The Format of Trial Balance for Ledger typically includes three columns: the account names, debit balances, and credit balances. Each ledger account balance is listed under its respective debit or credit column to ensure total debits equal total credits. This structured format helps in detecting errors and verifying the accuracy of the ledger accounts.

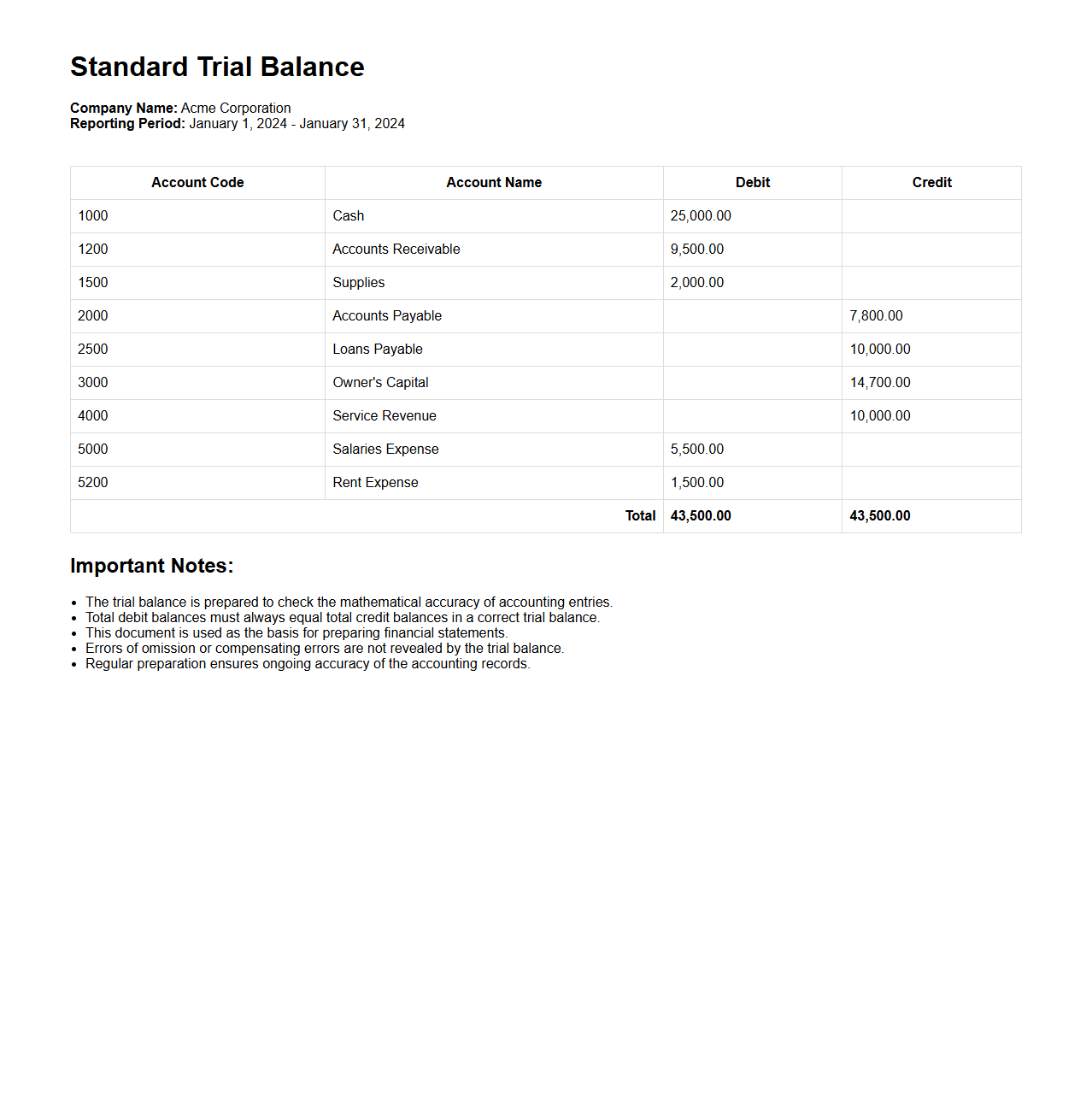

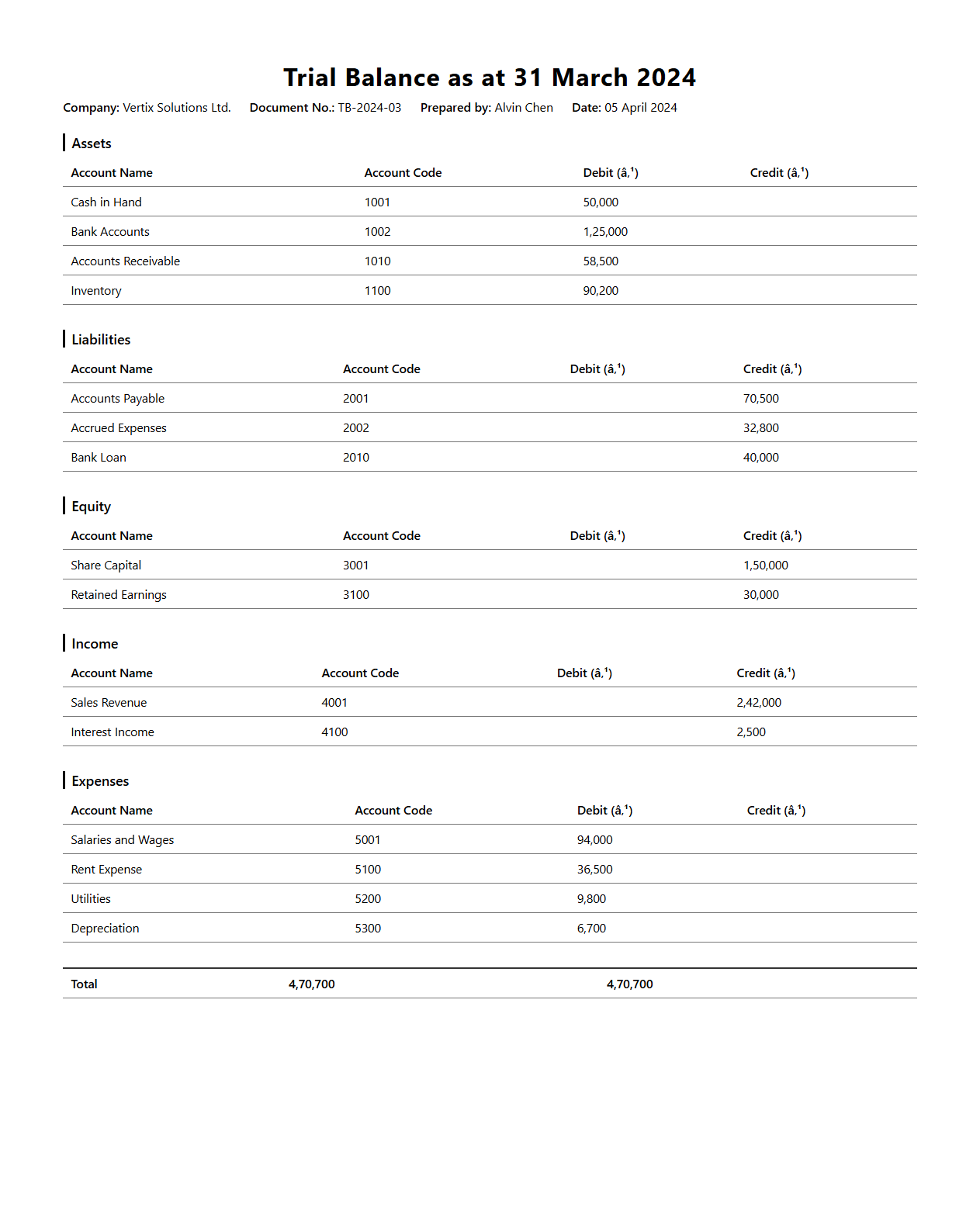

Standard Trial Balance Document Format

A

Standard Trial Balance Document Format is a structured financial report that lists all ledger accounts and their balances at a specific point in time, used to verify the accuracy of bookkeeping entries. It ensures that total debits equal total credits, serving as a key tool in the accounting cycle before preparing financial statements. This format typically includes columns for account names, debit balances, credit balances, and allows for easy identification of discrepancies.

