The format of audit report for company typically includes the title, addressee, and introduction that states the auditor's responsibility. It then presents the scope of the audit, auditor's opinion, and any additional explanatory paragraphs if necessary. The report concludes with the auditor's signature, date, and address, ensuring clarity and compliance with auditing standards.

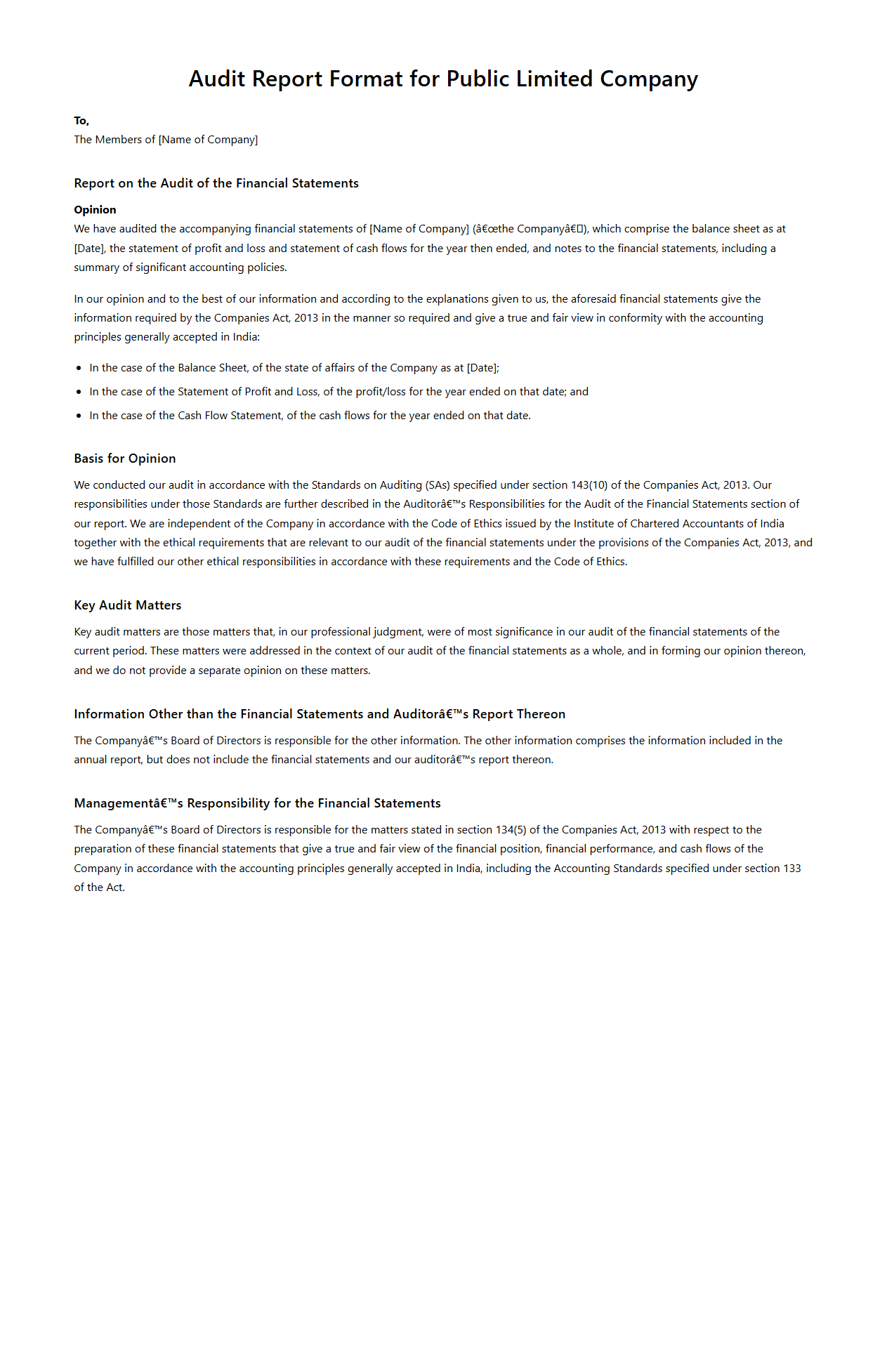

Title: Audit Report Format for Public Limited Company

The

Audit Report Format for Public Limited Company document provides a standardized structure for auditors to present their findings on a company's financial statements. It ensures compliance with regulatory requirements, including disclosures about the company's financial position, audit scope, and auditor's opinion. This format enhances transparency and accountability for stakeholders such as investors, regulators, and management.

