The Format of Tax Residency Certificate for Non-residents typically includes the applicant's name, country of residence, and tax identification number. It must also state the period of residency and certify that the individual is a tax resident in the issuing country. This certificate is essential for claiming tax treaty benefits and avoiding double taxation.

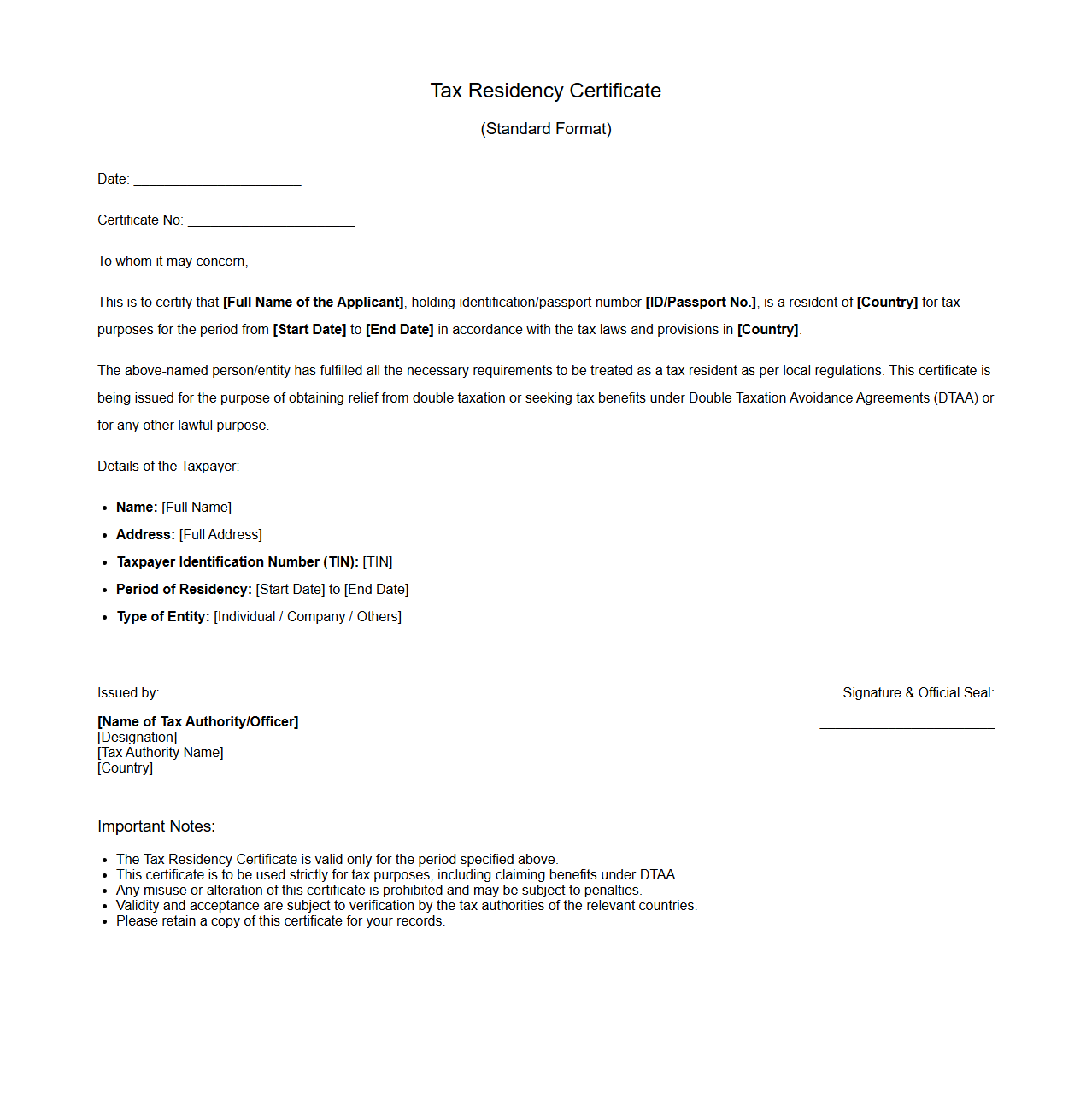

Standard Tax Residency Certificate Format

A

Standard Tax Residency Certificate Format is an official document issued by tax authorities confirming an individual's or entity's residency status for tax purposes. This certificate is essential for claiming benefits under double taxation avoidance agreements (DTAA), ensuring that taxes paid in one country are recognized in another. It typically includes details such as the taxpayer's name, identification number, period of residency, and certifying authority's signature.

