The Format of Operating Profit Statement for Managerial Review typically includes detailed breakdowns of revenues, direct costs, and operating expenses to highlight the profitability from core business operations. This format emphasizes key components such as gross profit, operating expenses, and operating profit to facilitate informed decision-making by managers. Clear presentation of these elements aids in analyzing operational efficiency and guiding strategic actions.

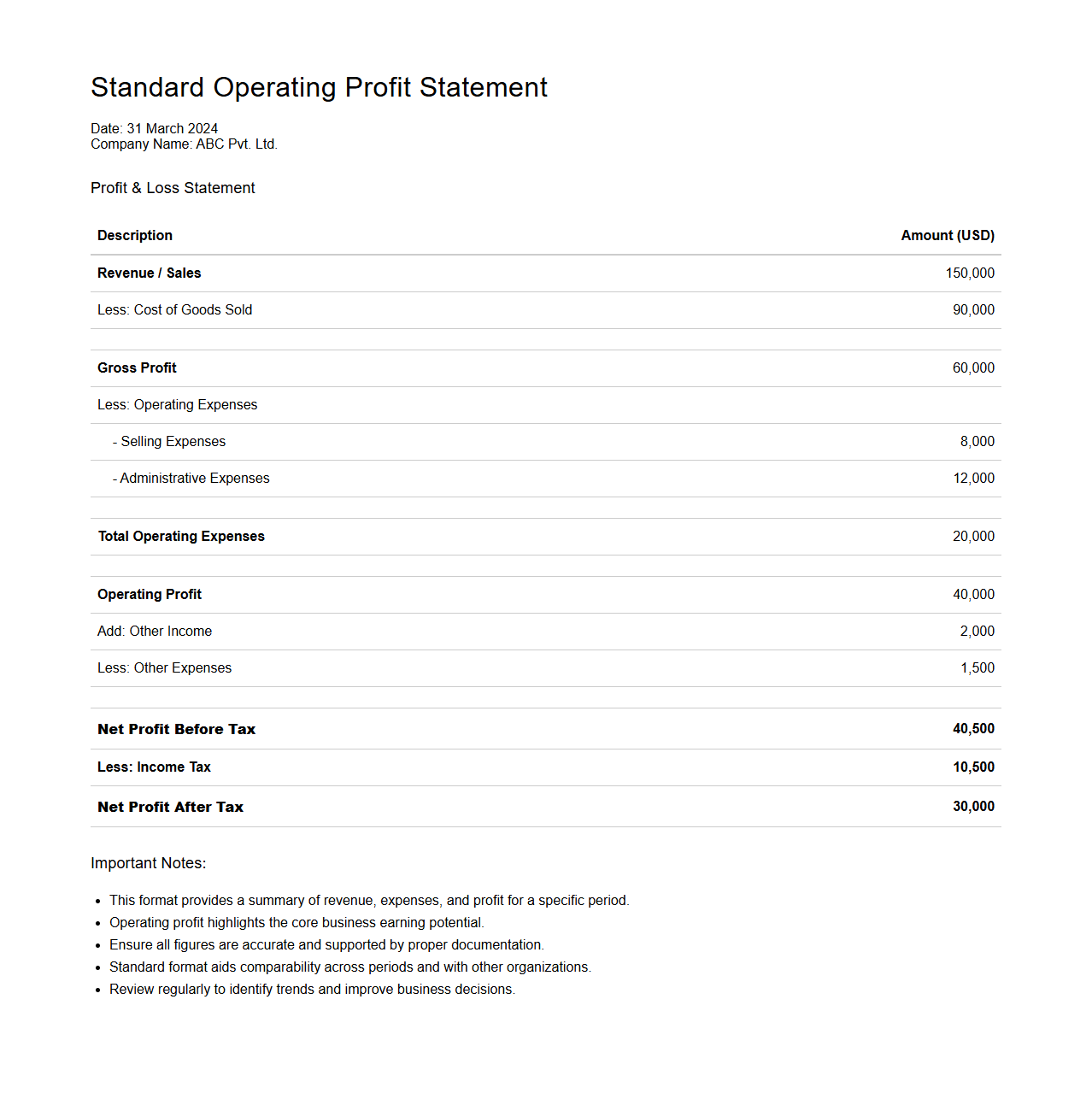

Standard Operating Profit Statement Format

A

Standard Operating Profit Statement Format document presents a structured financial report highlighting a company's operating revenues and expenses to determine net operating profit. It categorizes income and costs such as sales revenue, cost of goods sold, operating expenses, and depreciation, facilitating clear analysis of operational efficiency. This format aids stakeholders in assessing profitability by isolating operational performance from non-operating items.

