The Format of Cash Flow Statement for Profit Assessment typically categorizes cash flows into operating, investing, and financing activities, providing a clear view of how a company generates and uses cash. It focuses on net cash inflows and outflows to determine the liquidity position and operational efficiency rather than just accounting profits. This format helps stakeholders assess the sustainability of profit by analyzing actual cash movements instead of reported earnings.

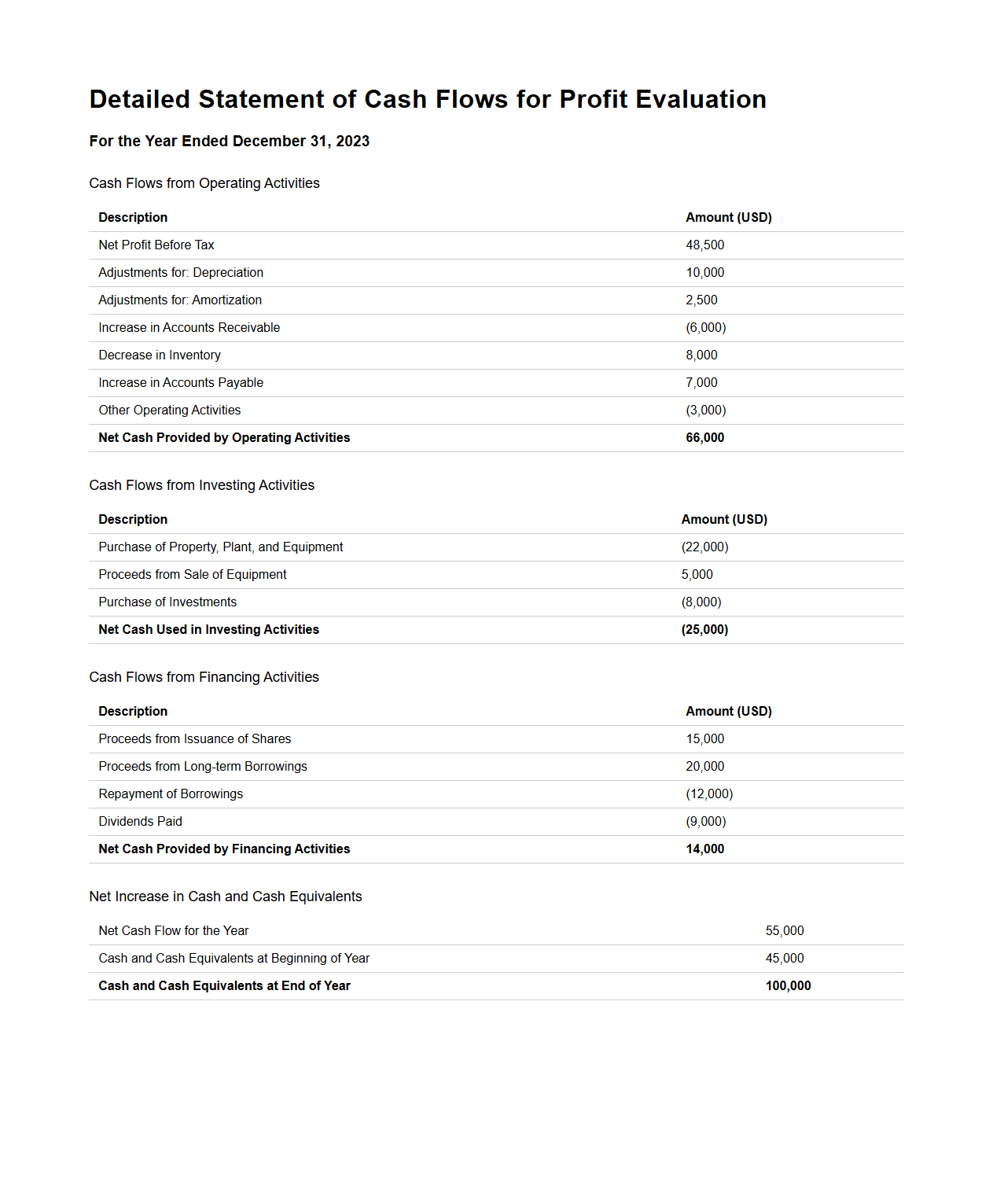

Detailed Statement of Cash Flows for Profit Evaluation

The

Detailed Statement of Cash Flows for Profit Evaluation provides a comprehensive analysis of a company's cash inflows and outflows, categorizing them into operating, investing, and financing activities. This document is essential for assessing the company's liquidity, financial flexibility, and ability to generate sustainable profits. By examining the precise movement of cash, stakeholders can evaluate the quality of earnings beyond net income figures.