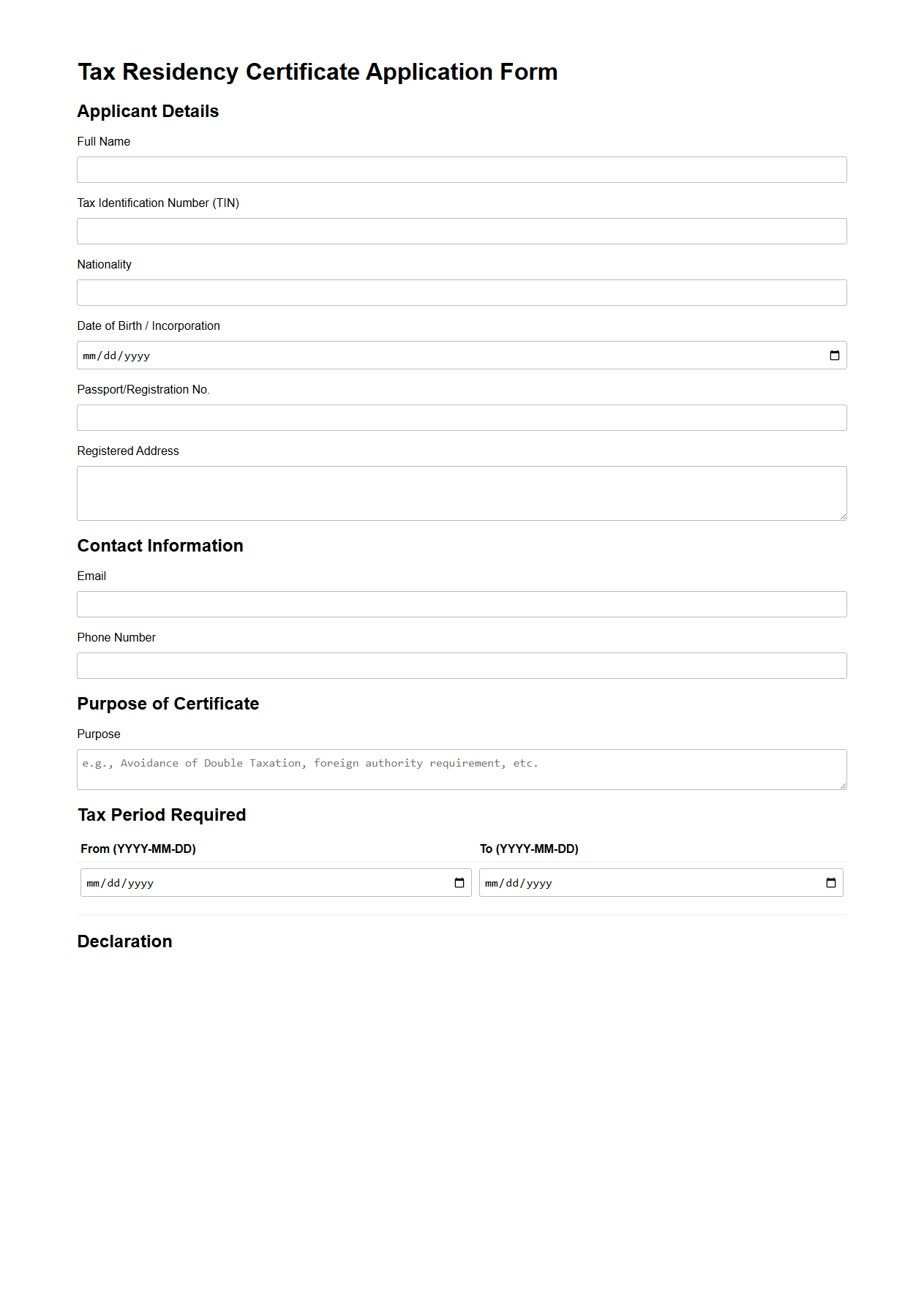

Tax Residency Certificate Application Form

The

Tax Residency Certificate Application Form is an official document submitted to tax authorities to certify an individual or entity's tax residency status in a specific country. This certificate is essential for claiming tax treaty benefits and avoiding double taxation on income earned in foreign jurisdictions. Accurate completion of the form requires details such as taxpayer identification, country of residence, and periods of stay, ensuring compliance with local tax regulations.

