The Format of Audit Report for Financial Statements typically includes the title, addressee, introductory paragraph, scope paragraph, opinion paragraph, and signature of the auditor. It clearly states the responsibility of both the management and the auditor, emphasizing the basis for the audit opinion. The report concludes with the auditor's opinion on whether the financial statements present a true and fair view in accordance with the applicable financial reporting framework.

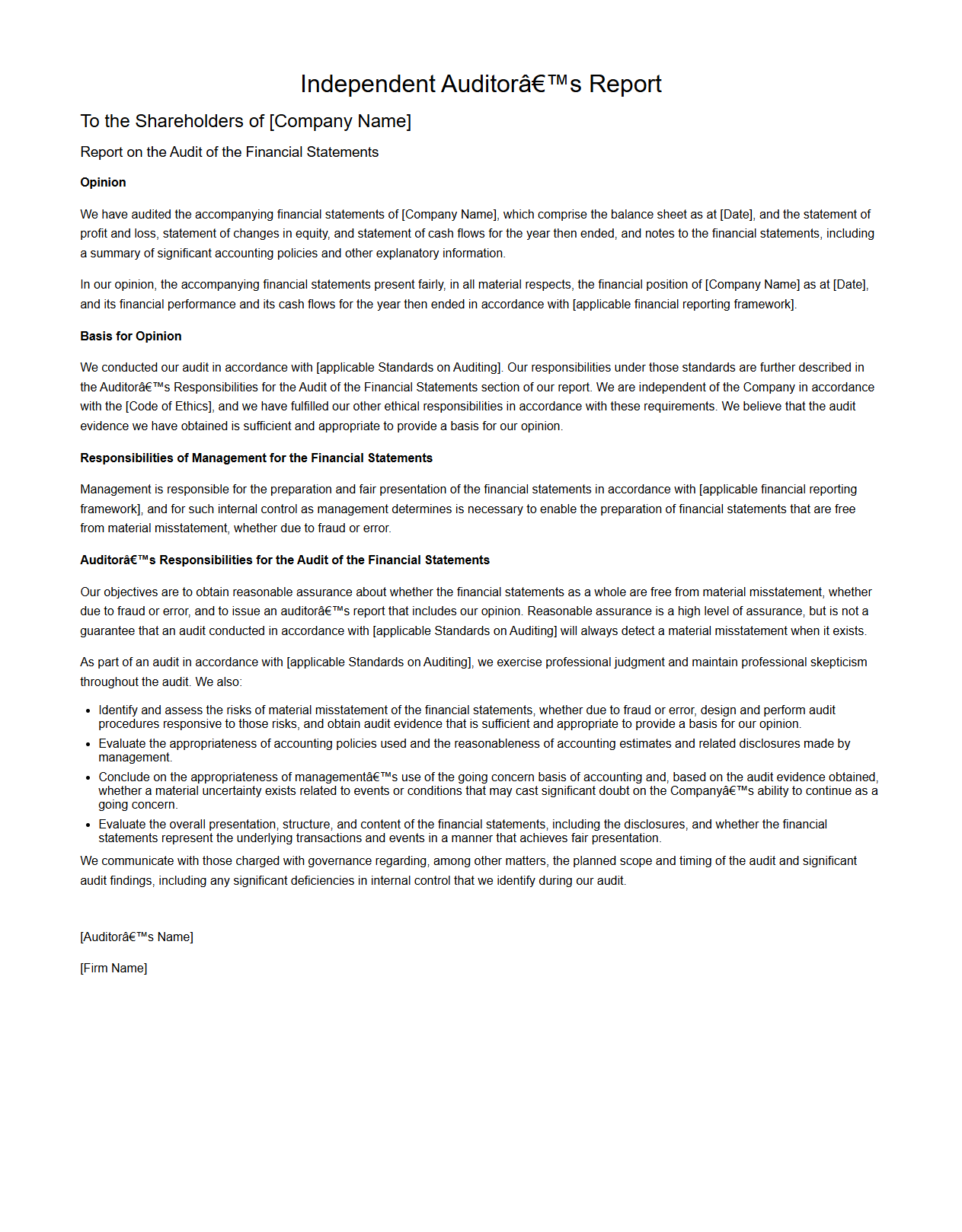

Unqualified Audit Report Format

An

Unqualified Audit Report Format document is a formal statement issued by auditors indicating that the financial statements of an organization present a true and fair view, free from material misstatements. This report follows a standardized structure including the auditor's opinion, basis for opinion, management's responsibility, and auditor's responsibility sections. It serves as an assurance tool for stakeholders, confirming the accuracy and reliability of the financial information provided.

