The format of financial statements for capital typically includes a detailed presentation of equity components such as share capital, reserves, and retained earnings. It ensures transparency by clearly showing changes in capital structure and investor contributions over a specific period. Proper formatting aids stakeholders in assessing the financial health and stability of the company.

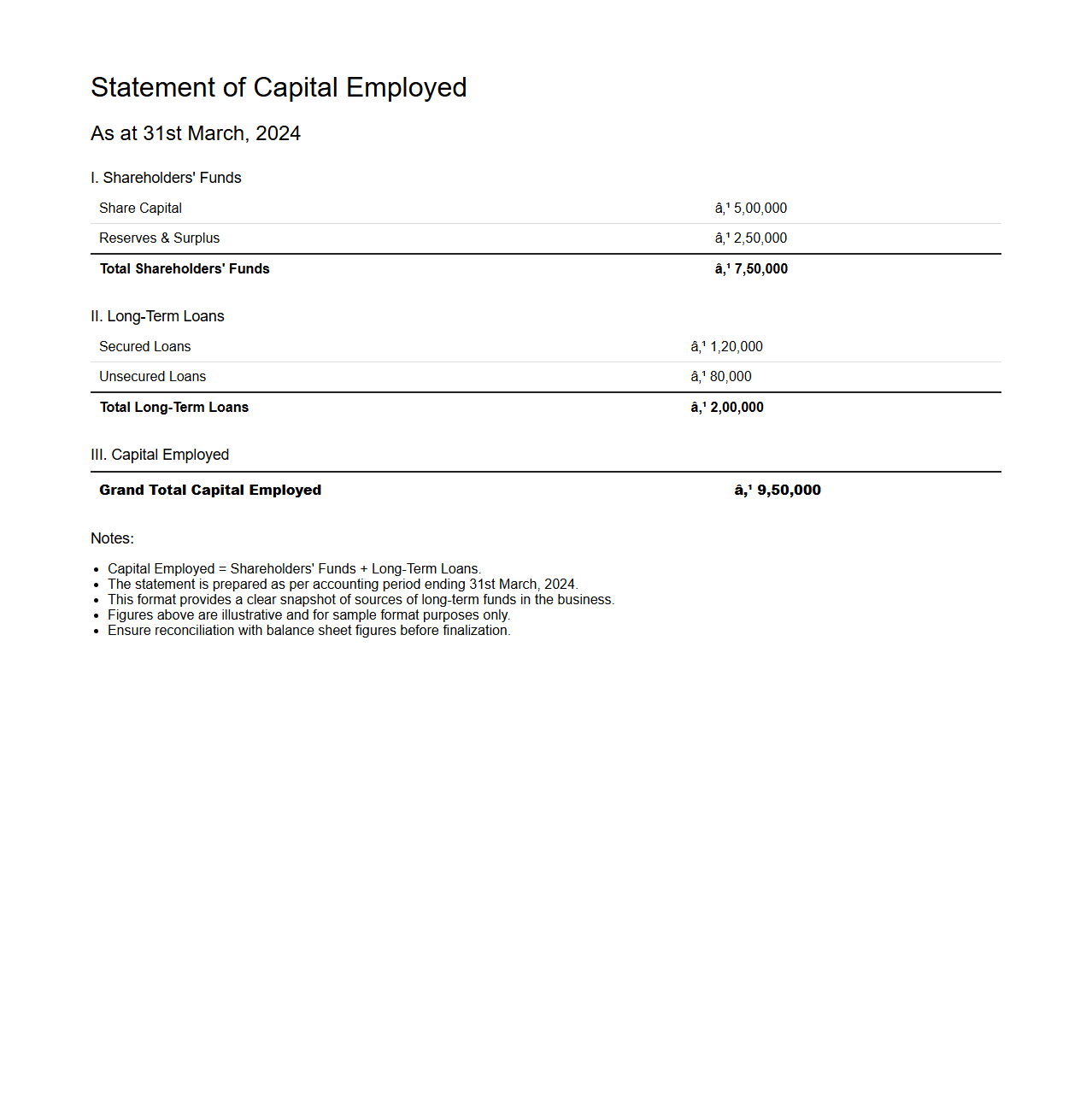

Statement of Capital Employed Format

The

Statement of Capital Employed Format document is a financial report outlining the total capital investment used in a business, highlighting long-term funds employed in operations. This statement provides a detailed breakdown of equity share capital, reserves, and long-term liabilities, allowing stakeholders to assess the company's financial structure. It is essential for analyzing the efficiency of capital utilization and the overall financial health of the organization.