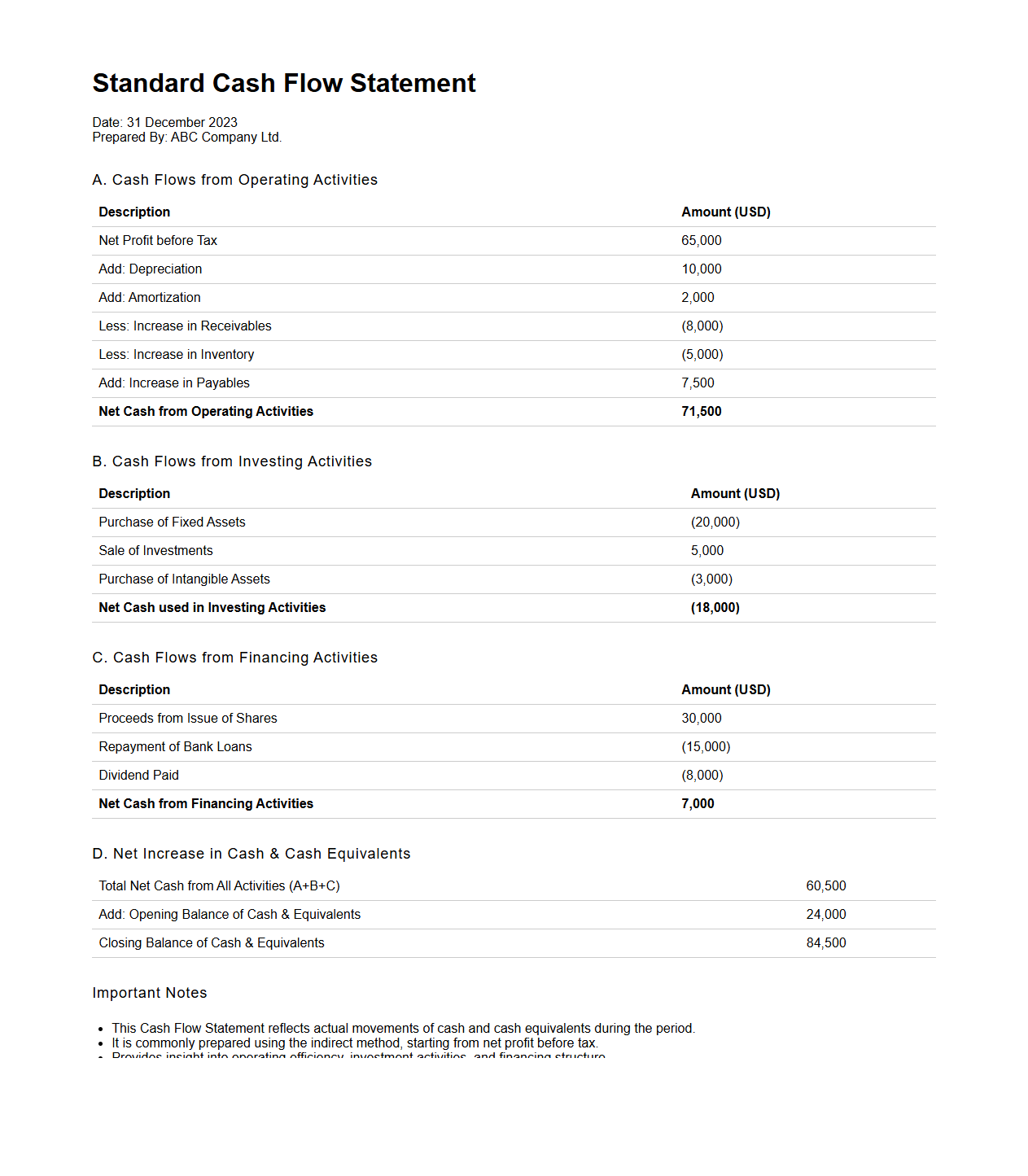

Standard Cash Flow Statement Format for Profit Assessment

The

Standard Cash Flow Statement Format for Profit Assessment is a structured financial document that details cash inflows and outflows over a specific period, categorized into operating, investing, and financing activities. This format helps businesses evaluate liquidity, operational efficiency, and overall profitability by highlighting the net cash generated or used in each section. It serves as an essential tool for stakeholders to assess the company's financial health and make informed investment or management decisions.

