The Format of Materiality Calculation Sheet for Audits includes sections for identifying quantitative and qualitative factors that influence materiality thresholds. It typically outlines the basis for selecting benchmarks such as total revenue or net assets and provides clear formulas for calculating preliminary and revised materiality levels. The sheet ensures consistent documentation to support audit planning and risk assessment.

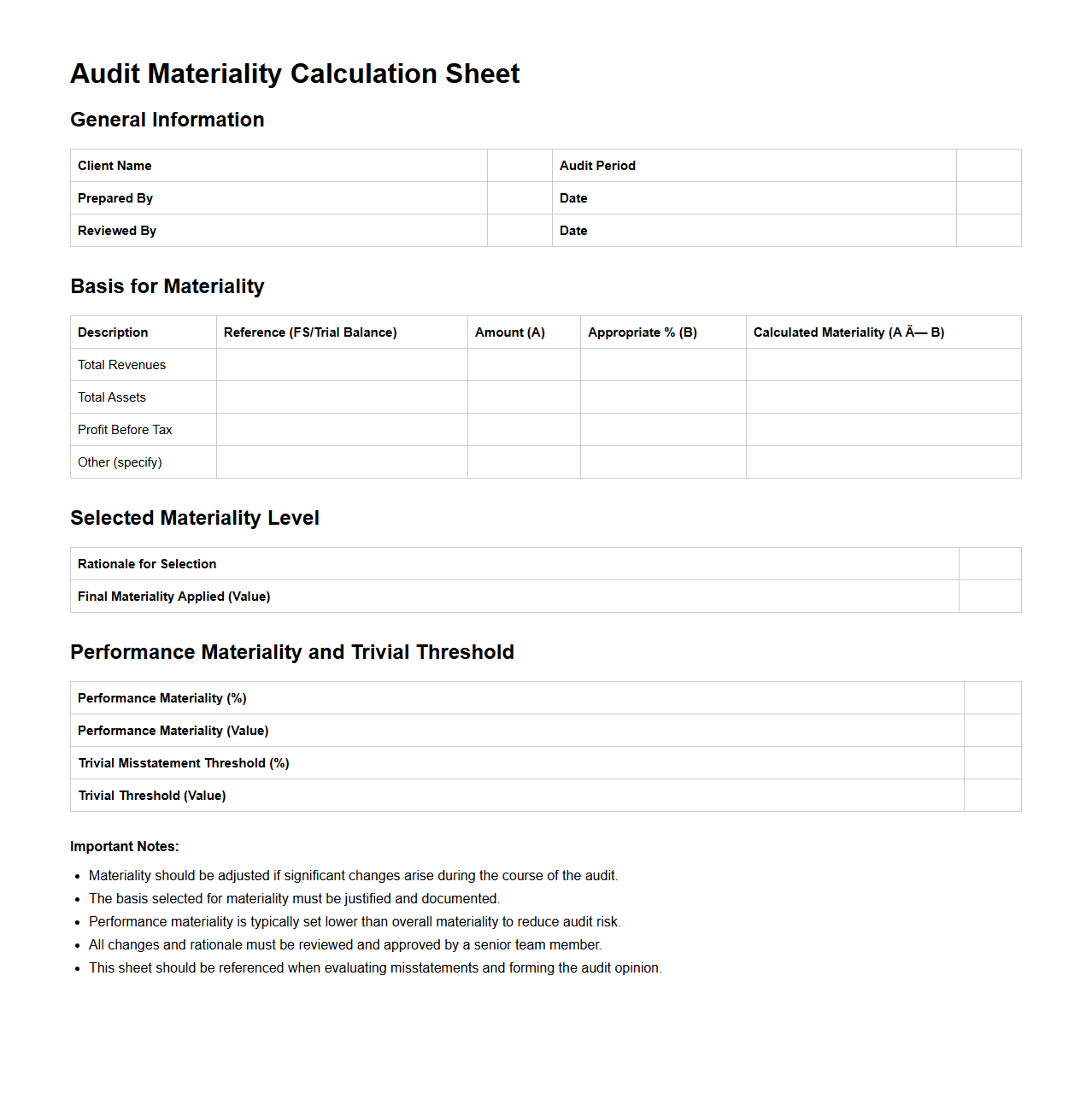

Audit Materiality Calculation Sheet Template

The

Audit Materiality Calculation Sheet Template document is a structured tool used by auditors to determine the threshold of materiality in financial audits. It assists in quantifying materiality by incorporating relevant financial data, risk factors, and predefined formulas, ensuring accurate assessment of significant misstatements. This template enhances consistency and transparency in audit planning and decision-making processes.