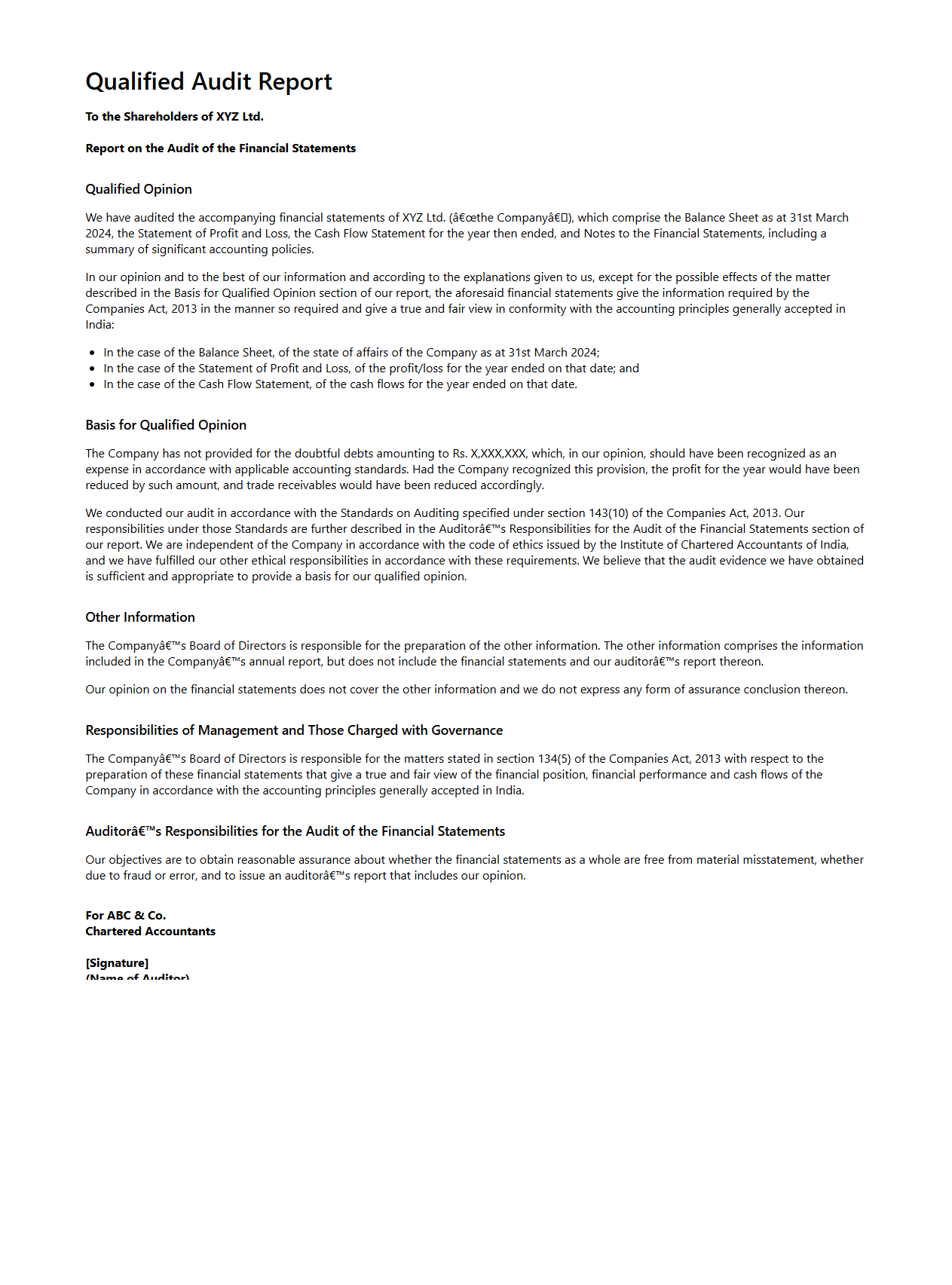

Qualified Audit Report Format

A

Qualified Audit Report Format is a standardized document used by auditors to communicate findings where the financial statements are mostly accurate but contain specific exceptions or deviations. This format clearly outlines the scope of the audit, the areas of concern, and the reasons for the qualification, ensuring transparency and compliance with auditing standards. It serves as a critical tool for stakeholders to assess the reliability and integrity of the organization's financial reporting.

