A Format of Loss Statement for Financial Reporting typically includes key components such as gross revenue, cost of goods sold, operating expenses, and net loss. Each section is clearly itemized to provide a transparent view of the company's financial performance over a specific period. This structured format ensures accurate representation of losses, aiding stakeholders in making informed decisions.

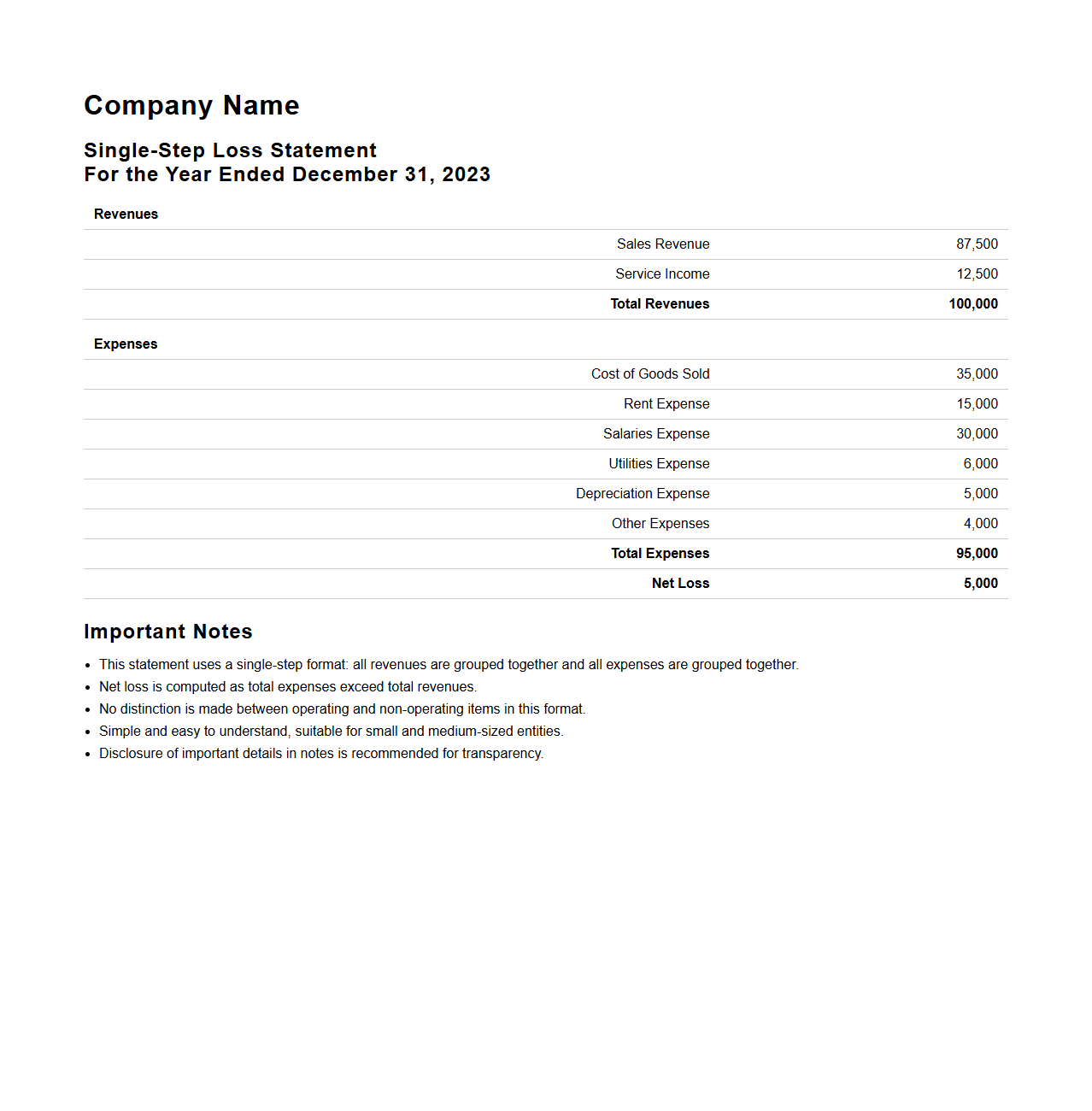

Single-Step Loss Statement Format

The

Single-Step Loss Statement Format is a financial document that consolidates all revenues and gains into a single section and all expenses and losses into another, simplifying the calculation of net loss. This format emphasizes the overall loss or profit by subtracting total expenses from total revenues in one step, without categorizing operating and non-operating items separately. It is particularly useful for businesses seeking straightforward reporting, aiding in quick assessment of financial performance without complex breakdowns.

