The Format of Retained Earnings Statement for Profit typically begins with the opening balance of retained earnings, followed by the addition of net profit earned during the period. Dividends paid to shareholders are then deducted, resulting in the ending balance of retained earnings. This structured format helps in clearly presenting the changes in retained earnings over a specific timeframe.

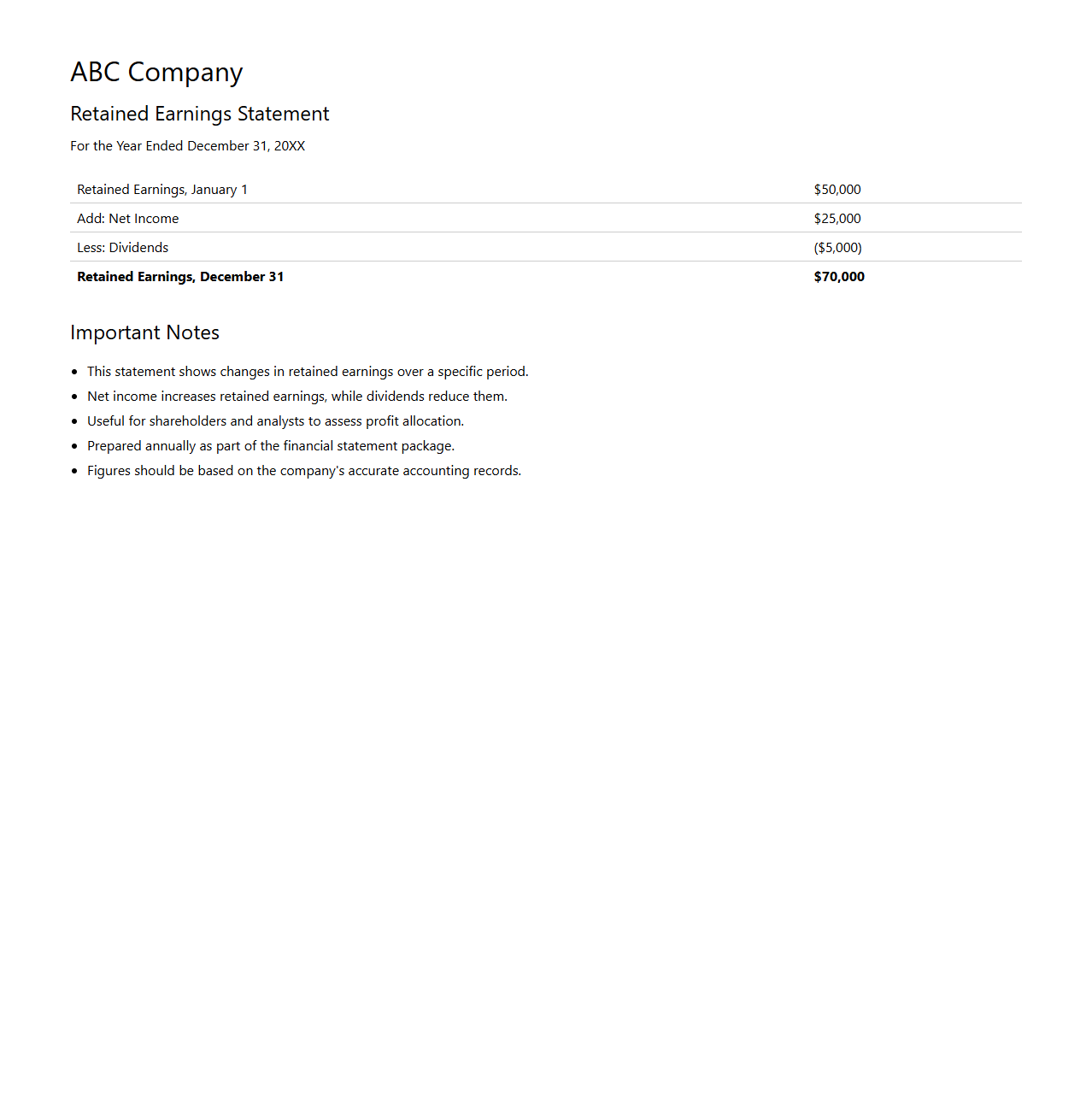

Basic Retained Earnings Statement Format

The

Basic Retained Earnings Statement Format document outlines the structure used to report changes in retained earnings over a specific accounting period. It typically includes the beginning retained earnings balance, net income or loss, dividends paid, and the ending retained earnings balance. This document is essential for investors and management to understand how profits are reinvested in the company or distributed.