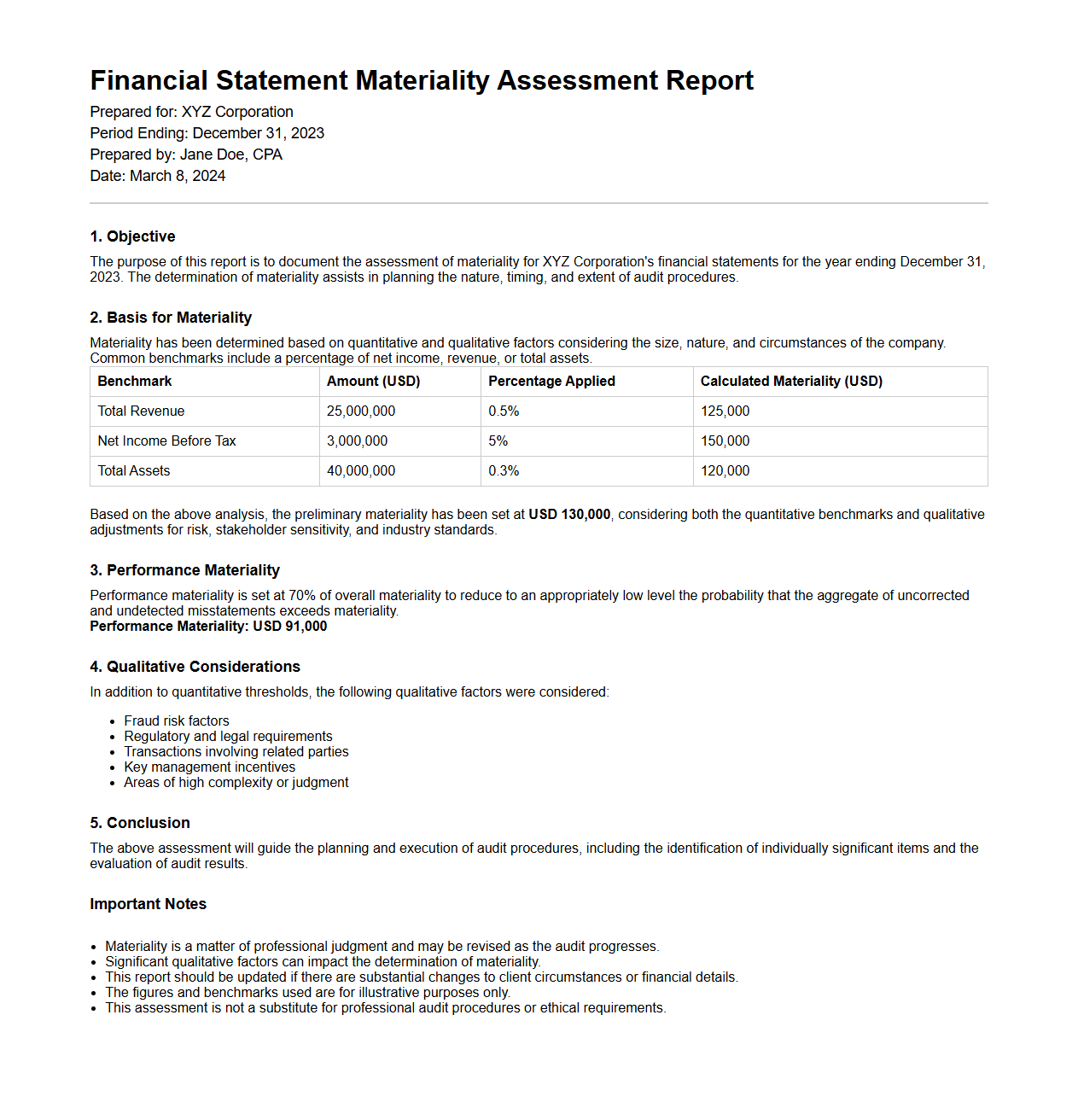

Financial Statement Materiality Assessment Report

A

Financial Statement Materiality Assessment Report is a crucial document used to evaluate and quantify the significance of financial information within a company's financial statements. It helps auditors and management determine which items or discrepancies could influence economic decisions made by users of the financial reports. This report ensures accurate, reliable financial disclosure by identifying material misstatements that require correction or further investigation.