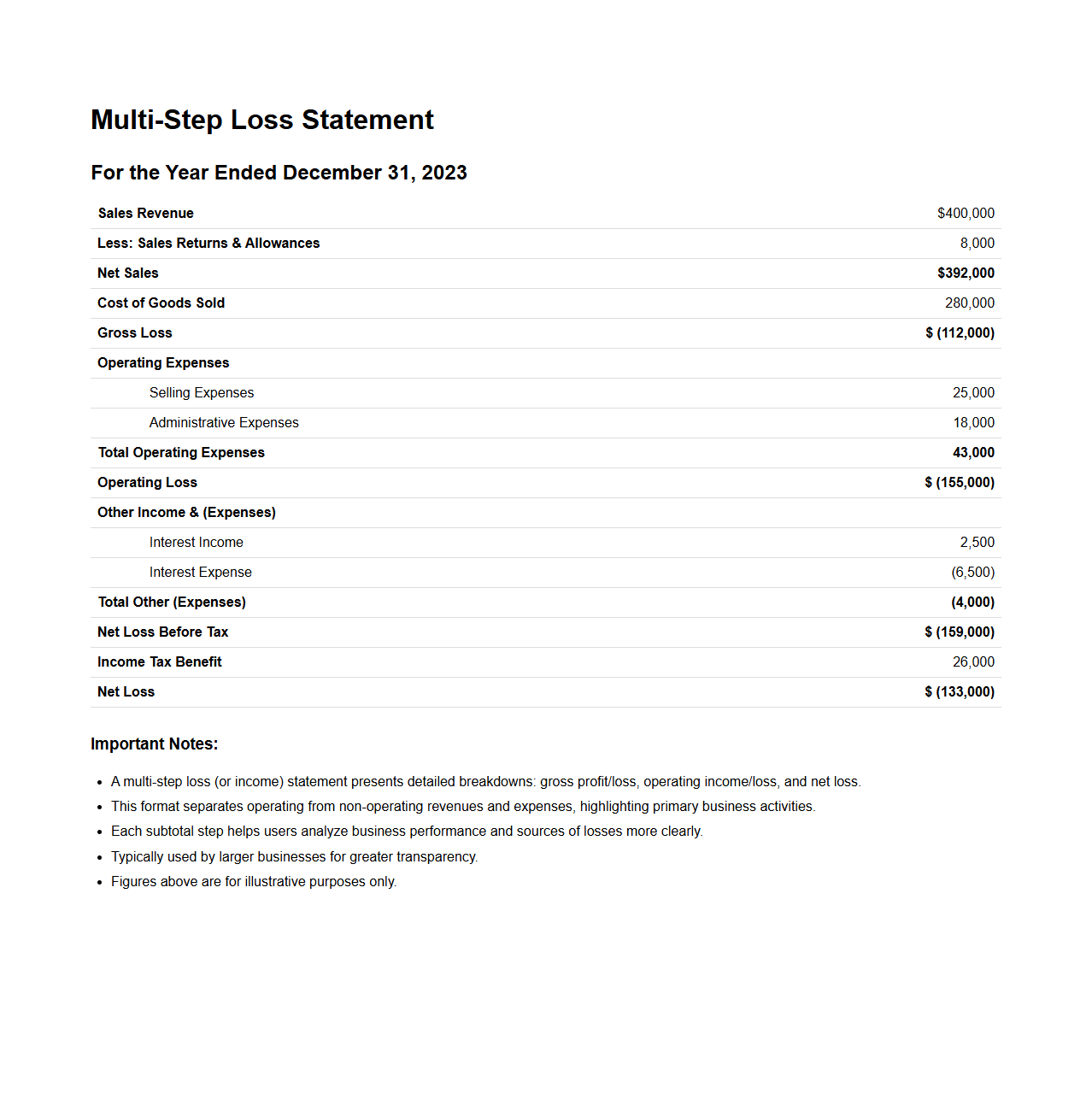

Multi-Step Loss Statement Format

A

Multi-Step Loss Statement Format document organizes insurance claim expenses by detailing multiple categories such as incurred losses, loss reserves, and adjustment expenses to provide a comprehensive overview of financial impacts. This format enables precise tracking and analysis of claim developments over time, facilitating better risk management and accurate financial reporting. Insurers rely on this structured approach to assess overall loss experience, monitor claim trends, and ensure regulatory compliance.