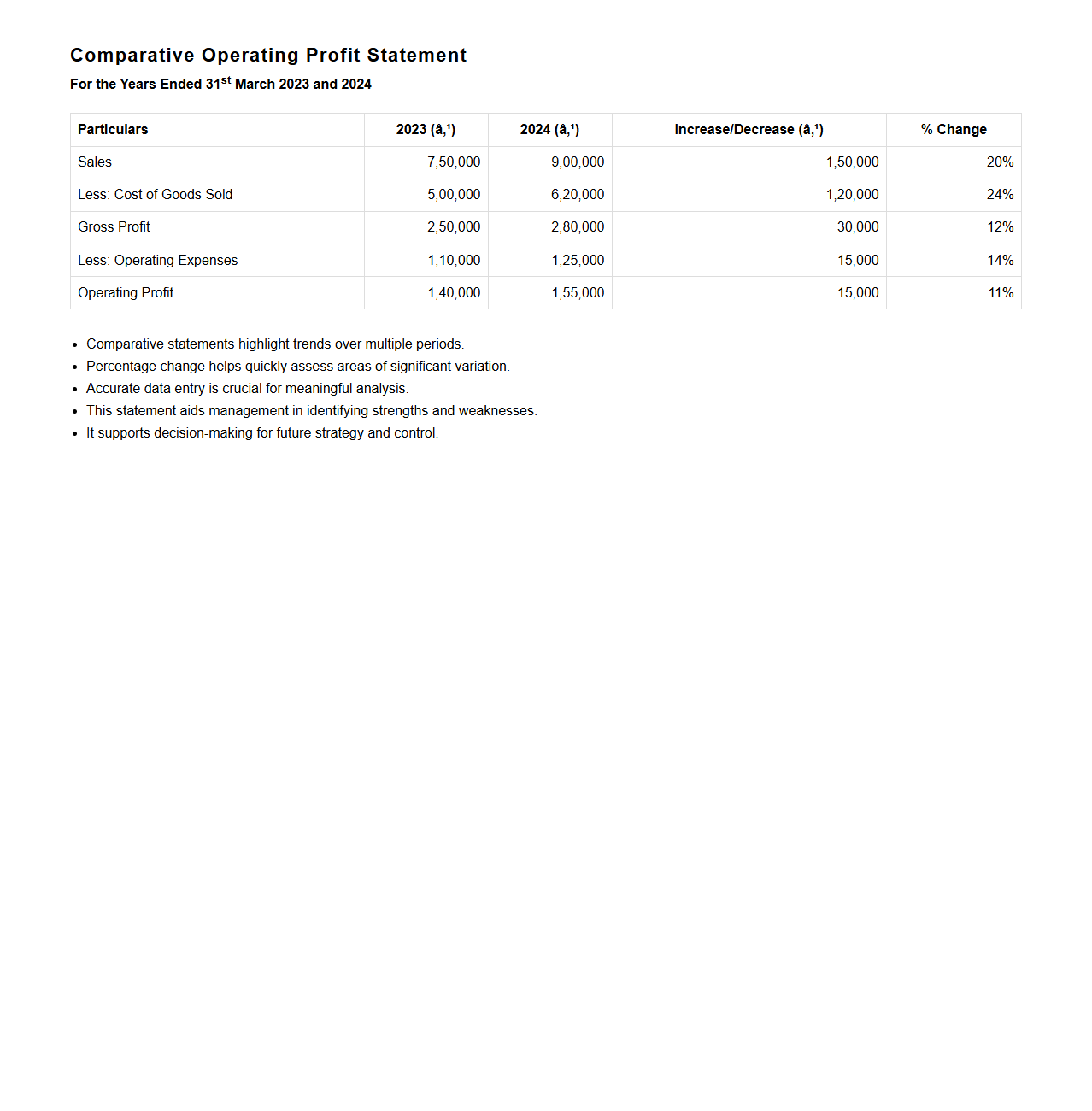

Comparative Operating Profit Statement Format

A

Comparative Operating Profit Statement Format document presents financial data side-by-side for multiple periods, enabling businesses to analyze trends and operational efficiency over time. It highlights key components such as revenues, cost of goods sold, operating expenses, and net operating profit, facilitating performance comparison. This format is essential for identifying growth patterns, cost control effectiveness, and strategic decision-making in business management.