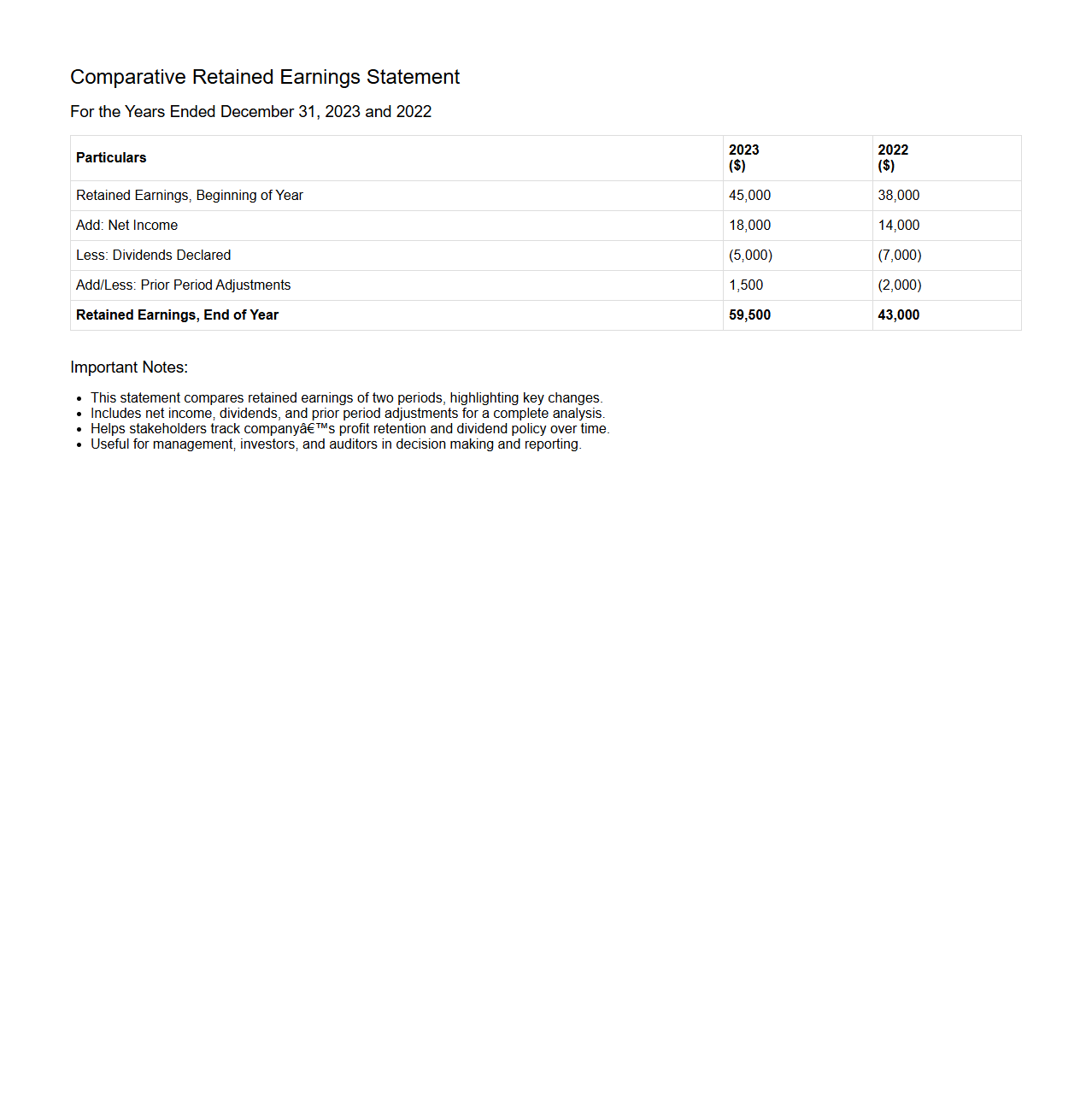

Comparative Retained Earnings Statement Format

The

Comparative Retained Earnings Statement Format document systematically presents retained earnings data over multiple periods, highlighting changes such as net income and dividends. This format aids in analyzing trends and evaluating a company's profitability and dividend distribution policies. It is essential for stakeholders to assess financial health and make informed investment decisions.