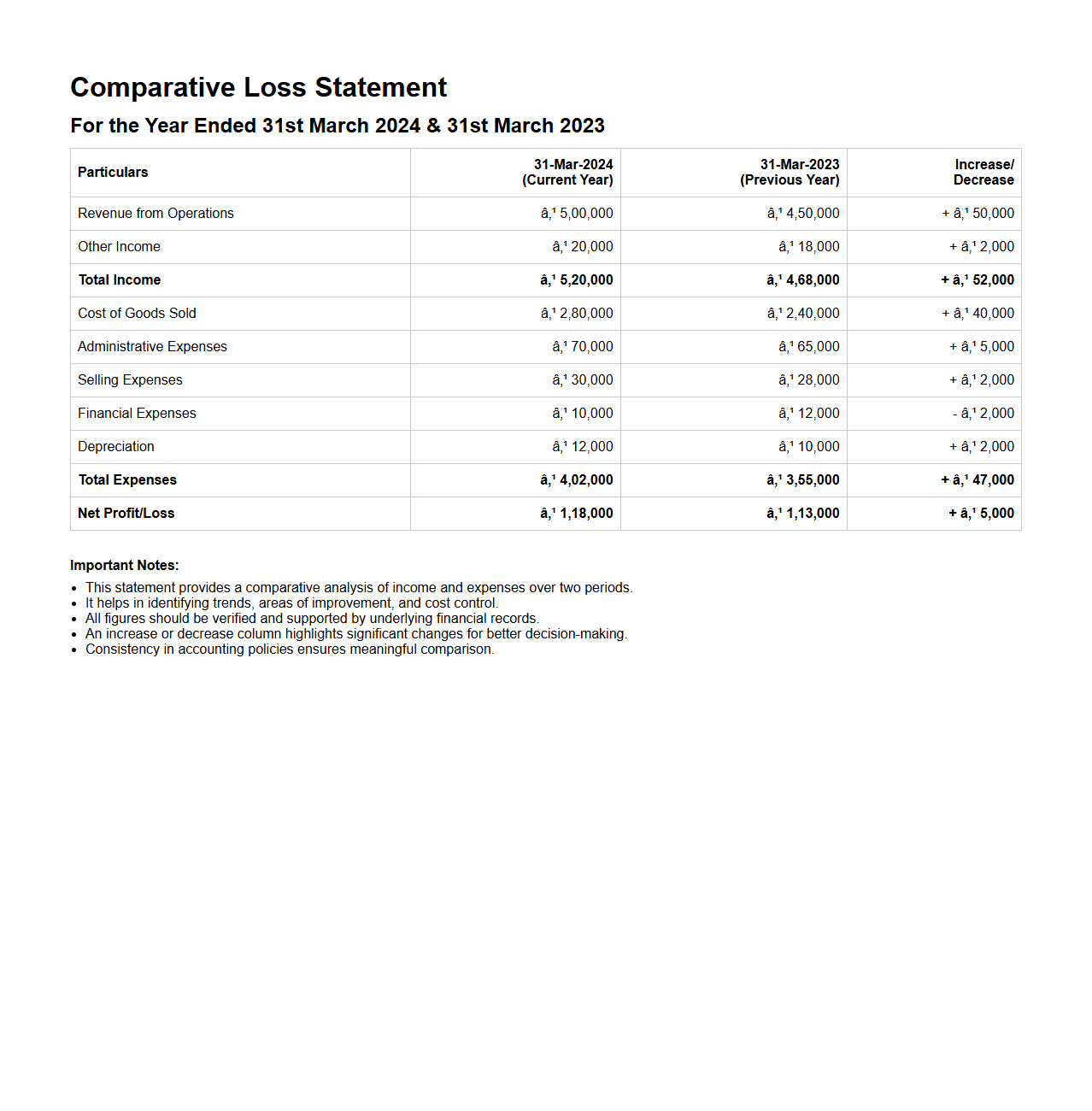

Comparative Loss Statement Format

A

Comparative Loss Statement Format document systematically presents financial loss data across multiple periods, enabling clear analysis of trends and variances in business performance. This format highlights key loss components side-by-side, facilitating informed decision-making and strategic planning by identifying areas of increased risk or inefficiency. Businesses often use this document to benchmark losses over quarters or years, ensuring accurate financial reporting and regulatory compliance.

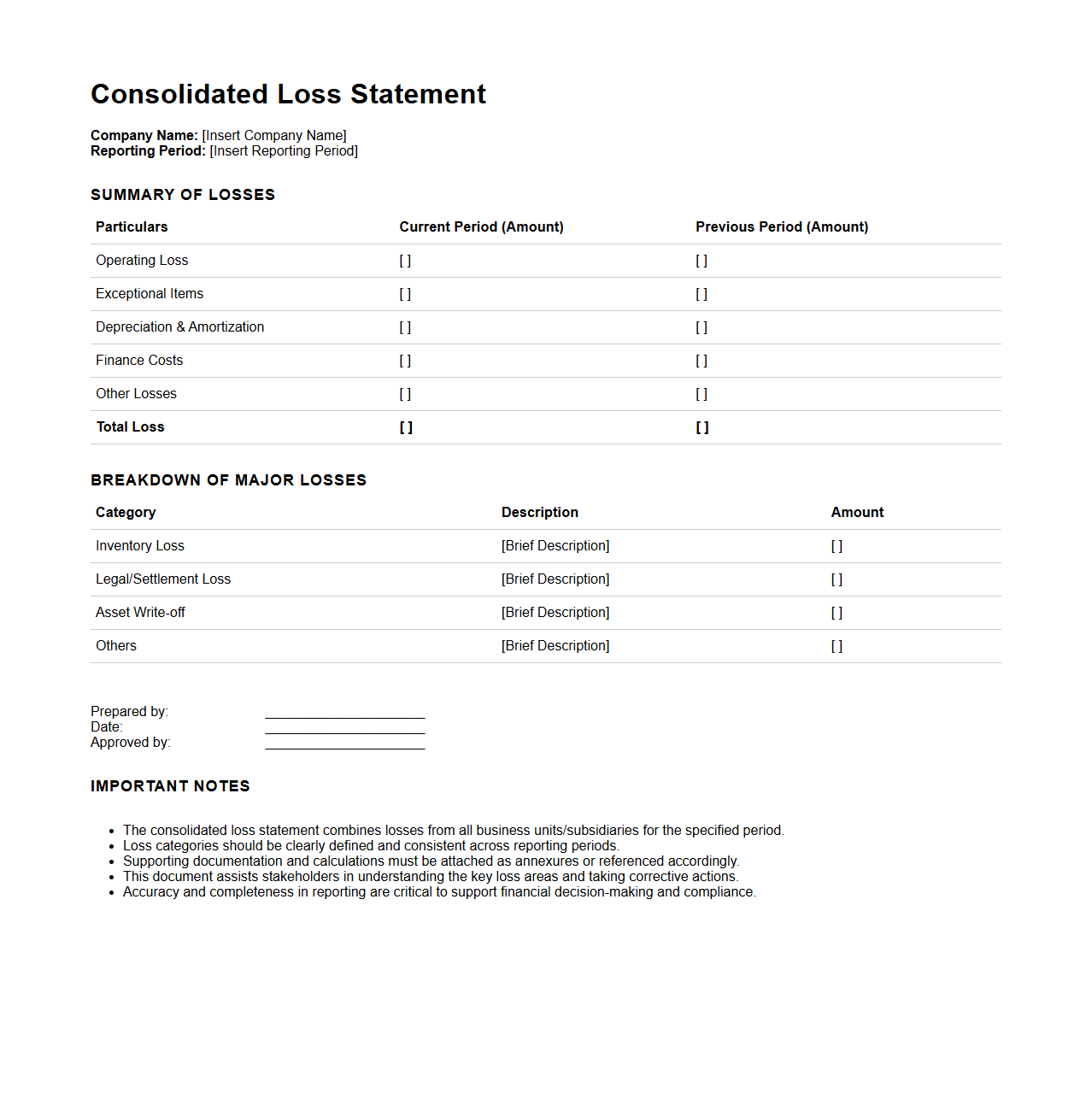

Consolidated Loss Statement Format

A

Consolidated Loss Statement Format document provides a comprehensive summary of the aggregate financial losses incurred by a company or group of companies during a specific period. It combines individual loss statements from all subsidiaries or business units, presenting a unified view of total expenses, provisions for bad debts, and other loss-related financial impacts. This format is essential for accurate financial reporting, regulatory compliance, and strategic risk management within corporate groups.