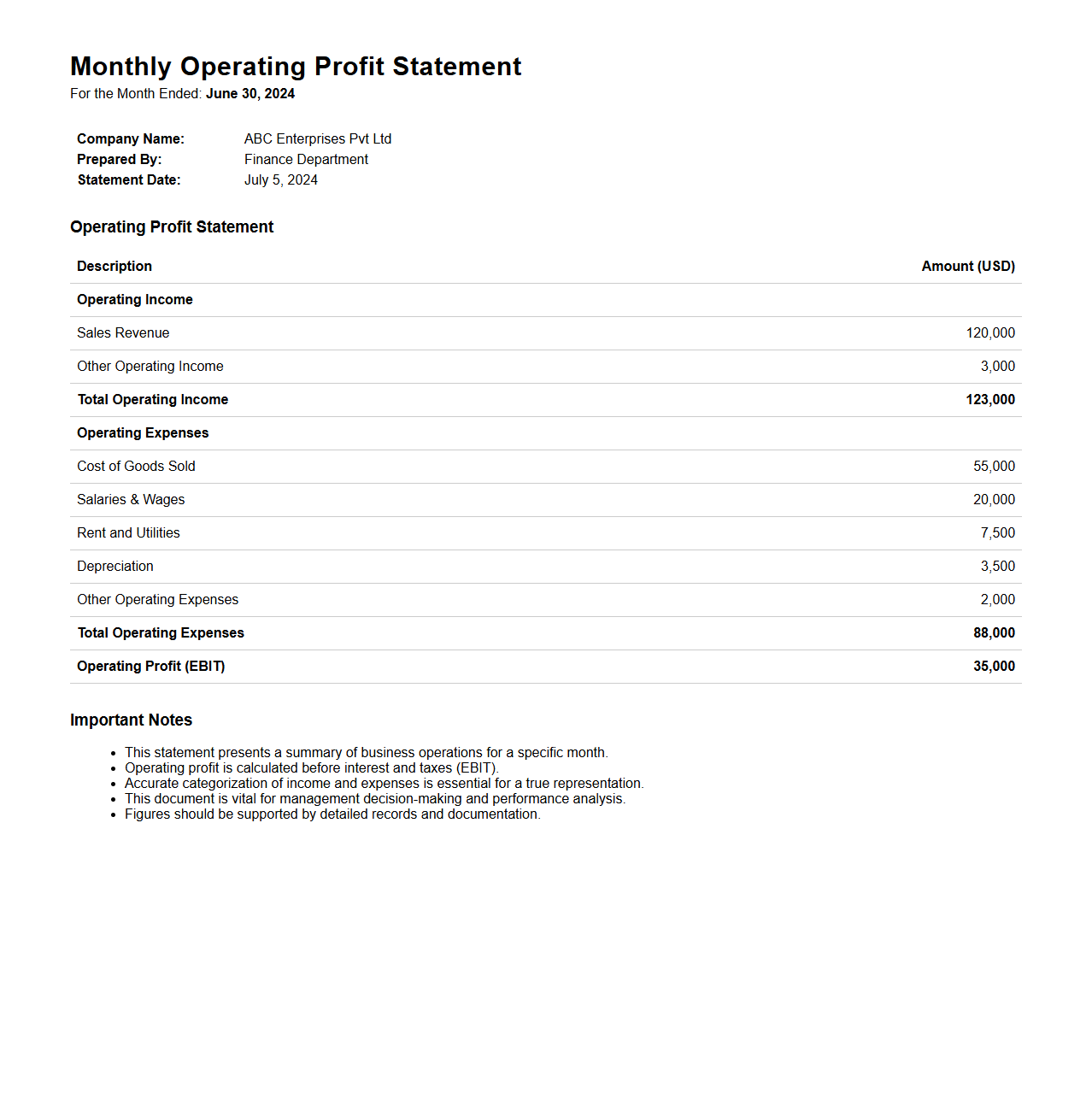

Monthly Operating Profit Statement Format

The

Monthly Operating Profit Statement Format document provides a structured layout for summarizing a company's monthly revenue, cost of goods sold, and operating expenses to calculate the operating profit. It helps businesses track financial performance over time, enabling better budgeting, cost control, and strategic decision-making. Accurate use of this format ensures consistent reporting and aids in identifying trends in profitability.

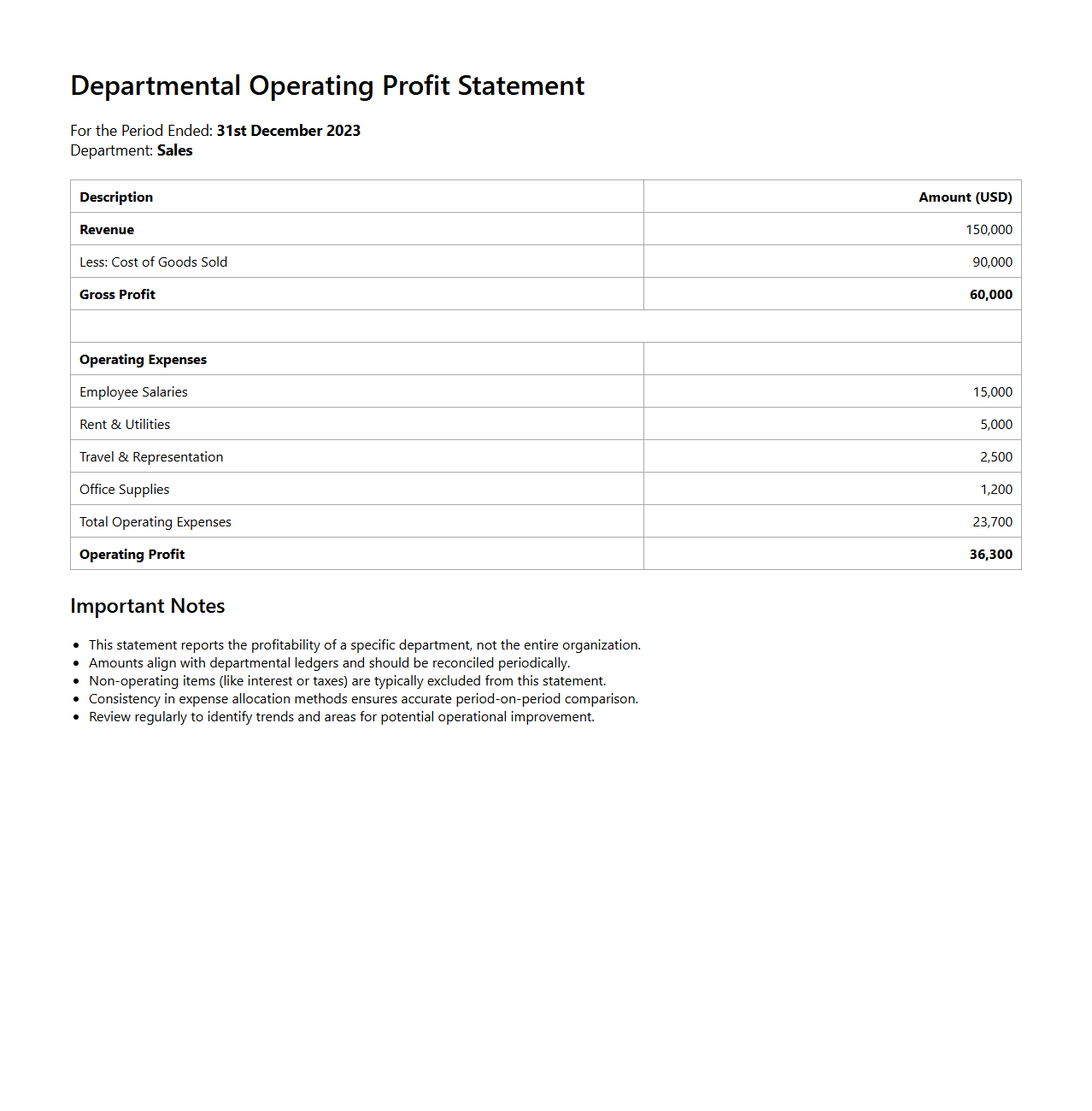

Departmental Operating Profit Statement Format

The

Departmental Operating Profit Statement Format document organizes financial data to evaluate the profitability of individual business departments. It typically includes sections for revenues, direct expenses, and allocated overheads, allowing for clear analysis of each department's contribution to overall profit. This format aids managers in identifying strengths and weaknesses within specific departments, supporting strategic decision-making and resource allocation.