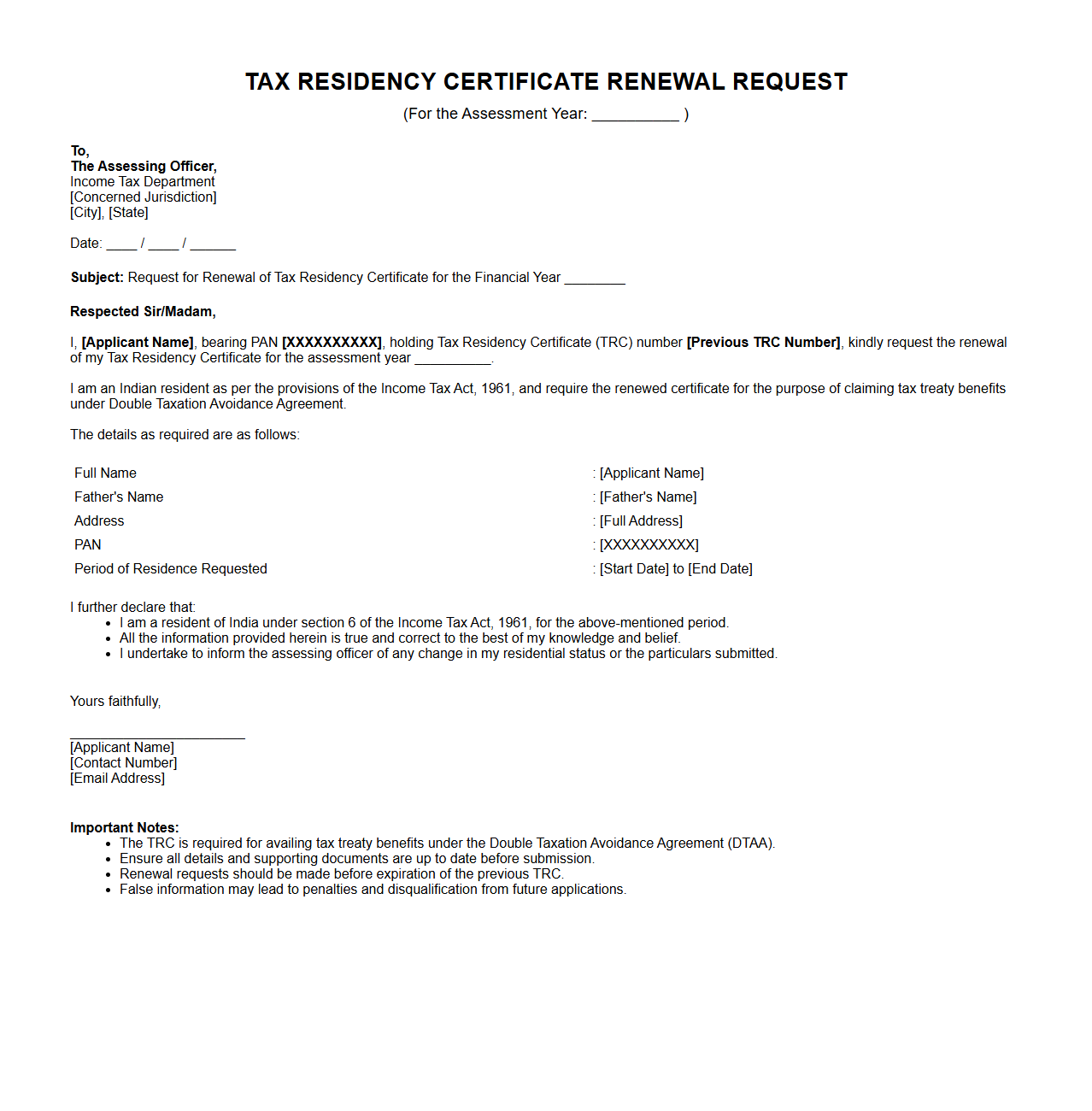

Tax Residency Certificate Renewal Format

A

Tax Residency Certificate Renewal Format document is a formal template used to apply for the extension of an existing tax residency certificate issued by tax authorities. This document requires specific details such as the applicant's personal information, previous certificate details, and proof of continued residency status to validate eligibility. It ensures compliance with tax regulations and facilitates seamless cross-border taxation processes.