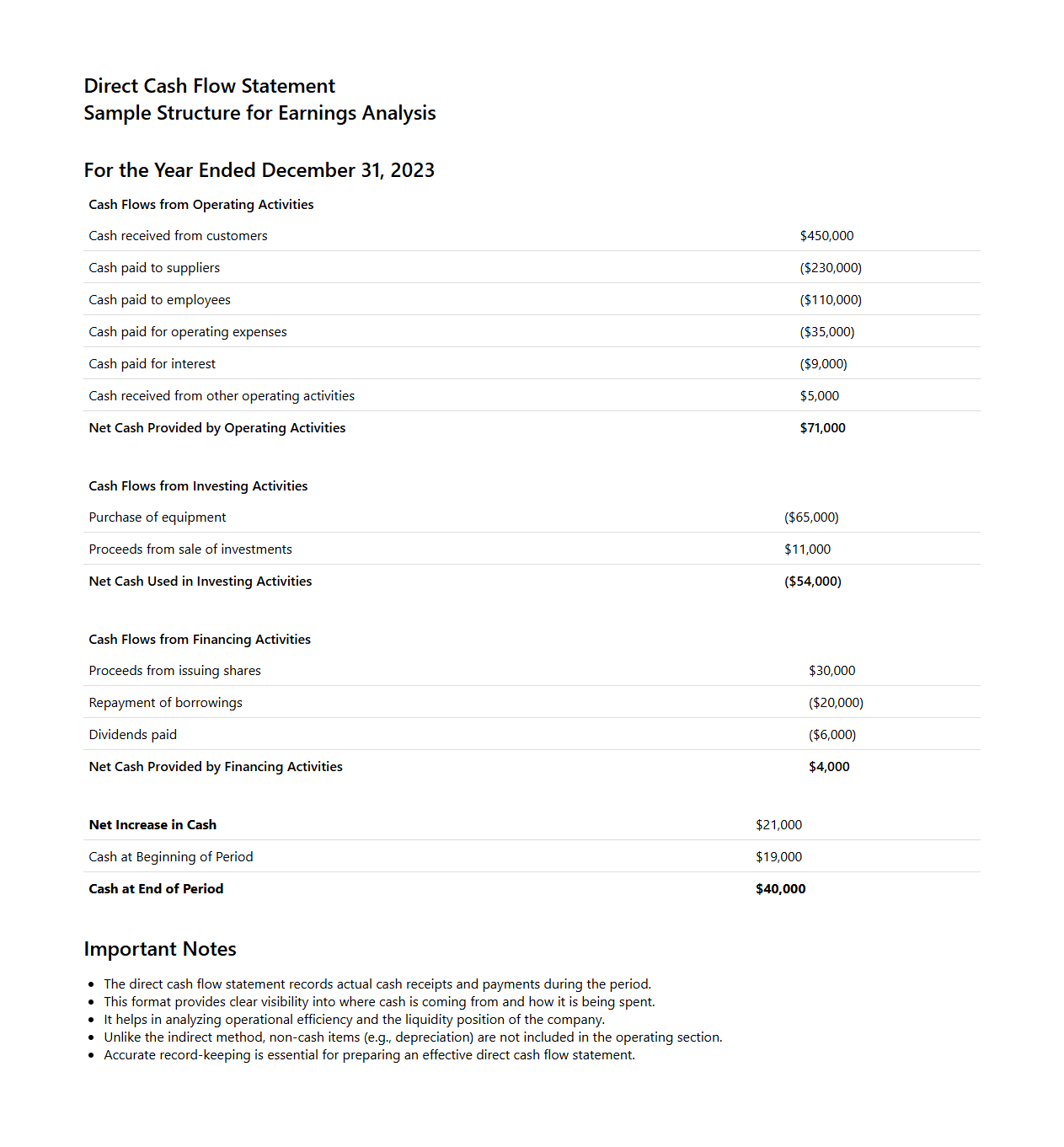

Direct Cash Flow Statement Structure for Earnings Analysis

The

Direct Cash Flow Statement Structure for Earnings Analysis document outlines the systematic presentation of cash inflows and outflows from operating activities, excluding non-cash transactions. This structure enables precise assessment of a company's liquidity by detailing actual cash receipts and payments, facilitating accurate evaluation of operational efficiency. Analysts rely on this format to identify cash sources and uses, ensuring transparent insight into earnings quality and financial health.

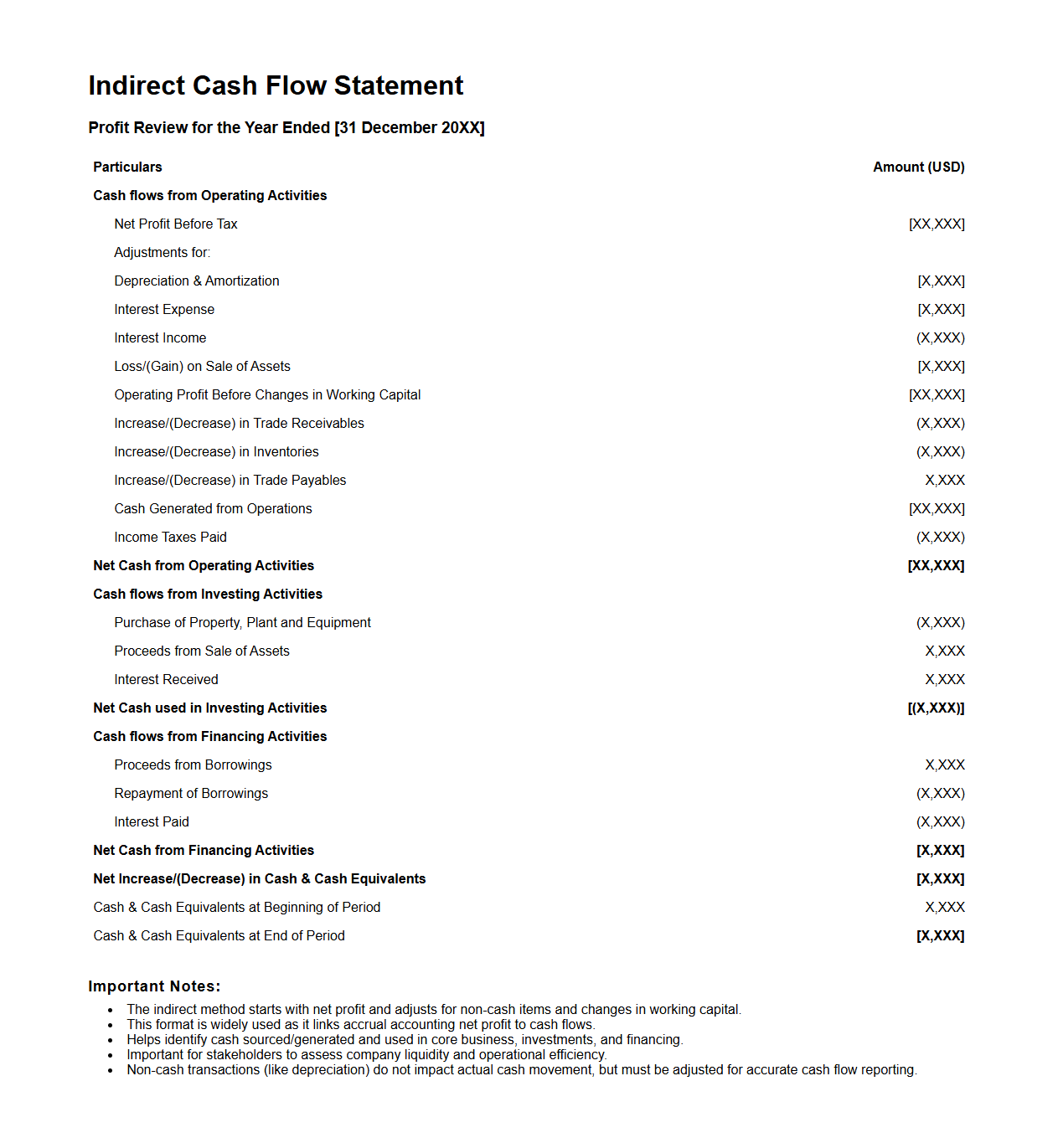

Indirect Cash Flow Statement Format for Profit Review

The

Indirect Cash Flow Statement Format for a Profit Review document summarizes net income by adjusting for non-cash transactions and changes in working capital, providing a clear view of operational cash flow. This format starts with net profit and reconciles it with cash movements, highlighting areas such as depreciation, accounts receivable, and inventory fluctuations. It is essential for assessing the actual cash generated from business operations beyond accounting profit, aiding in more accurate financial analysis and decision-making.