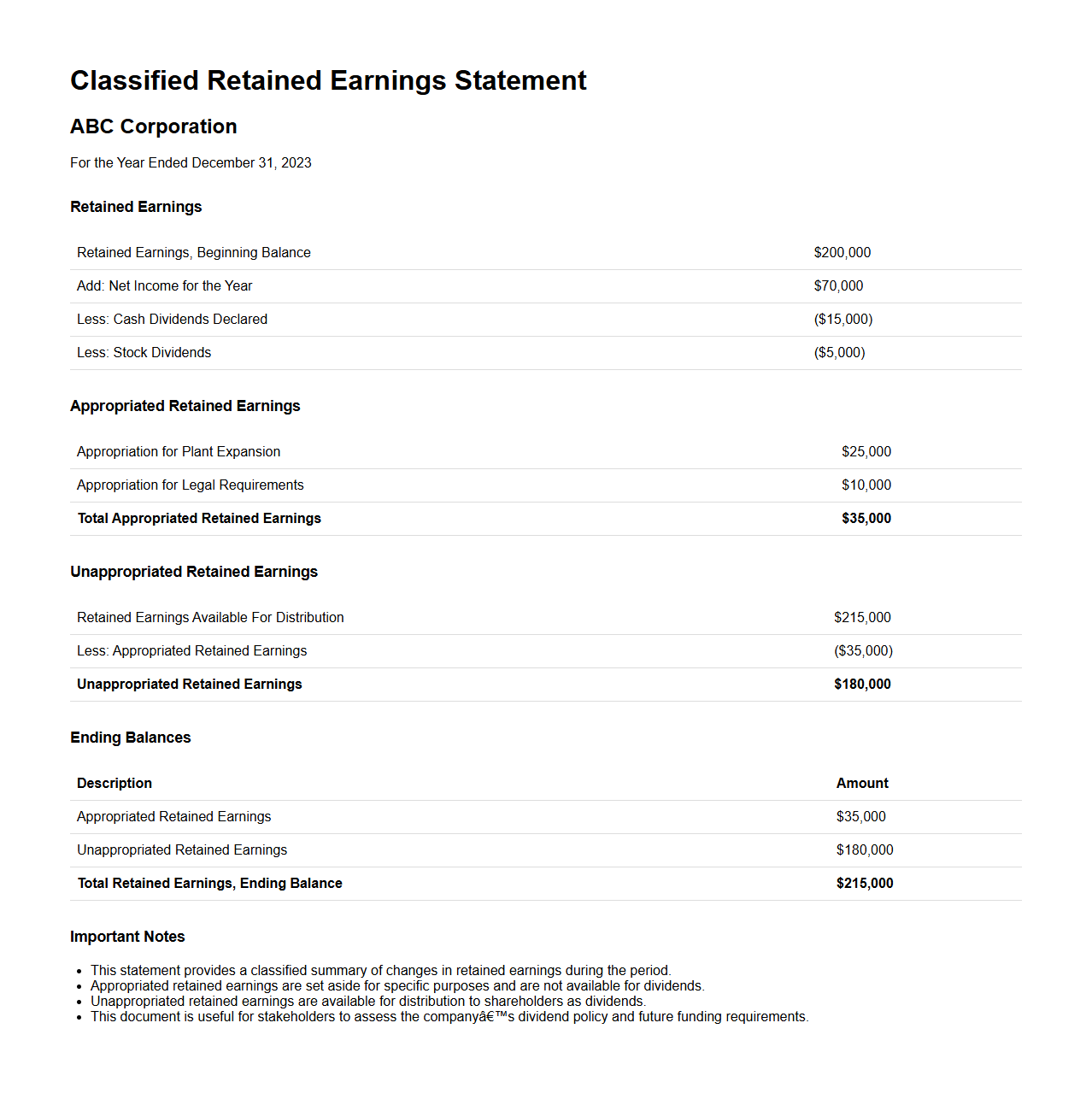

Classified Retained Earnings Statement Format

The

Classified Retained Earnings Statement Format is a structured financial document that categorizes retained earnings into distinct sections, such as beginning retained earnings, net income, dividends, and ending retained earnings. This format provides clarity by organizing these components systematically, facilitating easier analysis and transparency for stakeholders. It is essential for tracking the changes in a company's accumulated profits that are reinvested in the business rather than distributed as dividends.

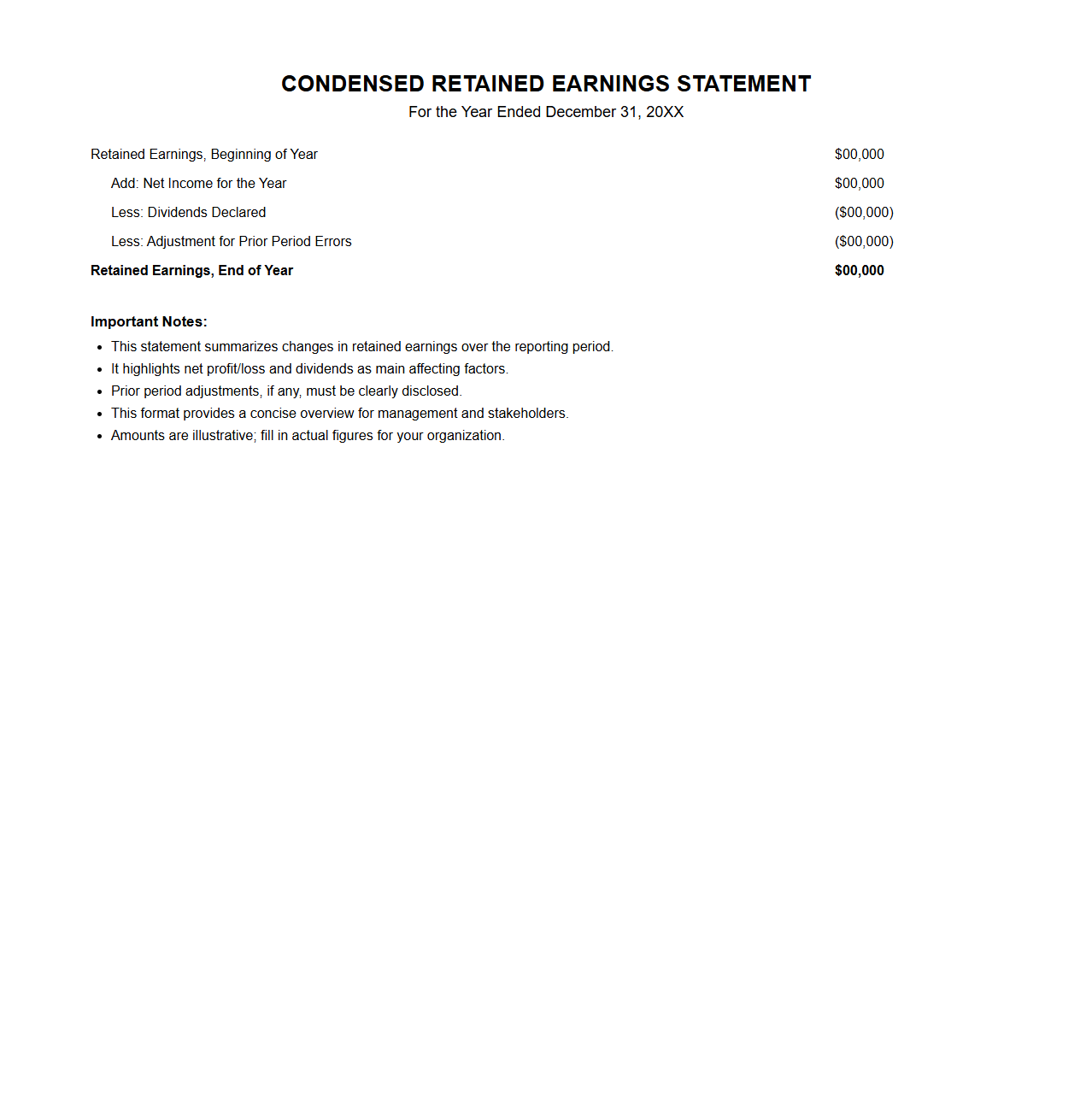

Condensed Retained Earnings Statement Format

The

Condensed Retained Earnings Statement Format document summarizes changes in retained earnings over a specific period, highlighting net income and dividends paid. This financial statement provides a quick snapshot of a company's earnings retained rather than distributed as dividends, essential for stakeholders assessing profitability and reinvestment strategies. It typically includes beginning retained earnings, additions from net income, deductions for dividends, and ending retained earnings balance.