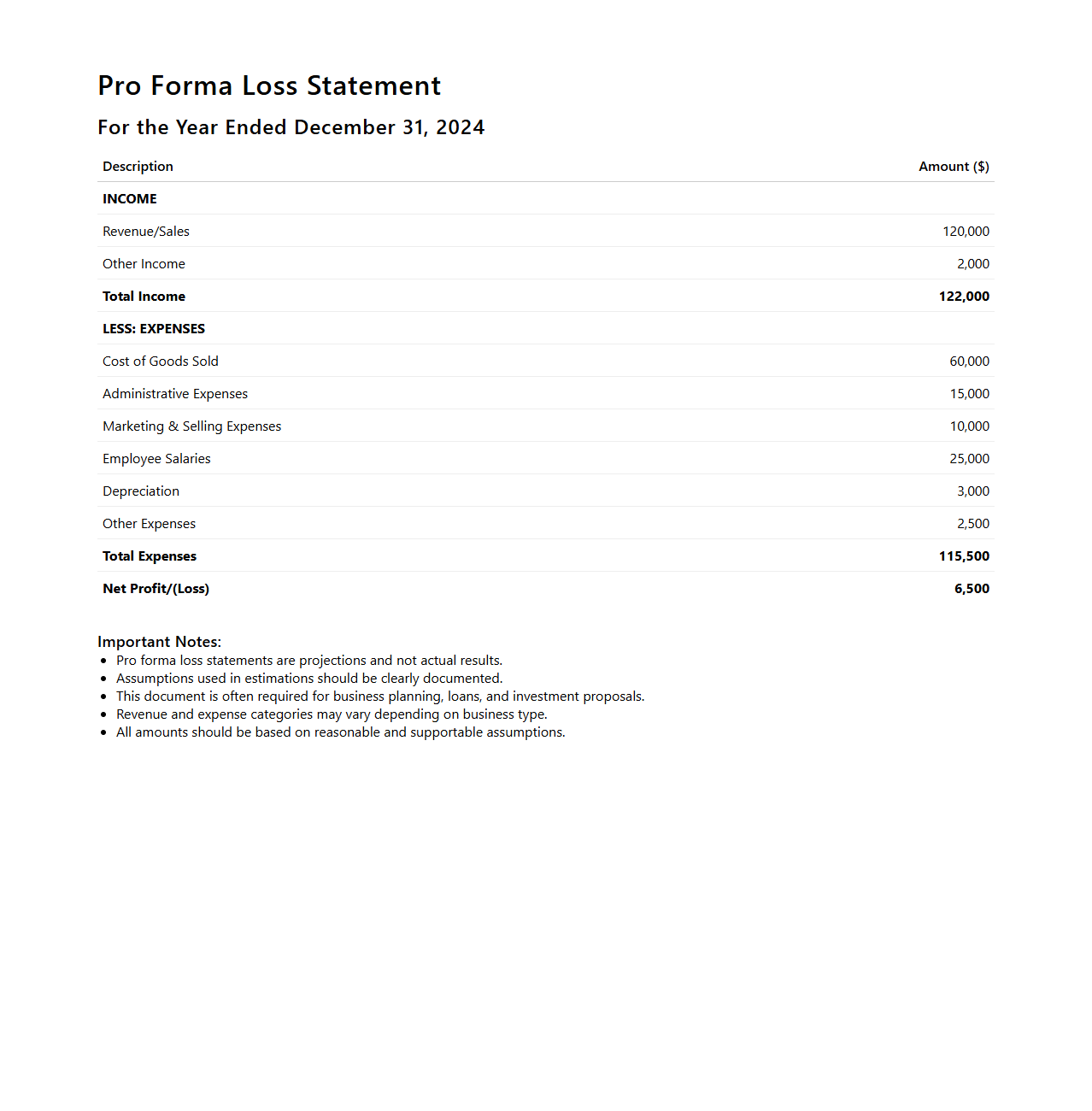

Pro forma Loss Statement Format

A

Pro forma Loss Statement Format document is a financial report used to project potential losses within a specific period based on hypothetical scenarios or anticipated business activities. It helps stakeholders assess risk by estimating expenses, losses, and overall financial impact before actual transactions occur. This format is essential for budgeting, strategic planning, and evaluating the viability of business decisions.