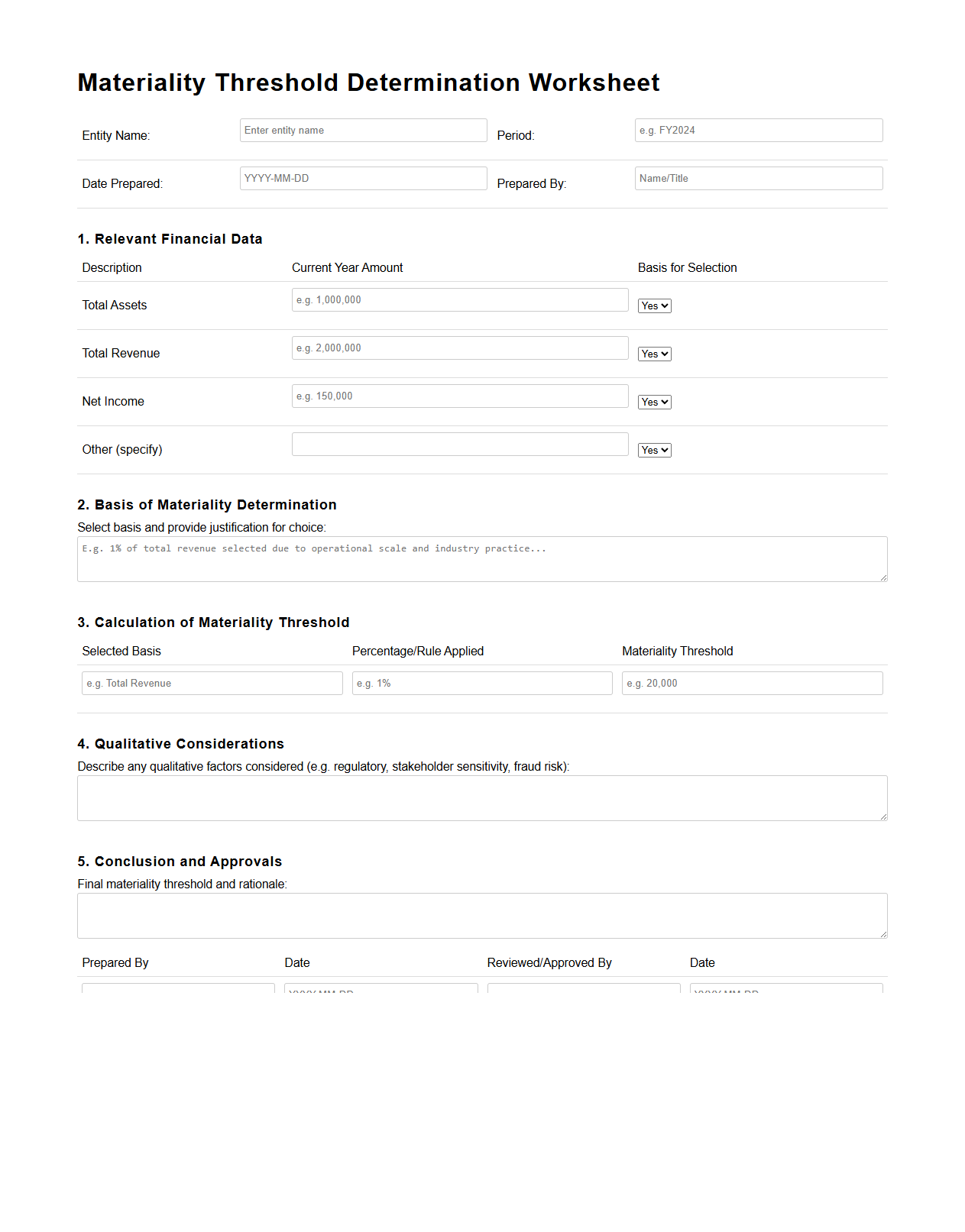

Materiality Threshold Determination Worksheet

The

Materiality Threshold Determination Worksheet document is used to establish quantitative and qualitative criteria that define the significance of financial statement items during an audit or financial review. It helps auditors and accountants identify the threshold above which misstatements are considered material and potentially impactful to decision-making processes. This document ensures consistent evaluation of materiality levels in accordance with regulatory standards and auditing guidelines.