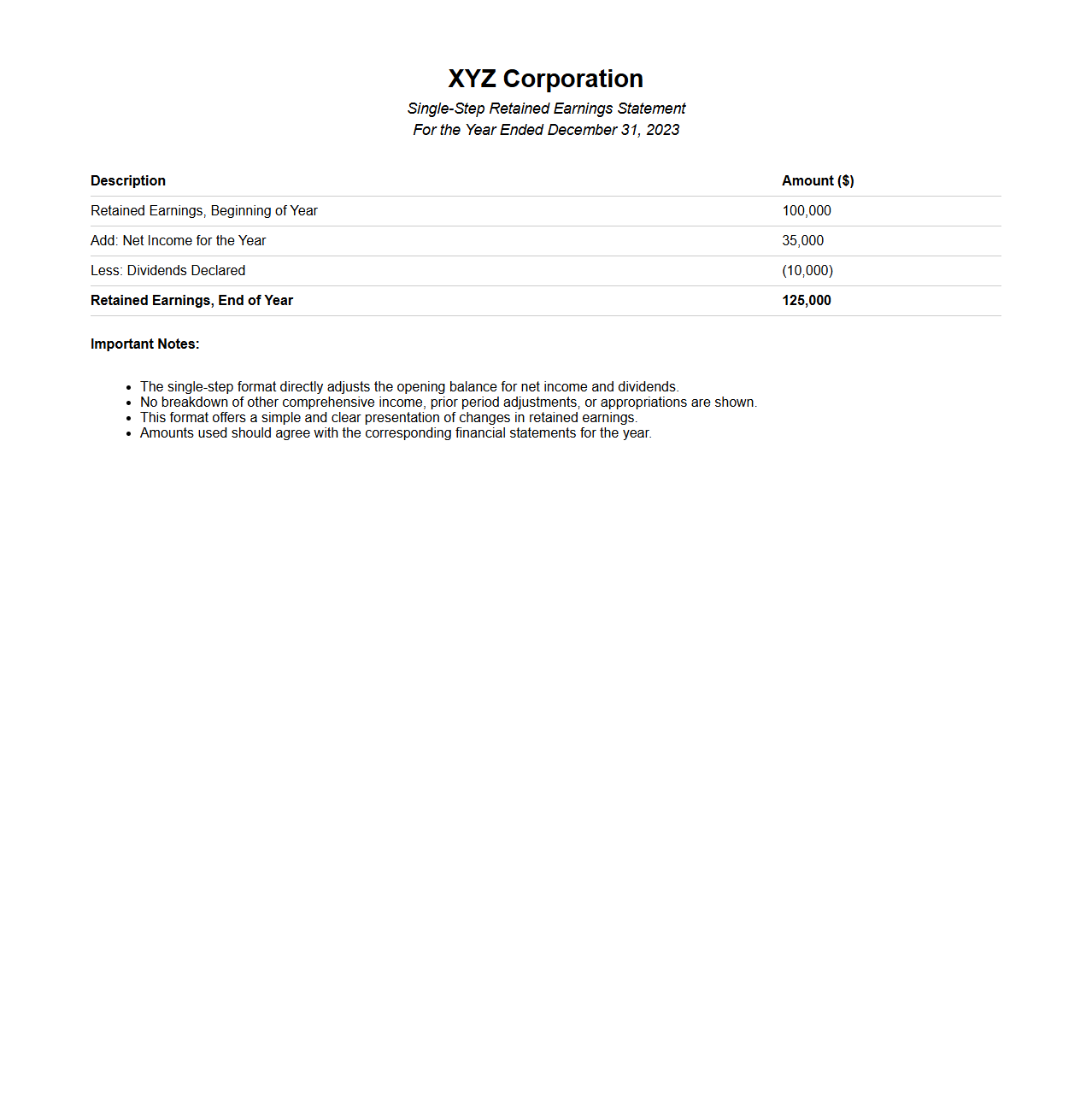

Single-Step Retained Earnings Statement Format

The

Single-Step Retained Earnings Statement Format document presents a clear and concise overview of a company's retained earnings changes during a specific period. It summarizes net income and dividends in a straightforward manner without separating operating and non-operating activities, making it easier for users to understand overall earnings retention. This format is essential for financial analysts and stakeholders to assess how profits are being retained or distributed as dividends.