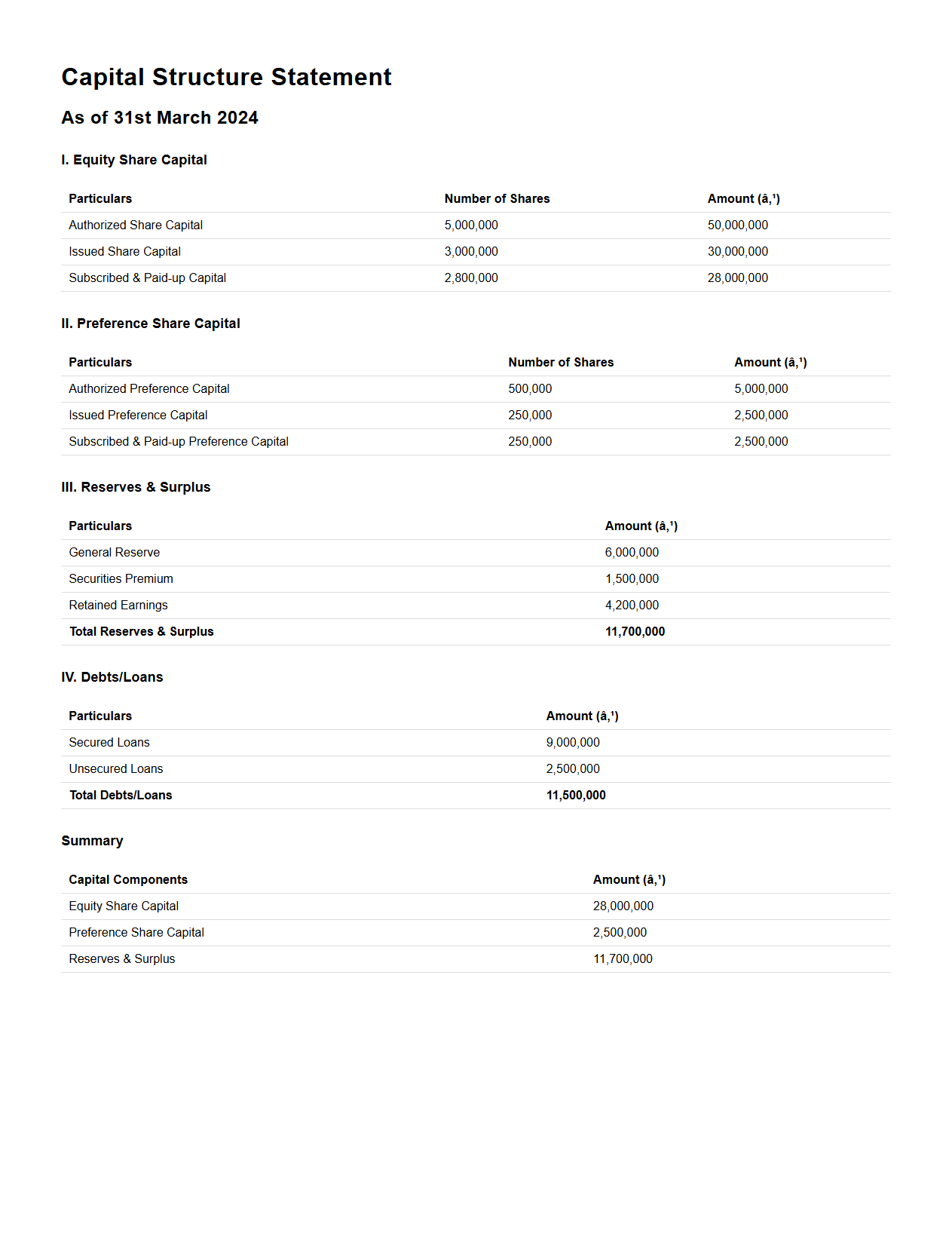

Capital Structure Statement Format

A

Capital Structure Statement Format document outlines the detailed composition of a company's equity and debt, providing a clear view of the financial framework supporting business operations. It typically includes information on share capital, reserves, retained earnings, long-term liabilities, and other sources of finance. This format aids stakeholders in analyzing the company's financial stability and planning future growth strategies.