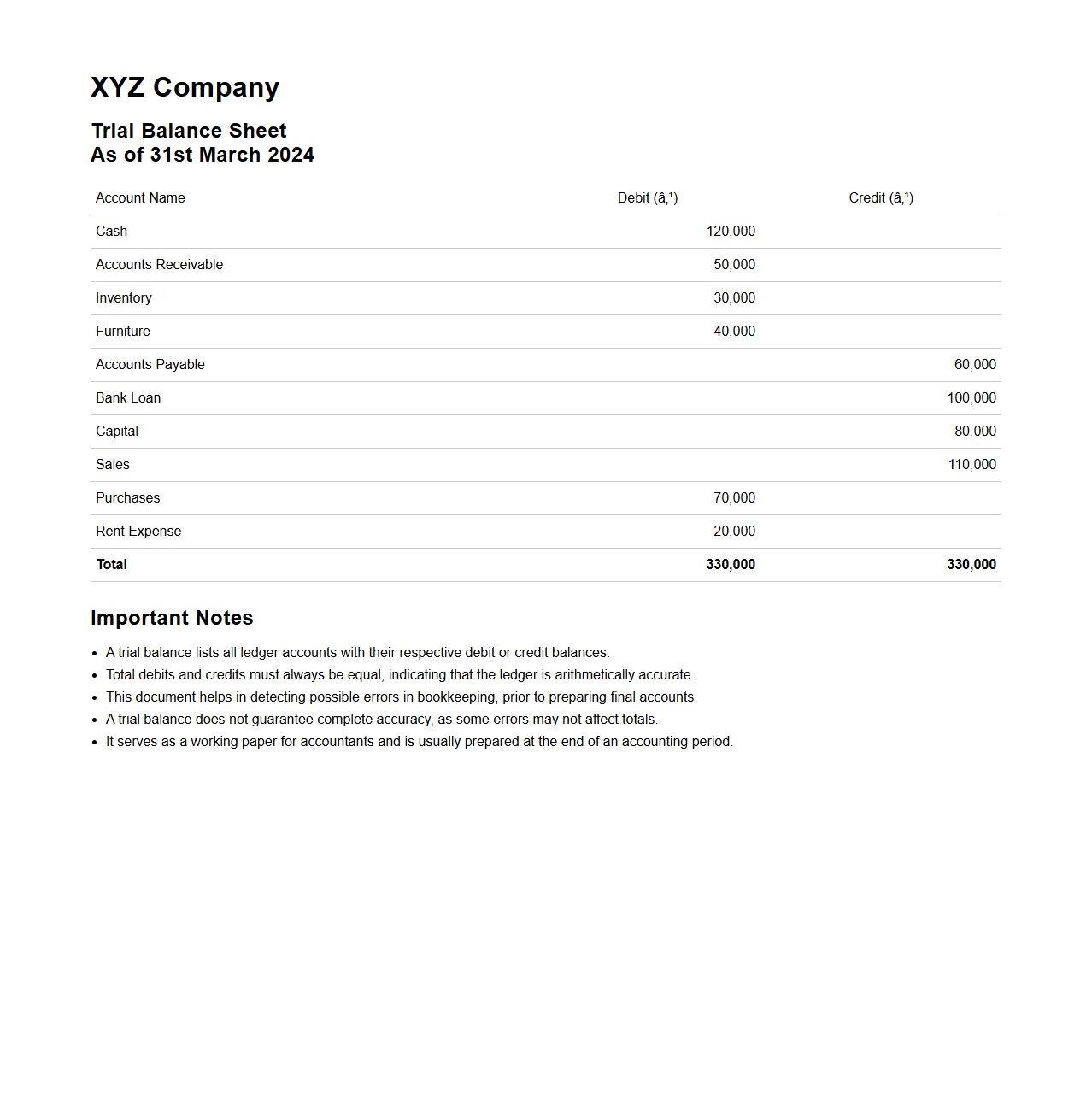

Simple Trial Balance Sheet Format

A

Simple Trial Balance Sheet Format document is a financial statement that lists all general ledger account balances at a specific point in time, ensuring that total debits equal total credits. It serves as a foundational tool for detecting errors in bookkeeping and verifying the accuracy of financial records during the accounting cycle. This format is essential for preparing accurate financial statements and maintaining balanced accounts.

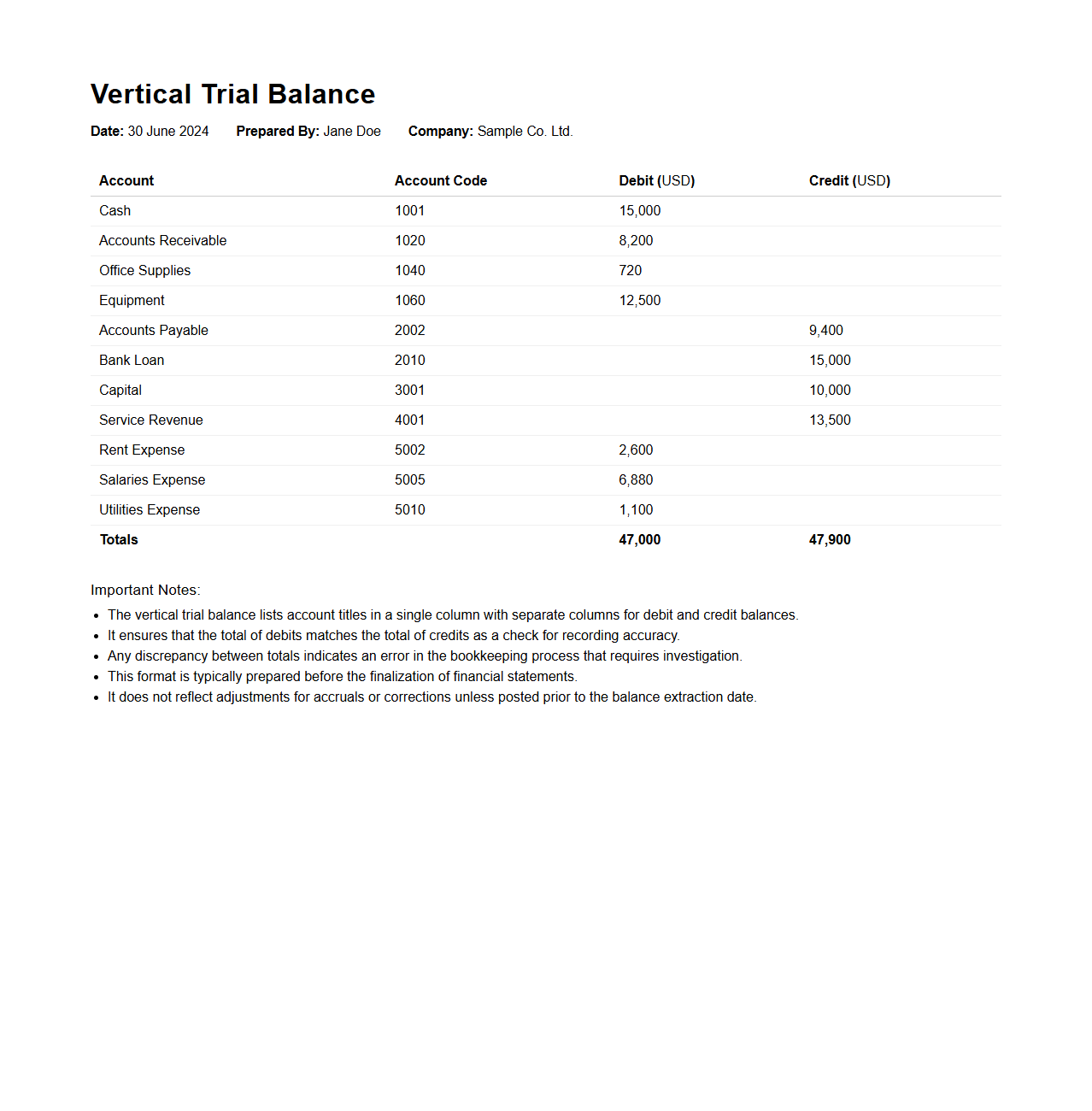

Vertical Trial Balance Document Template

A

Vertical Trial Balance Document Template is a structured financial tool used by accountants to list all ledger account balances in a vertical format, facilitating the detection of discrepancies in double-entry bookkeeping. This template systematically displays debit and credit balances side by side, making it easier to verify that total debits equal total credits before preparing financial statements. It enhances accuracy and efficiency in the reconciliation process and serves as a crucial step in the accounting cycle.