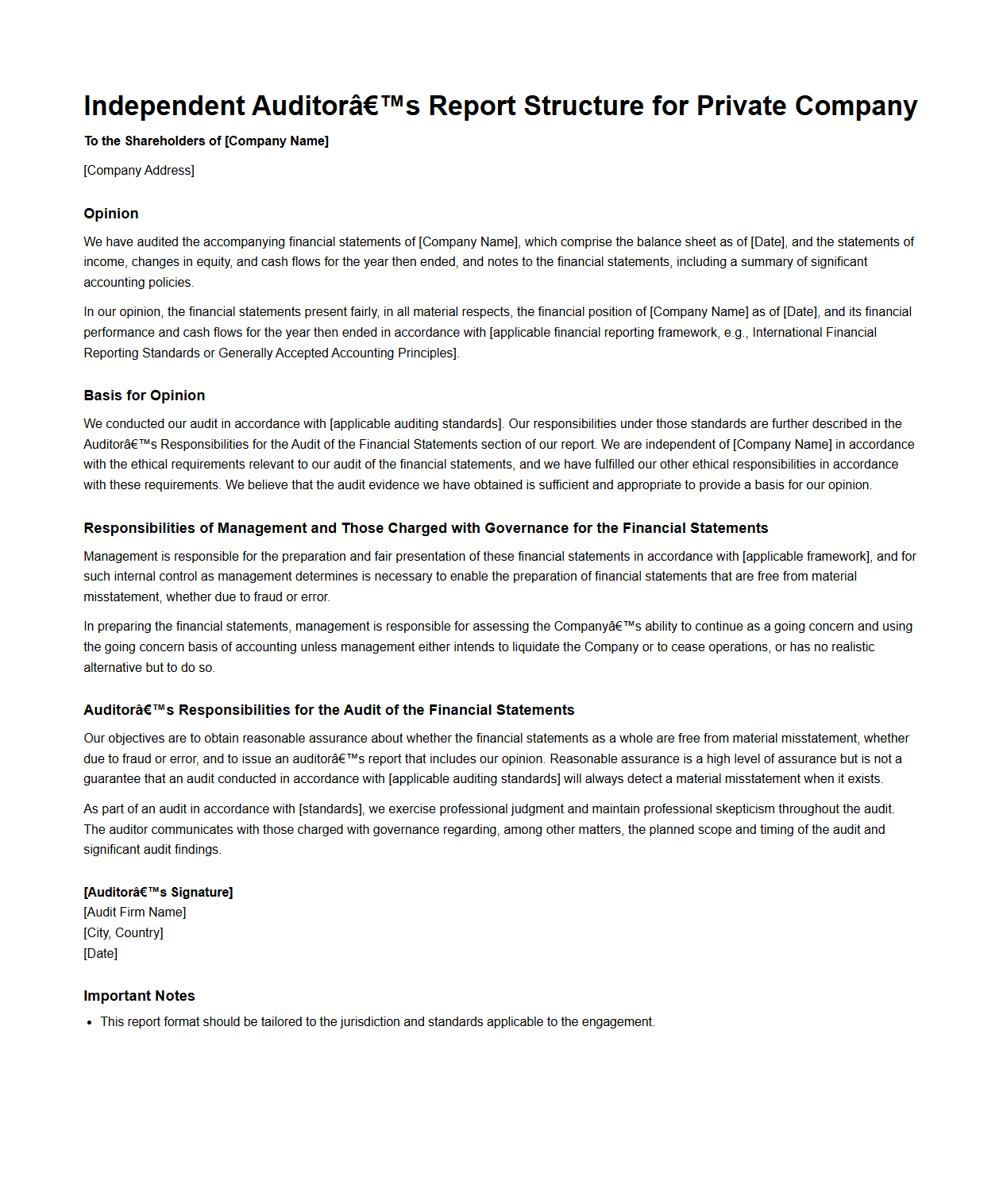

Title: Independent Auditor’s Report Structure for Private Company

The

Independent Auditor's Report Structure for private companies outlines the standardized format and essential components auditors must follow when expressing their opinion on a company's financial statements. This document ensures clarity, transparency, and compliance with auditing standards such as the ISA (International Standards on Auditing) or GAAS (Generally Accepted Auditing Standards). Key sections include the auditor's opinion, basis for opinion, responsibilities of management, and auditor's responsibilities, providing stakeholders with reliable assurance on financial accuracy.