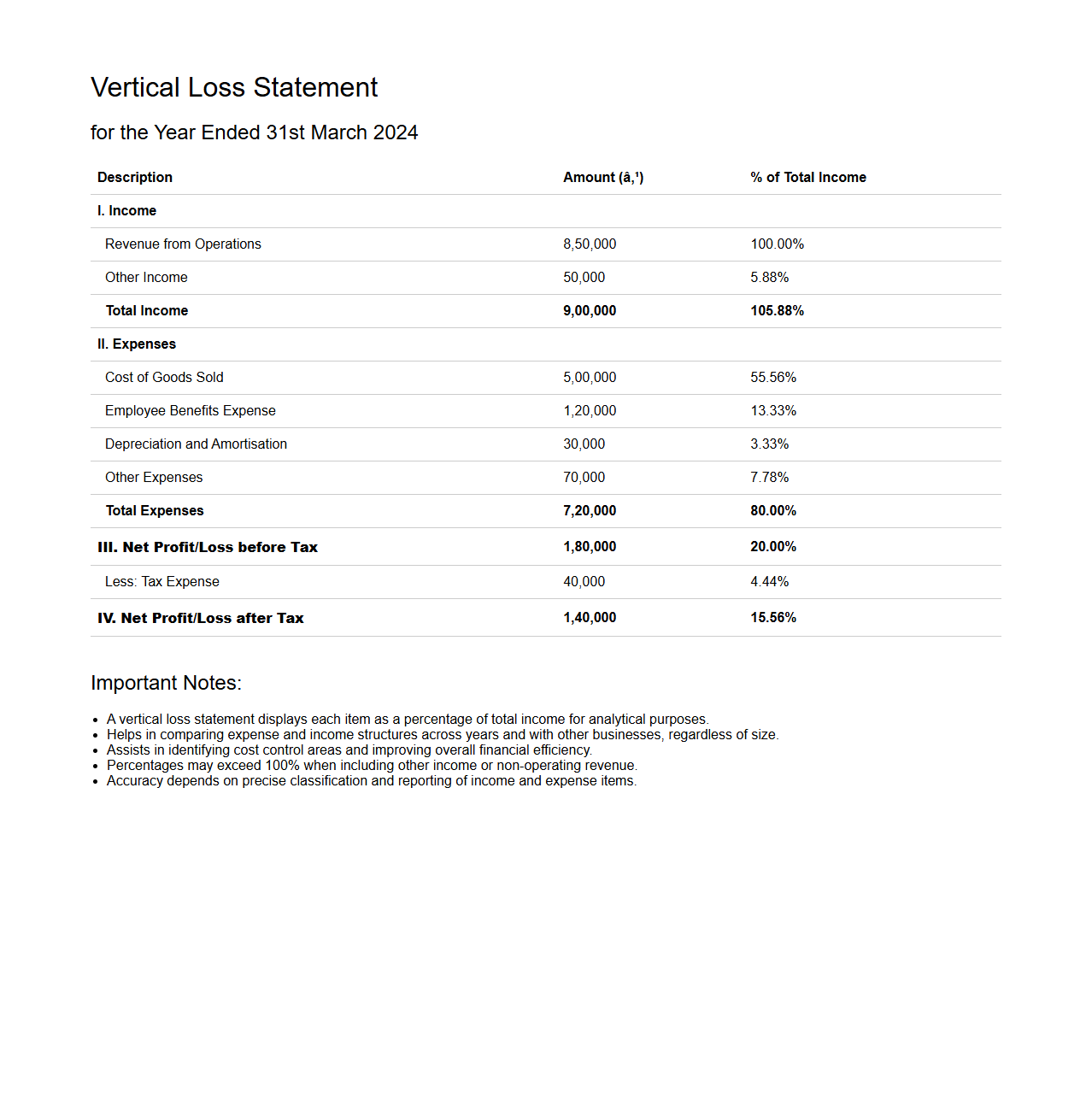

Vertical Loss Statement Format

A

Vertical Loss Statement Format document organizes financial losses by listing each expense category in a downward sequence, allowing clear visibility of total losses and their impact on net income. This format emphasizes the proportional relationship of each loss component relative to total revenue, which helps businesses identify critical areas of financial concern. It is widely used in accounting and financial analysis for precise loss tracking and reporting.