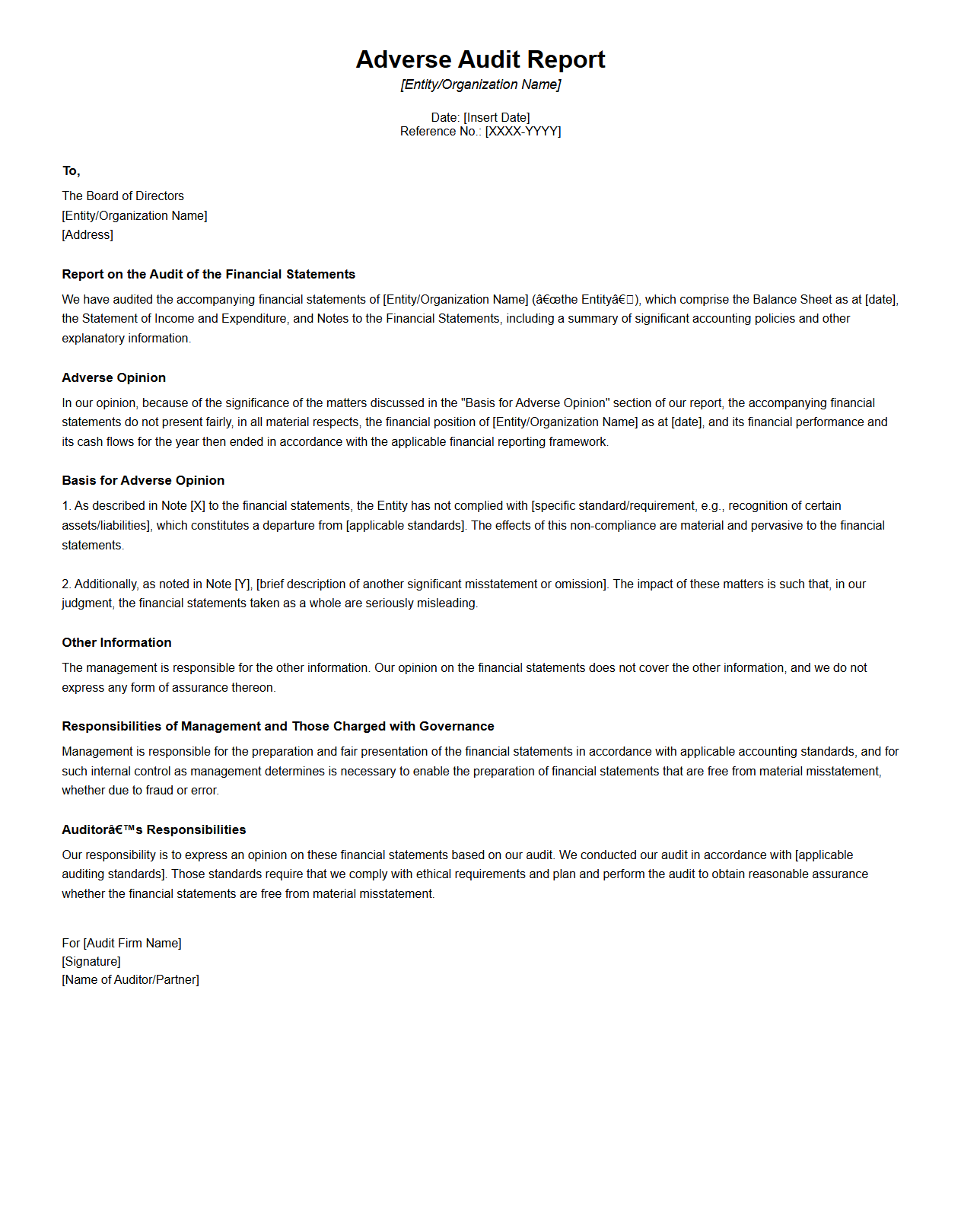

Adverse Audit Report Format

An

Adverse Audit Report Format document is a formal statement issued by auditors when financial statements contain significant misstatements or deviations from accounting standards, making them unreliable. It highlights critical issues such as fraud, errors, or non-compliance with regulatory requirements, negatively impacting the credibility of the entity's financial health. This report includes detailed findings, auditor's opinion, and the specific reasons for the adverse conclusion, serving as an essential tool for stakeholders to assess financial risks.

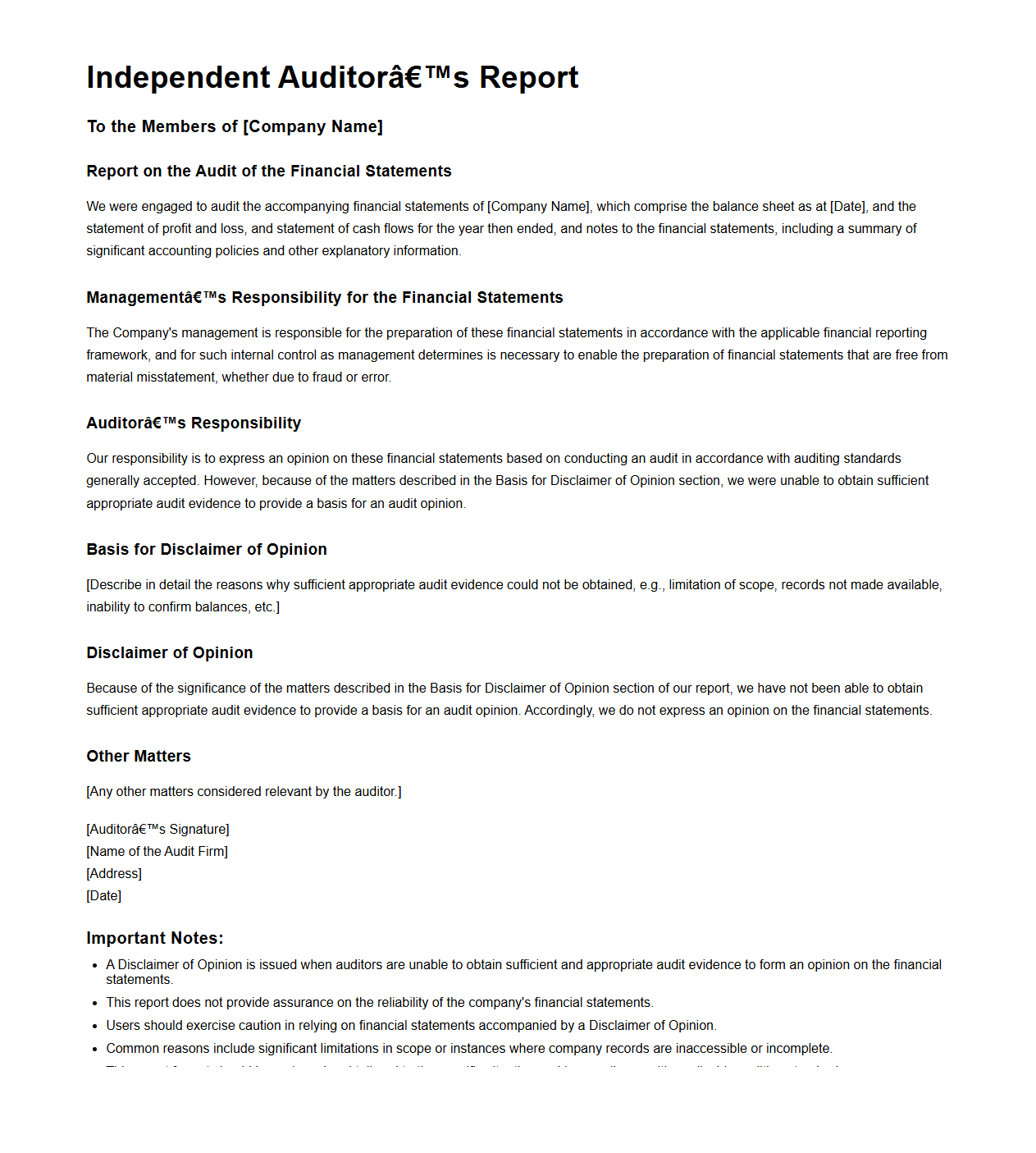

Disclaimer of Opinion Audit Report Format

A

Disclaimer of Opinion Audit Report Format document outlines the structure and content used by auditors when they are unable to obtain sufficient appropriate evidence to form an opinion on financial statements. This format explicitly states that the auditor does not express an opinion due to significant uncertainties or limitations in the audit scope. It ensures clear communication of the auditor's inability to provide assurance, safeguarding both the auditor and the users of the financial report.