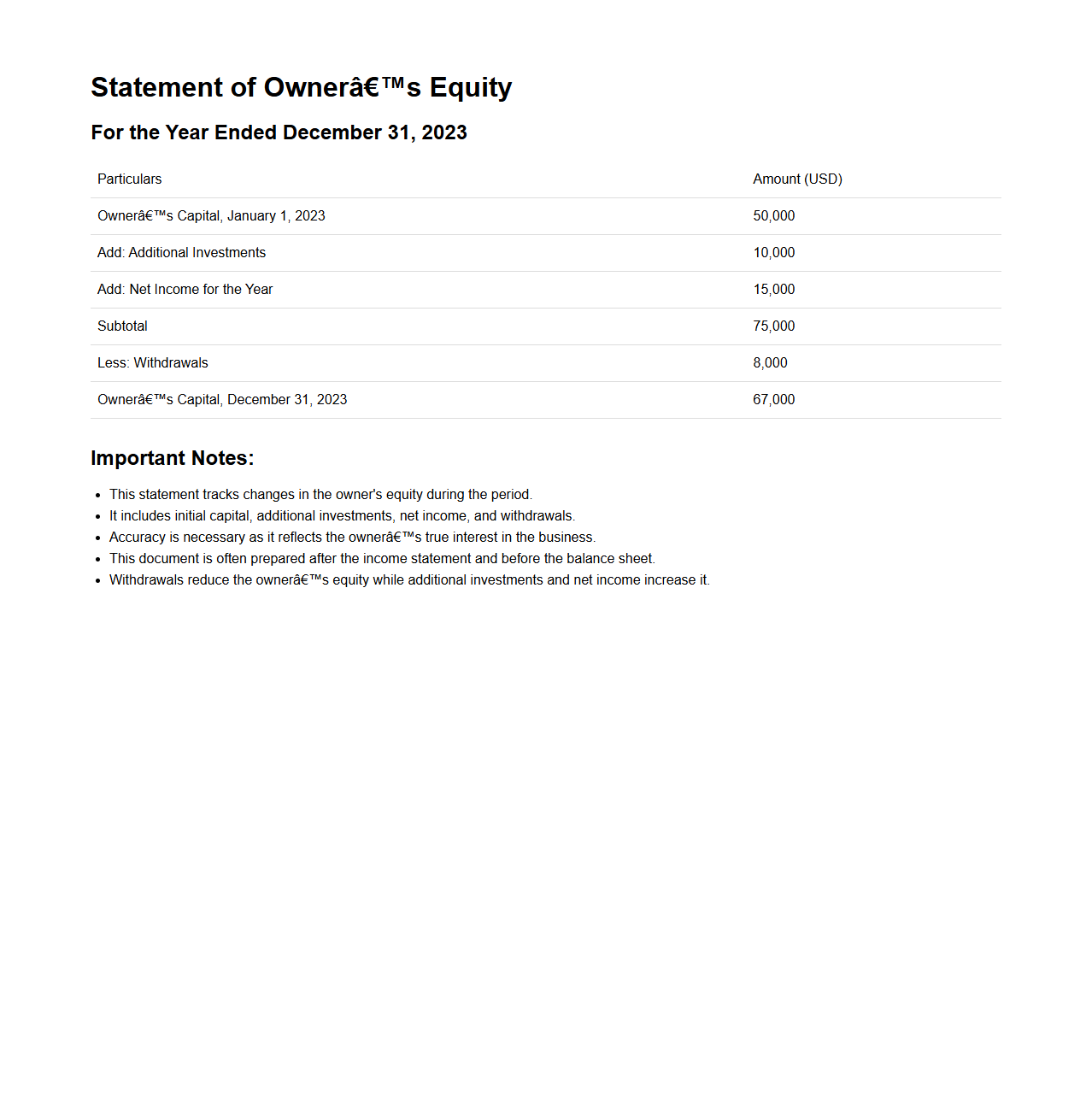

Statement of Owner’s Equity Format

A

Statement of Owner's Equity Format document outlines the structure used to present changes in an owner's equity during a specific accounting period. It includes key components such as beginning equity, additional investments, net income or loss, withdrawals, and ending equity balance. This format ensures transparency and clarity in tracking the financial interest of the owner in the business.

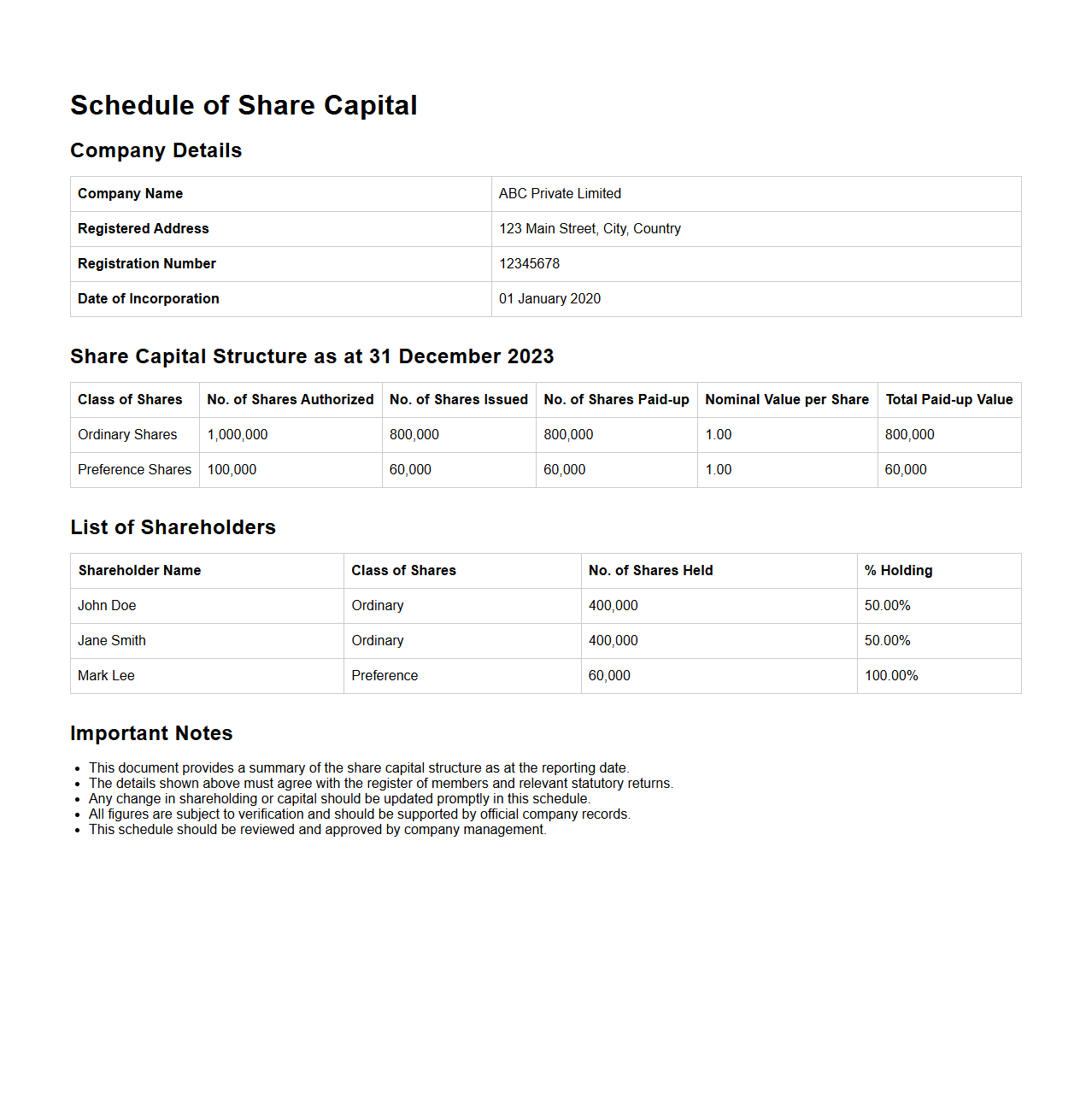

Schedule of Share Capital Format

The

Schedule of Share Capital Format document outlines the detailed breakdown of a company's share capital, including types of shares, their nominal values, and the total number issued. It serves as a critical record for regulatory compliance, investor communication, and internal financial management. This format ensures clarity and consistency in documenting equity structure for audits and corporate filings.