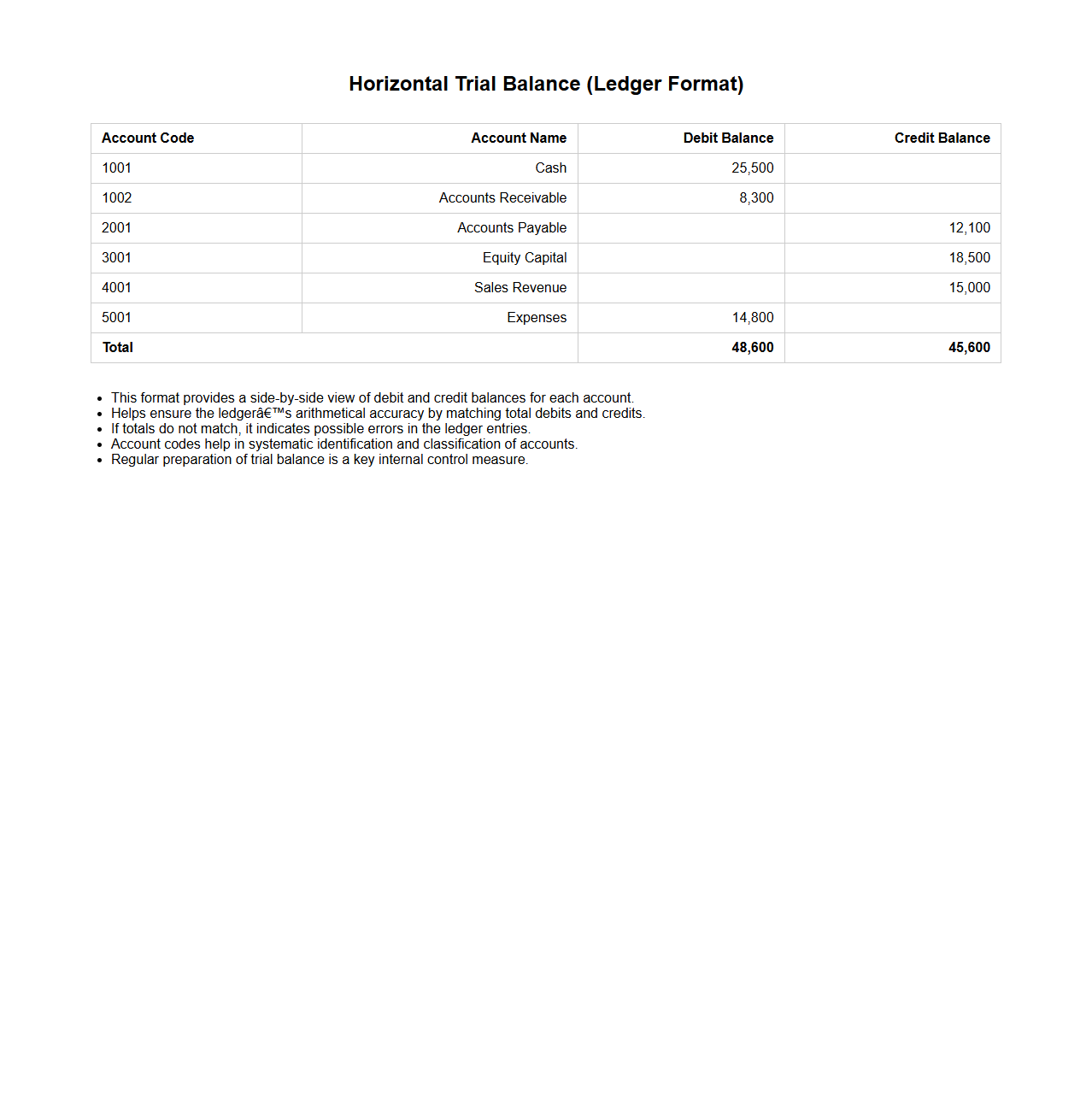

Horizontal Trial Balance Format for Ledger

The

Horizontal Trial Balance Format for a Ledger document organizes debit and credit balances in a side-by-side layout, facilitating easy comparison of account balances across multiple ledger accounts. This format displays accounts horizontally with columns for debit and credit balances, enhancing clarity in financial statement preparation and error detection. It is widely used in accounting to ensure the equality of total debits and credits before finalizing financial reports.