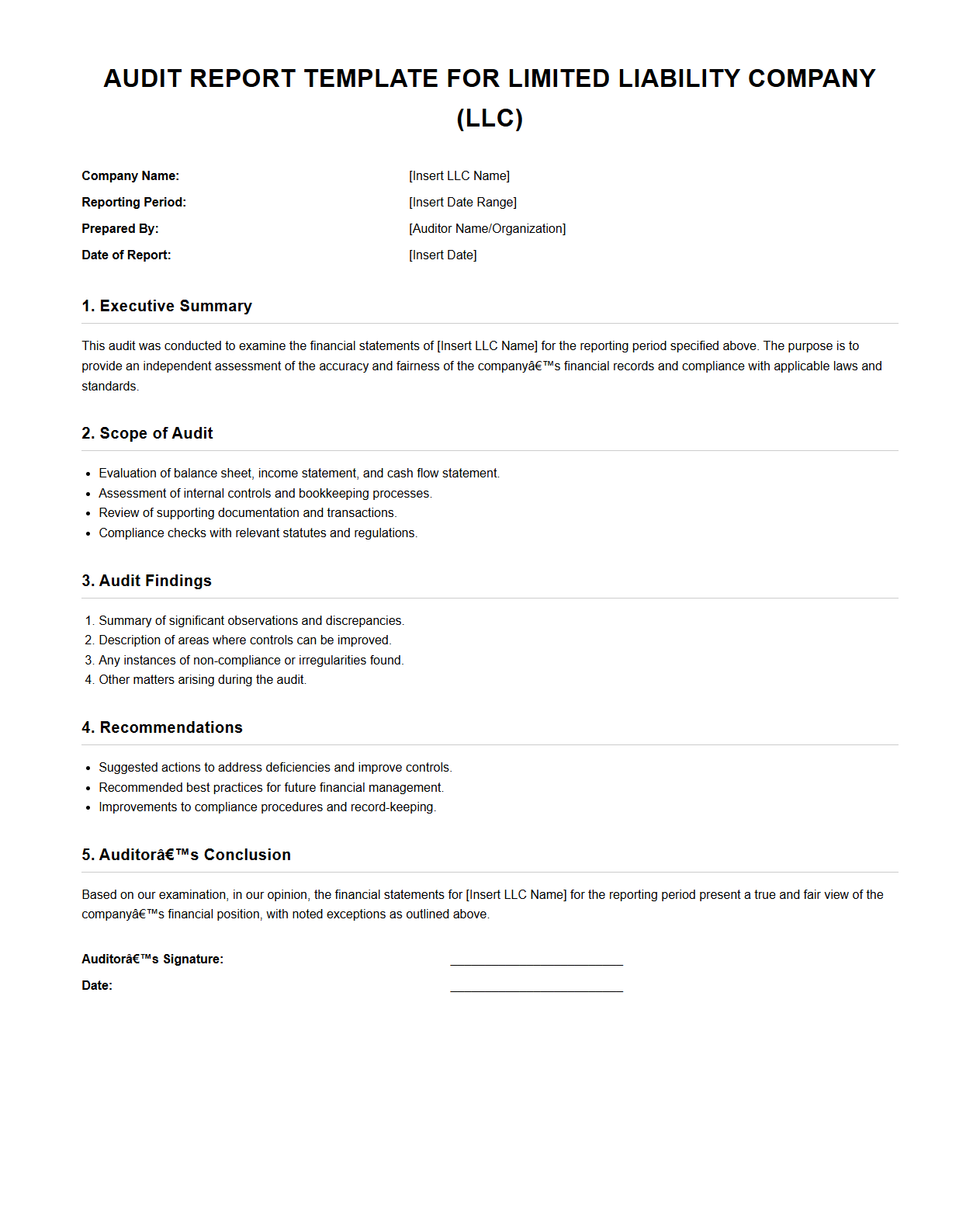

Title: Audit Report Template for Limited Liability Company (LLC)

The

Audit Report Template for Limited Liability Company (LLC) is a structured document designed to standardize the presentation of financial audit findings specific to LLCs. It includes essential sections such as the auditor's opinion, financial statements review, compliance assessment, and internal control evaluation. This template ensures clarity, consistency, and regulatory compliance, facilitating accurate communication of the LLC's financial health to stakeholders.

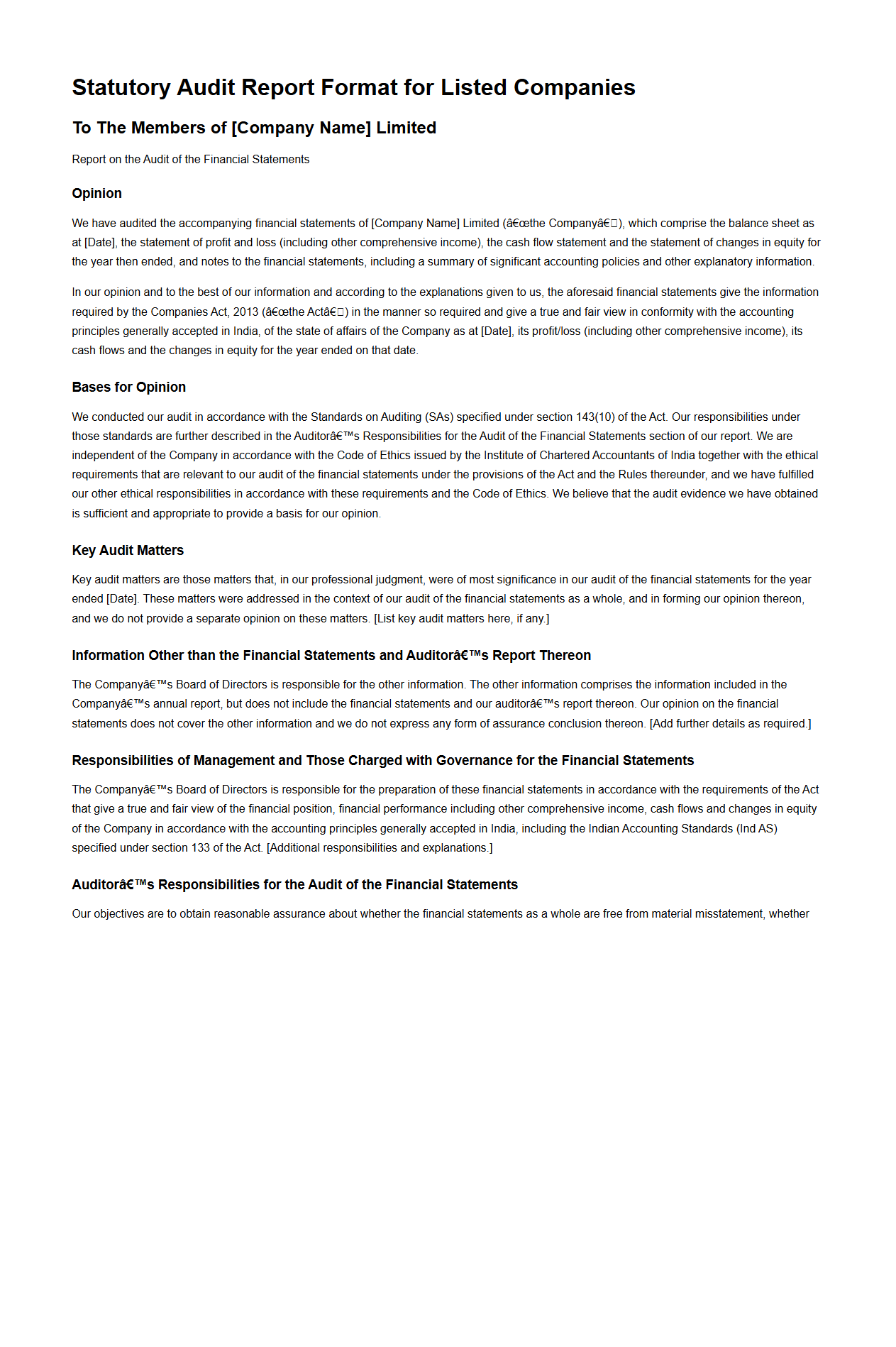

Title: Statutory Audit Report Format for Listed Companies

The

Statutory Audit Report Format for Listed Companies document outlines the standardized structure and essential components required for audit reports submitted by auditors of publicly traded firms. It ensures compliance with regulatory frameworks set by authorities such as the Securities and Exchange Board of India (SEBI) and the Institute of Chartered Accountants of India (ICAI). This format enhances transparency, accuracy, and uniformity in financial reporting for stakeholders and regulators.