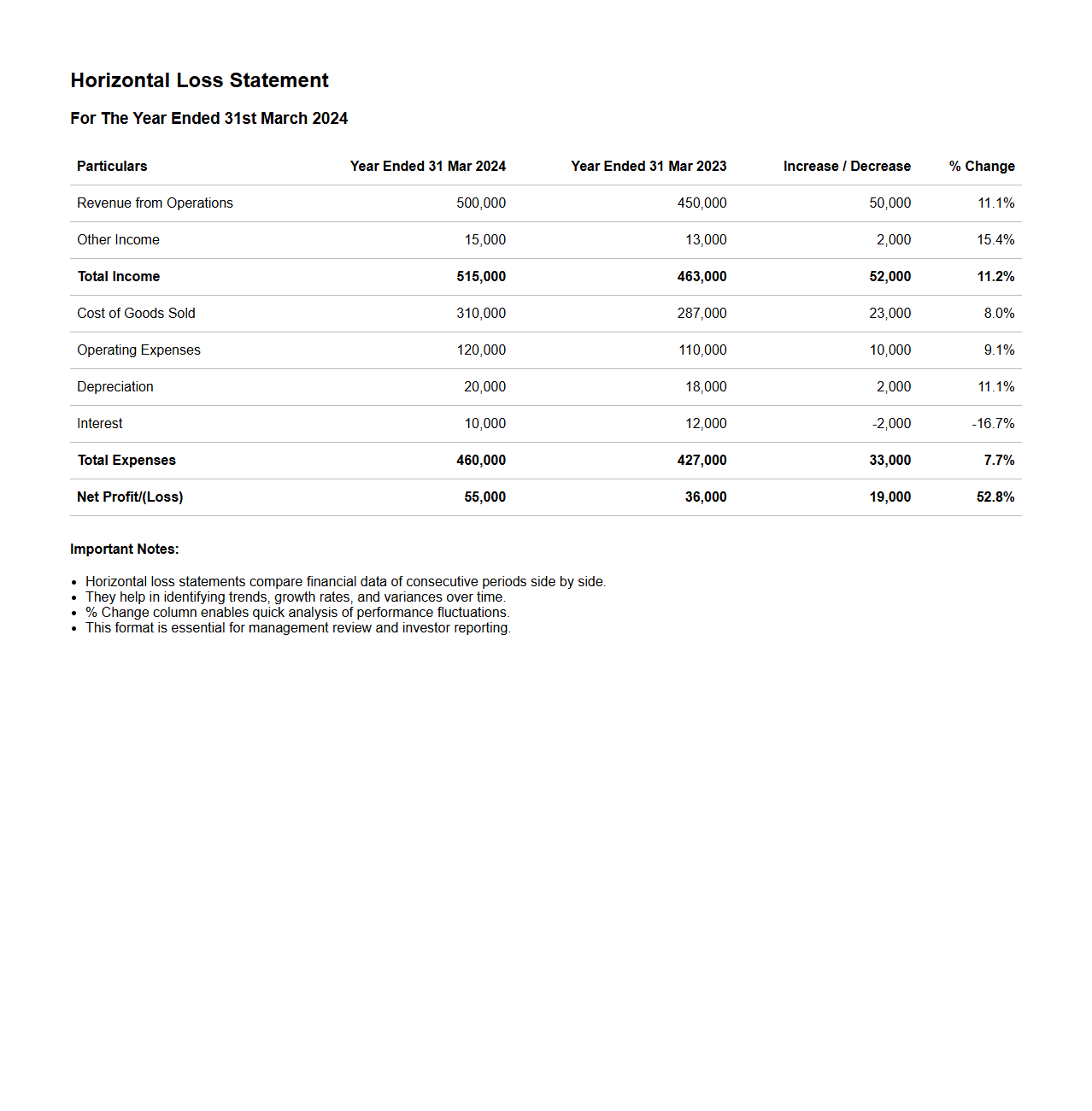

Horizontal Loss Statement Format

The

Horizontal Loss Statement Format document presents financial data in a structured, side-by-side layout, allowing for easy comparison of losses across multiple periods or categories. This format typically includes columns for various time frames or loss types, enabling businesses to track trends and identify areas needing improvement efficiently. It is a crucial tool for accountants and financial analysts to assess and communicate loss-related information clearly and effectively.