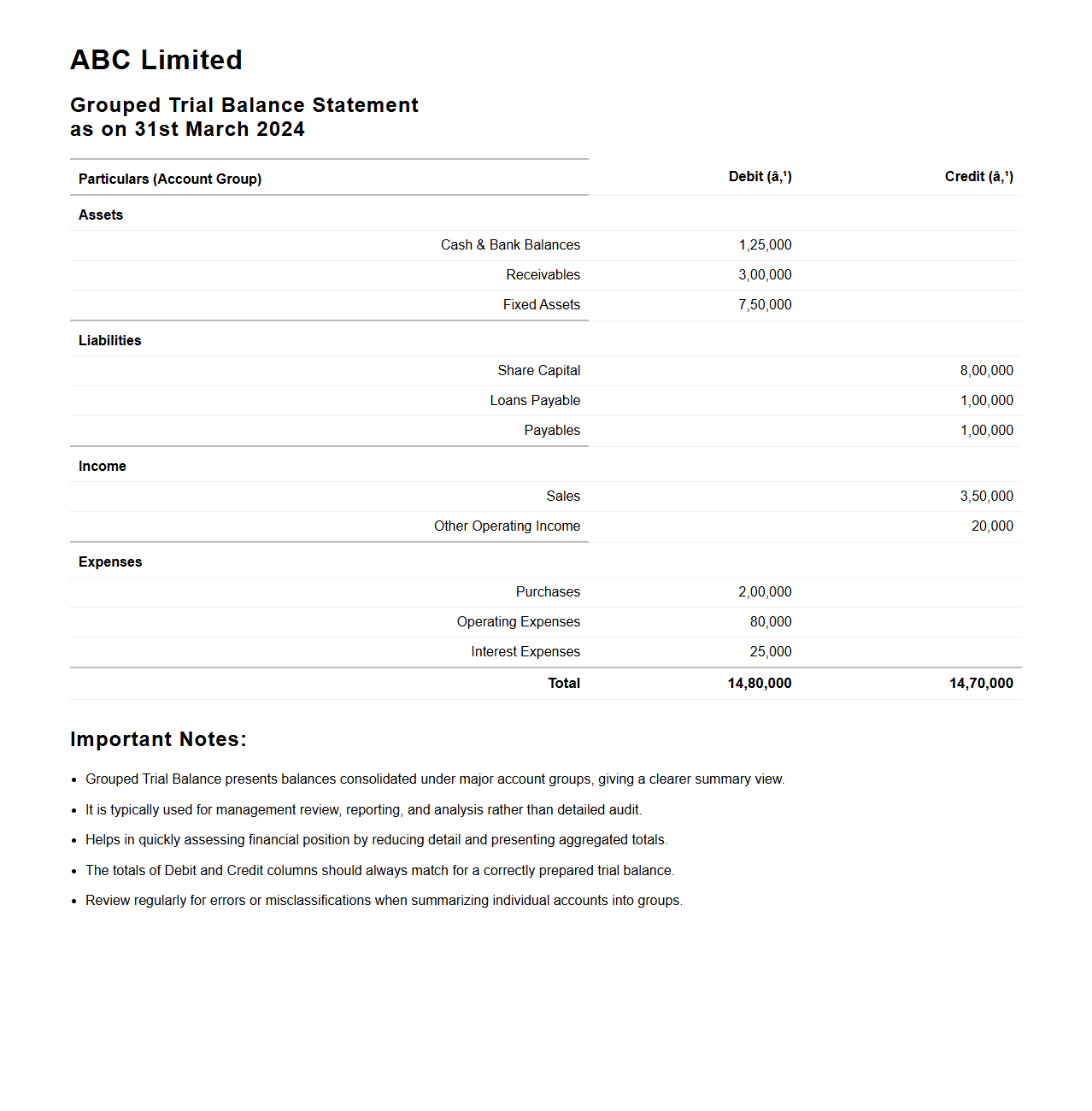

Grouped Trial Balance Statement Format

A

Grouped Trial Balance Statement Format document organizes account balances by categories, such as assets, liabilities, equity, revenues, and expenses, facilitating easier financial analysis and error detection. This format aids accountants in summarizing data efficiently, ensuring all ledger balances are accurately classified before preparing financial statements. Using a grouped layout enhances clarity and supports compliance with accounting standards like GAAP or IFRS.