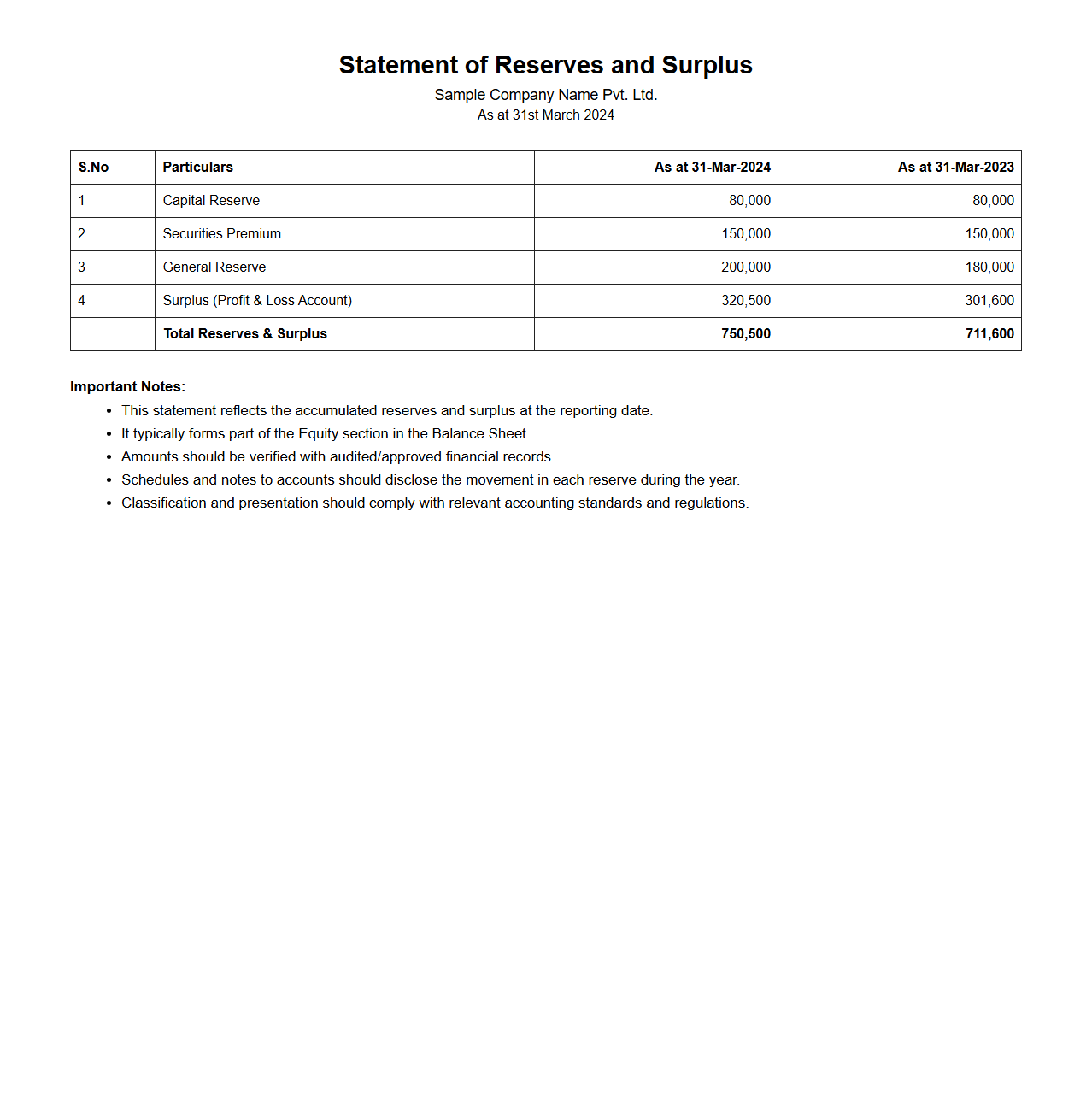

Statement of Reserves and Surplus Format

The

Statement of Reserves and Surplus Format document provides a structured layout detailing a company's equity section, highlighting the components of reserves and retained earnings. It showcases critical financial elements such as capital reserves, securities premium, general reserves, and accumulated profits, offering transparency about the accumulation and utilization of surplus funds. This format is essential for stakeholders to assess the financial stability and reinvestment capability of a business.