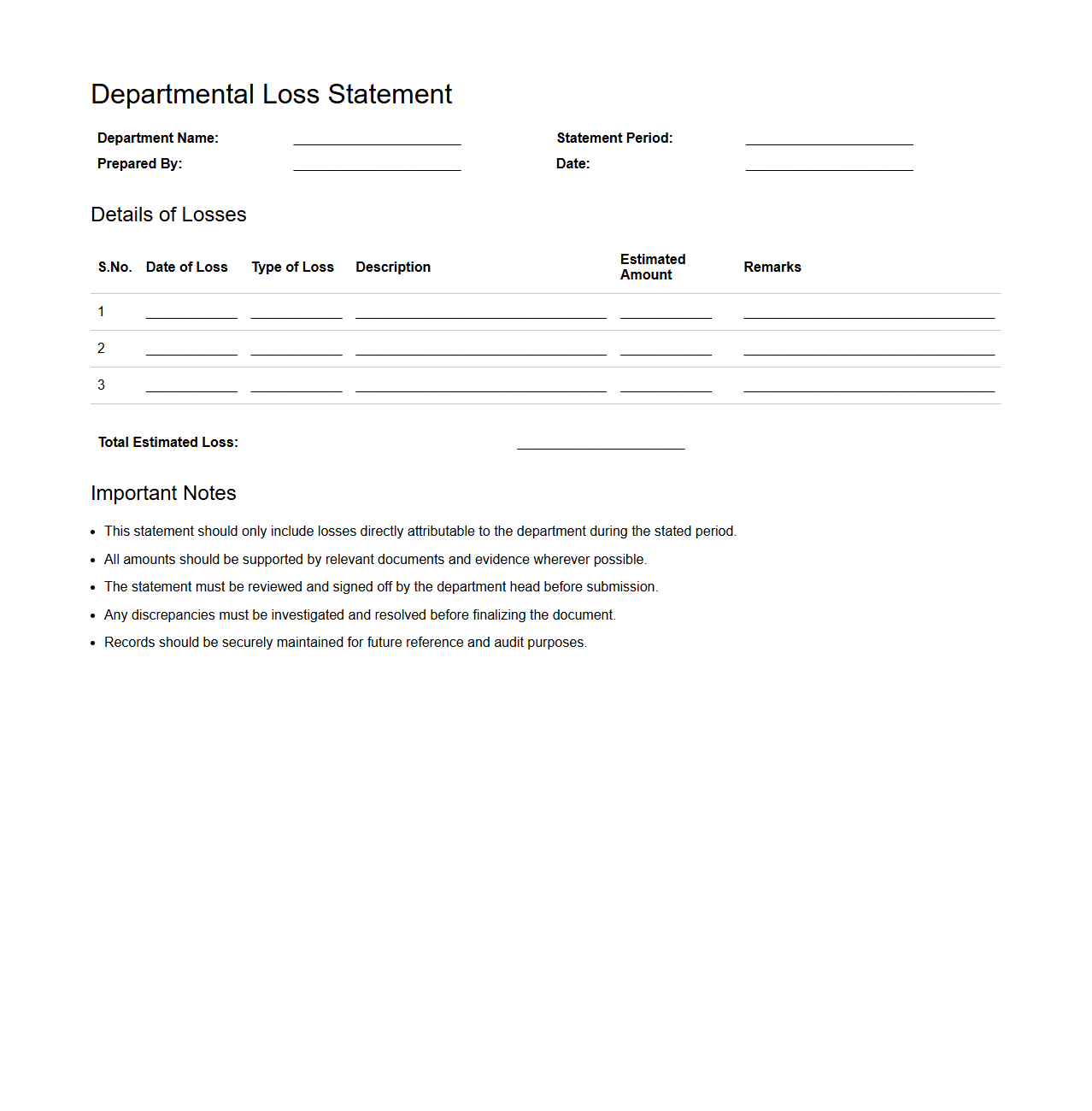

Departmental Loss Statement Format

A

Departmental Loss Statement Format document organizes and presents financial losses incurred by individual departments within an organization, enabling clear tracking and analysis. It typically includes fields for department name, period, types of losses, amounts, and explanations, helping management identify loss sources and implement corrective measures. This format is essential for maintaining transparency, budgeting accuracy, and improving overall financial performance.

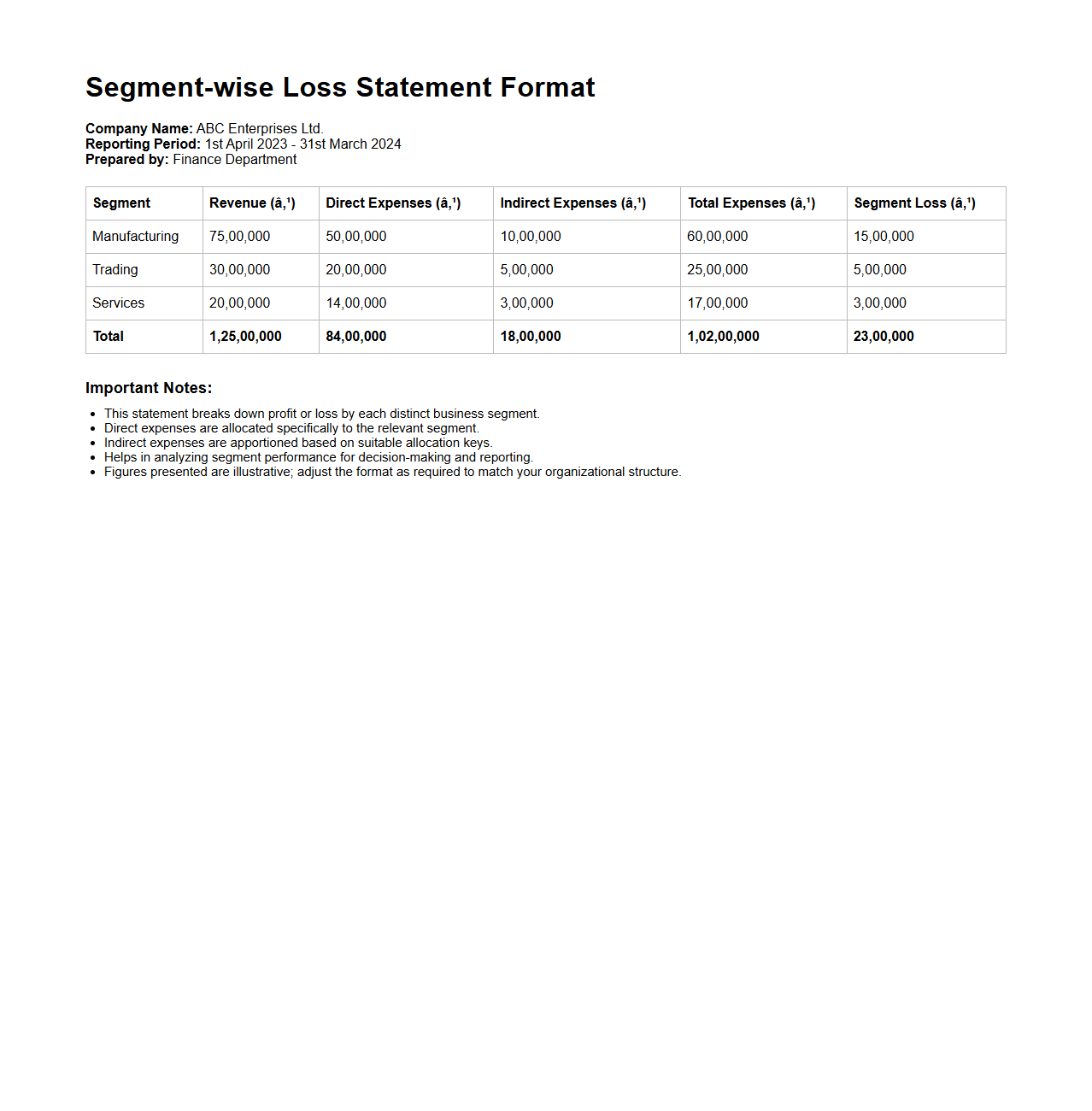

Segment-wise Loss Statement Format

The

Segment-wise Loss Statement Format document systematically categorizes financial losses incurred across different business segments, enabling precise tracking and analysis. This format aids organizations in identifying loss patterns, facilitating better risk management and targeted corrective measures. Detailed segment-wise data ensures transparency and supports strategic decision-making for improved financial performance.