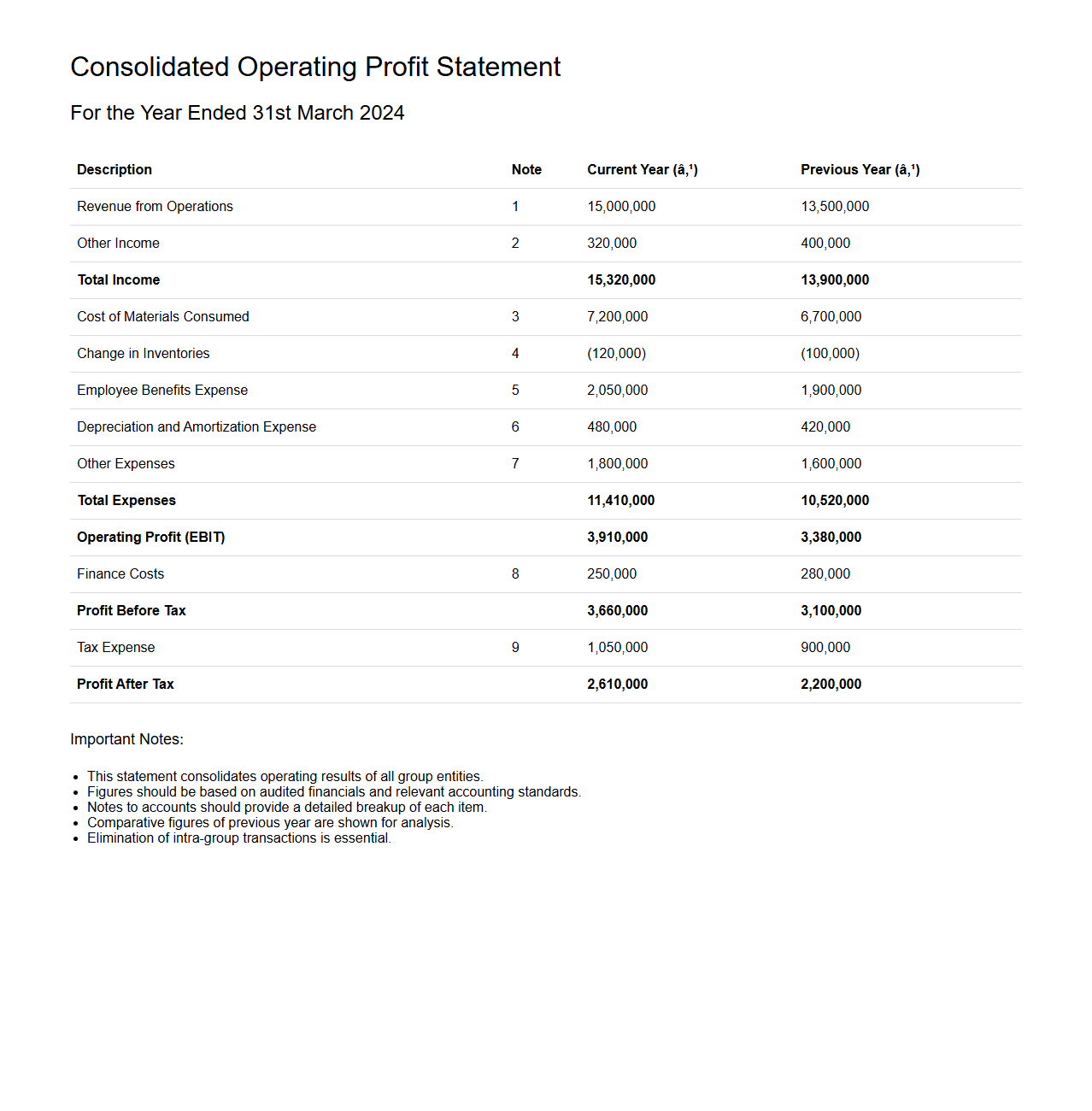

Consolidated Operating Profit Statement Format

The

Consolidated Operating Profit Statement Format document provides a structured layout for compiling the combined operational revenues and expenses of multiple subsidiaries within a parent company. It enables businesses to present a unified view of profitability by aggregating financial results, excluding non-operating incomes and expenses, to focus solely on operational performance. This format is crucial for stakeholders to assess the overall efficiency and earnings potential of the entire corporate group.