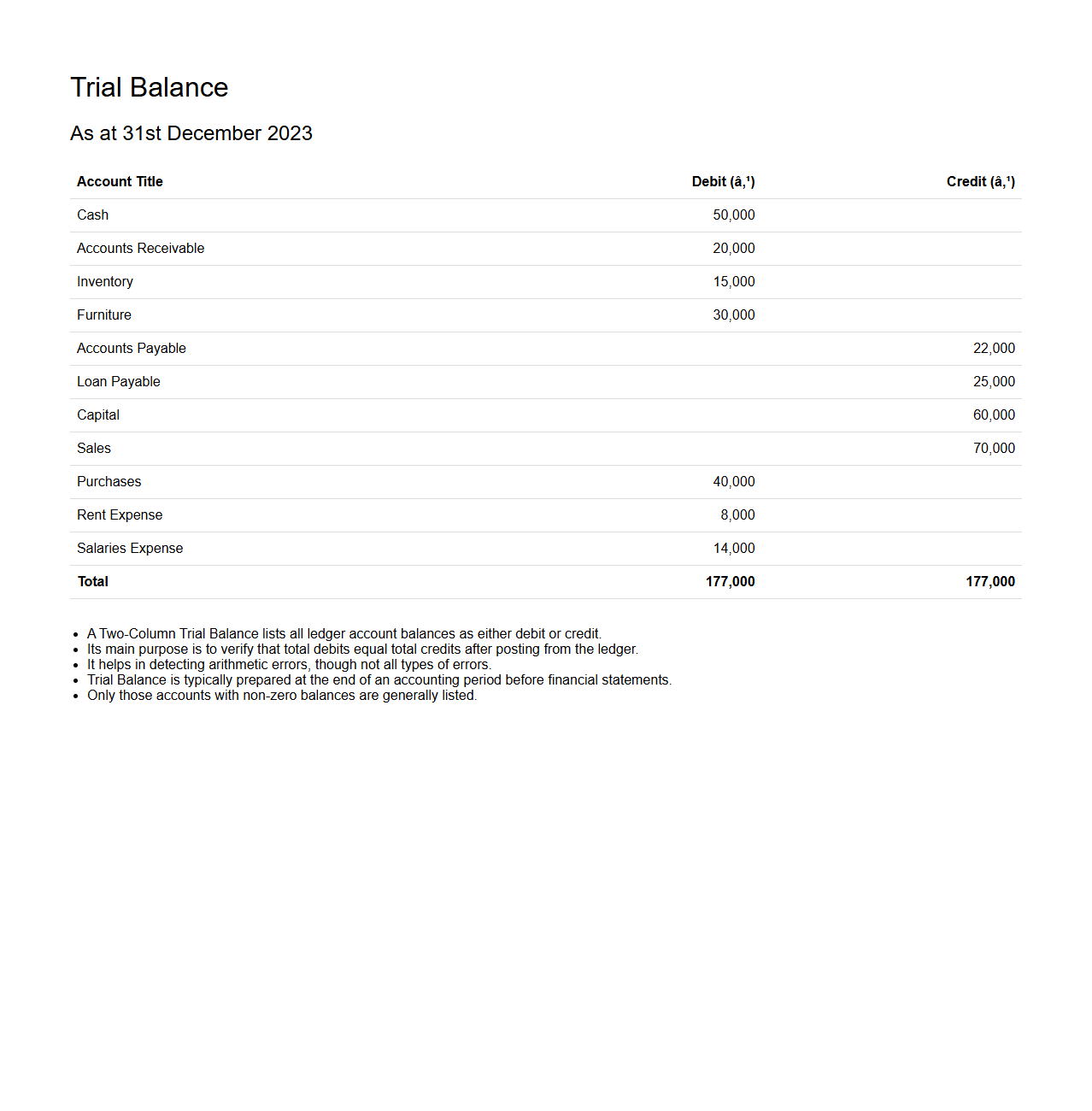

Two-Column Trial Balance Document Format

The

Two-Column Trial Balance Document Format is an accounting tool used to summarize all ledger balances into debit and credit columns, ensuring the accounting equation balances correctly. This document format helps identify discrepancies in accounts by listing each account's balance side-by-side, facilitating easy comparison and error detection. It is essential for preparing financial statements and maintaining accurate bookkeeping records.

