items such as cash, accounts receivable, inventory, fixed assets, accounts payable, and capital accounts.

Each line item should represent a separate ledger account to allow for detailed tracking of financial transactions.

Compliance ensures transparency and facilitates audit processes by aligning with generally accepted accounting standards.

What is the correct format for documenting opening balances for different account types?

The correct format involves noting debit balances for assets and expenses, and credit balances for liabilities, equity, and revenues.

Opening balances must be clearly stated in the ledger with proper account codes and descriptions for each account type.

Proper formatting ensures the accurate reflection of the company's financial position at the start of an accounting period.

How should prior period adjustments be reflected in the opening balance sheet for a ledger?

Prior period adjustments must be incorporated directly into the opening balances to correct any errors from previous periods.

These adjustments are typically recorded in a separate line item or account titled "Prior Period Adjustments" to maintain transparency.

Reflecting these adjustments accurately is crucial for reliable financial reporting and compliance with accounting standards.