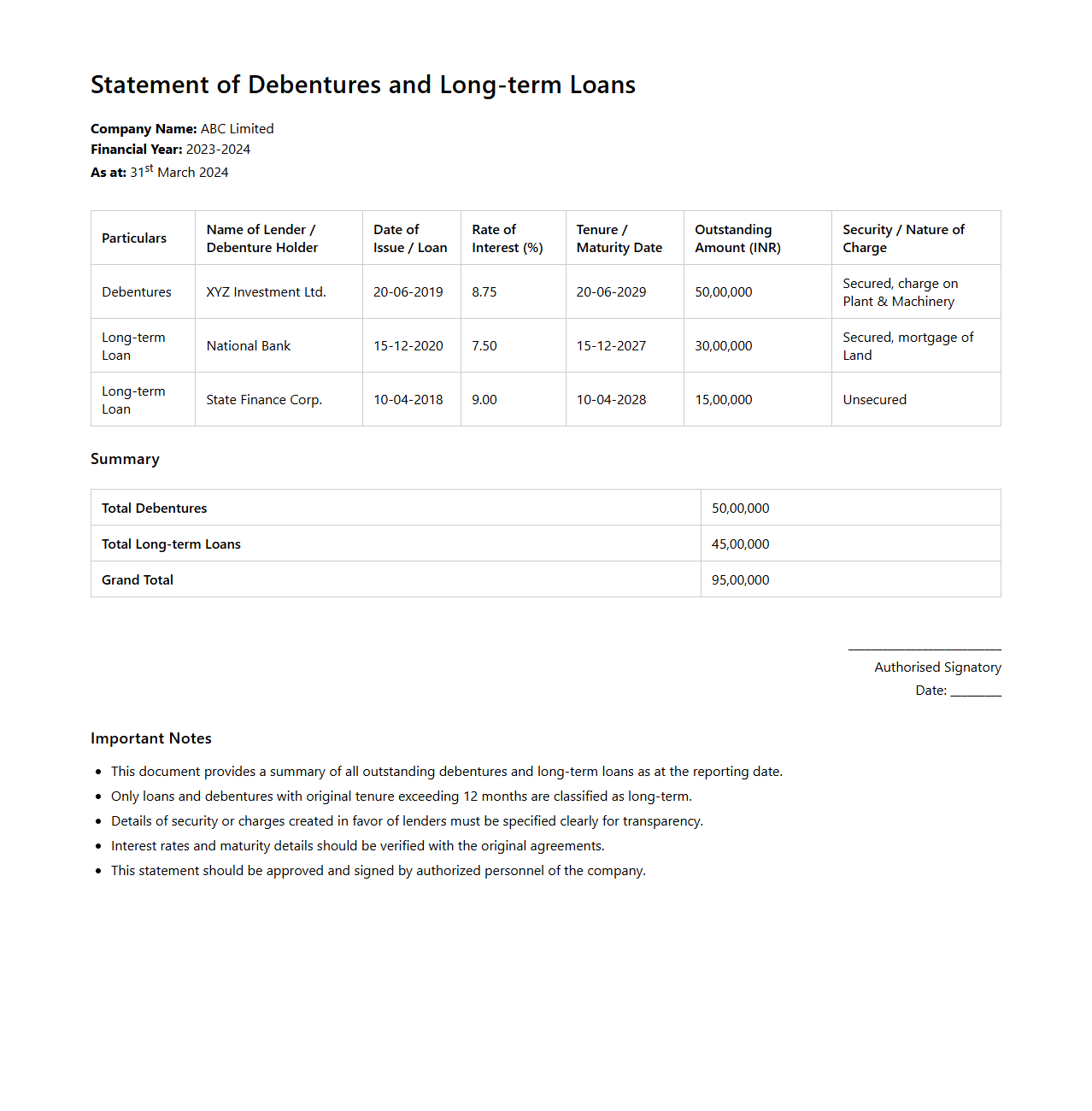

Statement of Debentures and Long-term Loans Format

The

Statement of Debentures and Long-term Loans Format document outlines the detailed financial information related to a company's outstanding debentures and long-term borrowings. It typically includes sections such as the principal amount, interest rates, maturity dates, and repayment schedules, providing a clear summary of the company's long-term liabilities. This document is essential for stakeholders to assess the organization's debt structure and financial stability over an extended period.