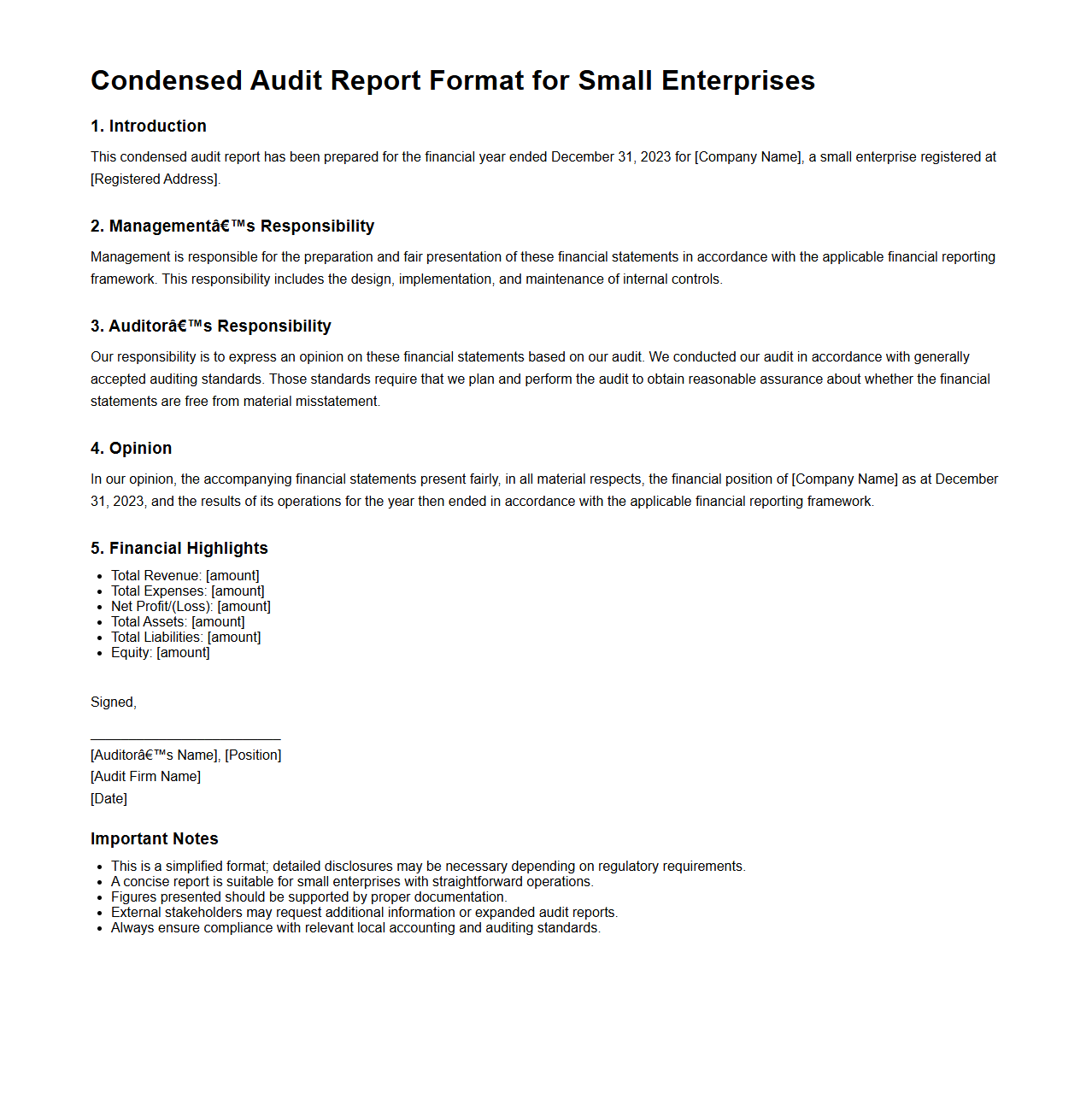

Title: Condensed Audit Report Format for Small Enterprises

The

Condensed Audit Report Format for Small Enterprises document provides a streamlined framework for auditors to present their findings clearly and concisely, tailored to the specific needs of small businesses. It emphasizes simplified disclosures while maintaining compliance with regulatory standards to enhance transparency and reliability. This format supports efficient communication of financial health and audit results, fostering trust among stakeholders and facilitating informed decision-making.