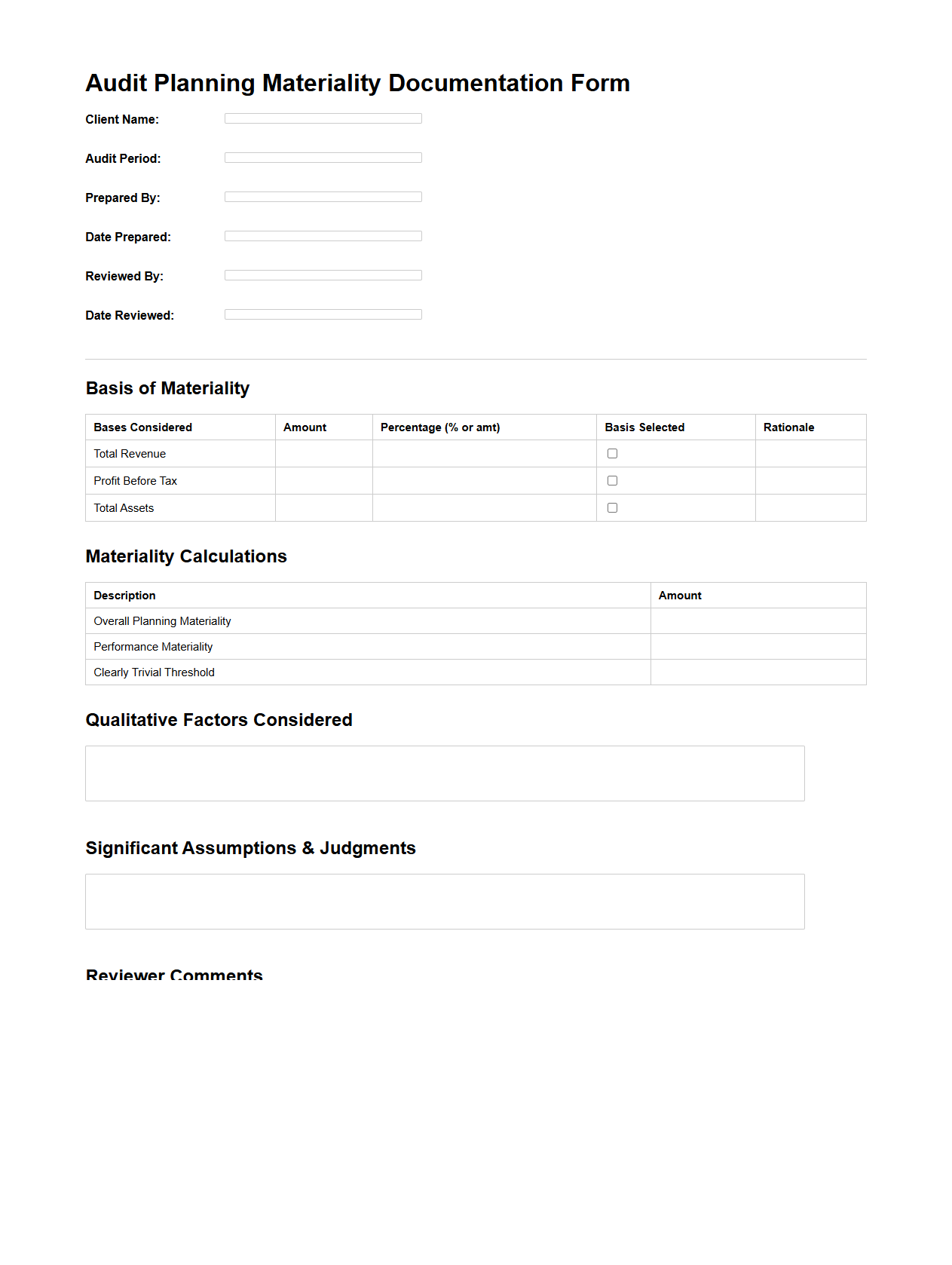

Audit Planning Materiality Documentation Form

The

Audit Planning Materiality Documentation Form is a crucial document used by auditors to establish and record the materiality thresholds during the planning phase of an audit. This form helps ensure that the audit focuses on significant financial statement areas by setting quantitative and qualitative benchmarks based on entity size and risk factors. Proper documentation supports audit quality, compliance with auditing standards, and facilitates effective communication among audit team members.