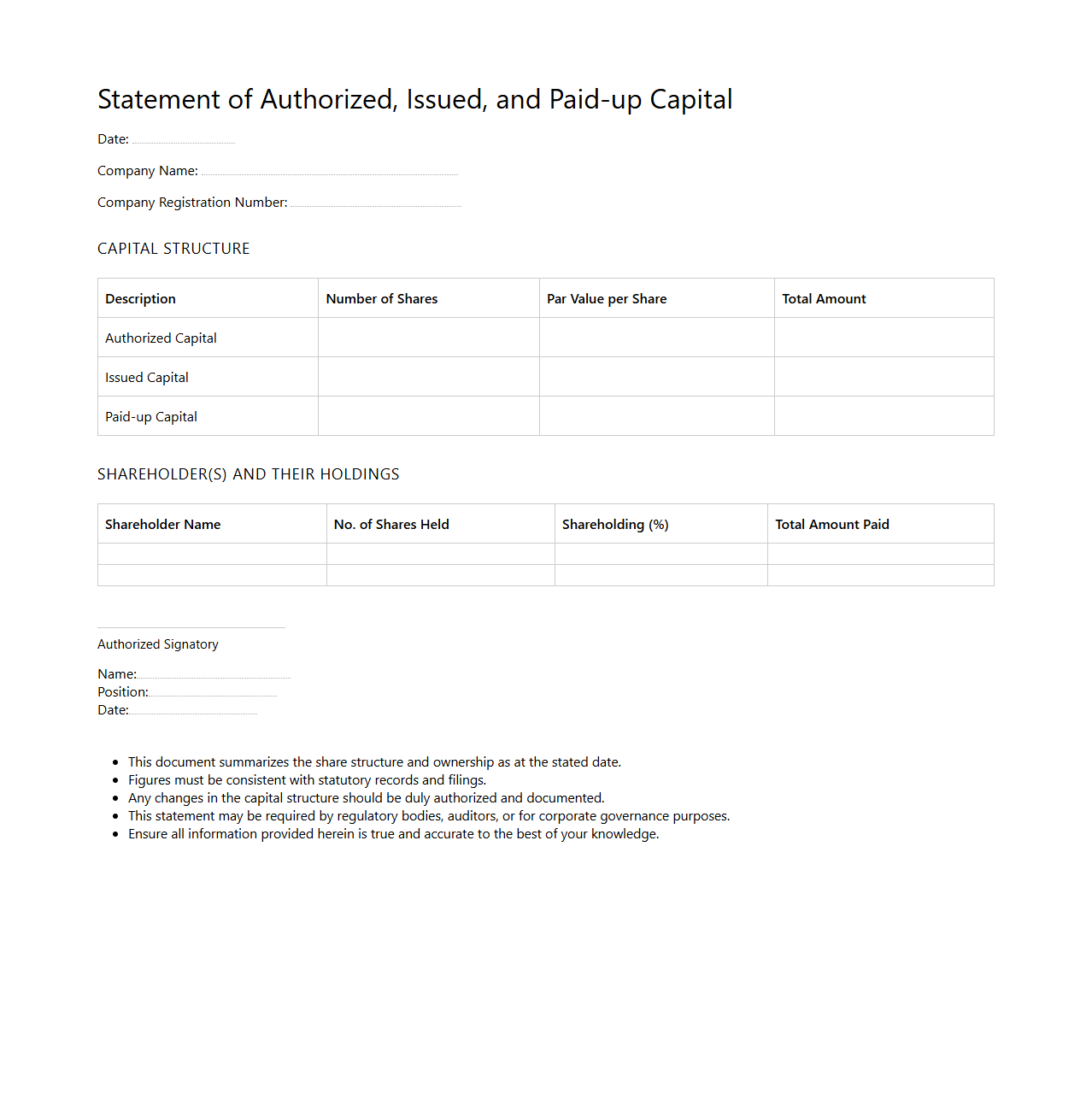

Statement of Authorized, Issued, and Paid-up Capital Format

The

Statement of Authorized, Issued, and Paid-up Capital Format document outlines the details of a company's share capital, including the maximum number of shares authorized to be issued, the actual number of shares issued to shareholders, and the portion of those shares that have been fully paid. This format ensures clear disclosure of capital structure for regulatory compliance and investor transparency. It typically includes sections for share classes, nominal values, and corresponding financial data to maintain accurate corporate records.