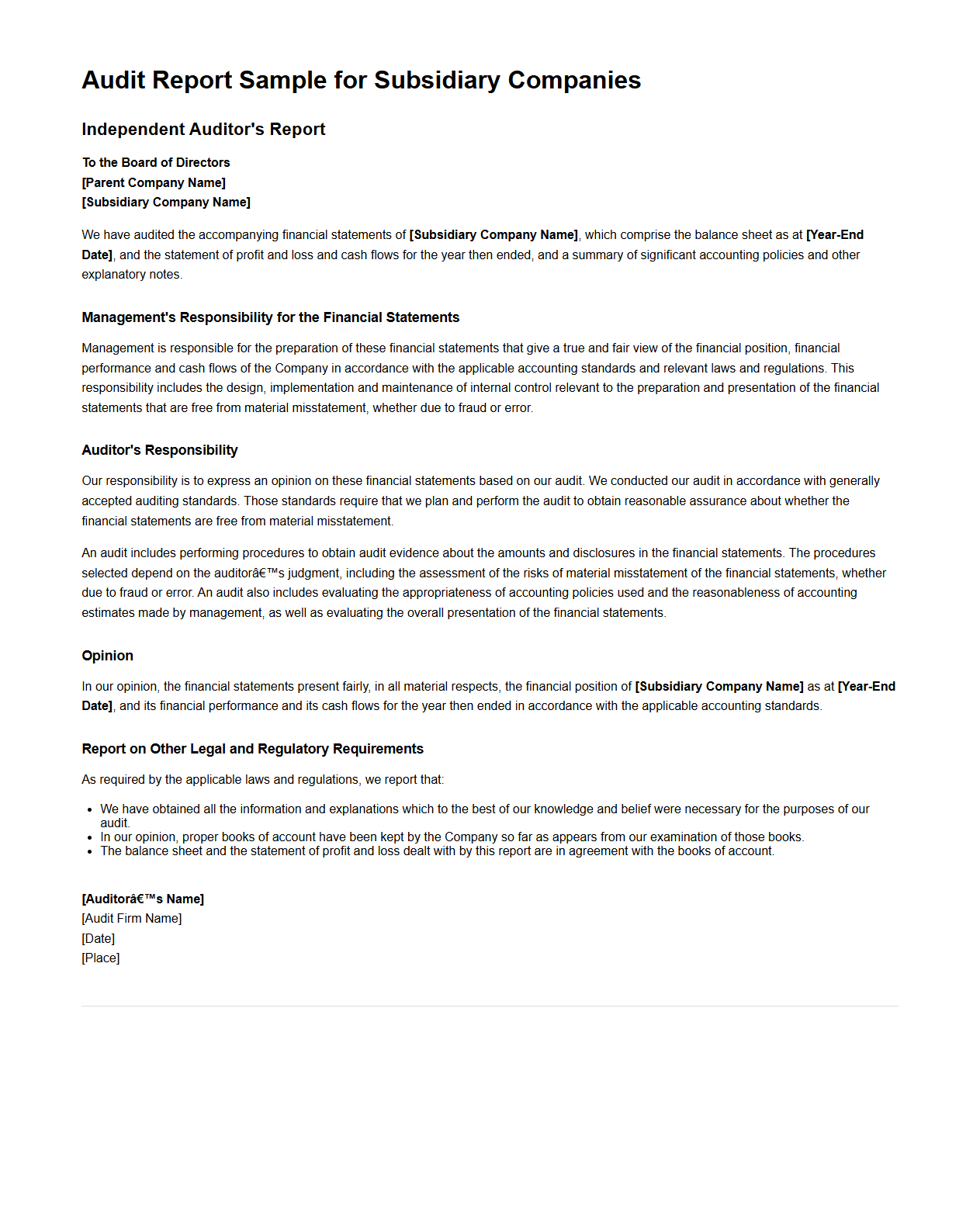

Title: Audit Report Sample for Subsidiary Companies

The

Audit Report Sample for Subsidiary Companies document provides a standardized template illustrating how auditors present their findings on the financial statements of subsidiary entities. It highlights key components such as the auditor's opinion, scope of the audit, and management's responsibilities, ensuring compliance with regulatory standards. This sample serves as a valuable reference for preparing transparent and consistent audit reports across subsidiary organizations.