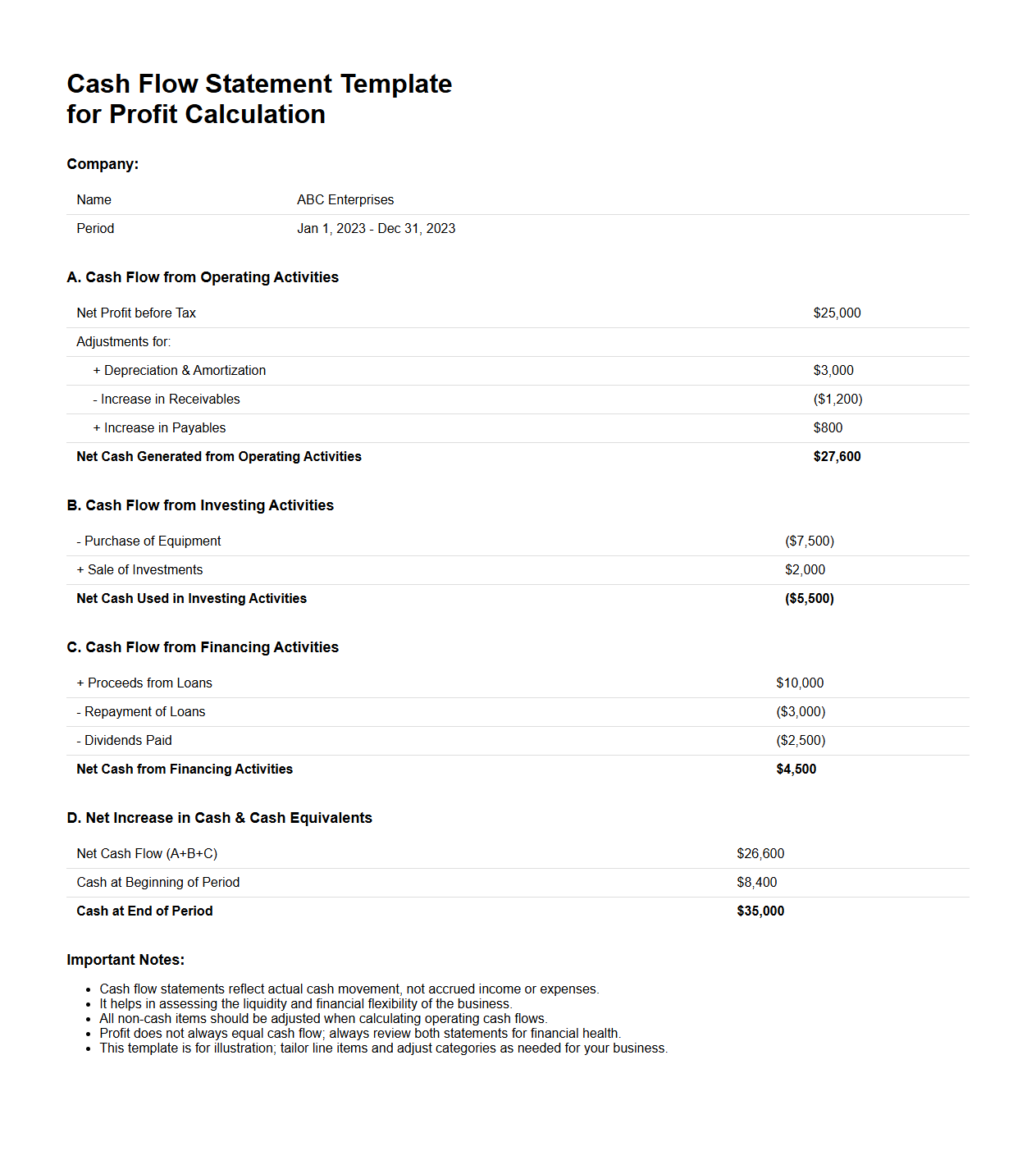

Cash Flow Statement Template for Profit Calculation

A Cash Flow Statement Template for Profit Calculation document systematically tracks the inflows and outflows of cash within a business, providing a clear view of liquidity and operational efficiency. This template helps identify how cash is generated from core business activities, investments, and financing, allowing for accurate profit assessment. Using a

cash flow statement ensures a precise understanding of a company's financial health beyond just profit figures, aiding better decision-making.