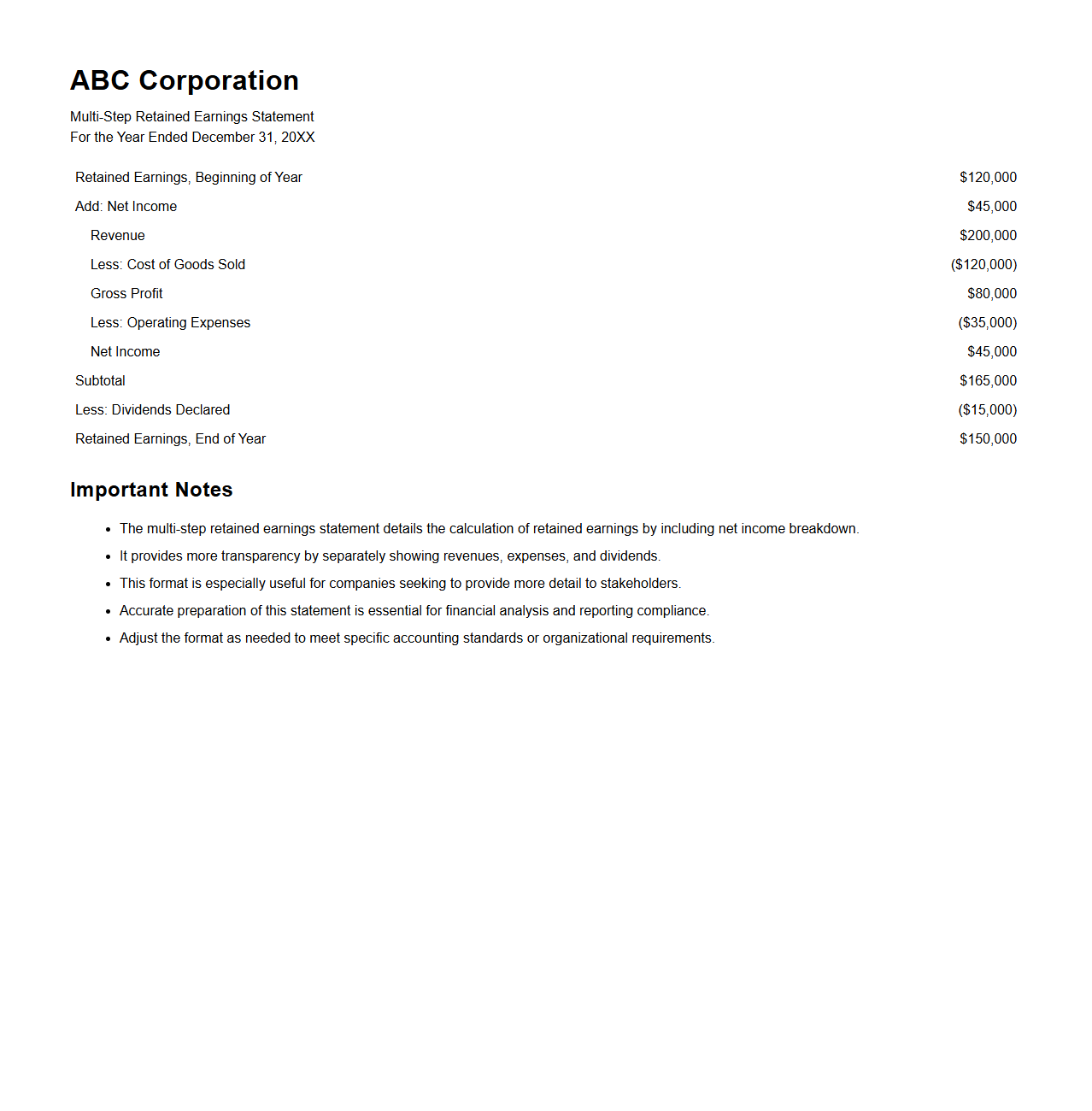

Multi-Step Retained Earnings Statement Format

The

Multi-Step Retained Earnings Statement Format document systematically outlines changes in retained earnings over a specific period, separating operating transactions from non-operating ones. It typically includes detailed sections for net income, dividends, and adjustments from prior periods, providing a clear and comprehensive view of how earnings are retained or distributed. This format enhances financial transparency and aids stakeholders in assessing a company's profitability and dividend policies.