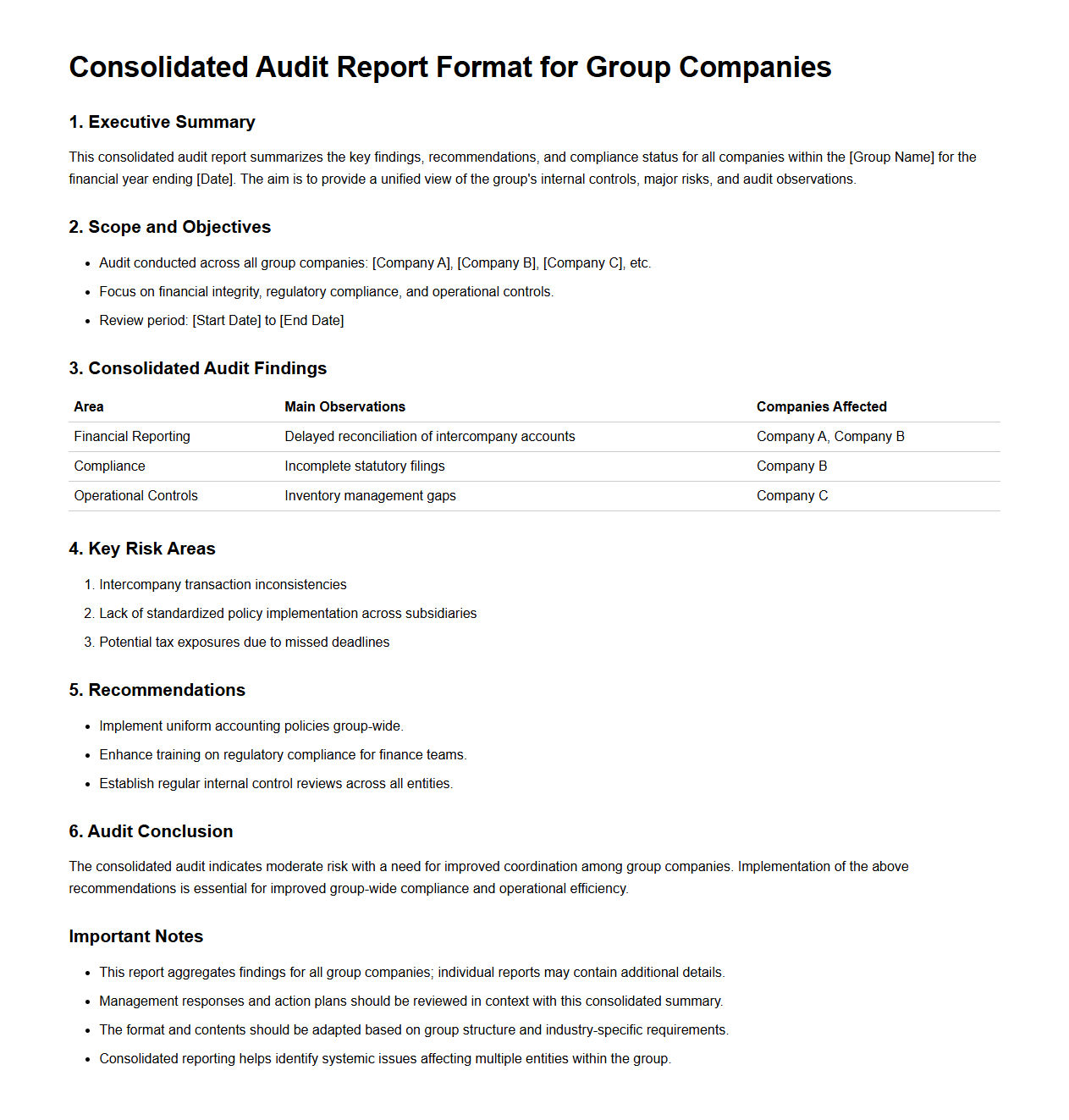

Title: Consolidated Audit Report Format for Group Companies

The

Consolidated Audit Report Format for Group Companies document standardizes the presentation of financial audit findings across multiple entities within a corporate group. It ensures consistent reporting of financial statements, audit observations, and compliance issues, facilitating clear communication between auditors, stakeholders, and regulatory bodies. This format aids in comprehensive assessment by integrating individual company audits into a singular, coherent report.