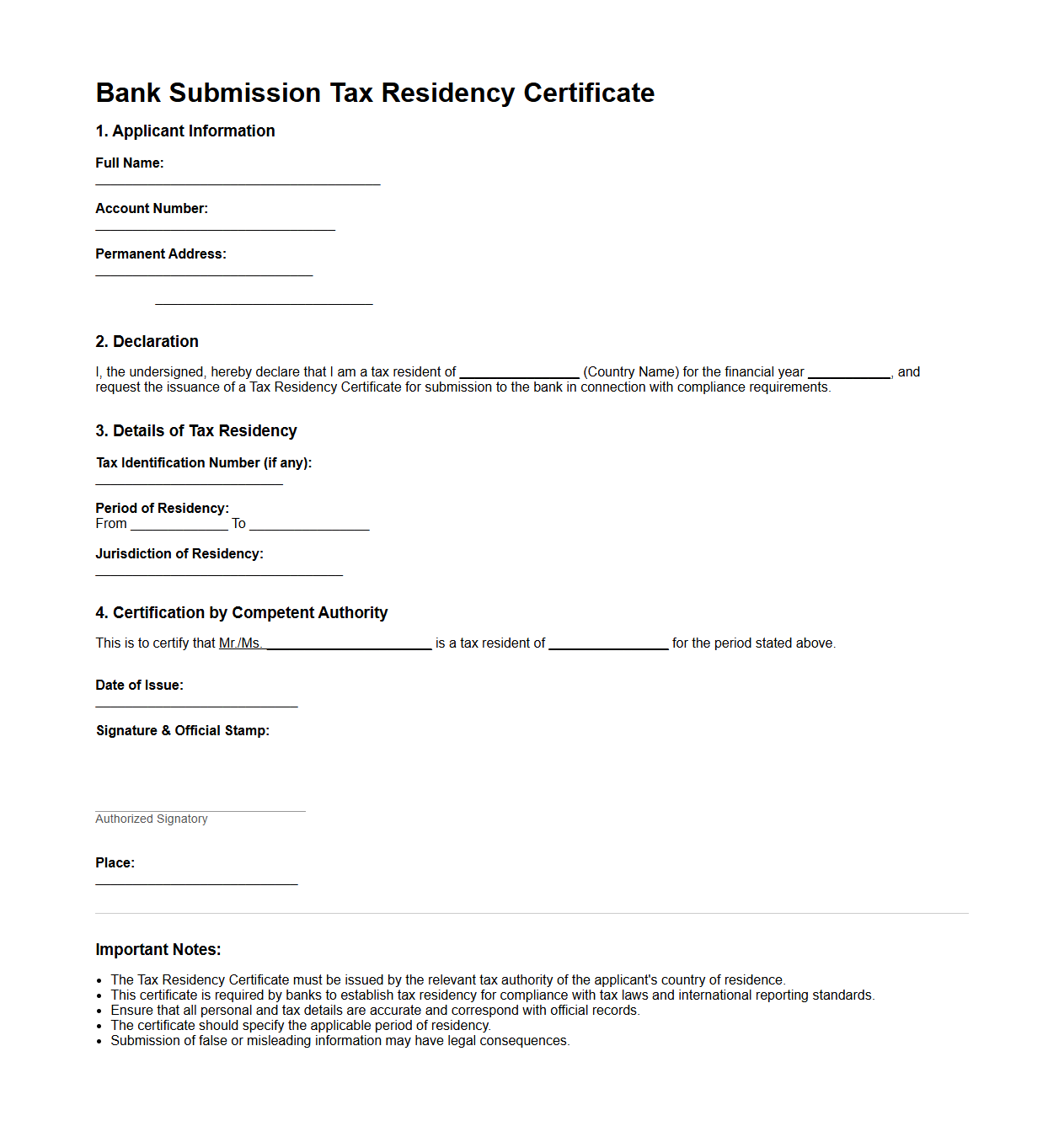

Bank Submission Tax Residency Certificate Format

The

Bank Submission Tax Residency Certificate Format is an official document required by banks to verify an individual's or entity's tax residency status for compliance with international tax regulations. This certificate typically includes essential details such as the taxpayer's name, country of residence, tax identification number, and confirmation from the relevant tax authority. Banks use this format to ensure proper withholding tax rates and to avoid double taxation under applicable tax treaties.