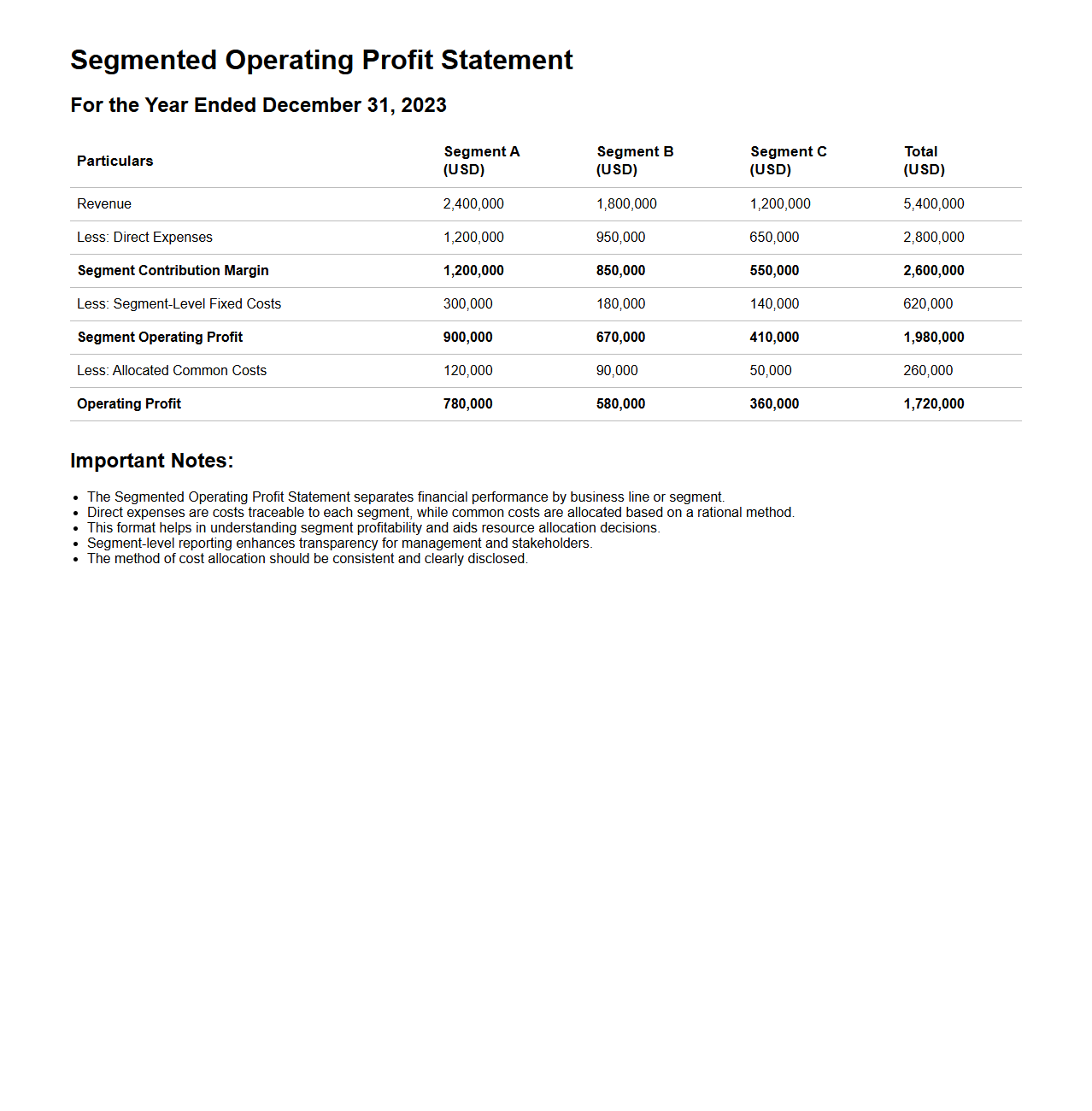

Segmented Operating Profit Statement Format

The

Segmented Operating Profit Statement Format document breaks down a company's operating profit by different business segments or divisions, providing detailed insights into each unit's financial performance. This format helps management evaluate profitability, allocate resources effectively, and make informed strategic decisions based on segment-level data. It typically includes revenue, direct costs, and operating profits for each segment, facilitating clearer financial analysis and reporting.