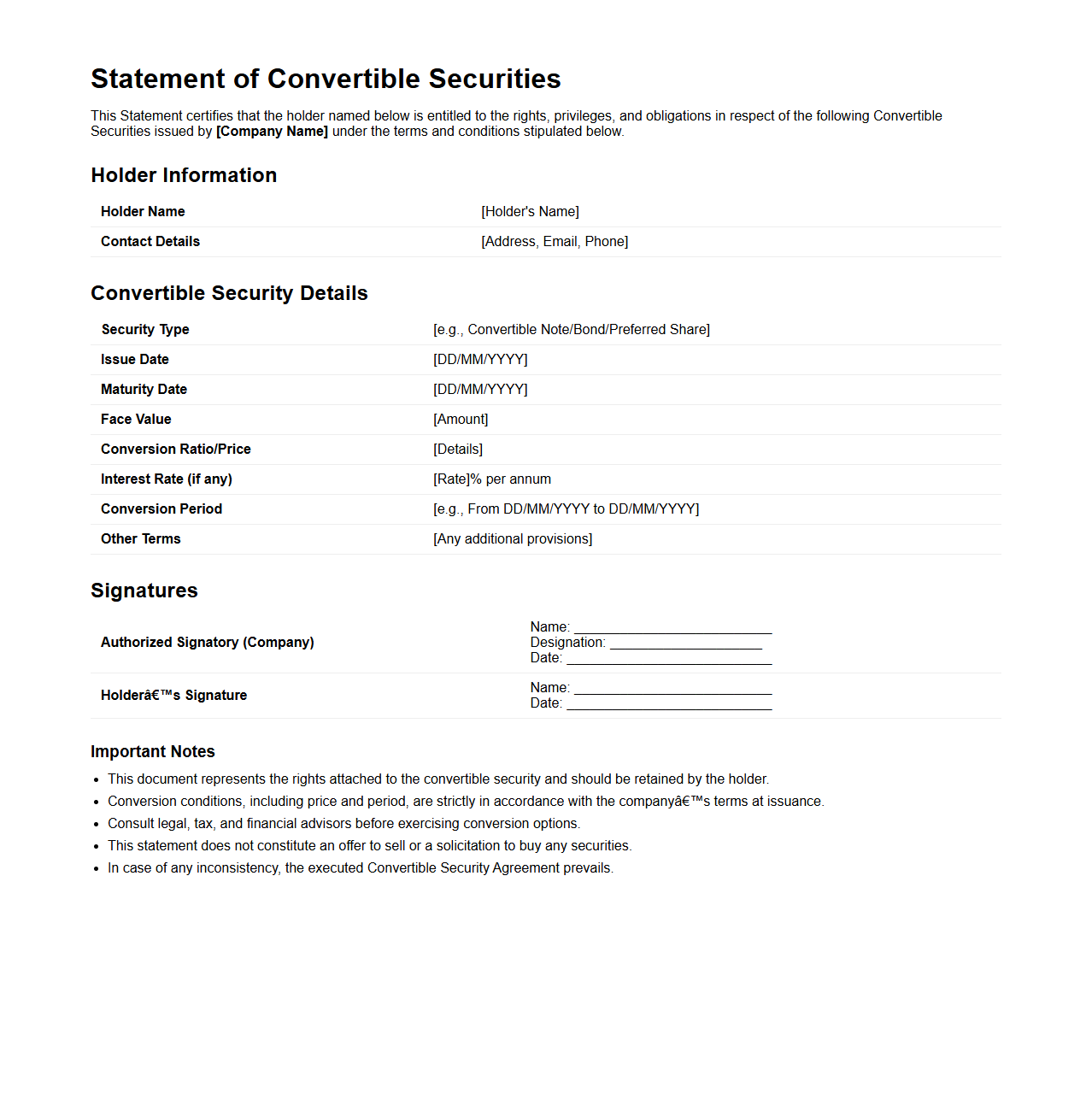

Statement of Convertible Securities Format

A

Statement of Convertible Securities Format document details the terms and conditions of securities that can be converted into equity, such as convertible bonds or preferred shares. It specifies conversion rates, dates, and any associated rights or restrictions, providing clarity for investors and regulatory compliance. This format ensures uniformity and transparency in presenting convertible securities information.

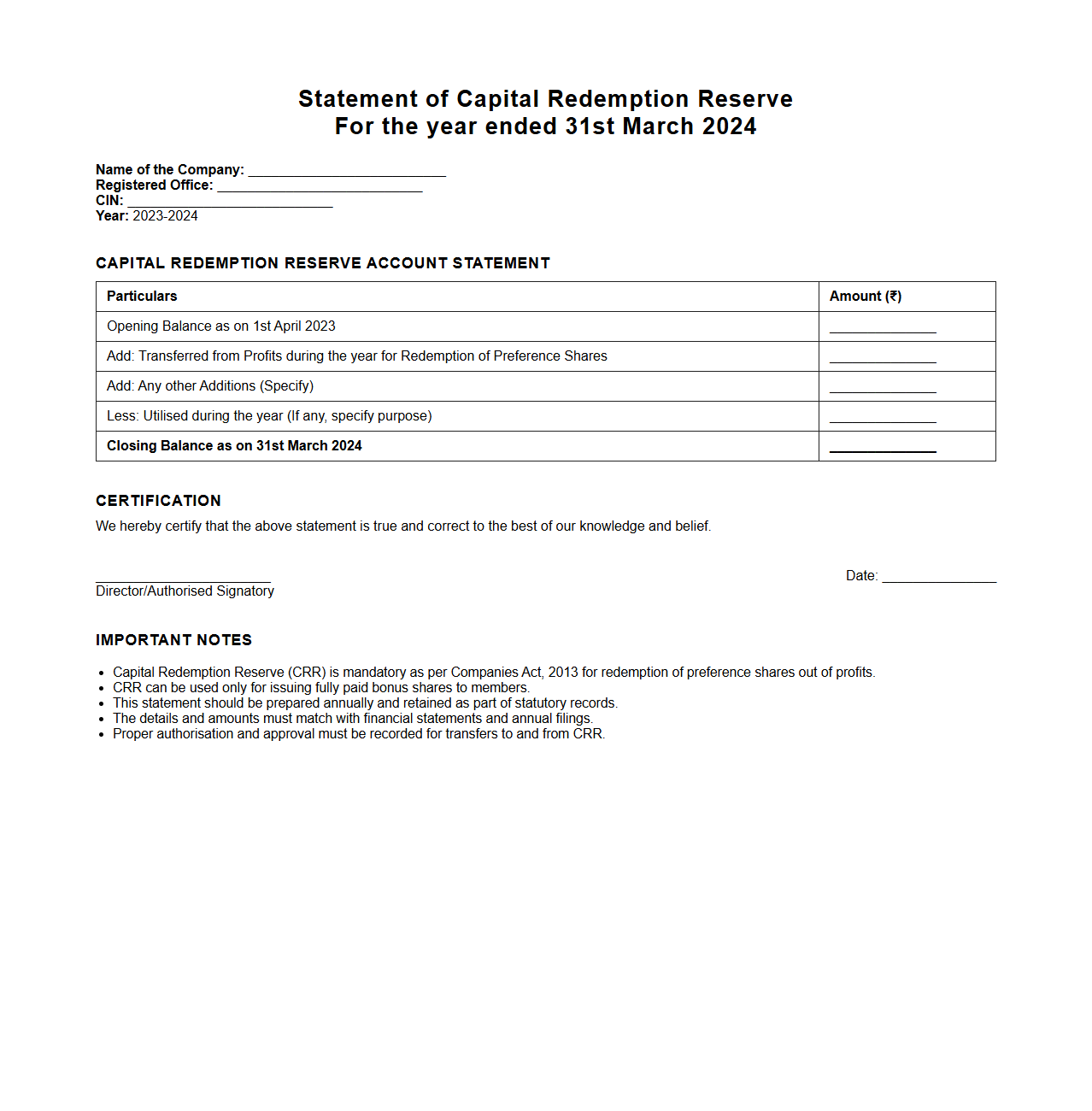

Statement of Capital Redemption Reserve Format

The

Statement of Capital Redemption Reserve Format document outlines the structured presentation of the reserve created when a company redeems its preference shares, ensuring compliance with accounting standards and regulatory requirements. It details the capital redemption reserve balance, transactions affecting the reserve, and reconciles opening and closing balances for accurate financial reporting. This format is crucial for maintaining transparency and validating the source of funds used in share redemption.