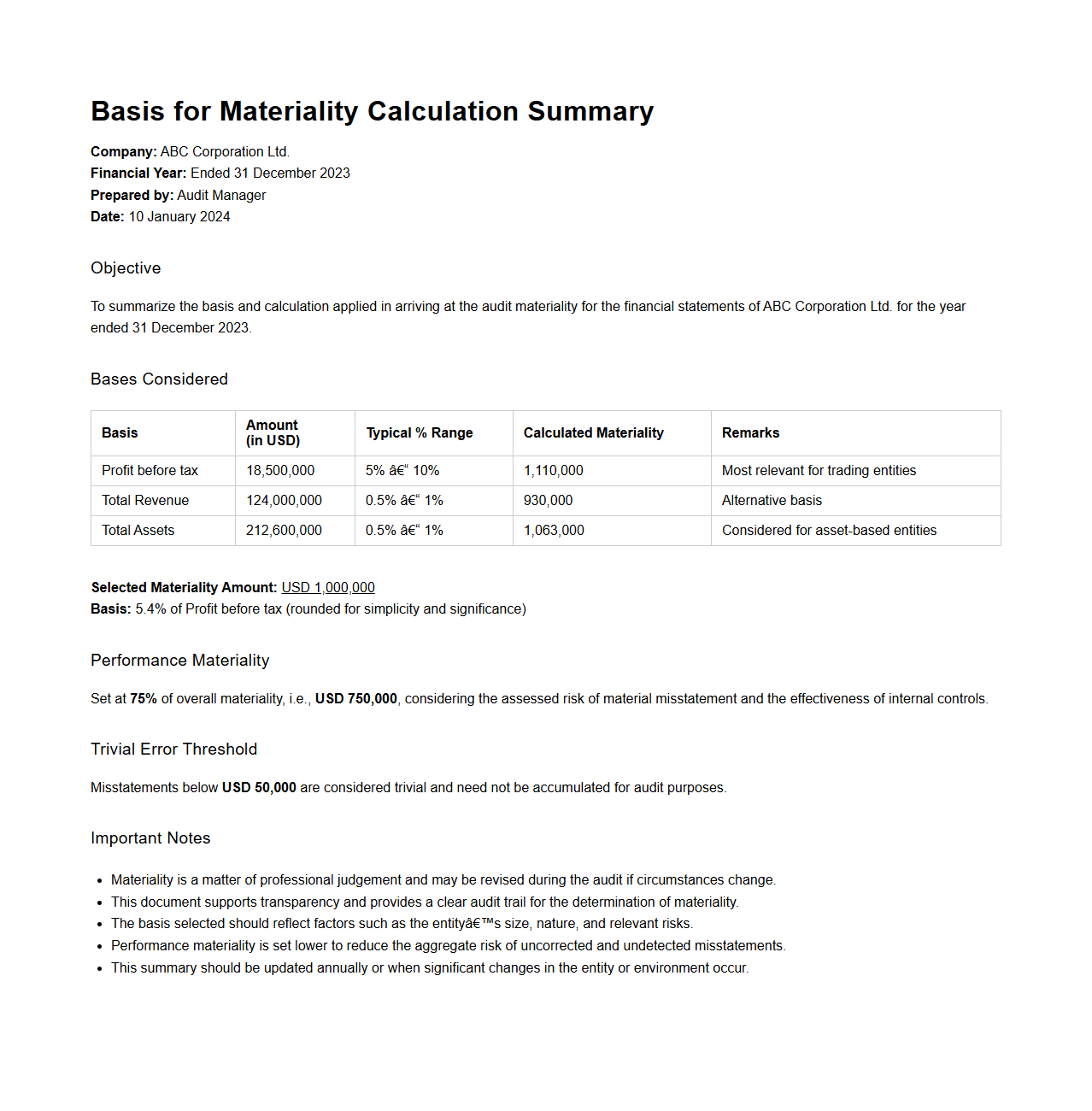

Basis for Materiality Calculation Summary

The Basis for Materiality Calculation Summary document outlines the criteria and quantitative thresholds used to determine materiality in financial reporting and auditing processes. It serves as a crucial reference for assessing which financial information is significant enough to influence decision-making by stakeholders. This document ensures transparency and consistency by detailing the rationale behind selecting specific materiality levels, supporting compliance with auditing standards and regulatory requirements.

Materiality Calculation is essential for accurate and reliable financial analysis.

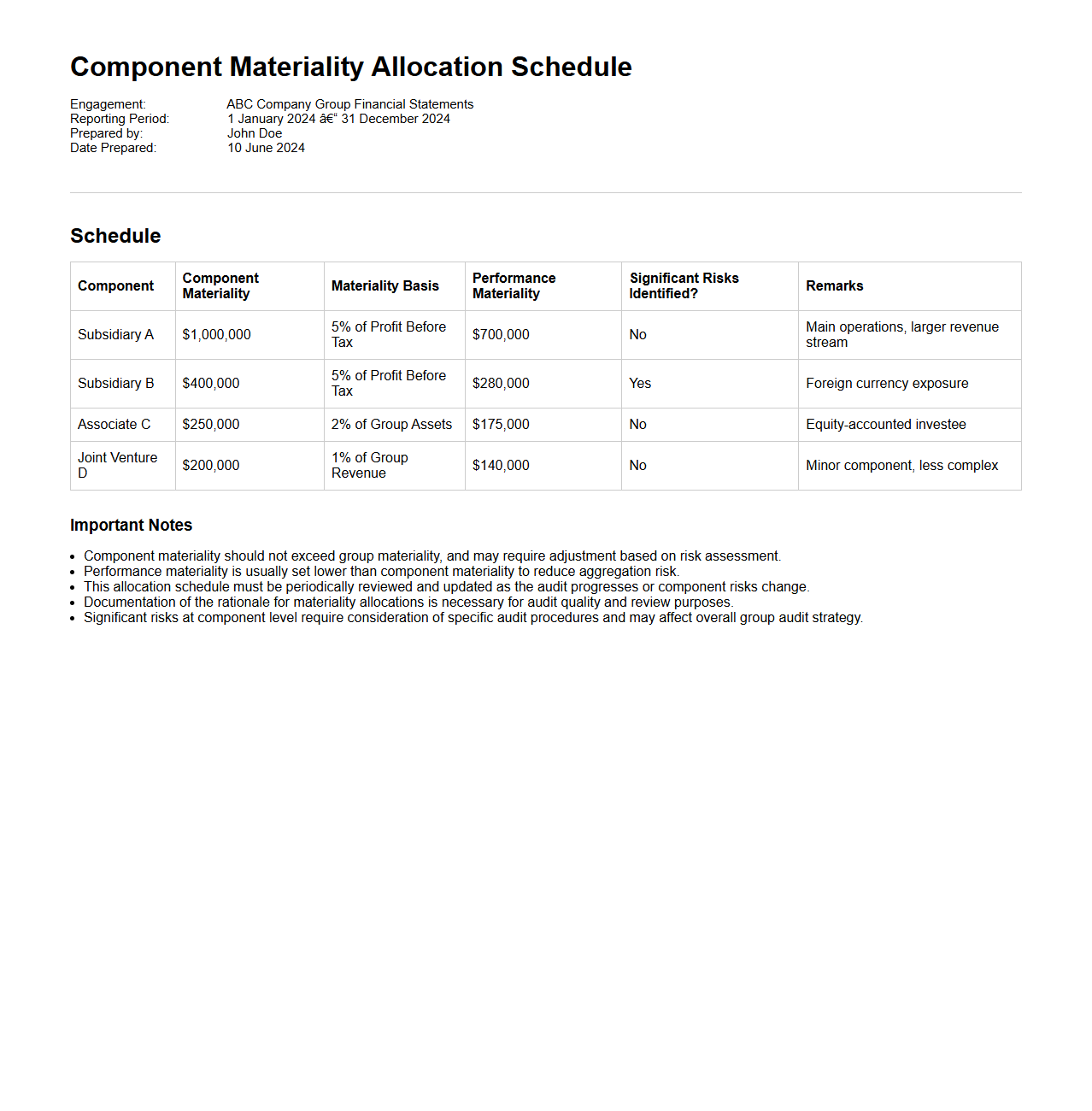

Component Materiality Allocation Schedule

The

Component Materiality Allocation Schedule document is a detailed framework used in financial reporting and auditing to allocate materiality thresholds to individual components or segments of an organization. It ensures that the materiality levels are appropriately assigned based on the size, risk, and significance of each component, facilitating accurate assessment and control of financial information. This document supports targeted audit procedures and enhances the reliability of consolidated financial statements by addressing component-level risks.