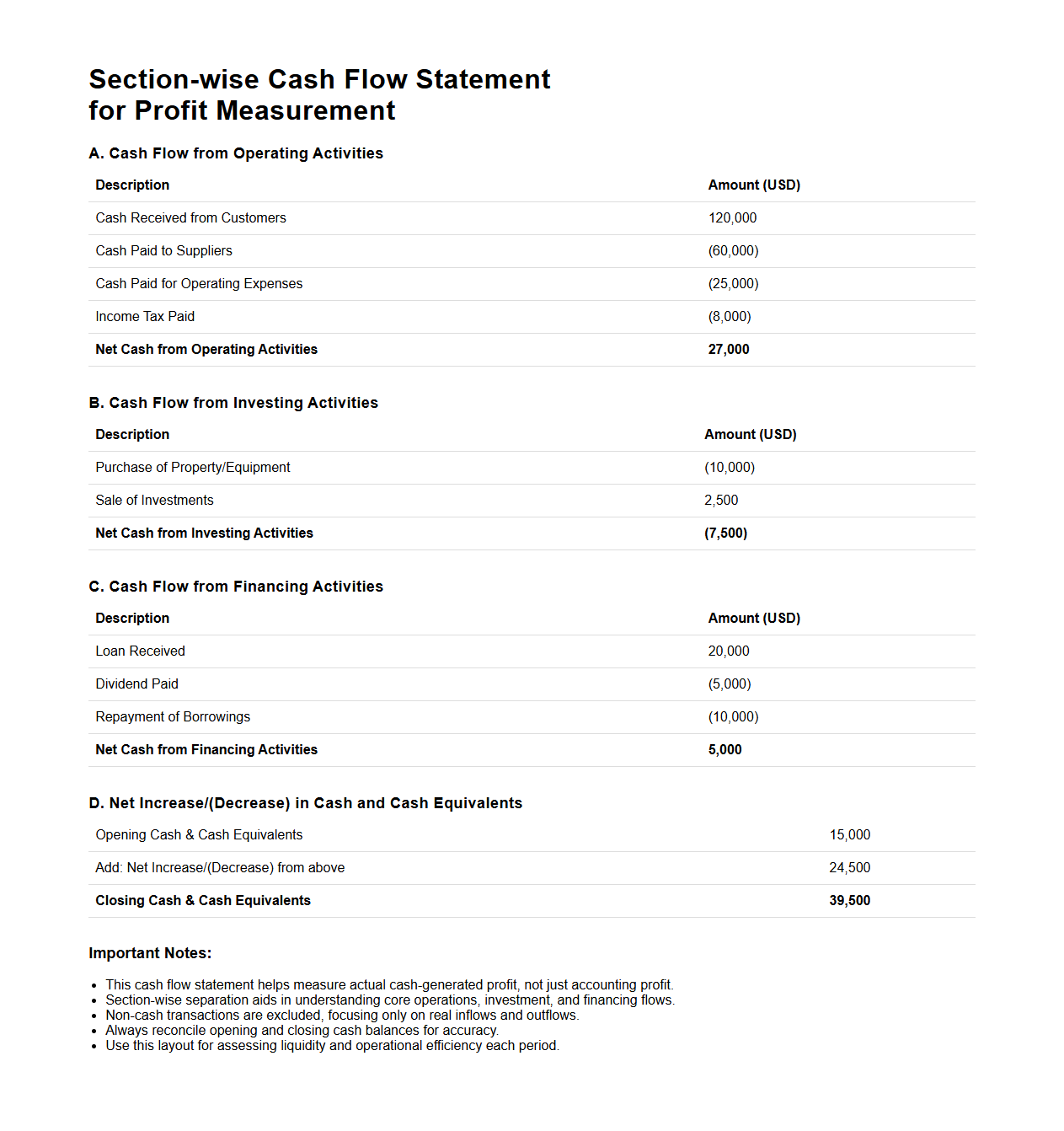

Section-wise Cash Flow Statement Layout for Profit Measurement

The

Section-wise Cash Flow Statement Layout for Profit Measurement document provides a structured format to analyze cash inflows and outflows categorized by operating, investing, and financing activities. This layout helps in accurately assessing the liquidity and profitability of a business by highlighting cash movements relevant to profit generation. It serves as a crucial tool for financial analysts and accountants to measure actual cash performance against reported profits.