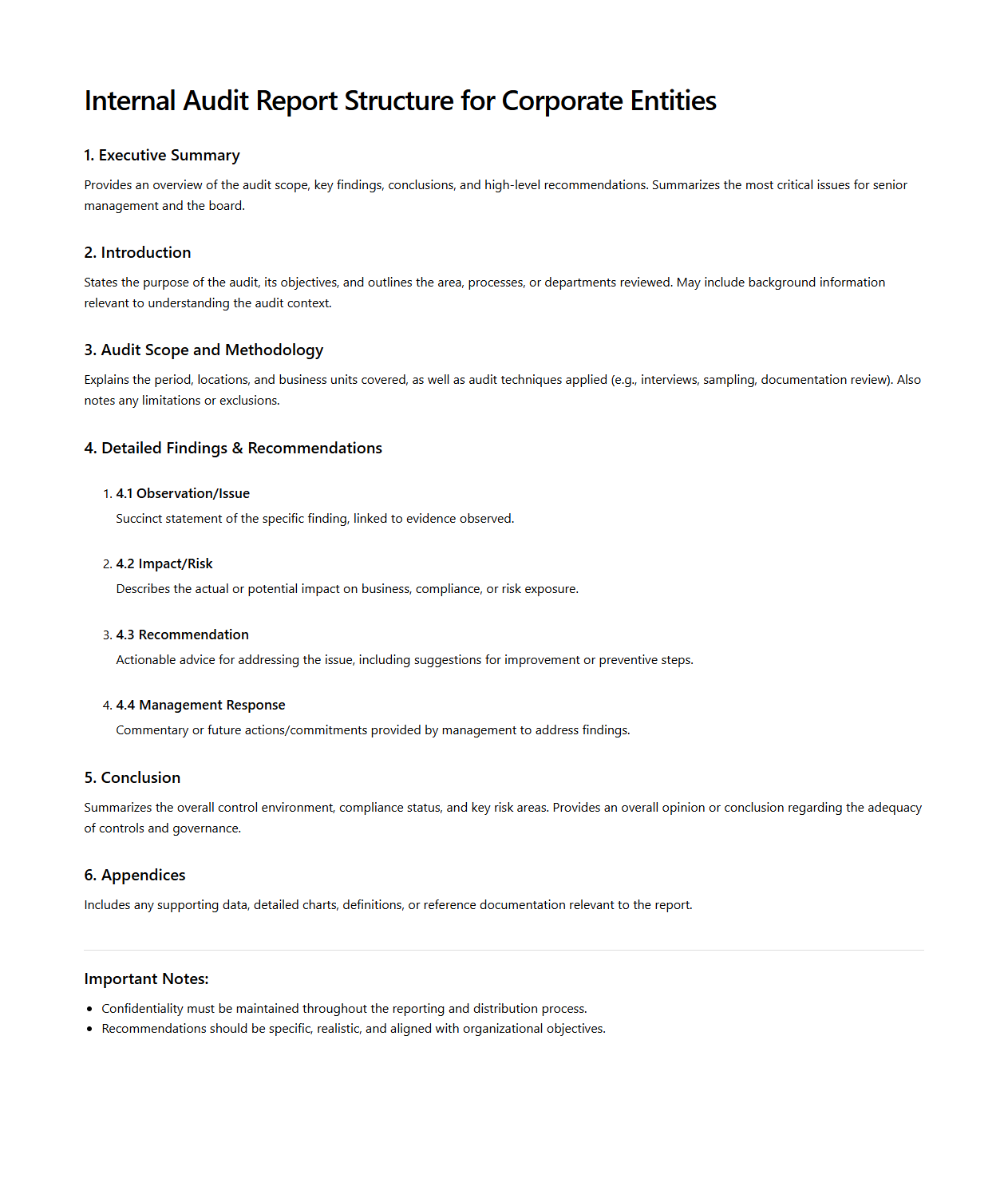

Title: Internal Audit Report Structure for Corporate Entities

The

Internal Audit Report Structure for corporate entities outlines the standardized format and essential components required to present audit findings clearly and effectively. It ensures transparency, consistency, and compliance with regulatory frameworks, enabling stakeholders to assess internal controls, risk management, and governance processes. This document typically includes sections such as auditor's opinion, scope of audit, observations, recommendations, and management responses.

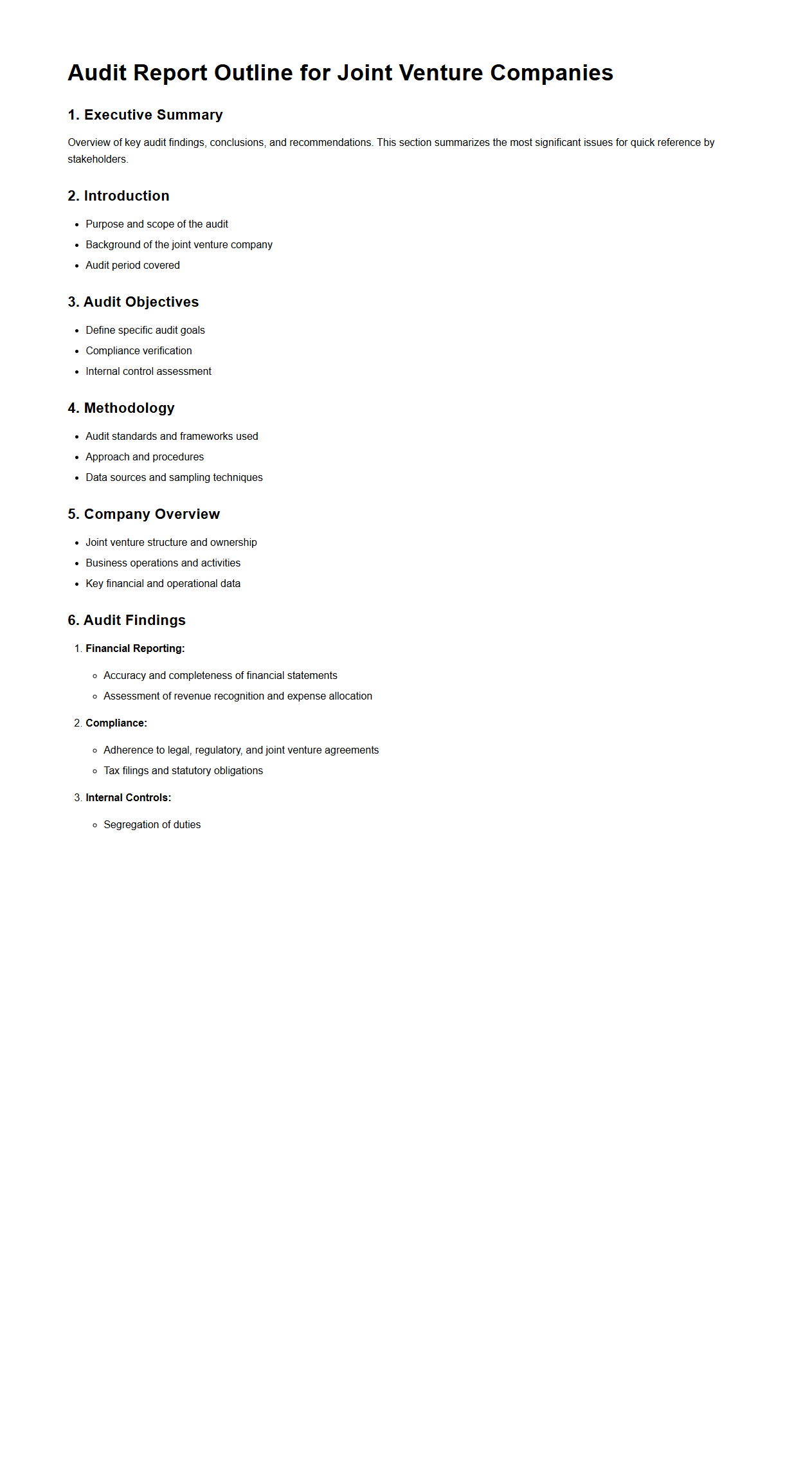

Title: Audit Report Outline for Joint Venture Companies

The

Audit Report Outline for Joint Venture Companies document provides a structured framework to ensure comprehensive financial and operational assessment specific to joint ventures. It highlights key areas such as financial statements accuracy, compliance with joint venture agreements, and risk management practices. This outline assists auditors in delivering precise, consistent, and transparent reports tailored to the complexities of joint venture partnerships.