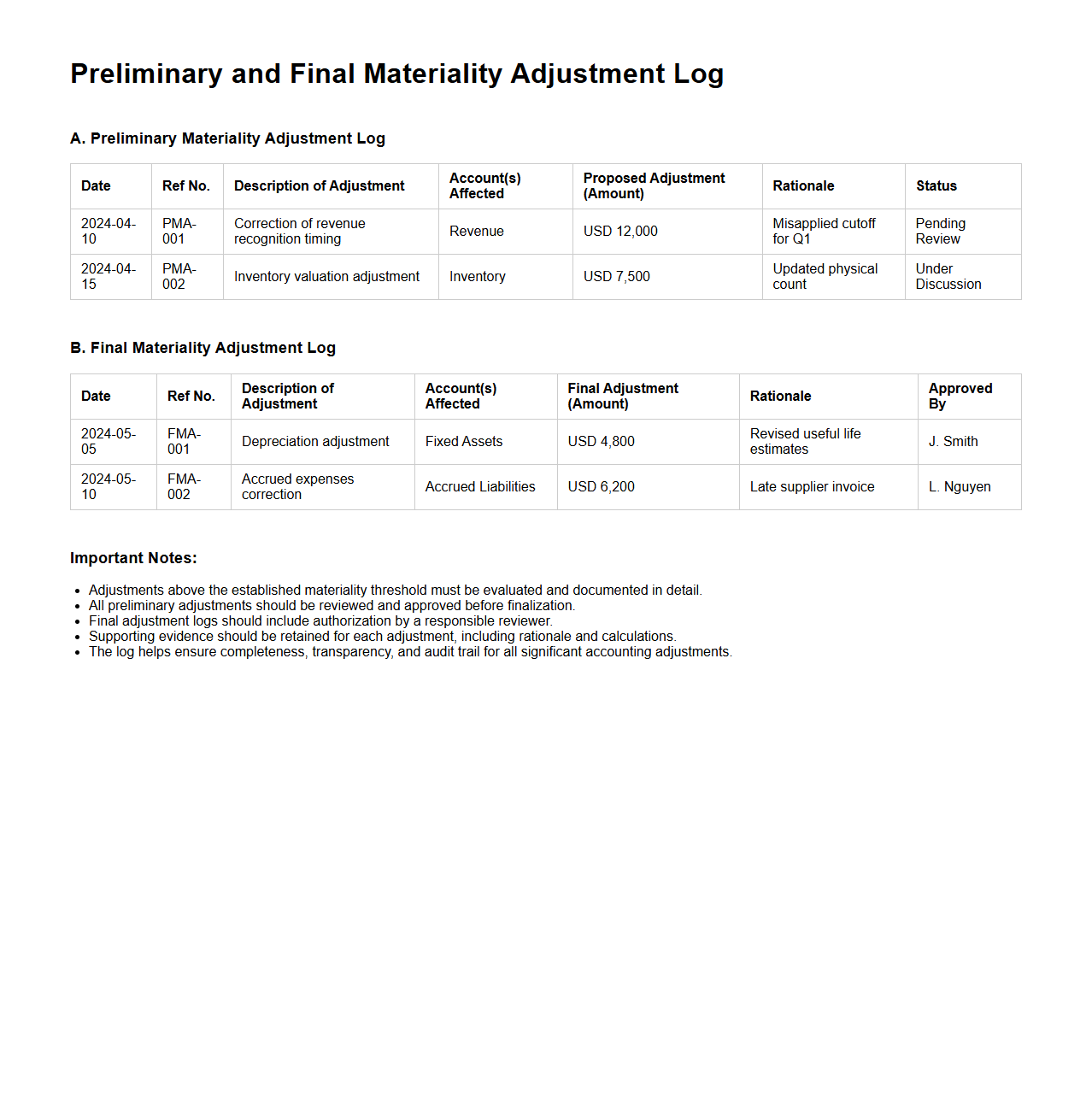

Preliminary and Final Materiality Adjustment Log

The

Preliminary and Final Materiality Adjustment Log document is a critical tool used in auditing and financial reporting to track and record all adjustments identified during the audit process that may affect the overall financial statements. It helps in documenting the magnitude and nature of errors or misstatements found, ensuring that they fall within acceptable materiality thresholds before final approval. This log enhances transparency, supports audit conclusions, and ensures compliance with accounting standards and regulatory requirements.