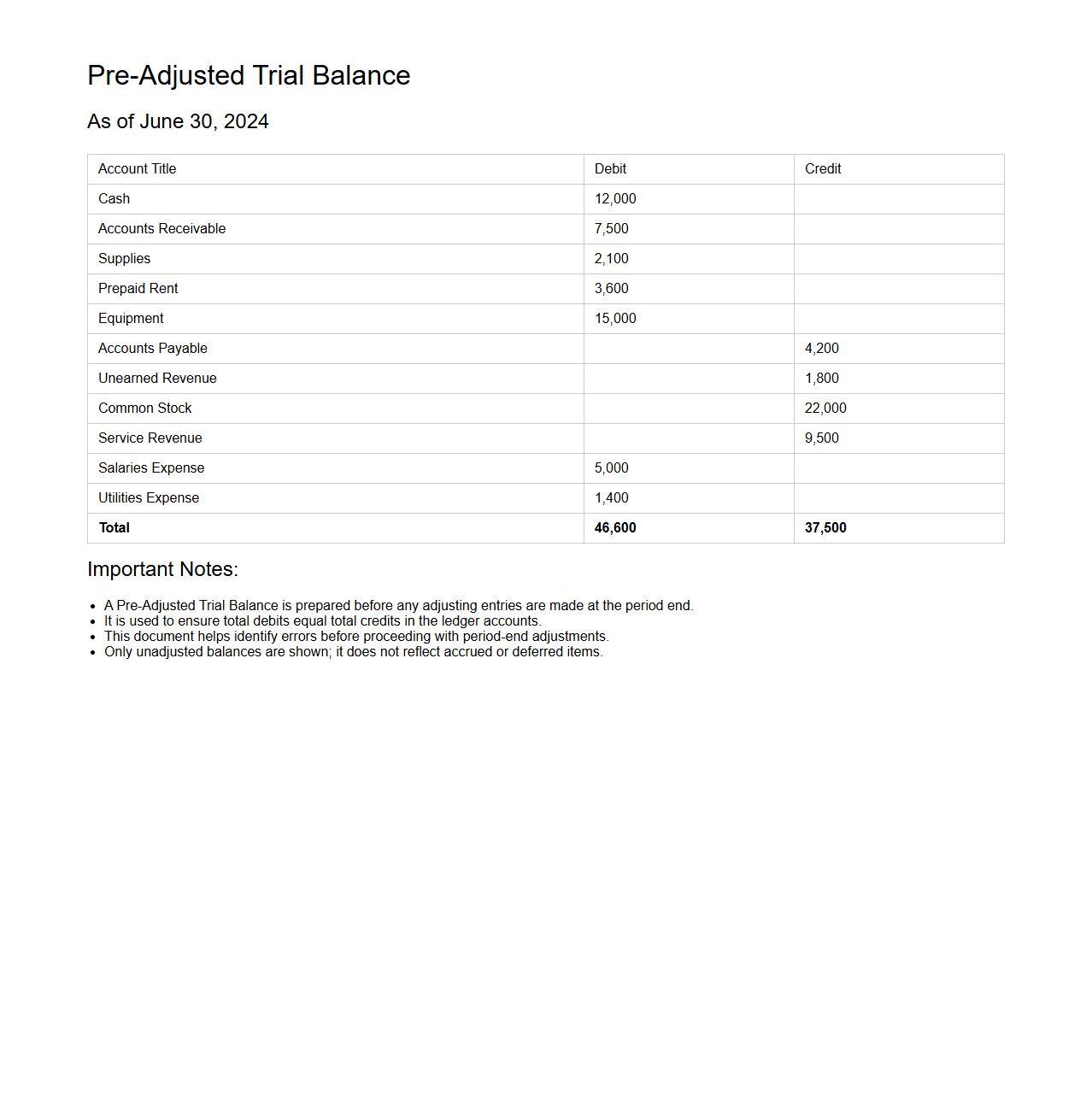

Pre-Adjusted Trial Balance Format

A

Pre-Adjusted Trial Balance Format document lists all ledger account balances before any adjusting entries are made at the end of an accounting period. It serves as a preliminary step in the accounting cycle to verify that total debits equal total credits. This format helps identify discrepancies and prepare for necessary adjustments to ensure accurate financial statements.

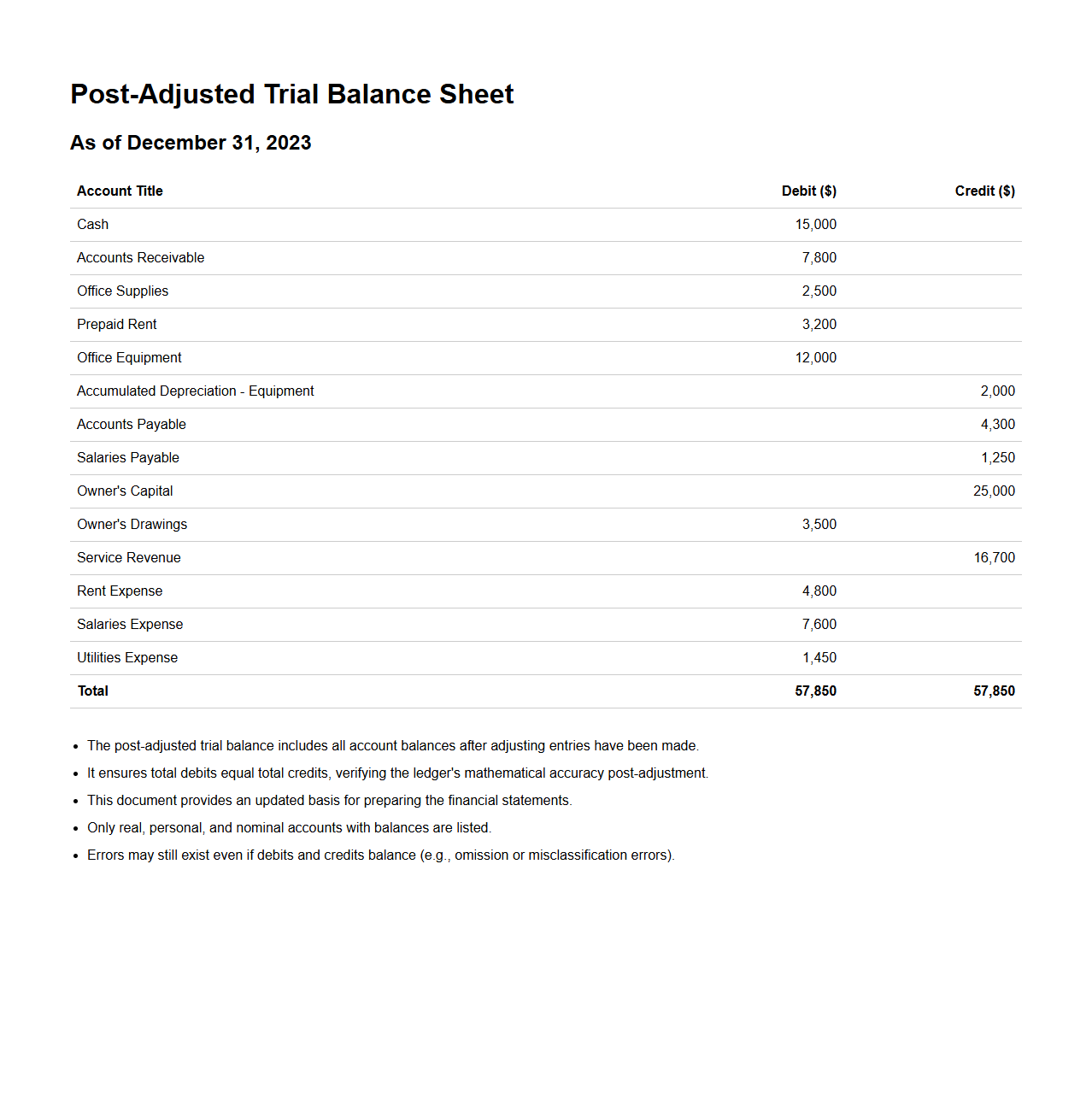

Post-Adjusted Trial Balance Sheet Format

A

Post-Adjusted Trial Balance Sheet Format document displays the final balances of all ledger accounts after adjusting entries have been recorded and posted. It ensures that debits and credits remain balanced, providing an accurate snapshot of a company's financial position before preparing financial statements. Accountants rely on this format to verify correctness and completeness in the adjusted financial data.

Multi-Section Trial Balance Document Format

The

Multi-Section Trial Balance Document Format is a structured financial report that categorizes account balances into multiple sections for detailed analysis. This format enhances clarity by separating assets, liabilities, equity, revenue, and expenses into distinct segments. It aids accountants and auditors in efficiently verifying the accuracy and completeness of ledger balances during the financial closing process.