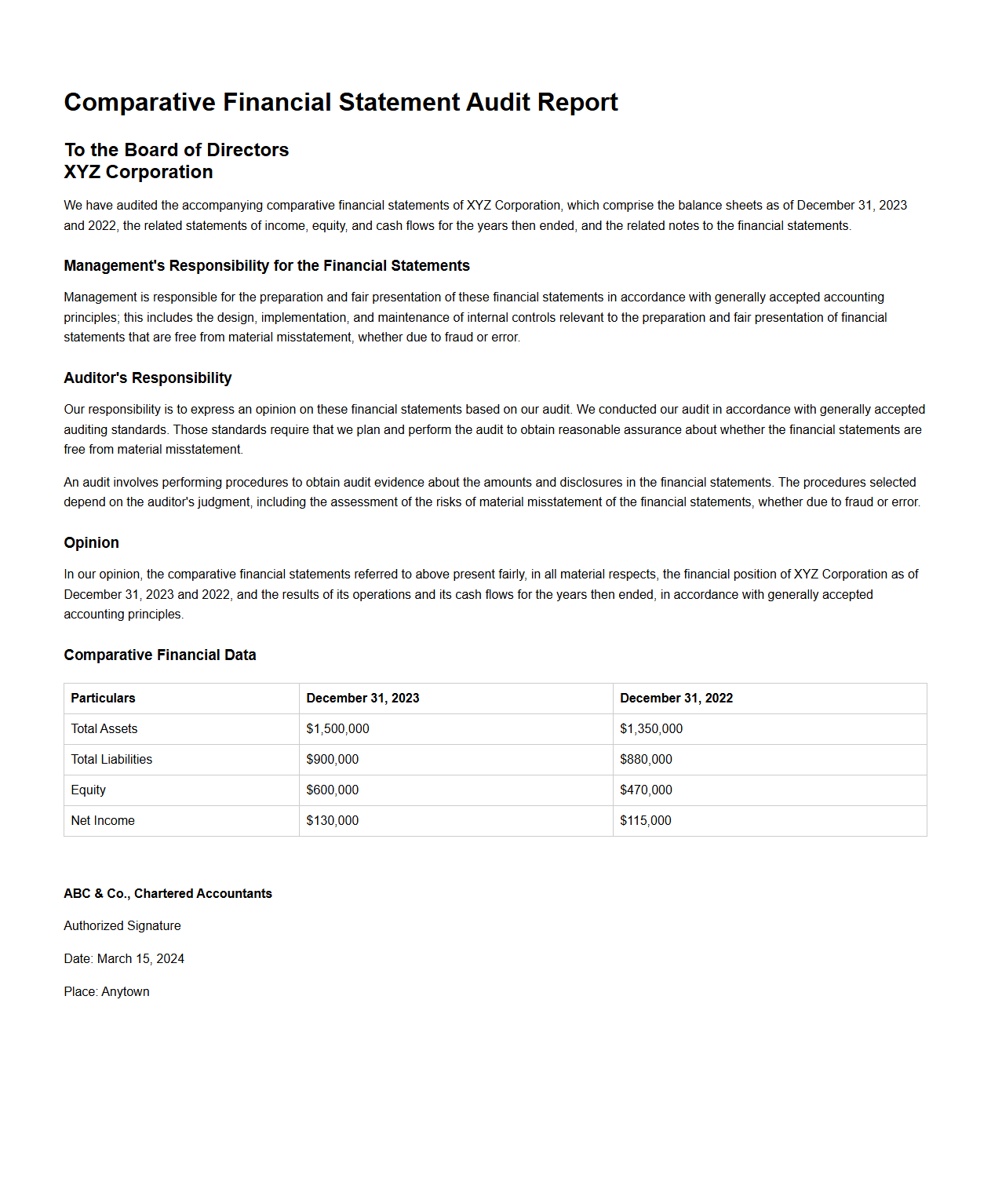

Comparative Financial Statement Audit Report Format

A

Comparative Financial Statement Audit Report Format document outlines the standardized structure used by auditors to present findings on multi-period financial statements. It ensures consistency in reporting key audit opinions, accounting policies, and financial data comparisons over different fiscal years. This format enhances transparency and aids stakeholders in assessing the organization's financial performance shifts accurately.