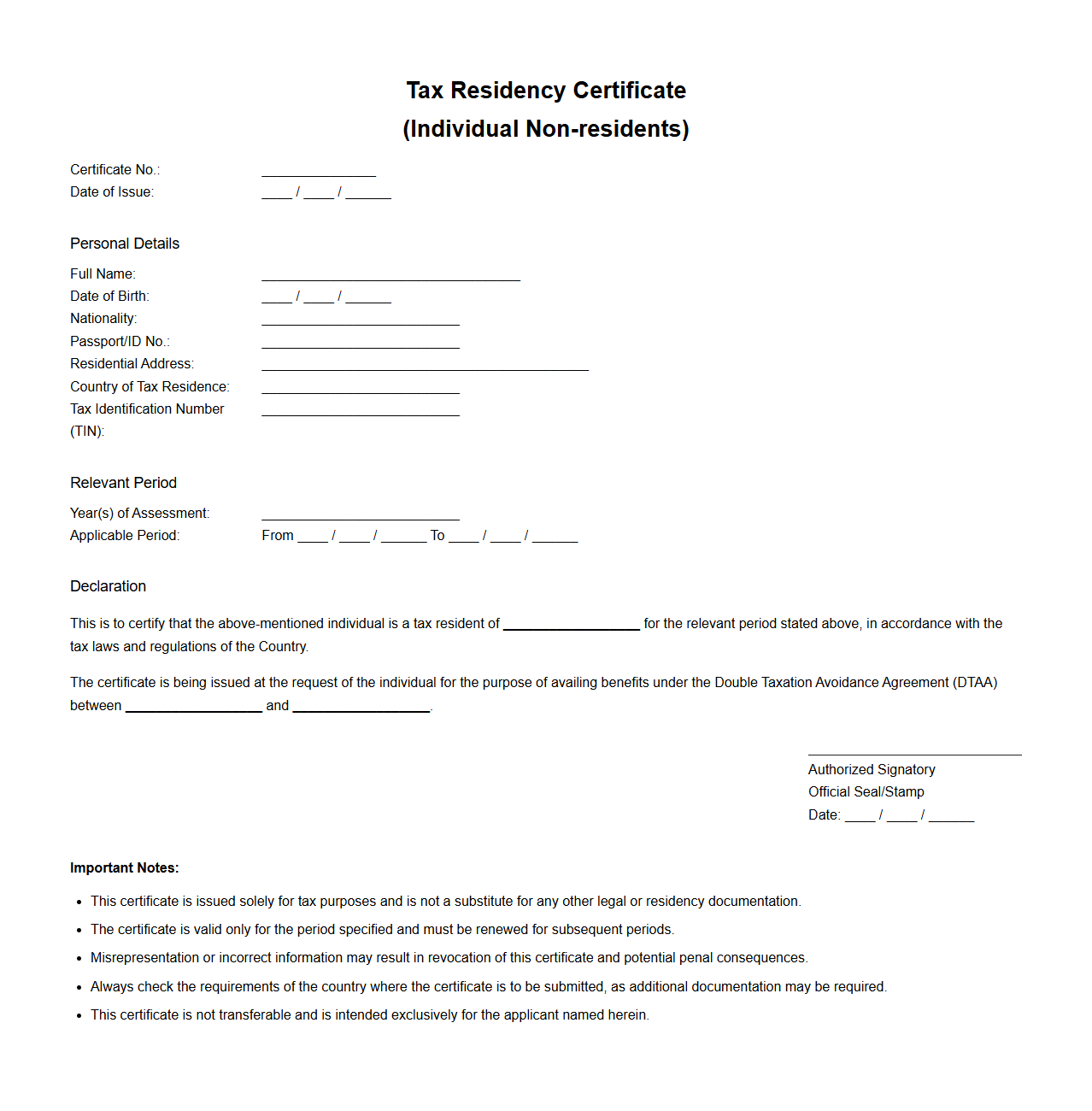

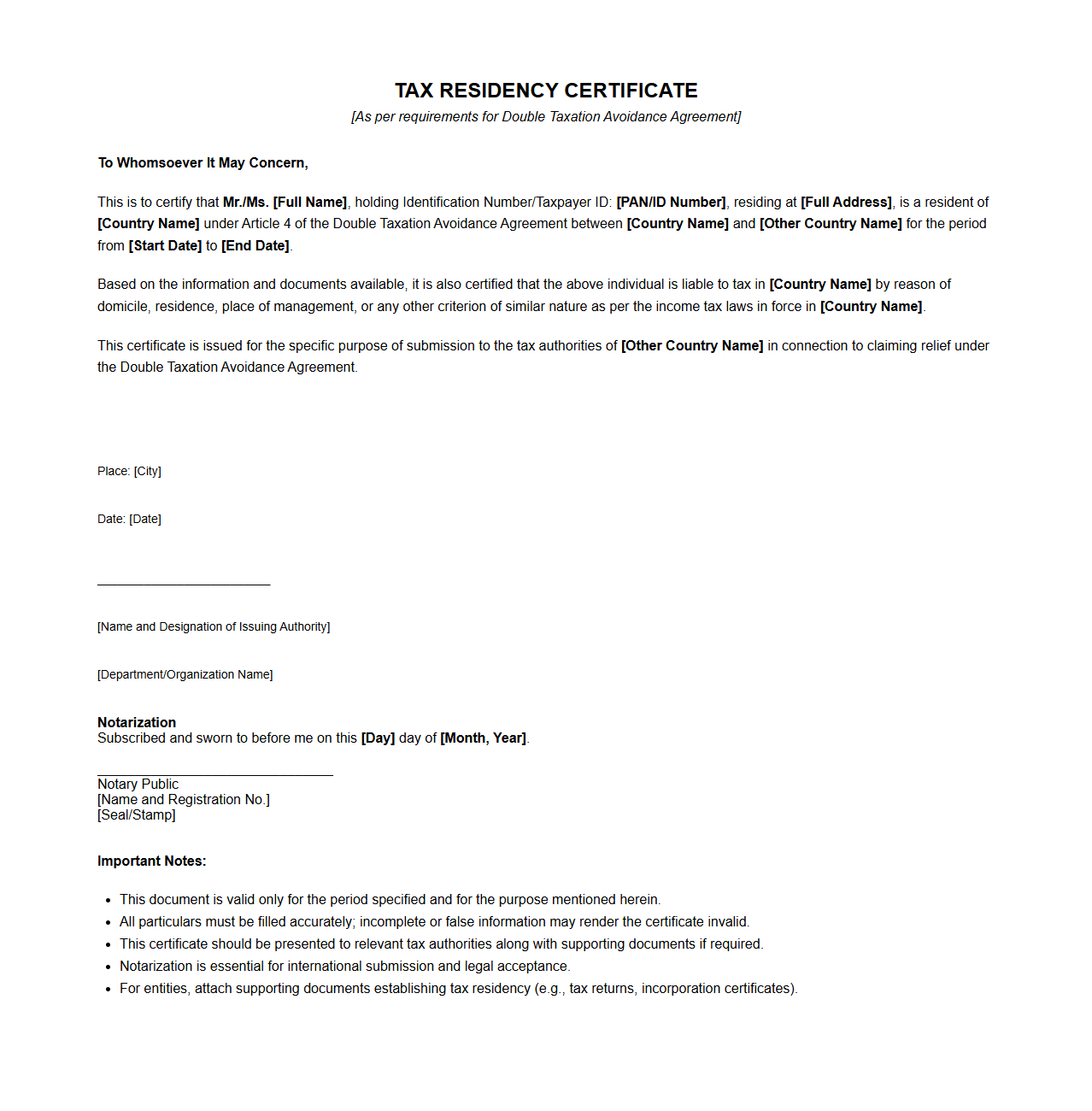

Tax Residency Certificate for Individual Non-residents Format

A

Tax Residency Certificate for Individual Non-residents is an official document issued by the tax authority to certify the individual's country of residence for tax purposes. This certificate helps prevent double taxation by confirming the taxpayer's residency status under relevant tax treaties. The format typically includes personal details, tax identification numbers, period of residence, and certification date, ensuring compliance with international tax regulations.