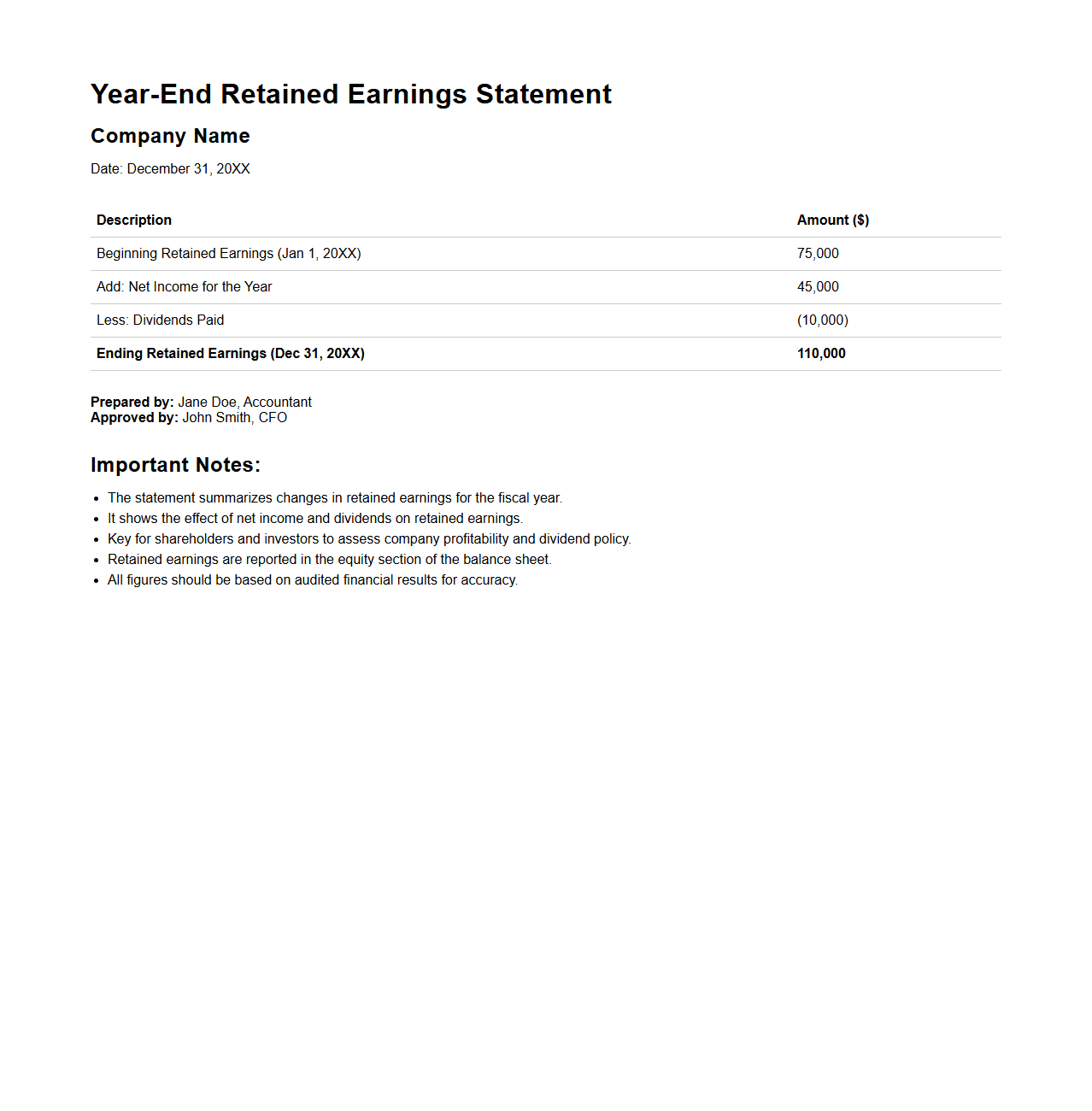

Year-End Retained Earnings Statement Format

The

Year-End Retained Earnings Statement Format document outlines the systematic presentation of changes in a company's retained earnings over the fiscal year. It typically includes beginning retained earnings, net income or loss, dividends paid, and the ending retained earnings balance. This format is essential for communicating financial performance and informing stakeholders about the company's reinvested profits.