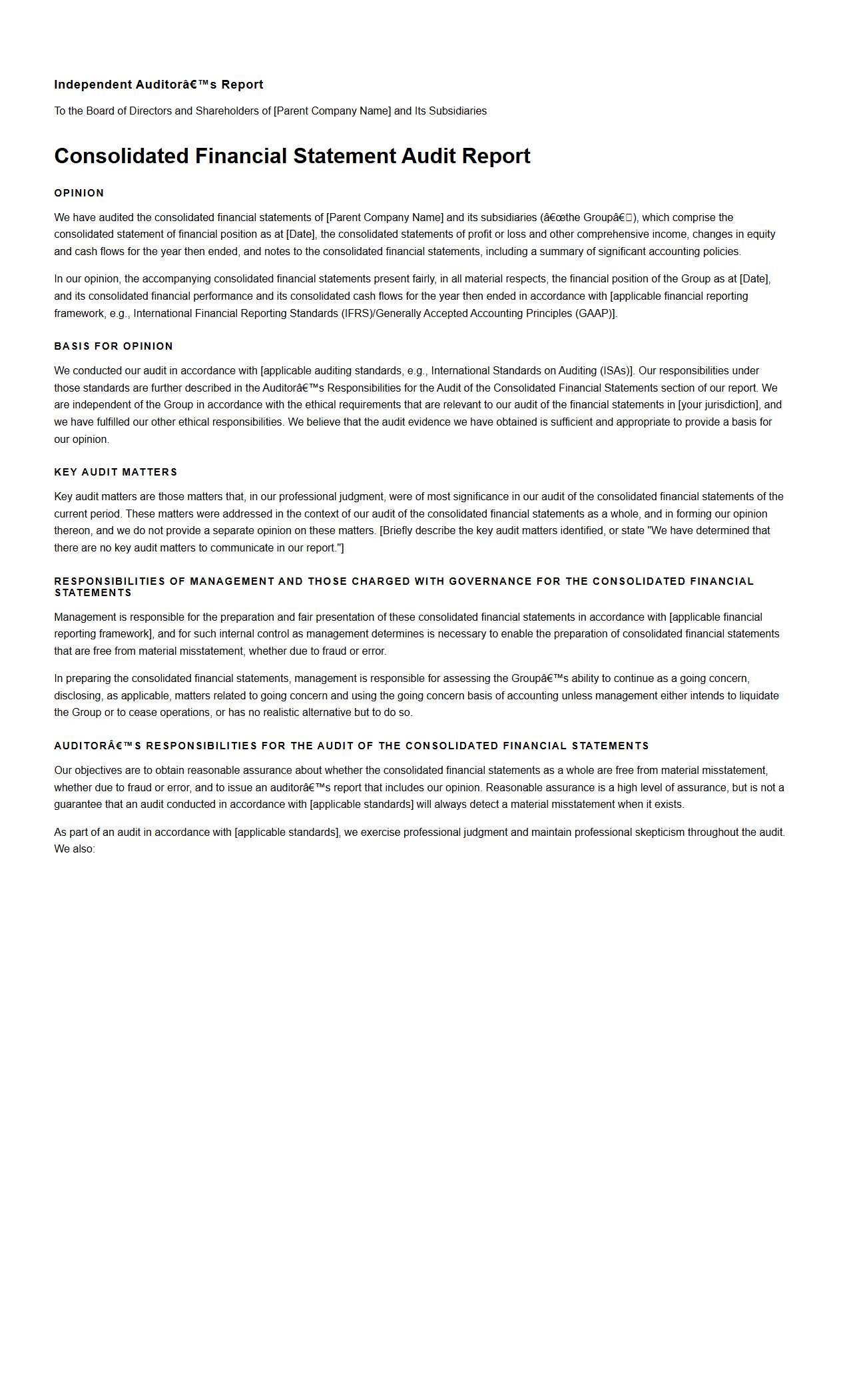

Consolidated Financial Statement Audit Report Format

The

Consolidated Financial Statement Audit Report Format document outlines the standardized structure and essential components required for auditing and reporting on consolidated financial statements of a parent company and its subsidiaries. It ensures compliance with regulatory standards such as IFRS or GAAP, providing clarity on auditor opinions, scope, and key audit findings. This format is critical for stakeholders to assess the financial health and performance of the entire corporate group accurately.