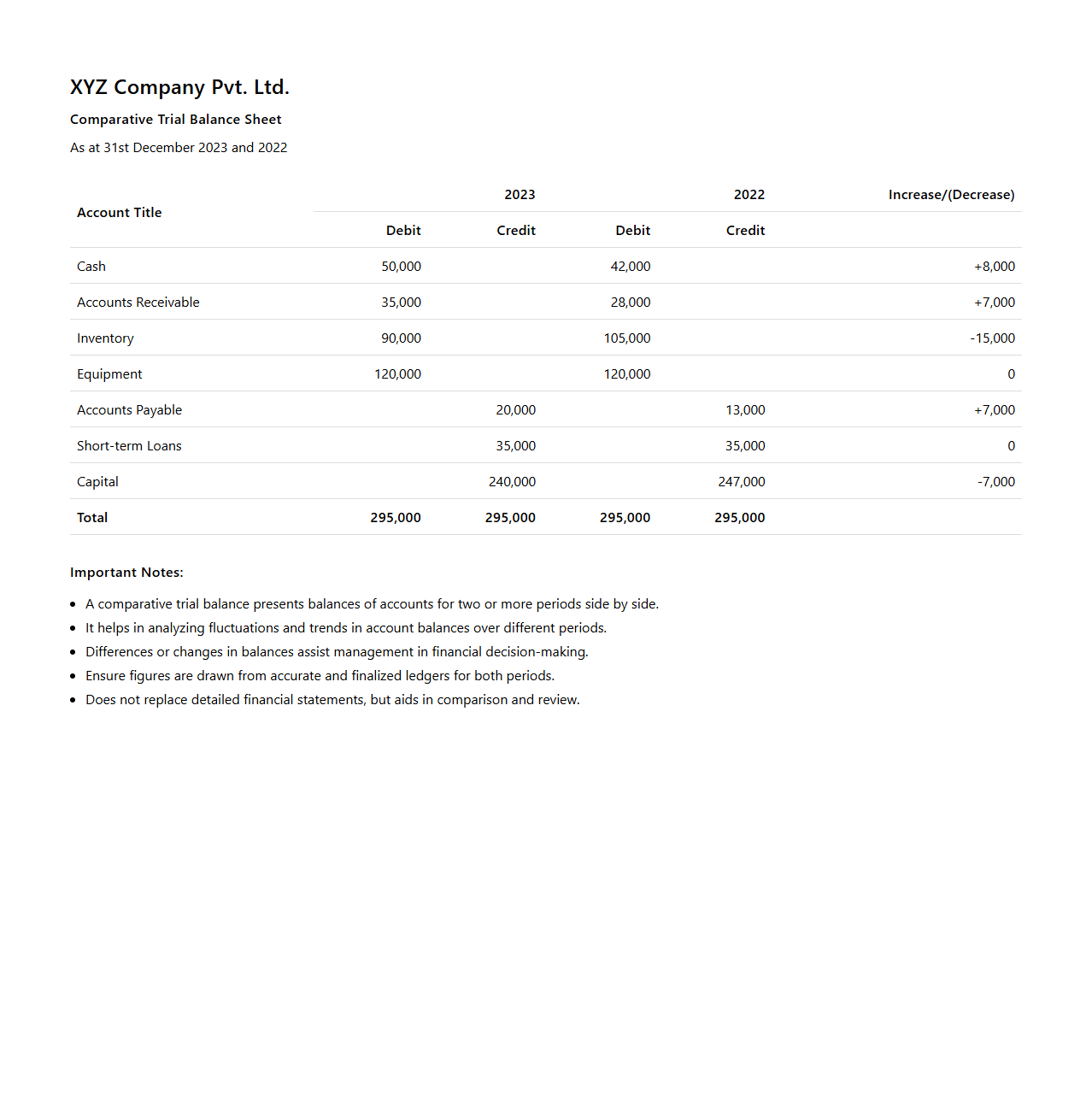

Comparative Trial Balance Sheet Format

A

Comparative Trial Balance Sheet Format document systematically displays financial data from multiple accounting periods side by side, facilitating easy comparison of account balances across different dates. This format helps identify trends, discrepancies, and changes in assets, liabilities, and equity over time. By presenting period-over-period financial information clearly, it enhances accuracy in financial analysis and decision-making.

What is the standard column arrangement in a trial balance extracted from the ledger?

The standard column arrangement in a trial balance includes columns for account names, debit balances, and credit balances. Typically, the debit and credit columns are placed side by side for easy comparison. This arrangement helps ensure that total debits equal total credits, confirming the ledger's accuracy.

How should opening and closing balances be represented in a trial balance format?

Opening balances are usually presented as the initial figures at the start of the accounting period. Closing balances reflect the final account status after all transactions are recorded. Both should be clearly distinguished, often with labels indicating opening and closing balances for transparency.

Which specific ledger accounts are mandatory to include in a trial balance document?

All ledger accounts with balances must be included, such as assets, liabilities, equity, revenue, and expenses. Omitting any ledger account can lead to inaccuracies in the trial balance. Therefore, it is mandatory to list every active account to maintain integrity.

What is the correct sequence for listing ledger accounts in the trial balance?

The correct sequence follows the accounting equation: assets first, followed by liabilities, equity, revenue, and expenses. This logical order helps users quickly understand the financial position. Maintaining a consistent sequence improves the readability of the trial balance.

How is the trial balance format affected by adjustments for errors or omissions in the ledger?

Adjustments for errors or omissions require updating the affected accounts in the trial balance. This often necessitates adding an adjustment column or revised balances to reflect corrections. Properly documenting these changes ensures the trial balance remains accurate and reliable.