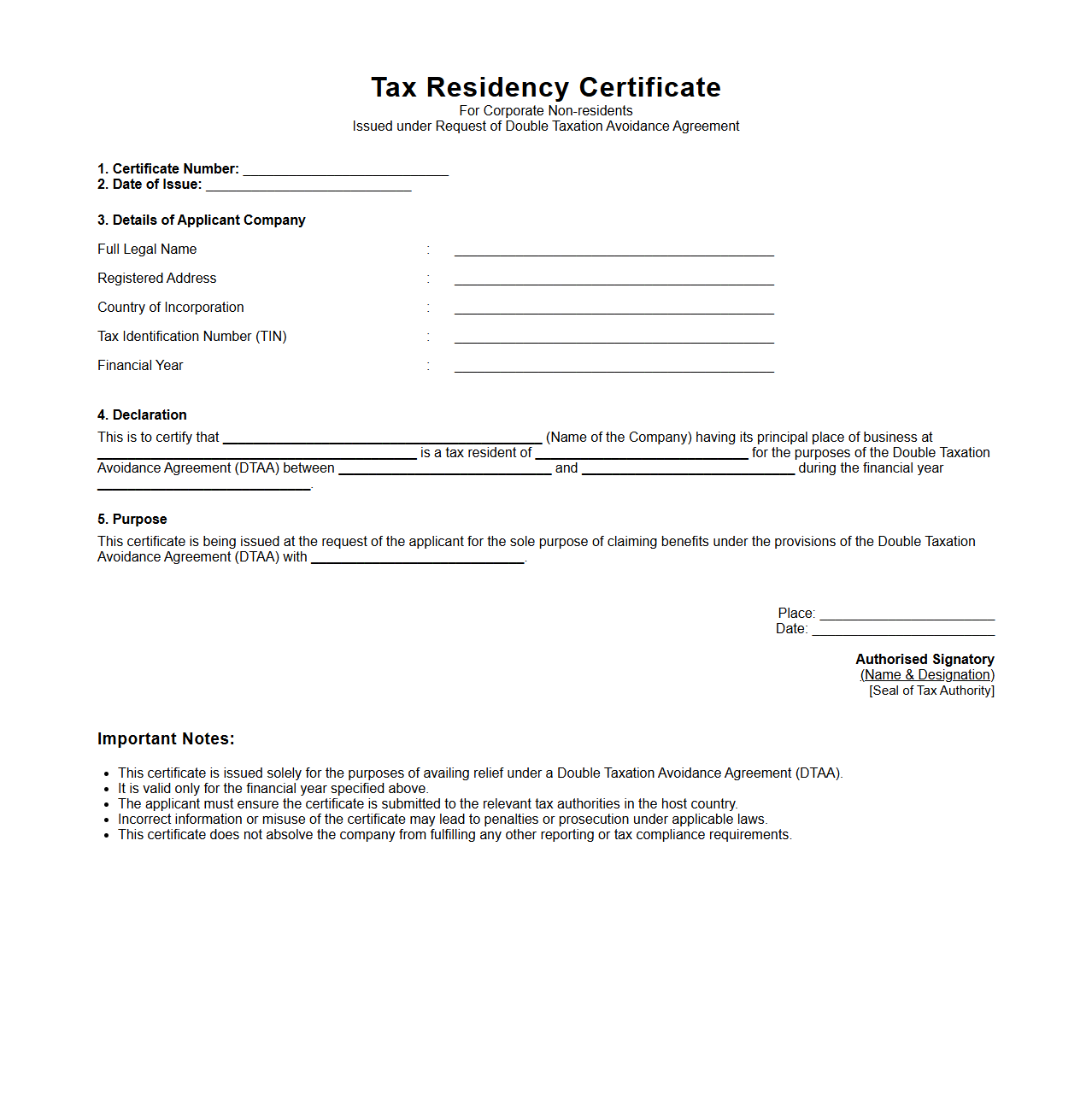

Tax Residency Certificate for Corporate Non-residents Format

A

Tax Residency Certificate (TRC) for Corporate Non-residents is an official document issued by a country's tax authority certifying that a company is a resident for tax purposes. This certificate helps prevent double taxation under bilateral tax treaties by proving the company's tax residency status. The format document typically includes the company's name, tax identification number, period of residency, and relevant treaty details.