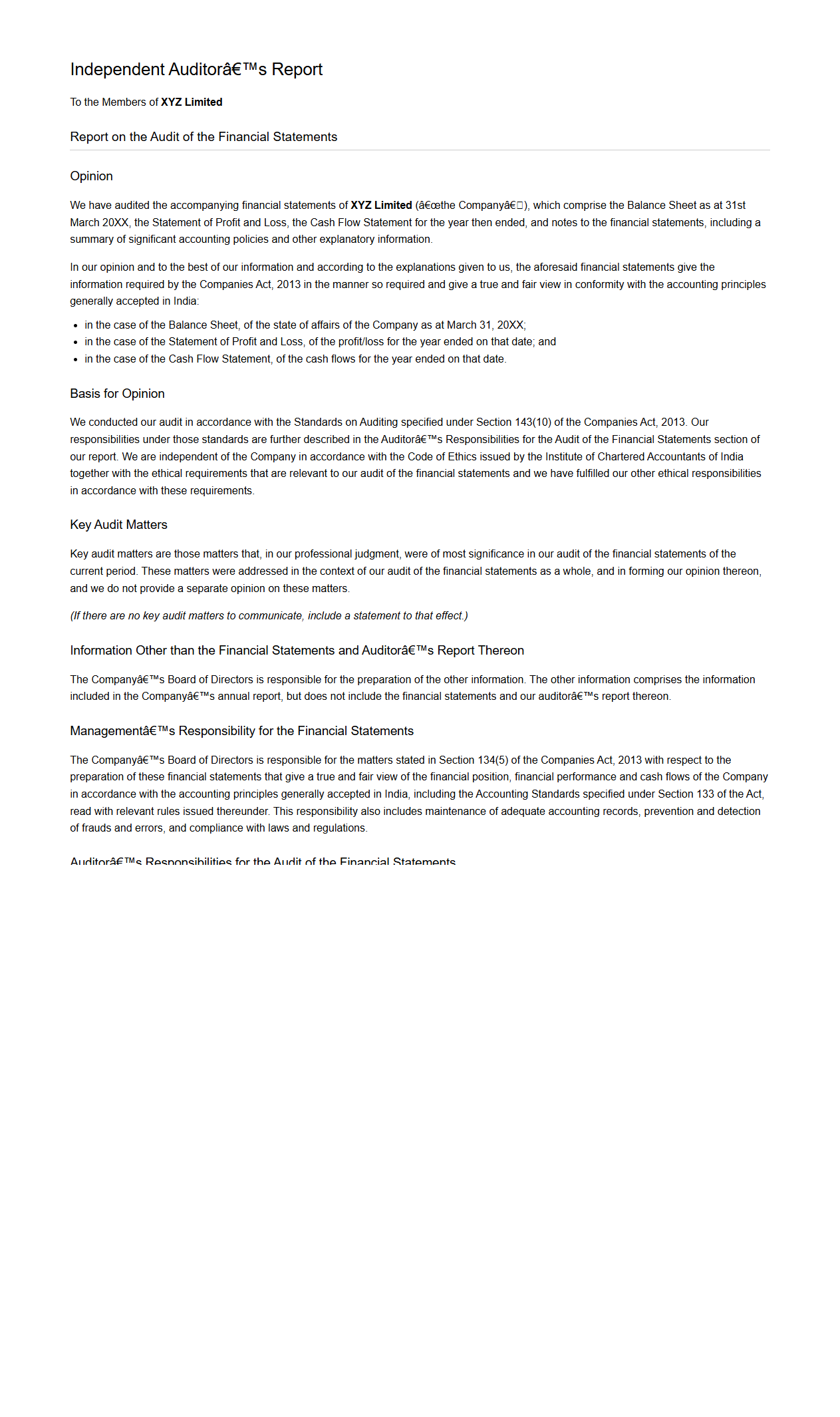

Statutory Audit Report Format

A

Statutory Audit Report Format document outlines the standardized structure and essential components required for presenting audit findings in compliance with legal and regulatory requirements. It typically includes sections such as the auditor's opinion, basis for opinion, responsibilities of management and auditors, and key audit findings, ensuring clarity and transparency for stakeholders. This format helps maintain uniformity and credibility in financial reporting across organizations.

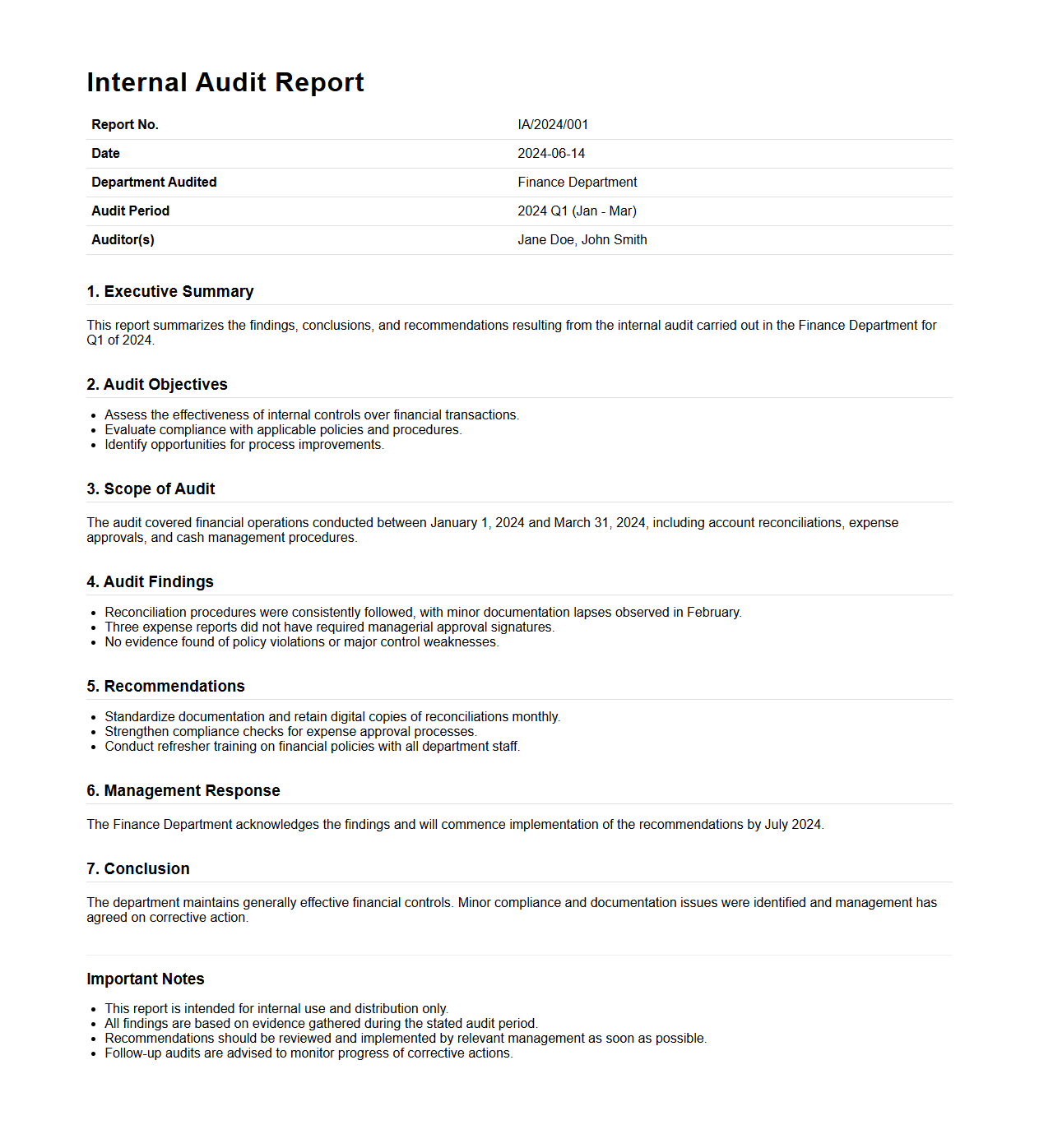

Internal Audit Report Format

An

Internal Audit Report Format document provides a structured template used to systematically present the findings, observations, and recommendations from an internal audit. It ensures consistency, clarity, and completeness by including sections such as objectives, scope, methodology, audit findings, and action plans. This format supports effective communication between auditors and management, aiding in risk management and operational improvements.