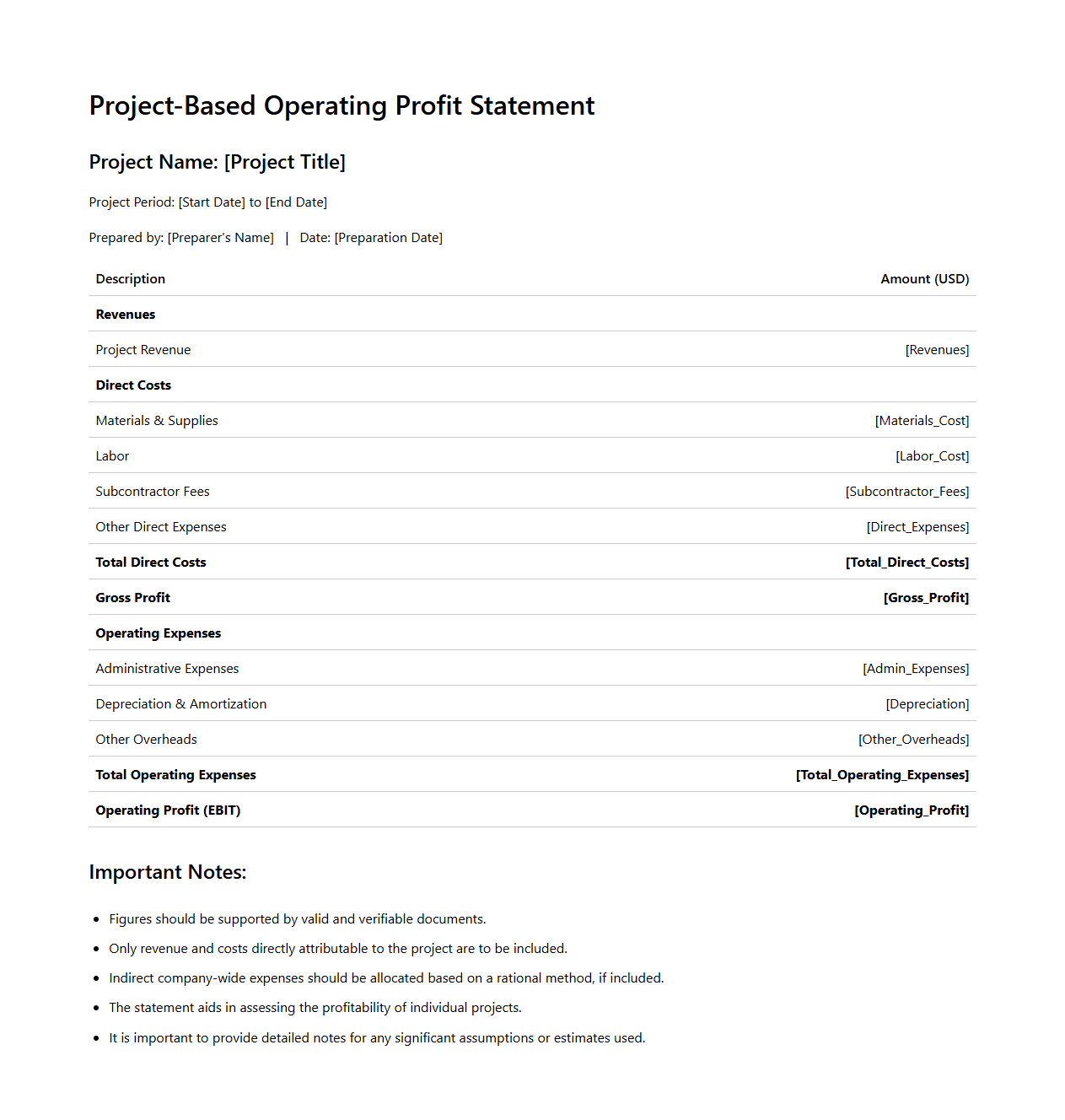

Project-Based Operating Profit Statement Format

The

Project-Based Operating Profit Statement Format document outlines the financial performance of individual projects by detailing revenues, direct costs, and operating expenses specific to each project. It provides a clear view of profitability on a project level, enabling better management decisions and resource allocation. This format is essential for organizations that handle multiple projects simultaneously and require precise financial tracking for each.