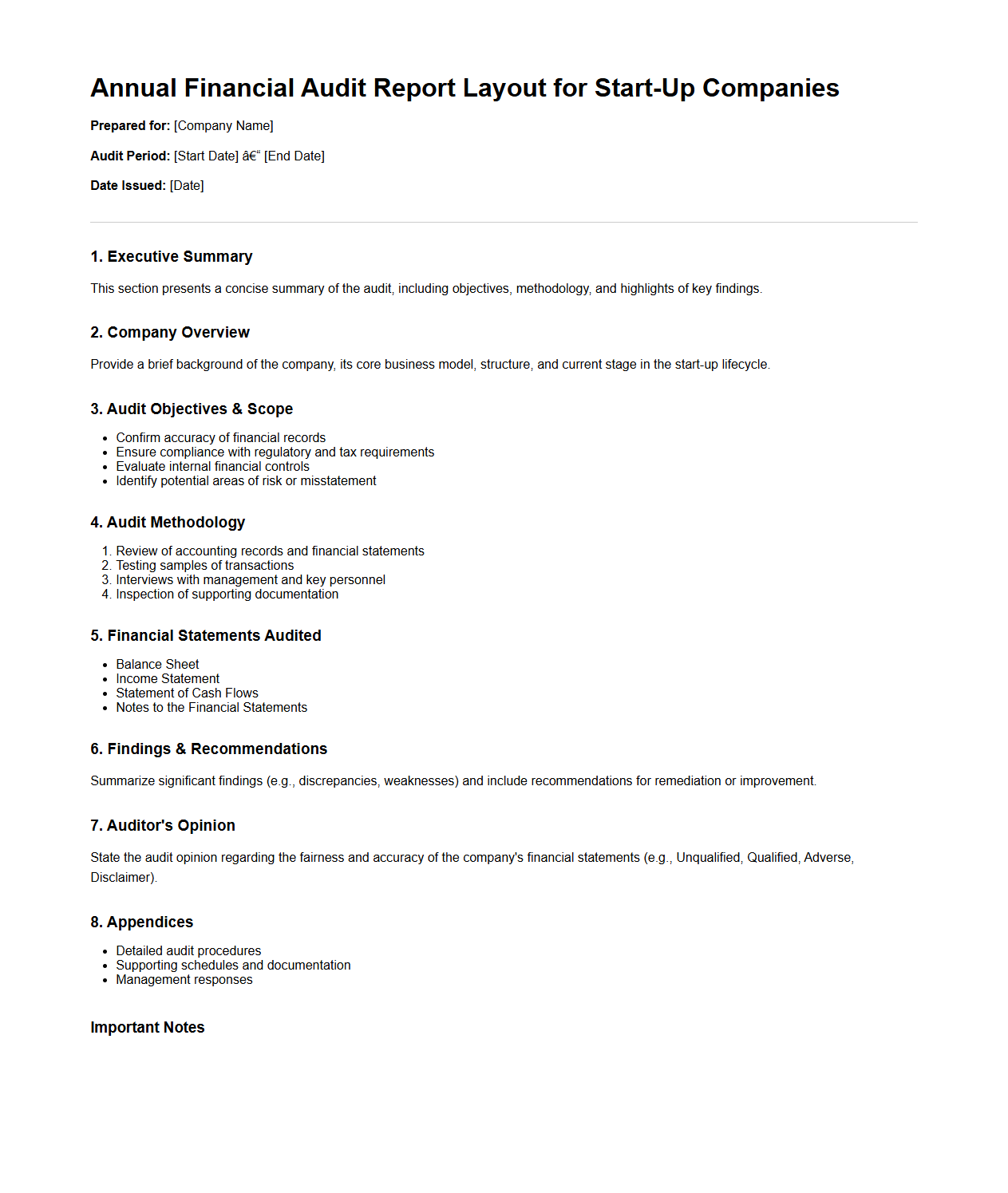

Title: Annual Financial Audit Report Layout for Start-Up Companies

The

Annual Financial Audit Report Layout for Start-Up Companies document serves as a structured template designed to guide new businesses in compiling their yearly financial statements and audit findings. It ensures compliance with accounting standards and regulatory requirements, facilitating clear presentation of financial health to investors and stakeholders. This report layout helps start-ups maintain transparency, supporting strategic decision-making and enhancing credibility in the competitive market.

What are the mandatory sections included in a standard audit report for a company?

A standard audit report typically includes sections such as the Title, Auditor's Opinion, Basis for Opinion, Management's Responsibility, Auditor's Responsibility, and Other Reporting Responsibilities. Each section serves to clarify the roles and conclusions of the audit process. These mandatory sections ensure transparency and consistency across audit reports.

How is the auditor's opinion typically structured and presented in the audit report format?

The auditor's opinion is clearly stated in the Opinion Paragraph, which follows the introduction of the report. It outlines whether the financial statements present a true and fair view in accordance with the applicable financial reporting framework. This section is written in a direct and unambiguous manner to convey the auditor's conclusion.

What formatting standards or guidelines must auditors follow when drafting a company's audit report?

Auditors must comply with recognized standards such as ISA (International Standards on Auditing) or GAAS (Generally Accepted Auditing Standards) for formatting audit reports. These guidelines ensure uniformity in structure, language, and presentation style. Following these standards helps maintain professional quality and legal compliance of the audit report.

Which disclosures regarding the company's financial statements are required in the audit report format?

The audit report must disclose any significant accounting policies, material uncertainties, and any related party transactions affecting the financial statements. It also includes statements about the auditor's assessment of risks and inherent limitations of the audit. These disclosures enhance the reader's understanding of the context and reliability of financial information.

How does the format of the audit report address any identified material misstatements or exceptions?

If material misstatements or exceptions are identified, the auditor's report must explicitly mention them in the Emphasis of Matter or Qualified Opinion sections. The report explains the nature and impact of these issues on the financial statements. This transparent approach alerts stakeholders to areas of concern or deviation from accepted accounting standards.