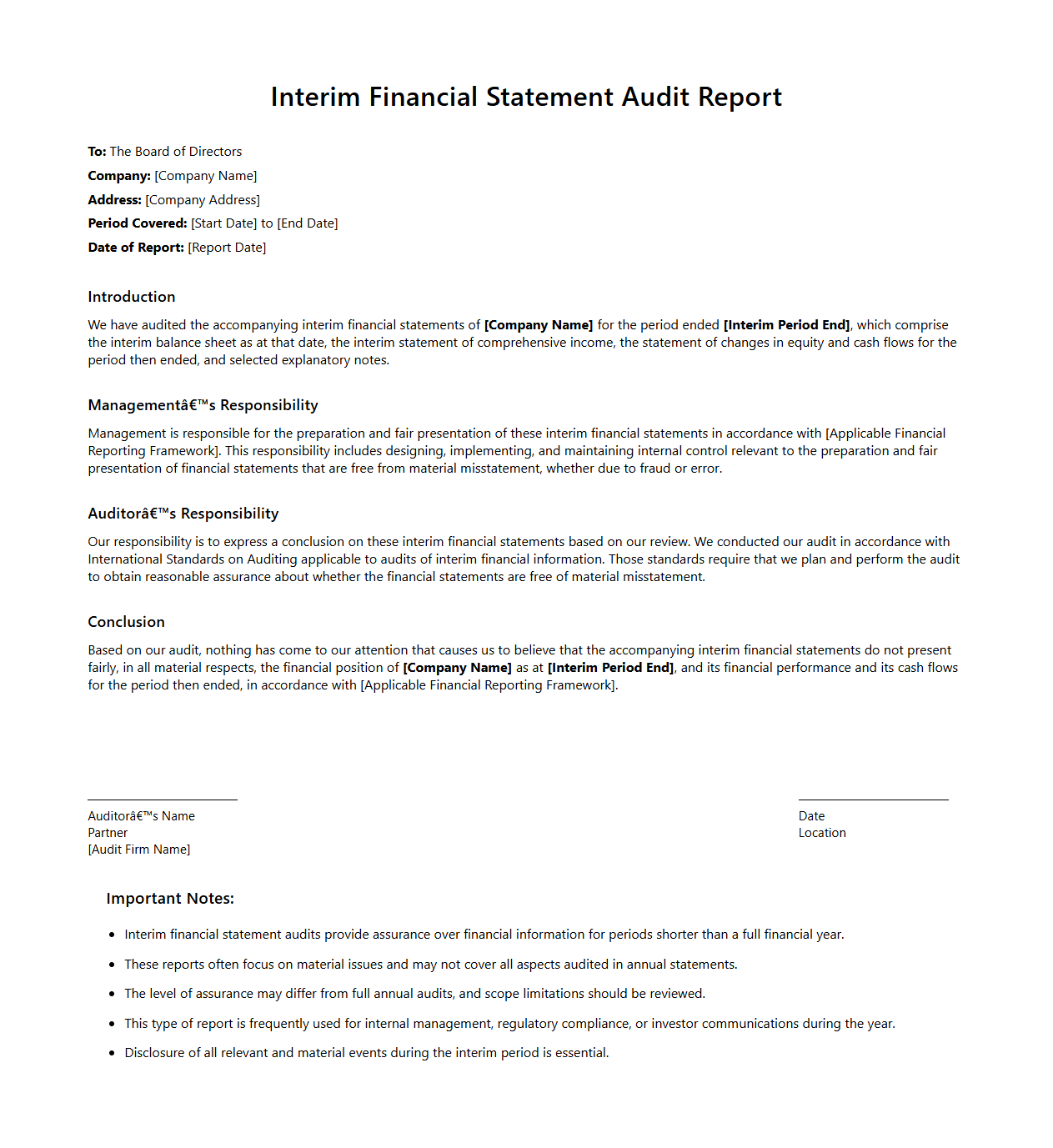

Interim Financial Statement Audit Report Format

The

Interim Financial Statement Audit Report Format document outlines the standardized structure and key components required for auditors to present their findings during a company's interim financial review. This format ensures clarity, consistency, and compliance with regulatory standards, facilitating stakeholders' understanding of the organization's financial position midway through the fiscal year. It typically includes sections on audit scope, methodology, identified issues, and conclusions based on the interim financial data.