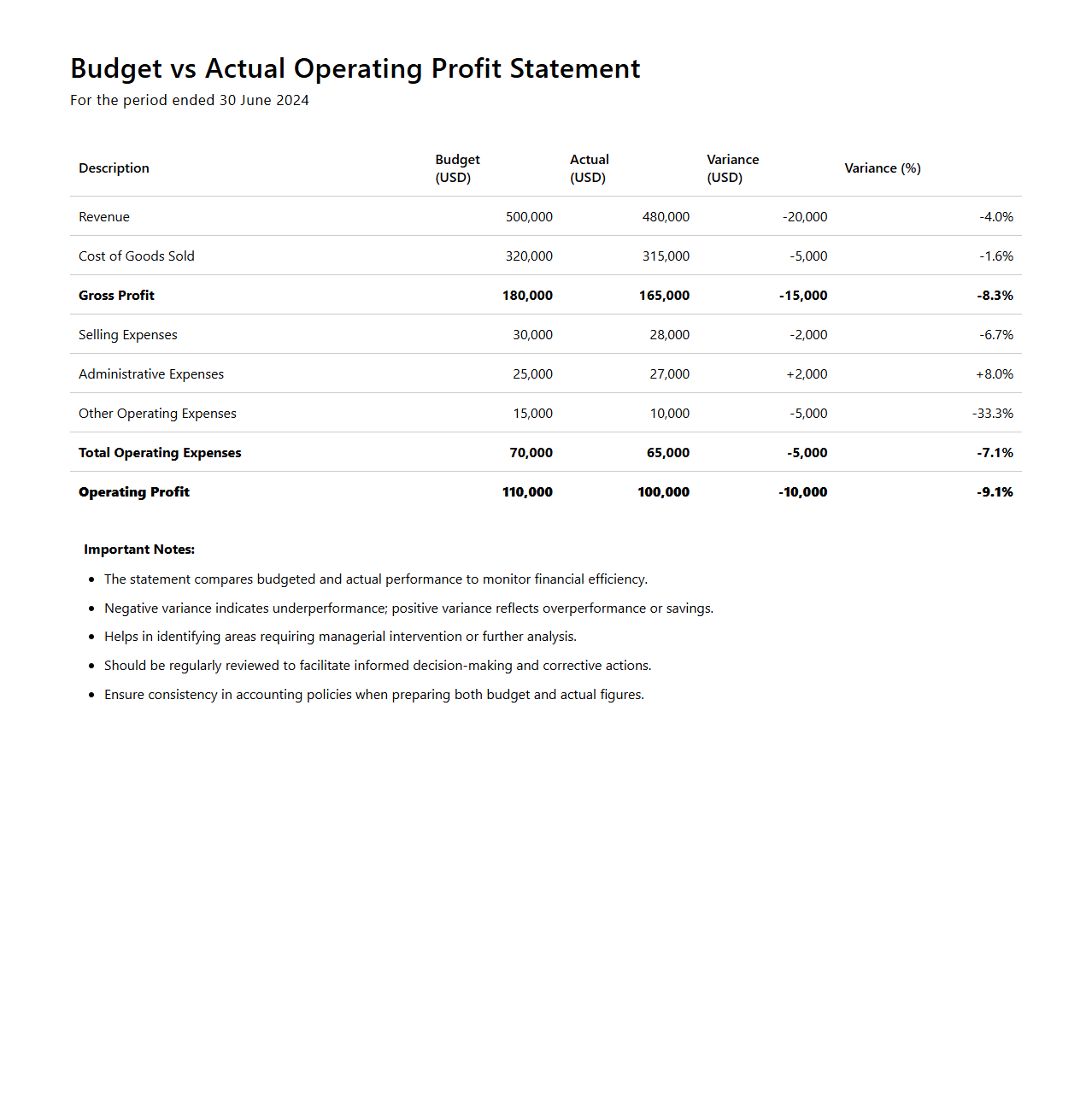

Budget vs Actual Operating Profit Statement Format

The

Budget vs Actual Operating Profit Statement Format document presents a comparative analysis of planned financial performance against actual results, highlighting variances in operating profit. It includes key components such as projected revenues, expenses, and net profit, enabling businesses to assess efficiency and identify areas requiring financial adjustments. This format is essential for performance tracking, guiding strategic decisions, and improving future budgeting accuracy.

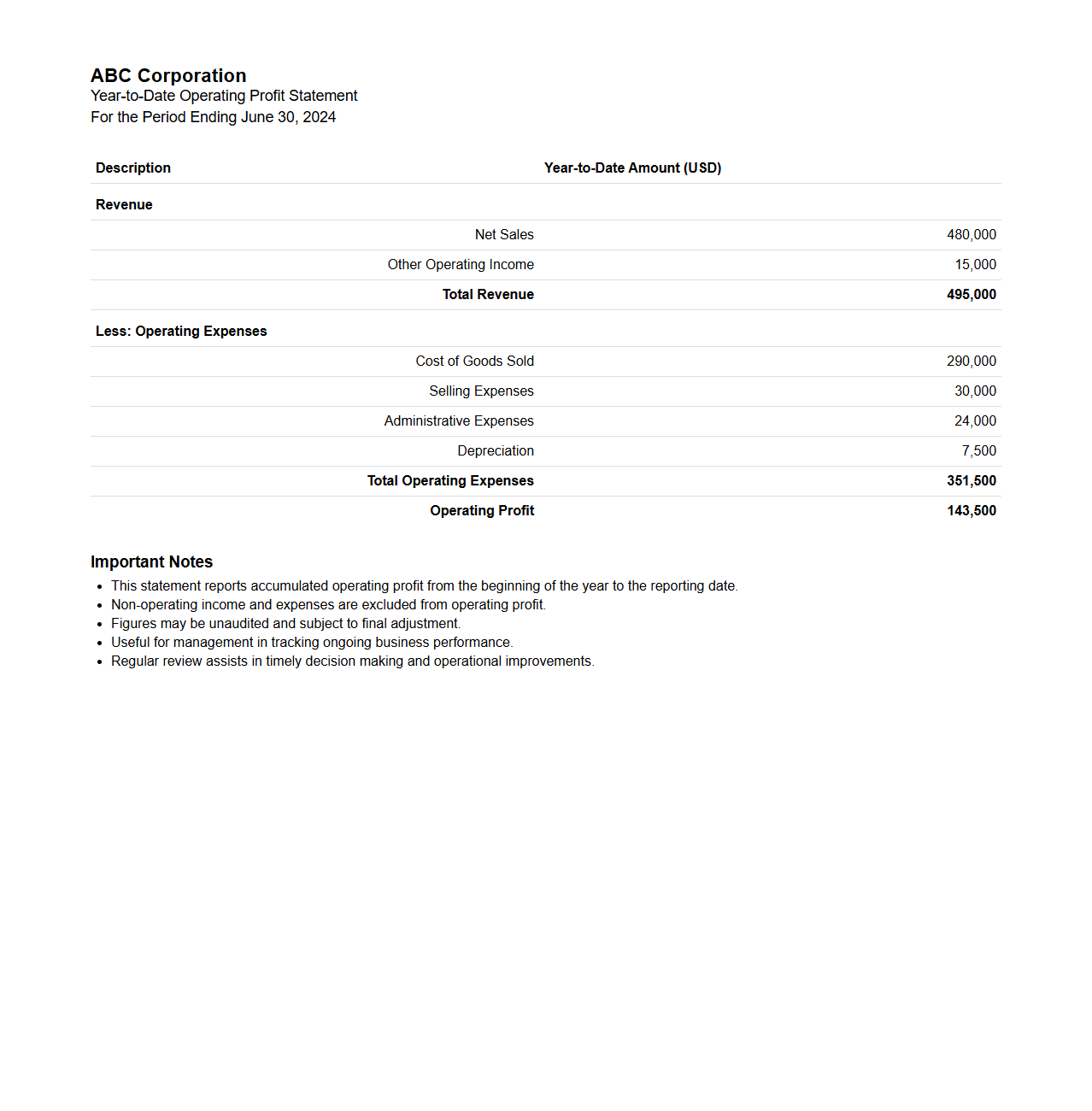

Year-to-Date Operating Profit Statement Format

A

Year-to-Date Operating Profit Statement Format document outlines a company's cumulative operating income generated from business activities from the beginning of the fiscal year to the current date. This format typically includes revenue, cost of goods sold, operating expenses, and operating income, providing a clear snapshot of financial performance over time. It serves as a crucial tool for management to assess operational efficiency and make informed strategic decisions.