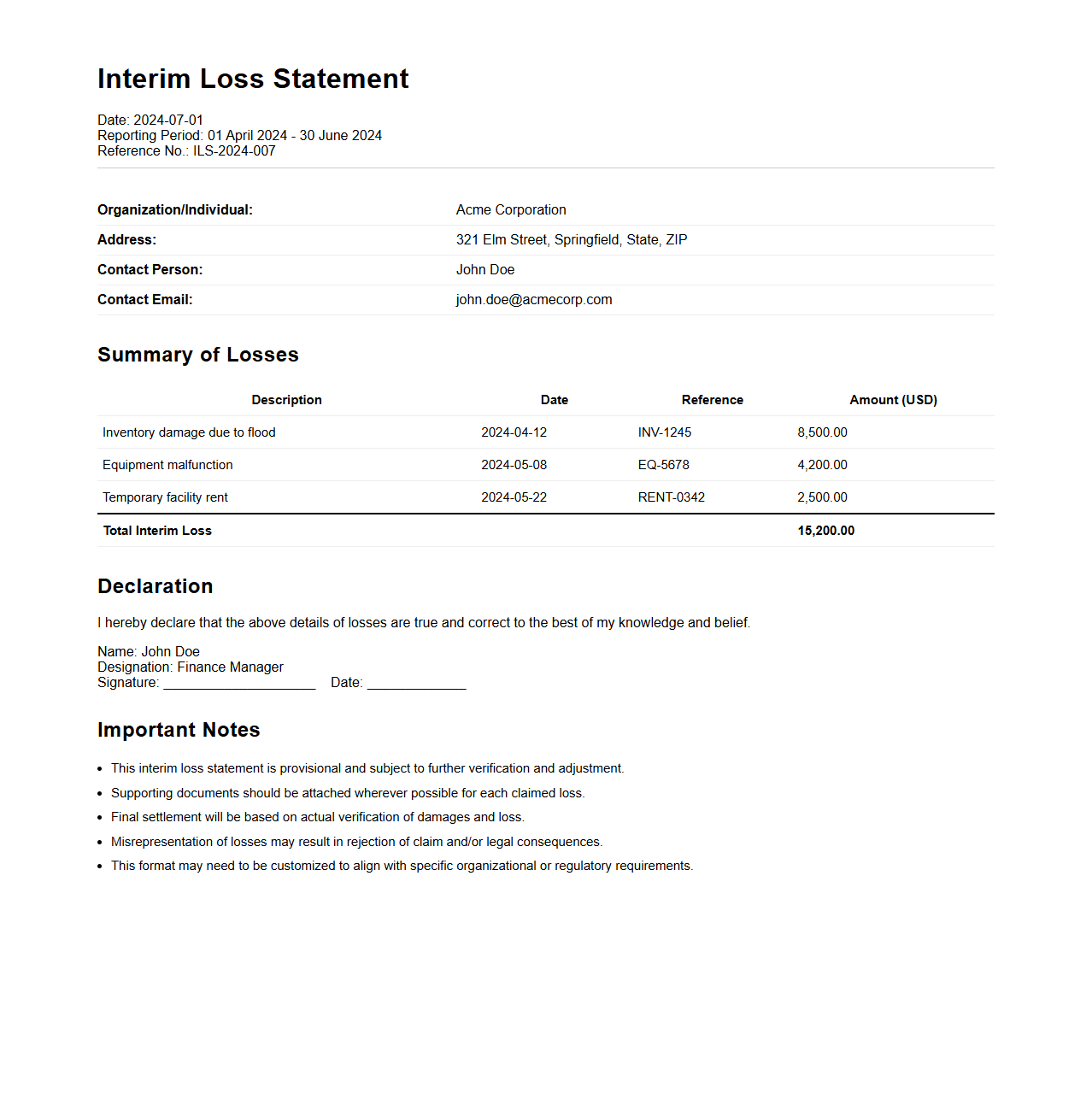

Interim Loss Statement Format

An

Interim Loss Statement Format document provides a structured template for reporting financial losses incurred over a specific interim period, such as quarterly or semi-annually. It enables businesses to present detailed loss figures, including causes and impacted areas, facilitating accurate financial analysis and decision-making. This format is essential for maintaining transparency with stakeholders and supports timely adjustments in financial strategies.

What key components are required in the format of a Loss Statement for financial reporting?

A Loss Statement must include essential components such as total revenues, cost of goods sold, gross loss, operating expenses, and non-operating losses. It should clearly distinguish between operating and non-operating activities to provide transparency. Additionally, net loss and earnings per share are critical elements for comprehensive reporting.

How should operating and non-operating losses be presented in a Loss Statement?

Operating losses should be presented separately from non-operating losses to highlight the company's core business performance. Operating losses typically appear immediately after the calculation of gross profit or gross loss. Non-operating losses are shown below operating income, ensuring clear differentiation for stakeholders.

Which accounting standards govern the structure and presentation of a Loss Statement?

The International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP) provide the framework for Loss Statement presentation. These standards ensure consistency, comparability, and transparency in financial reporting. Compliance with these accounting standards is mandatory for accurate and reliable financial disclosures.

How are extraordinary items and discontinued operations disclosed in a Loss Statement?

Extraordinary items and discontinued operations must be separately disclosed in the Loss Statement to avoid distorting ongoing business results. Typically, these are presented after income from continuing operations but before net income or net loss. This segregation aids users in understanding the impact of unusual or non-recurring events on financial performance.

What sequence should be followed when arranging expenses and losses in the Loss Statement?

The correct sequence entails listing expenses starting with cost of goods sold, followed by operating expenses, then non-operating losses. Exceptional items like discontinued operations and extraordinary items come next. Finally, the net loss or net income figure is presented at the bottom for a clear snapshot of financial results.