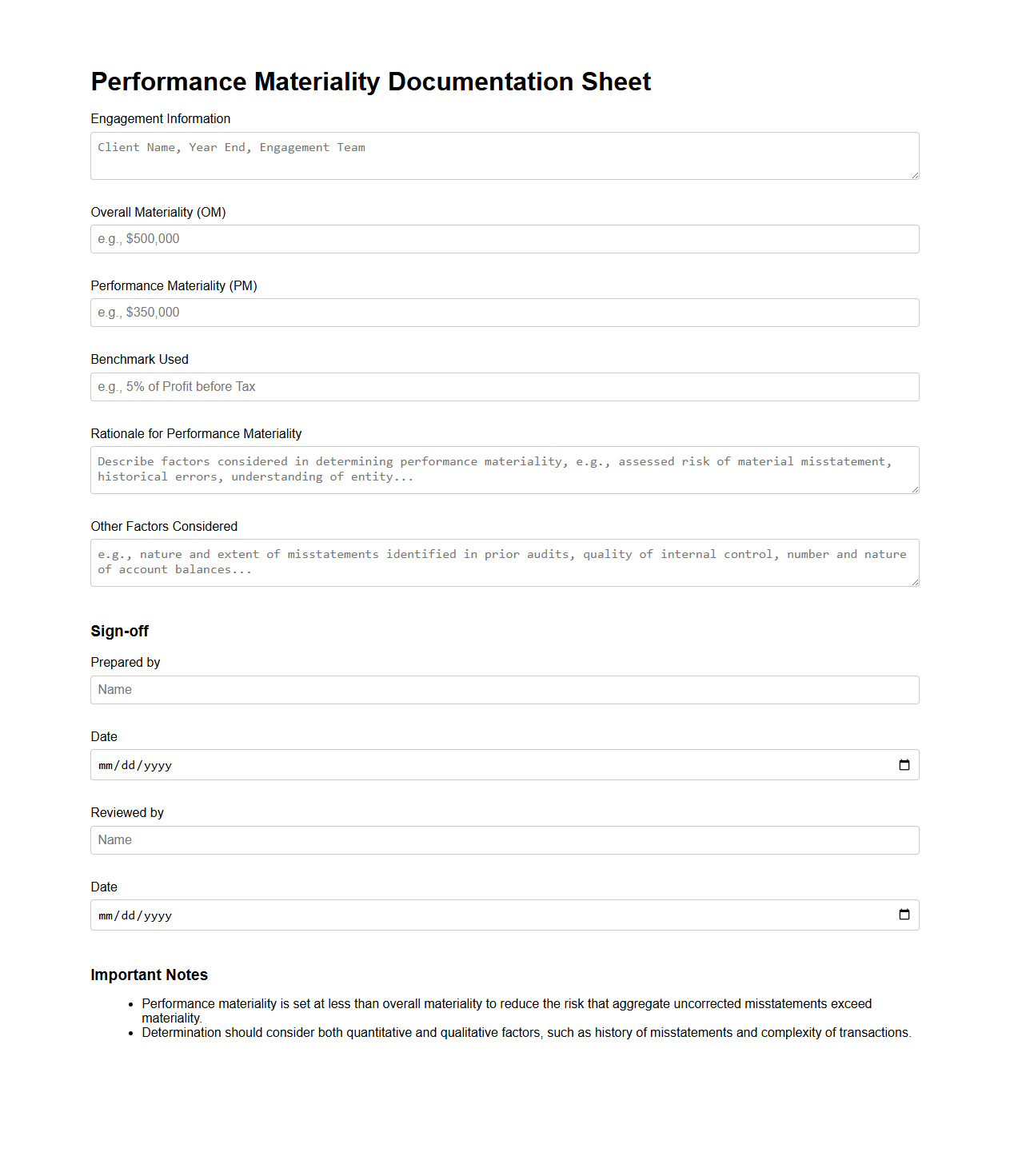

Performance Materiality Documentation Sheet

The

Performance Materiality Documentation Sheet is a critical audit document that outlines the threshold set below overall materiality to reduce the risk of undetected misstatements. It serves as a detailed record of the auditor's judgment on performance materiality levels, enhancing the clarity and consistency of the audit approach. This sheet supports compliance with auditing standards by ensuring that detected discrepancies remain within acceptable limits, improving the reliability of financial statements.

Materiality for Misstatements Tracking Table

The

Materiality for Misstatements Tracking Table document serves as a critical tool in the audit process, defining the threshold at which misstatements become significant enough to impact financial statements. It helps auditors prioritize and evaluate identified errors or discrepancies based on their potential effect on the overall accuracy and fairness of the financial reports. By setting clear materiality benchmarks, this document ensures consistent assessment and documentation of misstatements, supporting informed decision-making and regulatory compliance.