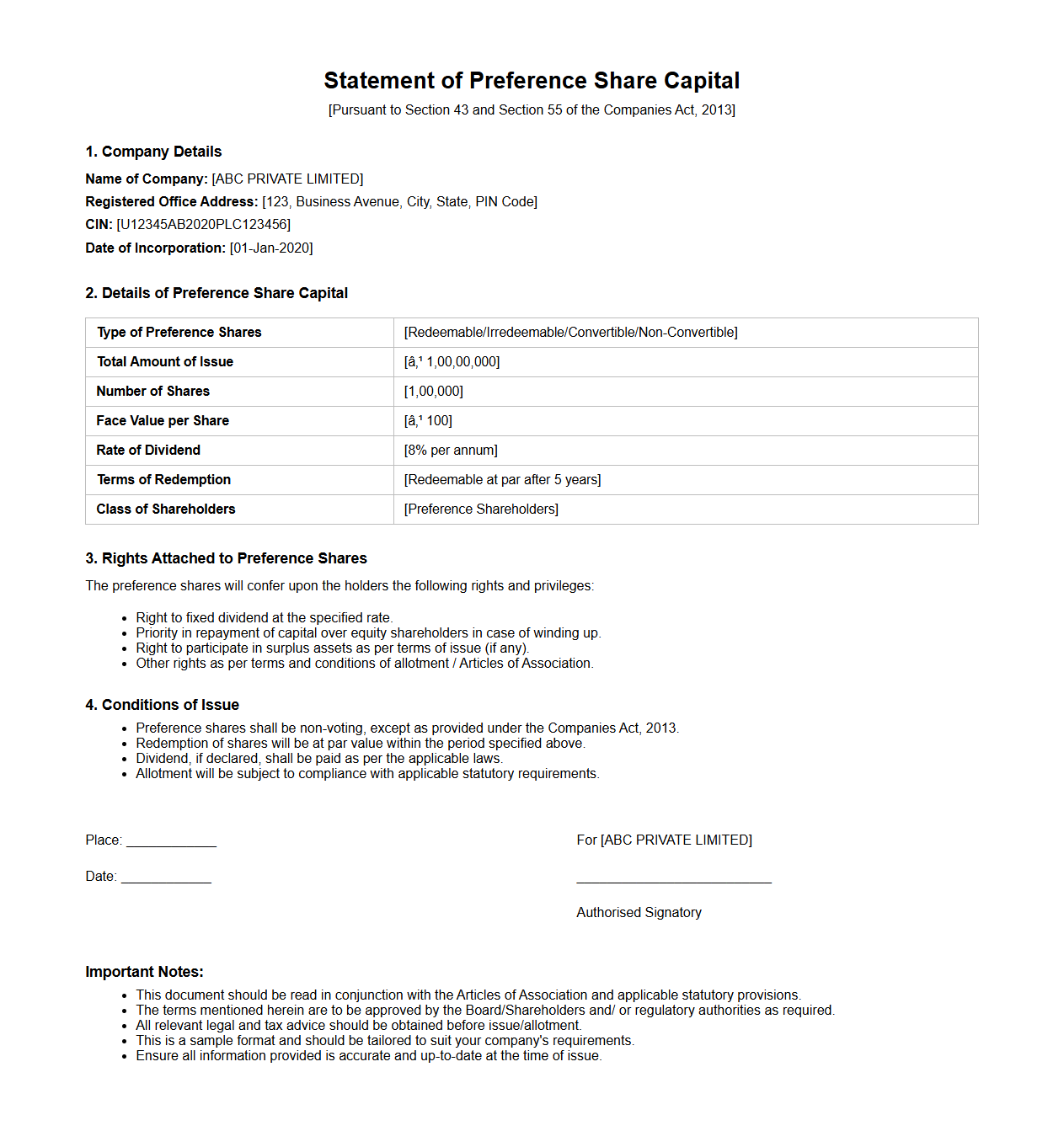

Statement of Preference Share Capital Format

The

Statement of Preference Share Capital Format document outlines the structure and details of preference shares issued by a company, including the number of shares, nominal value, and dividend rates. It serves as a formal record for accounting and regulatory purposes, ensuring clarity on the rights and obligations attached to preference shares. This document is essential for auditors, investors, and company management to monitor capital composition and shareholder equity.

What are the key components included in the capital section of financial statements?

The capital section of financial statements typically includes shareholders' equity, which is a primary element. This section details components such as common stock, preferred stock, retained earnings, and additional paid-in capital. It represents the residual interest in the assets of an entity after deducting liabilities.

How is owners' or shareholders' equity presented in the statement of financial position?

Owners' or shareholders' equity is presented as a distinct section within the statement of financial position. It is shown after liabilities and includes detailed subdivisions like share capital and retained earnings. This presentation reflects the entity's net worth to the owners.

What distinguishes contributed capital from retained earnings in capital reporting?

Contributed capital refers to the funds invested by shareholders through the purchase of stock. Retained earnings consist of accumulated profits retained in the business rather than distributed as dividends. These two components highlight the sources of equity capital from investors versus operational profits.

How are additional paid-in capital and reserves disclosed in financial statements?

Additional paid-in capital is reported separately from common stock in the equity section, representing amounts paid by shareholders above par value. Reserves are disclosed as part of equity and may include legal, statutory, or discretionary reserves. The clear disclosure ensures transparency of all equity-related funds.

What format requirements must be followed when presenting capital in accordance with financial reporting standards?

Financial reporting standards require the capital section to be presented in a clear, structured format with detailed labels for each equity component. Consistent classification and disclosure enhance comparability across reporting periods. This format ensures stakeholders can easily assess the company's financial health and equity structure.