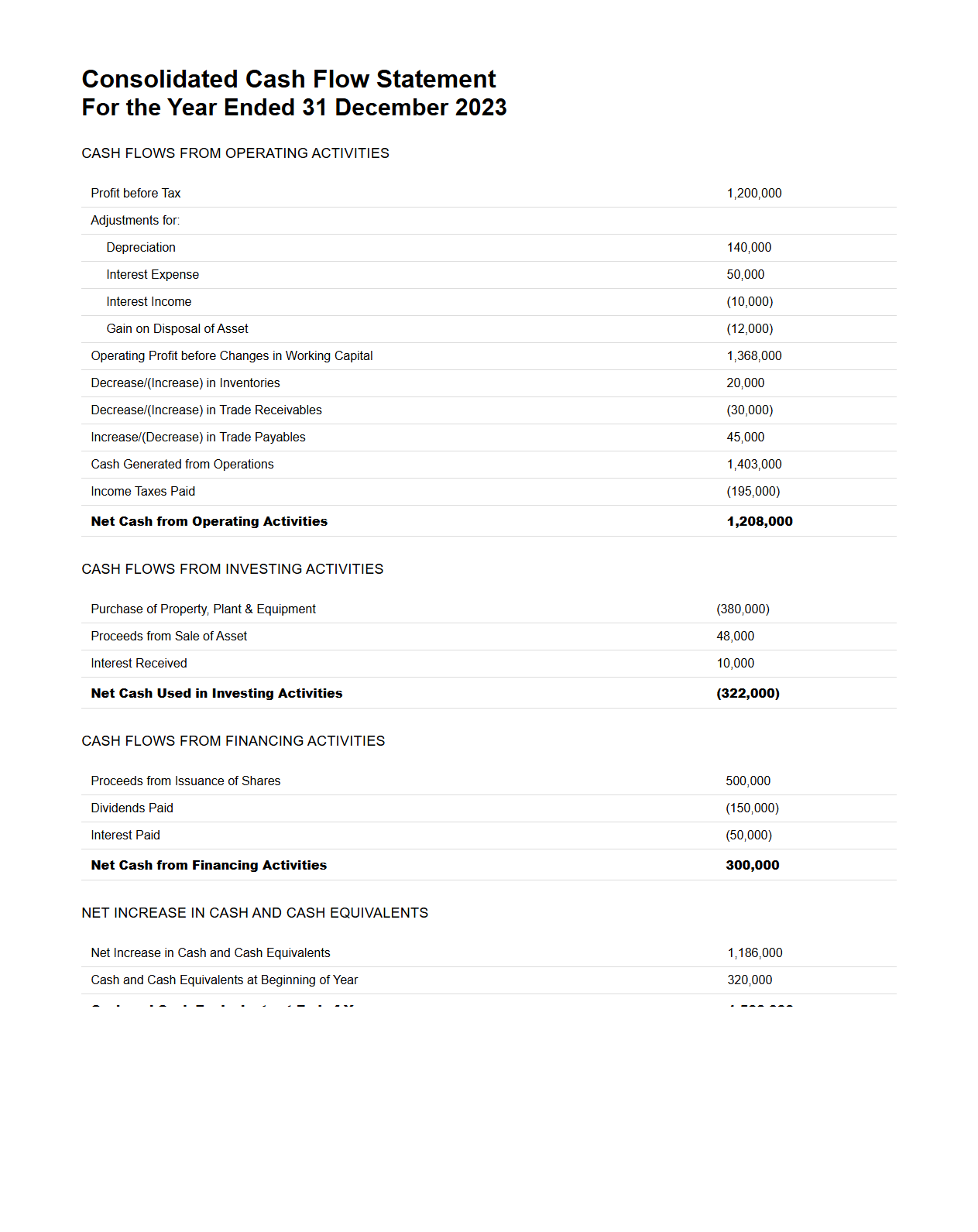

Consolidated Cash Flow Statement for Profit Assessment

A

Consolidated Cash Flow Statement for Profit Assessment is a financial document that aggregates cash inflows and outflows from all subsidiaries within a corporate group to provide a comprehensive view of liquidity. This statement highlights operational, investing, and financing activities, enabling stakeholders to assess the overall cash generation and usage relative to profit performance. It serves as a critical tool in evaluating a company's ability to generate sufficient cash flow to maintain profitability and meet financial obligations.