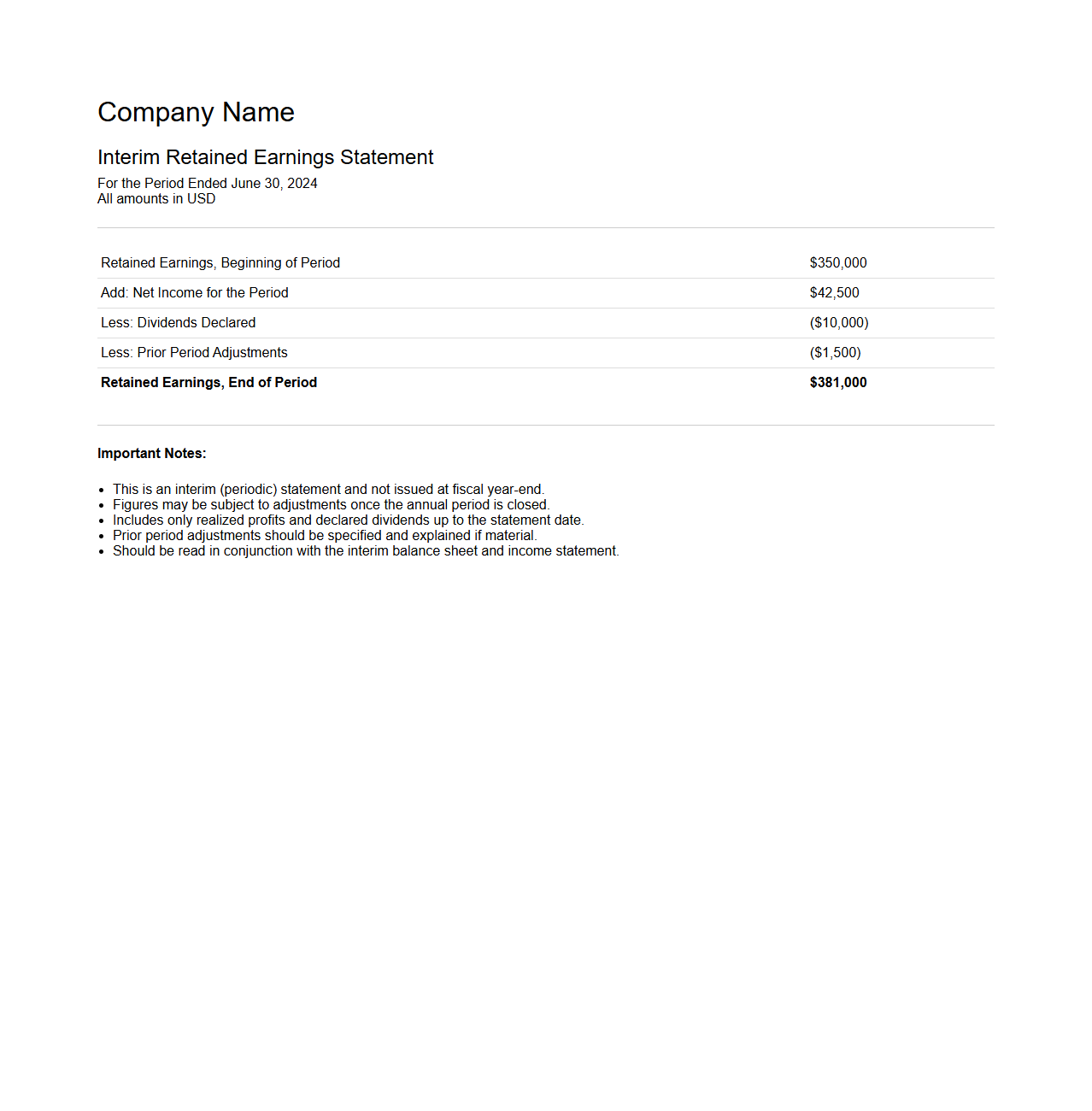

Interim Retained Earnings Statement Format

The

Interim Retained Earnings Statement Format document outlines the financial performance of a company over a partial reporting period, usually less than one fiscal year, by detailing the changes in retained earnings. It includes essential elements such as beginning retained earnings, net income or loss for the interim period, dividends declared, and any adjustments, providing a clear picture of how earnings are reinvested in the business. This format is crucial for stakeholders to assess the company's profitability and dividend policy between annual reports.

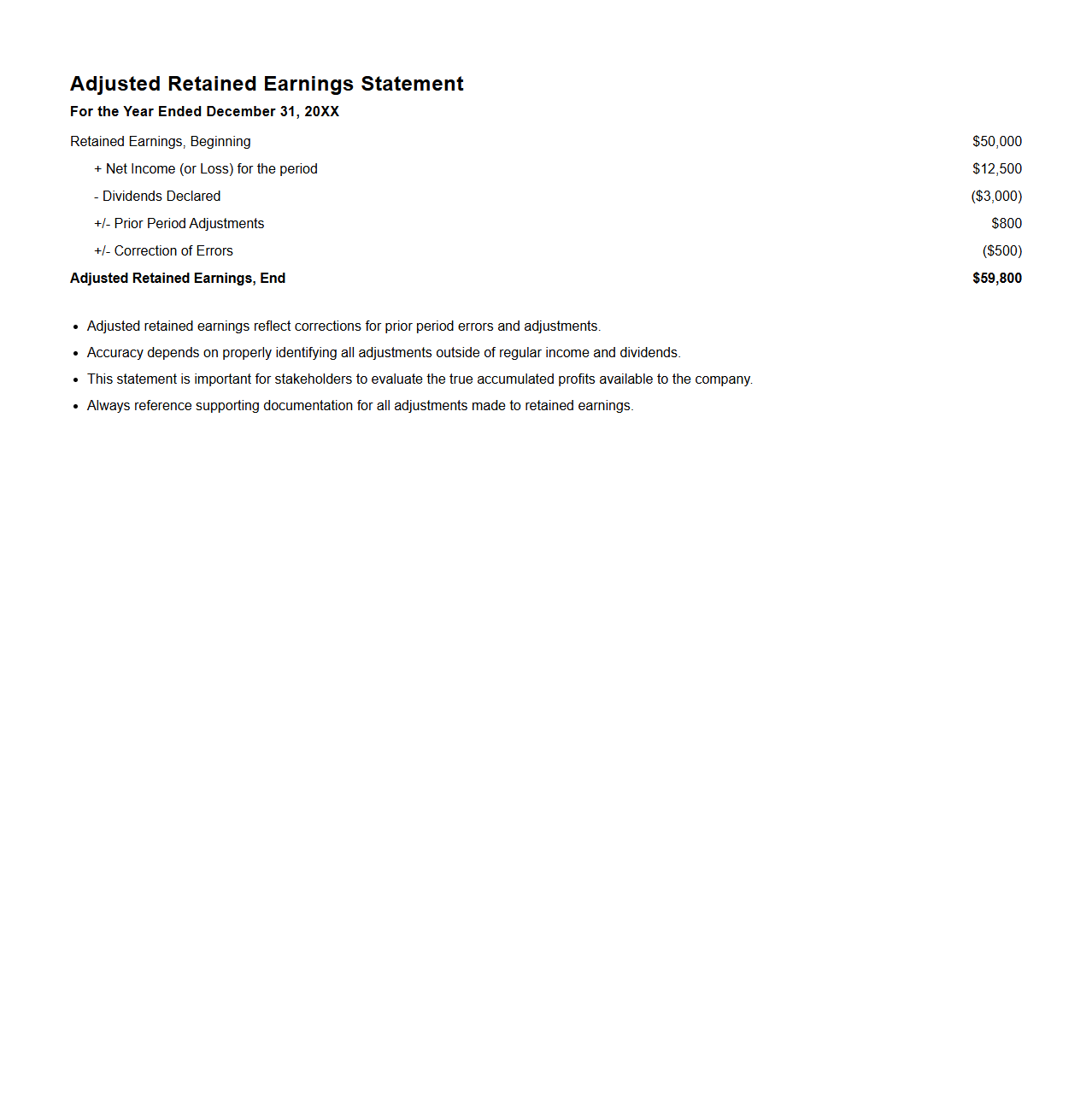

Adjusted Retained Earnings Statement Format

The

Adjusted Retained Earnings Statement format document outlines the changes in retained earnings during a specific period after adjusting for errors, prior period adjustments, and other comprehensive income. It provides a clear, structured presentation of the beginning retained earnings balance, net income or loss, dividends paid, and any adjustments required to reflect accurate financial performance. This format is essential for ensuring transparency and accuracy in shareholders' equity reporting in financial statements.