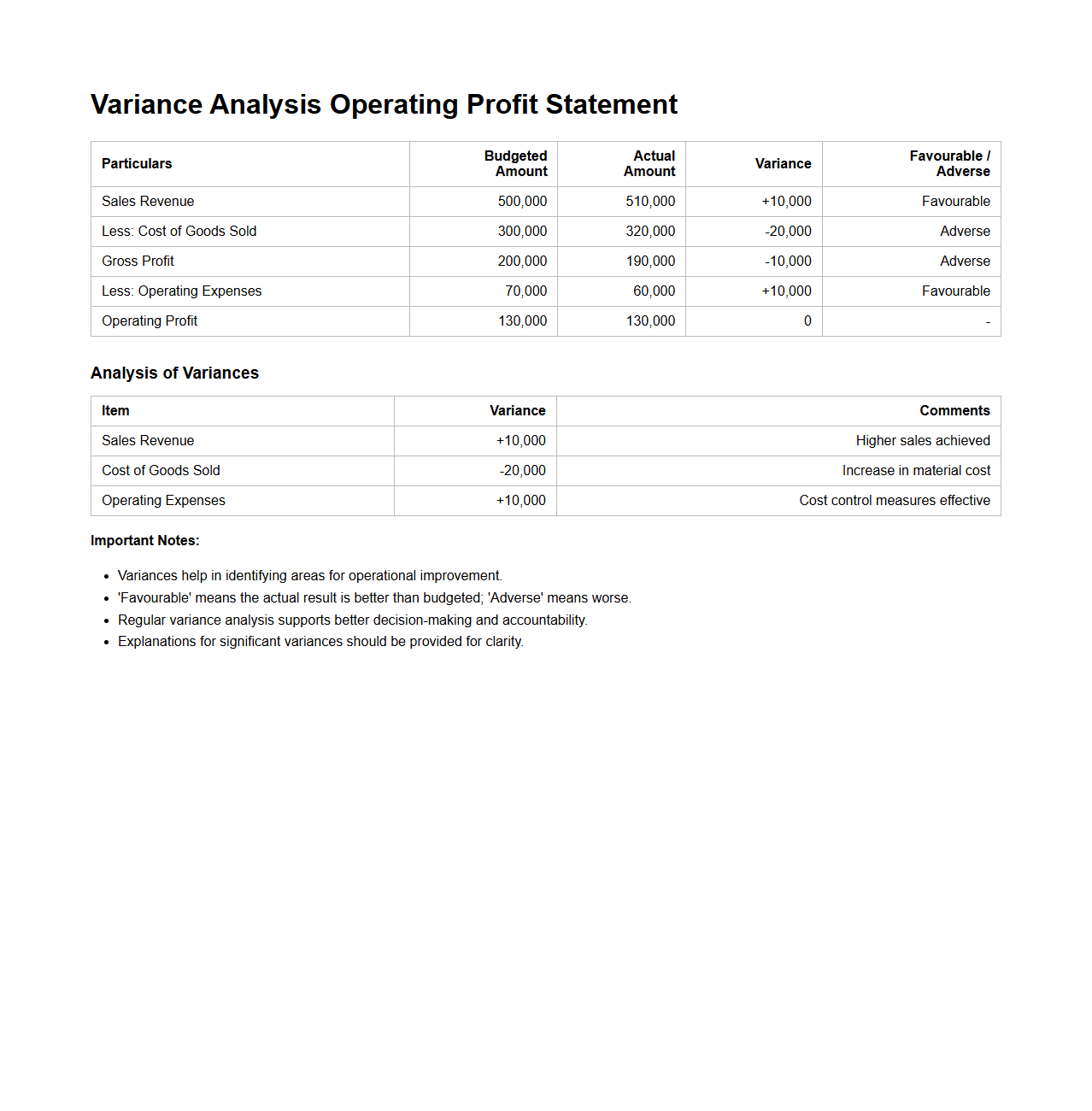

Variance Analysis Operating Profit Statement Format

Variance Analysis Operating Profit Statement Format document is a detailed financial report used to compare actual operating profit against budgeted or standard profit figures, identifying differences or variances. This document helps businesses pinpoint specific areas where performance deviates from expectations, facilitating informed decision-making to improve profitability.

Variance analysis enhances financial control by breaking down variances into components such as sales volume, price, and cost fluctuations.

Key Components in Operating Profit Statement for Managerial Review

The operating profit statement must include revenues, cost of goods sold, and operating expenses to provide a clear view of profitability. It should also highlight the gross profit and operating profit as critical performance metrics. These components enable management to assess operational efficiency and profitability accurately.

Presentation of Direct and Indirect Expenses

Direct expenses should be clearly separated from indirect expenses in the operating profit statement to enhance transparency. Direct expenses are typically associated with production costs, while indirect expenses relate to administrative and selling functions. This clear classification helps in pinpointing areas for cost control and operational improvements.

Sequence of Line Items for Optimal Clarity

The statement should begin with total revenue, followed by cost of goods sold to calculate gross profit. Next, list operating expenses in order of relevance, ending with operating profit at the bottom. This logical sequence improves readability and aids managerial decision-making.

Highlighting Variances Between Actual and Budgeted Figures

Variances should be presented in a separate column next to actual and budgeted figures to facilitate quick comparisons. Use variance analysis to indicate favorable or unfavorable differences with color coding or symbols. This approach allows managers to identify deviations and take corrective actions promptly.

Supporting Schedules and Notes for Management Analysis

The operating profit statement should reference supporting schedules such as detailed expense reports and variance analysis notes. These notes provide context and explanations for significant changes or anomalies in the figures. Including them enhances the statement's usefulness as a tool for informed management decisions.