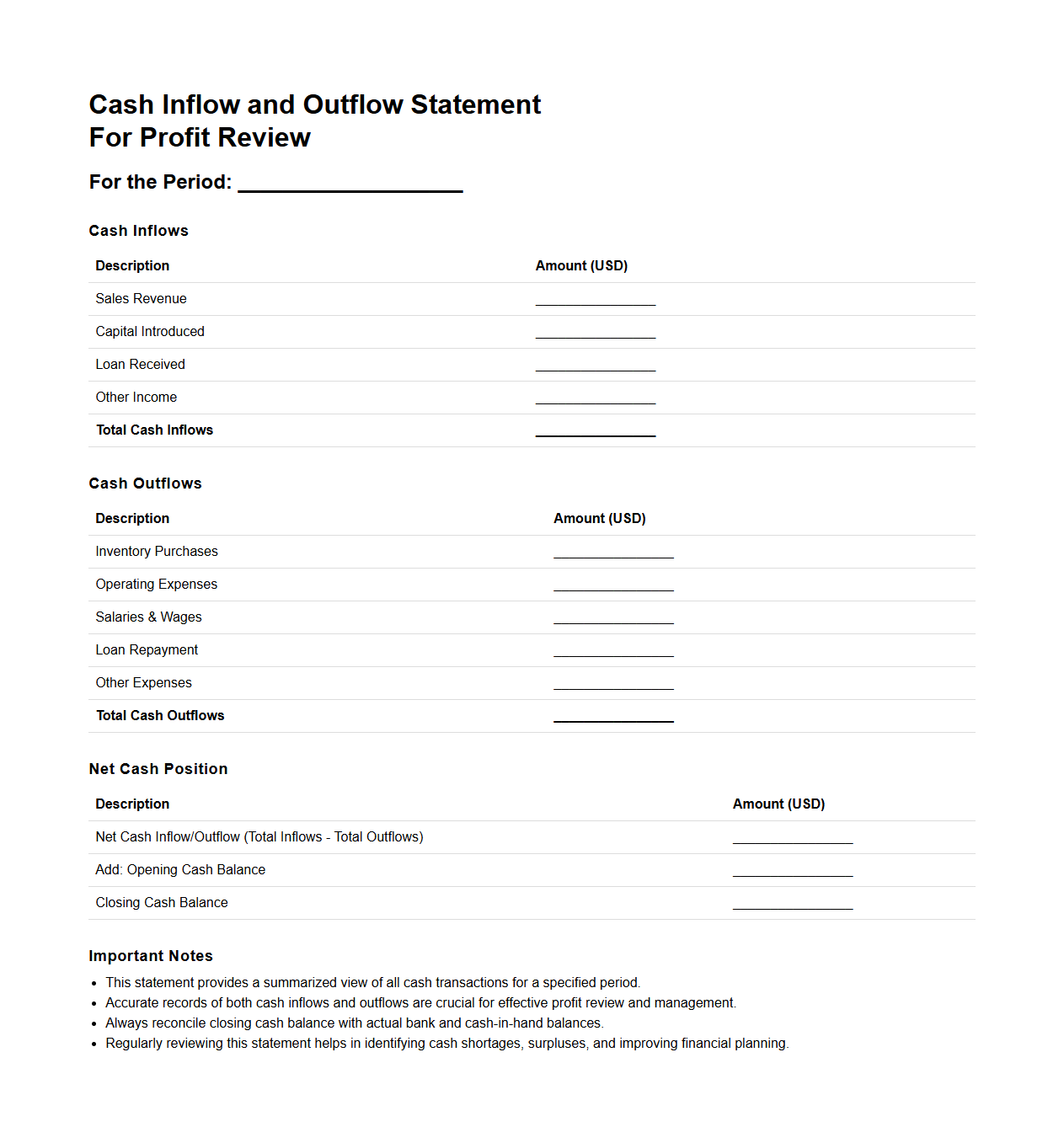

Cash Inflow and Outflow Statement Format for Profit Review

The

Cash Inflow and Outflow Statement Format for Profit Review is a financial document that tracks the movement of cash within a business, detailing all cash receipts and payments during a specific period. This statement categorizes cash sources such as operating activities, investments, and financing, alongside expenditures, enabling a clear analysis of liquidity and operational efficiency. It supports profit assessment by highlighting the actual cash effects of business activities rather than just accounting profits, ensuring more accurate financial decision-making.

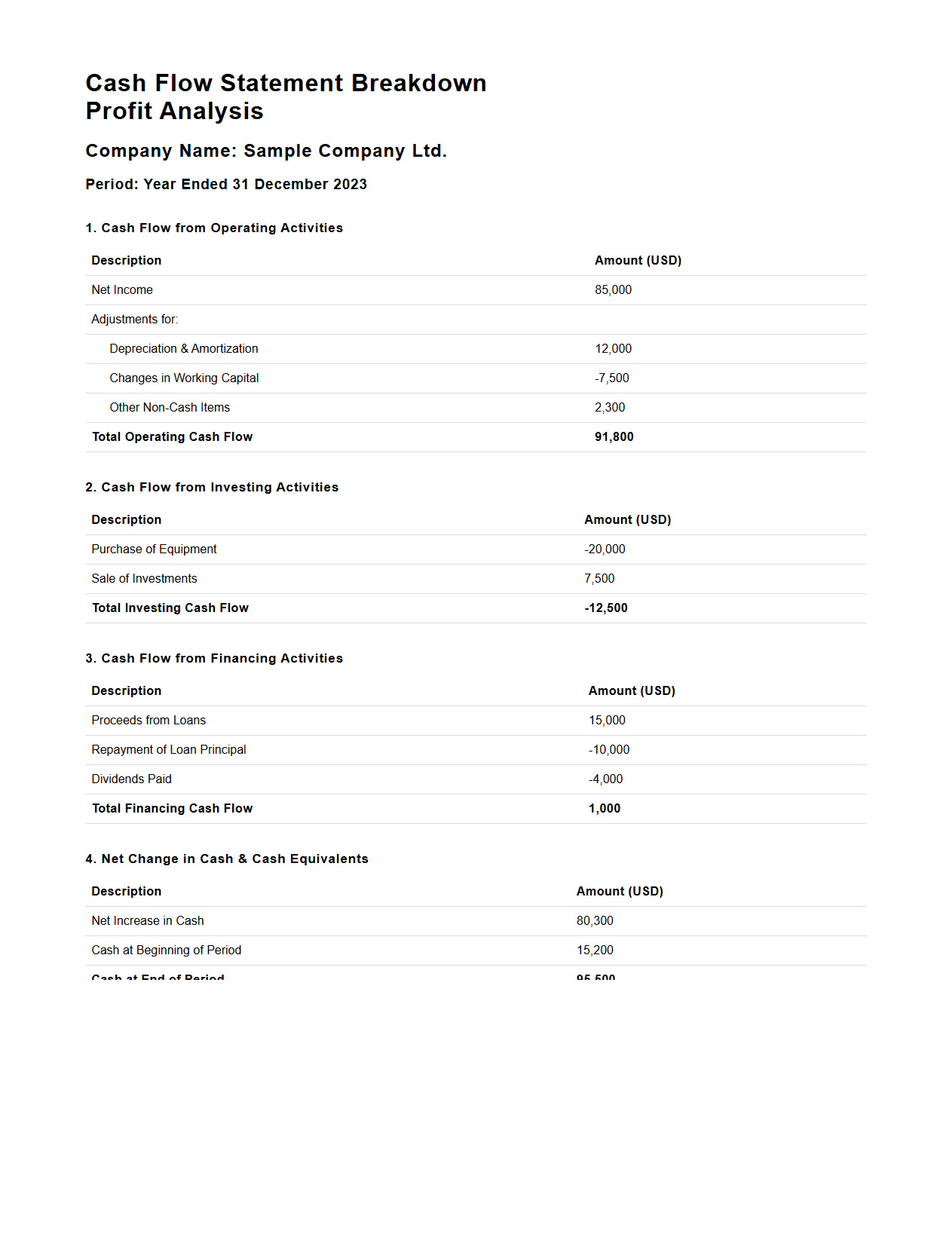

Cash Flow Statement Breakdown for Profit Analysis

The

Cash Flow Statement Breakdown for Profit Analysis document provides a detailed examination of cash inflows and outflows, categorizing operating, investing, and financing activities to assess a company's liquidity and profitability. It highlights how cash movement affects profit margins, enabling stakeholders to identify trends and make informed financial decisions. This breakdown supports comprehensive profit analysis by linking cash generation with expense management and investment returns.