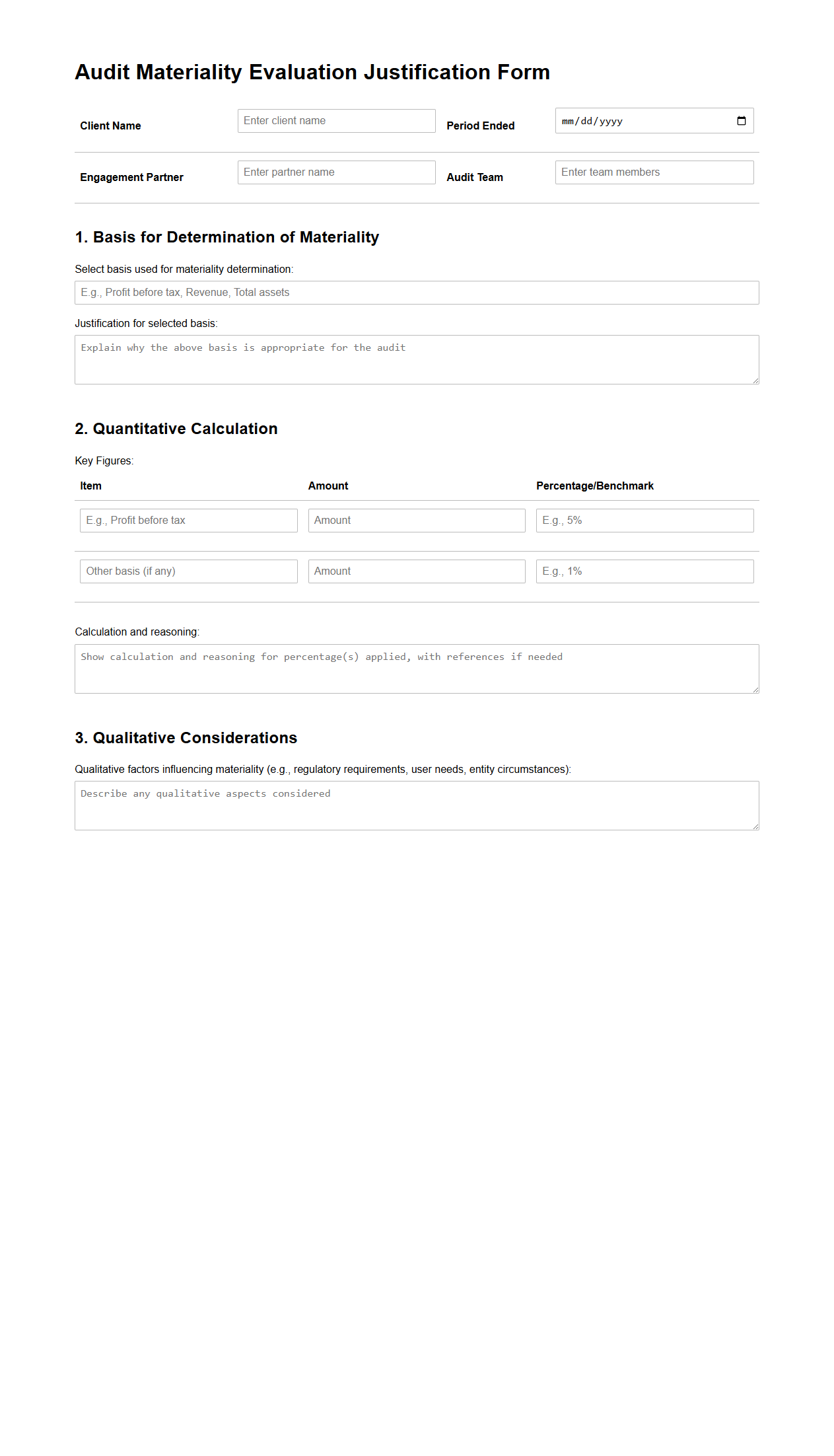

Audit Materiality Evaluation Justification Form

The

Audit Materiality Evaluation Justification Form document serves as a critical tool in the auditing process by providing a structured approach to determine the threshold of materiality for financial statements. This form guides auditors in justifying materiality decisions based on quantitative and qualitative factors, ensuring that assessed risks align with regulatory standards and organizational objectives. Proper documentation supports transparent communication with stakeholders and enhances the effectiveness of audit conclusions by focusing attention on significant financial information.

Key Components Required in a Materiality Calculation Sheet for Audit Documentation

The Materiality Calculation Sheet must include the benchmark figures used to determine materiality, such as total assets, revenue, or profit before tax. It should clearly show the rationale behind selecting the key performance indicators and the percentage thresholds applied. Additionally, the sheet must record any assumptions or professional judgments used during the calculation process.

Presentation of Benchmarks and Thresholds in the Materiality Format

Benchmarks and thresholds must be presented in a clear and structured manner, typically in tabular form for ease of review. Each benchmark should be linked to specific numerical thresholds expressed as percentages or fixed amounts to define the materiality level. Transparency in showing how these figures align with auditing standards enhances the reliability of the materiality assessment.

Supporting Schedules Accompanying the Materiality Calculation Sheet in Audit Files

The calculation sheet should be supported by detailed schedules including financial statement extracts, comparative analysis, and risk assessment summaries. These schedules serve as evidence backing up the chosen benchmarks and thresholds, enhancing the audit's traceability and compliance. It is essential to cross-reference all supporting documentation within the audit files for comprehensive understanding.

Documentation Format Capturing Qualitative Versus Quantitative Materiality Considerations

A combined format utilizing both narrative descriptions and quantitative tables best captures the full scope of materiality considerations. Qualitative factors such as regulatory changes or management bias must be documented in written explanations. Meanwhile, quantitative data should be clearly tabulated, ensuring that all materiality factors are comprehensively recorded and easy to interpret.

Reflection and Justification of Adjustments to Preliminary Materiality in the Sheet

Any adjustments to the preliminary materiality figures must be clearly recorded along with detailed justifications explaining the reasons for the change. These justifications often relate to developments in audit risk assessments or new financial information arising during the audit. Maintaining an audit trail for such adjustments ensures the integrity and transparency of the materiality determination process.