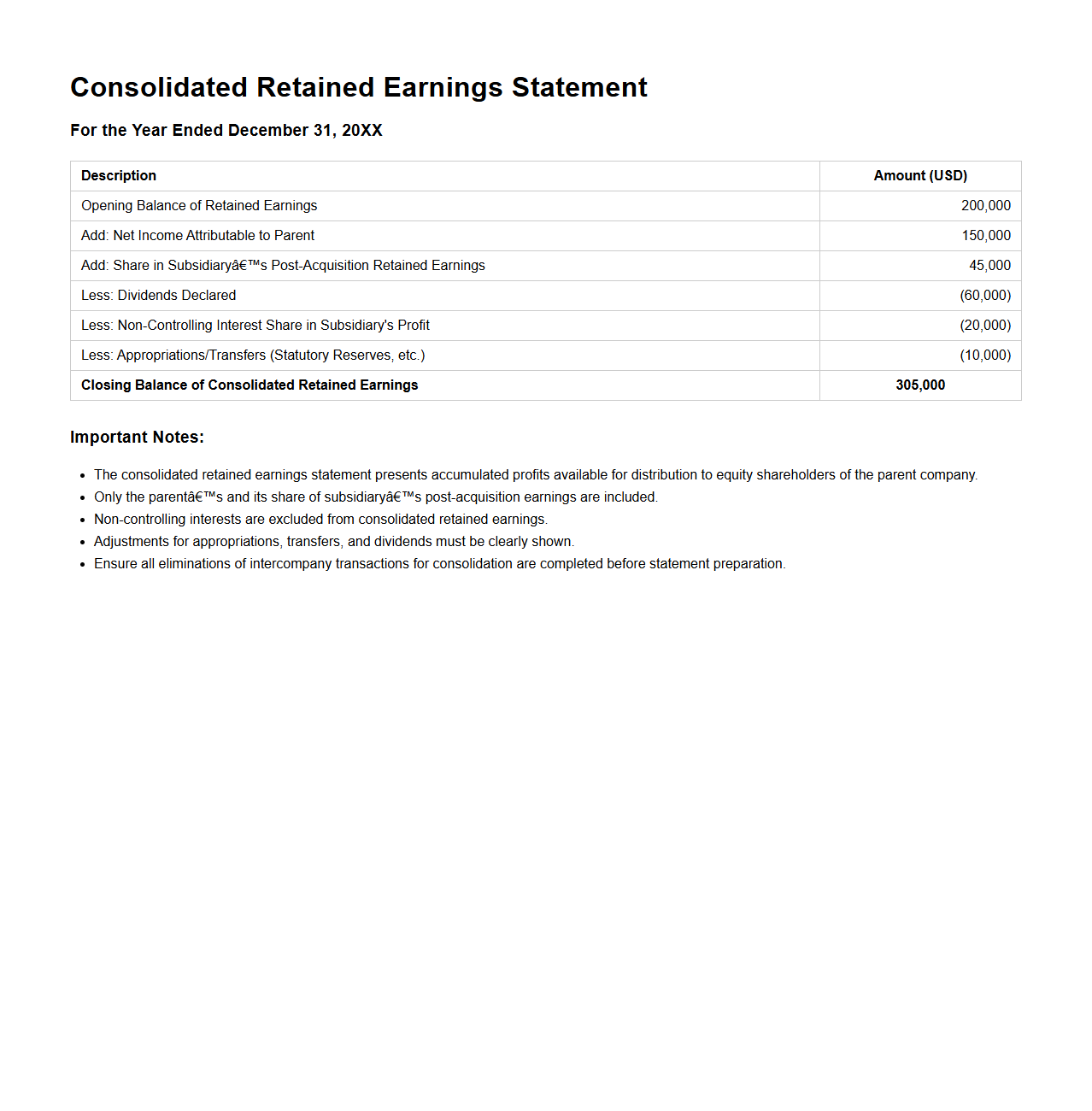

Consolidated Retained Earnings Statement Format

The

Consolidated Retained Earnings Statement Format document provides a detailed summary of the retained earnings of a parent company and its subsidiaries, combining their financial results into a unified statement. This format displays key components such as the opening balance, net income, dividends declared, and adjustments for prior periods, ensuring transparency and accuracy in reporting the cumulative earnings retained within the consolidated entity. It serves as a crucial tool for stakeholders to assess the company's reinvested profits and overall financial health over a specific accounting period.

Key Components Included in a Retained Earnings Statement for Profit

The retained earnings statement includes several key components such as the beginning retained earnings balance, net income or loss for the period, dividends paid, and any adjustments. This statement mainly reflects how the company's profits have been retained or distributed. It provides a clear view of the changes in retained earnings during a specific accounting period.

Incorporating Net Income into the Retained Earnings Statement Format

Net income is added to the beginning retained earnings balance within the statement. It represents the company's profit after all expenses have been deducted during the period. This addition increases the retained earnings amount, reflecting the company's earnings that are kept for future use.

Section Showing the Impact of Dividends Paid

The dividends paid section is typically shown after the net income line and represents amounts distributed to shareholders. This deduction lowers the retained earnings balance since dividends reduce the portion of profits retained in the company. Including this section ensures the statement accurately reflects the reduction in retained earnings.

Presentation of Beginning Retained Earnings Balance

The beginning retained earnings balance is presented as the first item in the retained earnings statement. It shows the retained earnings carried over from the prior period. This balance serves as the baseline for calculating changes due to net income, dividends, and adjustments during the current period.

Format Used to Display Adjustments and Corrections in Retained Earnings

Adjustments and corrections are usually displayed as separate line items in the statement, often titled as prior period adjustments. These entries modify the retained earnings balance to correct errors or reflect changes in accounting policies. Presenting them clearly ensures transparency and accuracy in financial reporting.