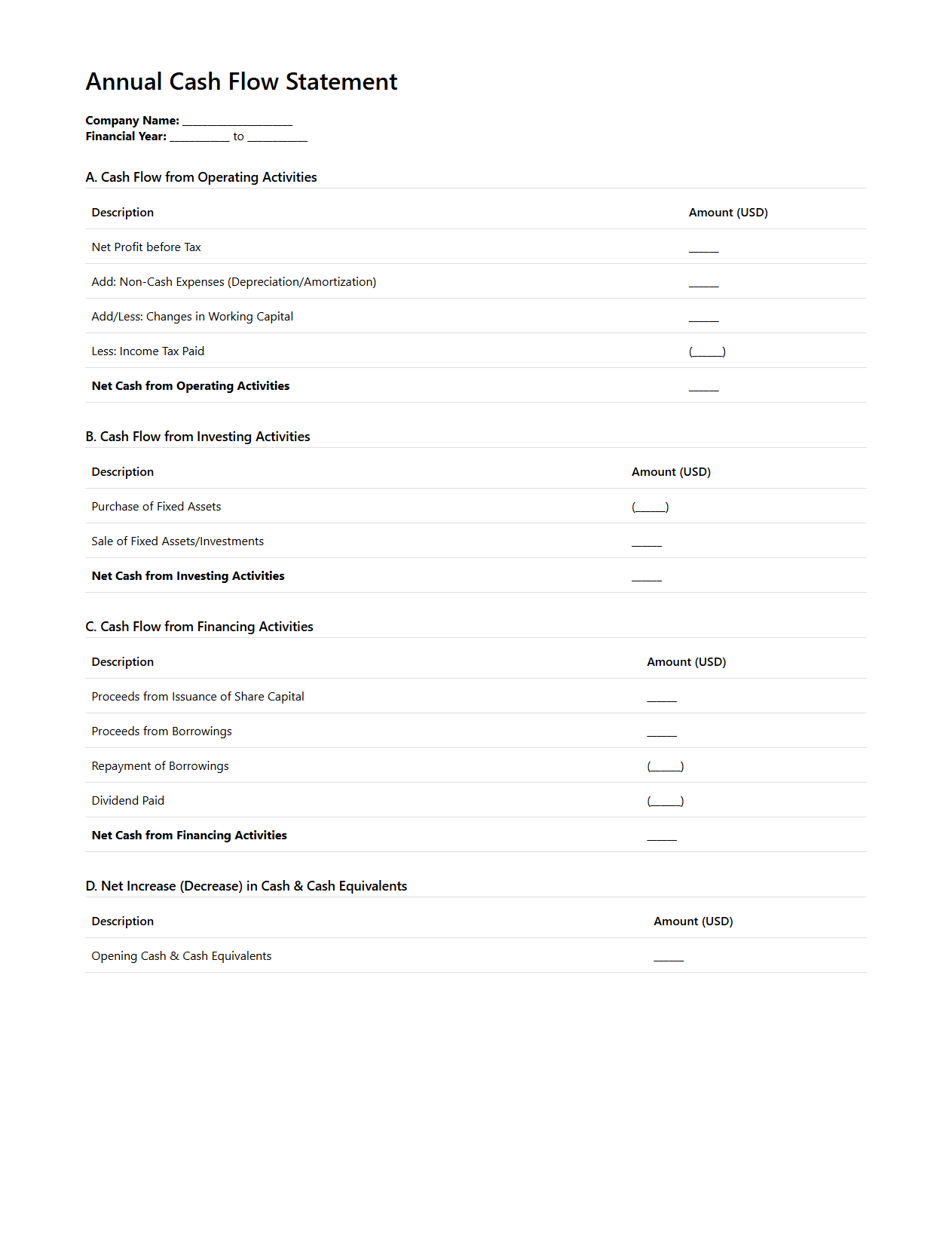

Annual Cash Flow Statement Format for Assessing Profit

The

Annual Cash Flow Statement Format for assessing profit is a structured financial document that details the inflows and outflows of cash over a fiscal year, highlighting operating, investing, and financing activities. This format enables businesses to evaluate their liquidity, operational efficiency, and ability to generate profit through cash management. Analysts utilize this statement to make informed decisions about financial health and sustainability.

What are the key components included in the format of a Cash Flow Statement for profit assessment?

The Cash Flow Statement primarily consists of three key components: operating activities, investing activities, and financing activities. Each section reports the cash inflows and outflows related to specific business operations, asset purchases or sales, and funding sources respectively. This format helps users understand how cash is generated and utilized within the business, essential for assessing profit liquidity.

How does the Cash Flow Statement distinguish between operating, investing, and financing activities?

Operating activities include cash flows from core business operations such as receipts from sales and payments to suppliers. Investing activities involve cash used for or obtained from buying and selling long-term assets like equipment or property. Financing activities relate to transactions with shareholders and creditors, such as issuing shares or repaying debt, clearly separating the company's financial operations from its main business activities.

Which method (direct or indirect) is commonly used in preparing the Cash Flow Statement for profit assessment, and why?

The indirect method is commonly used due to its simplicity and compatibility with accrual accounting systems. It starts with net profit and adjusts for non-cash items and changes in working capital to arrive at net cash from operating activities. This approach provides a clear reconciliation between net profit and actual cash generated, making it easier for profit assessment.

How are non-cash expenses such as depreciation treated in the Cash Flow Statement format?

Non-cash expenses like depreciation are added back to net profit in the operating activities section because they reduce reported earnings without affecting cash flow. This adjustment ensures the cash flow reflects actual cash movements rather than accounting expenses. It highlights the true cash-generating ability of the business, crucial for accurate profit evaluation.

How does the Cash Flow Statement reflect net profit or loss differently compared to the income statement?

The Cash Flow Statement focuses on cash movement rather than accrual-based earnings reported in the income statement. While the income statement shows profit based on revenues and expenses recognized, the cash flow statement reveals how much cash was actually received or spent. This distinction helps stakeholders understand the liquidity position and sustainability of reported profits.