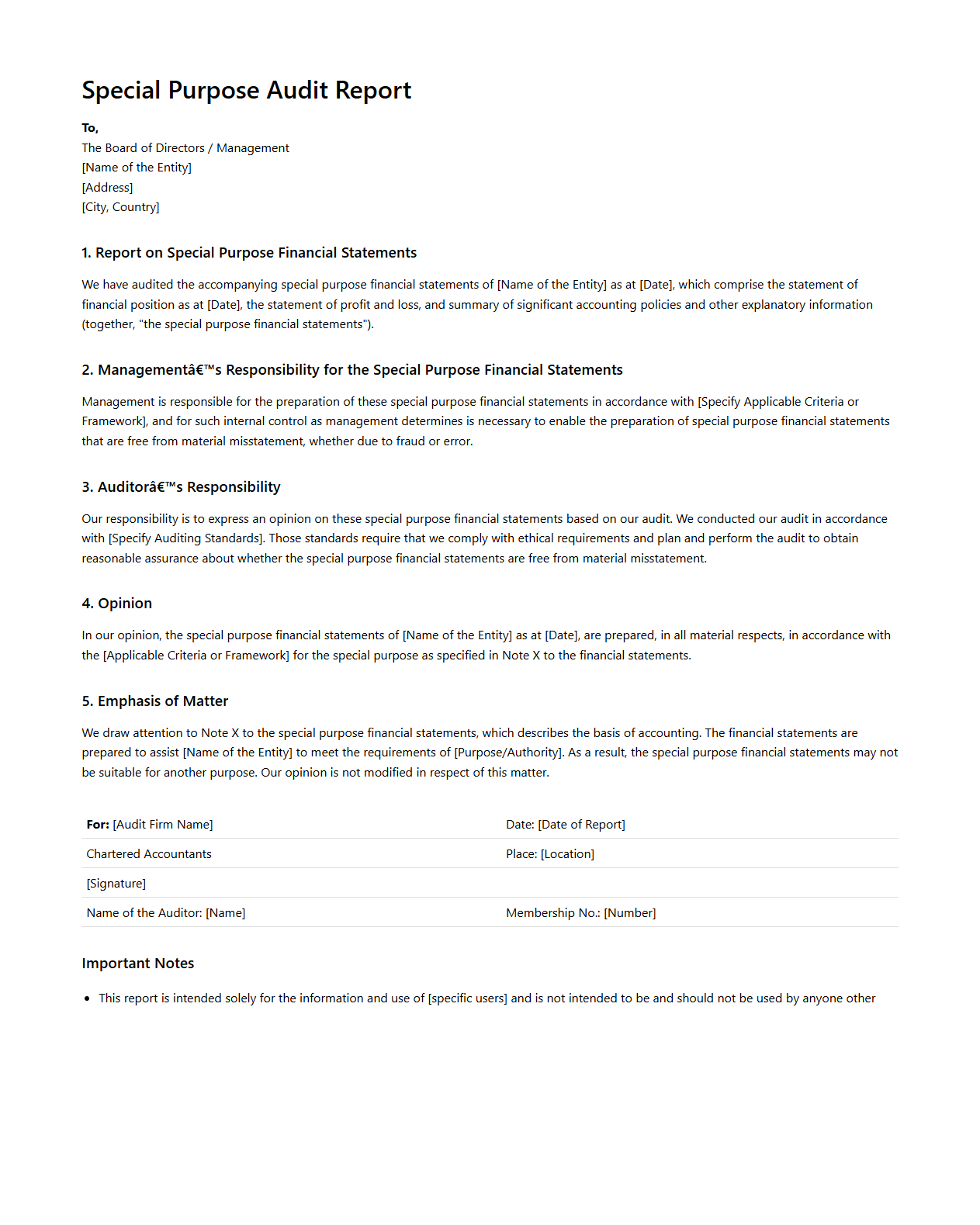

Special Purpose Audit Report Format

The

Special Purpose Audit Report Format document outlines the standardized way auditors present their findings for specific assignments tailored to unique client needs or regulatory requirements. It ensures clarity and consistency in reporting deviations, compliance, or particular financial data, facilitating targeted decision-making for stakeholders. This format typically includes scope, objectives, methodology, and detailed observations pertinent to the special purpose engagement.

Mandatory Sections in a Standard Audit Report Format for Financial Statements

The mandatory sections in a standard audit report include the Title, Addressee, Auditor's Opinion, Basis for Opinion, Key Audit Matters (if applicable), Responsibilities of Management and Those Charged with Governance, Auditor's Responsibilities, and the Signature with Date and Auditor's Address. Each section serves a unique purpose to enhance transparency and clarity regarding the audit process and findings. Including these sections ensures the report complies with professional standards and provides stakeholders with essential information.

Structure of the Auditor's Opinion Paragraph in the Audit Report

The auditor's opinion paragraph must clearly state the auditor's conclusion on the financial statements' fairness and compliance with the applicable financial reporting framework. It starts with identifying the financial statements audited, followed by the auditor's opinion on whether they present fairly, in all material respects. The opinion should be concise, unambiguous, and expressed in accordance with auditing standards to avoid misinterpretation.

Specific Wording Differentiating an Unqualified Audit Report from a Qualified One

An unqualified audit report includes wording that the financial statements present fairly, in all material respects, without reservations. In contrast, a qualified audit report uses phrases like "except for" or "except as noted" to indicate exceptions or limitations that prevent a clean opinion. This wording signals that the auditor encountered issues that are material but not pervasive enough to warrant an adverse opinion or disclaimer.

Required Disclosures for Emphasis of Matter and Other Matter Paragraphs

The emphasis of matter paragraph highlights matters appropriately disclosed in the financial statements but of such importance that they are fundamental to users' understanding. The other matter paragraph adds information not disclosed in the financial statements but relevant to users' understanding of the audit, auditor's responsibilities, or the audit report. Both paragraphs must clearly state the reason for their inclusion and reference related disclosures or circumstances.

Compliance of the Audit Report Format with International Standards Like ISA 700

The audit report format must adhere to ISA 700 by ensuring clarity, completeness, and consistency in the presentation of the auditor's opinion and related sections. It requires the inclusion of specific elements such as a title, addressee, auditor's opinion, basis for opinion, responsibilities, and signature, enhancing comparability across jurisdictions. Compliance with ISA 700 promotes the reliability and international acceptance of the audit report.