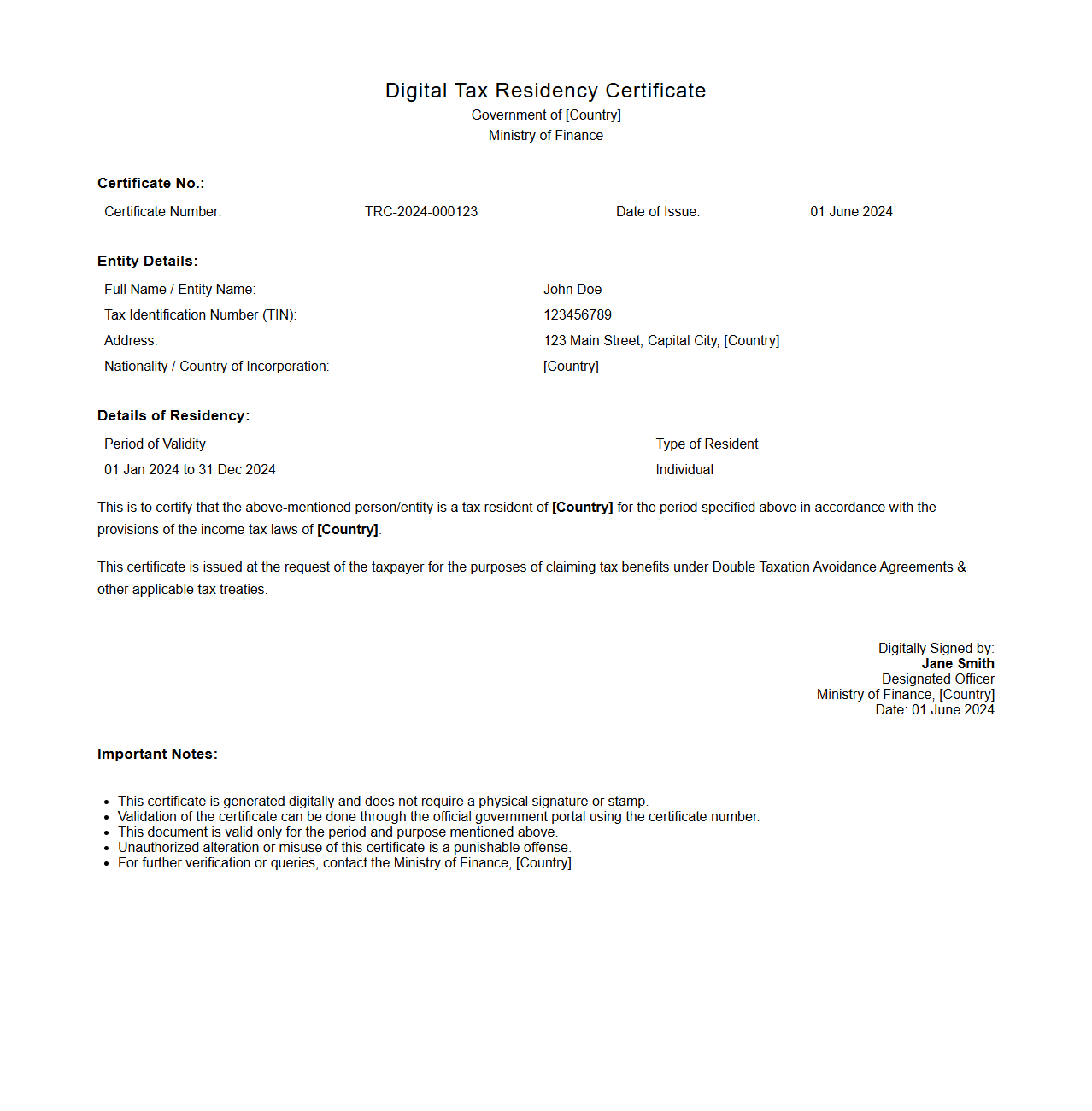

Digital Tax Residency Certificate Format

A

Digital Tax Residency Certificate Format document is an official electronic certificate issued by tax authorities to confirm an individual's or entity's tax residency status in a specific country. This format is standardized to include key information such as the taxpayer's identification details, residency period, and certification date, ensuring authenticity and compliance with international tax treaties. It facilitates seamless tax treaty benefits, eliminates double taxation, and streamlines cross-border financial transactions.

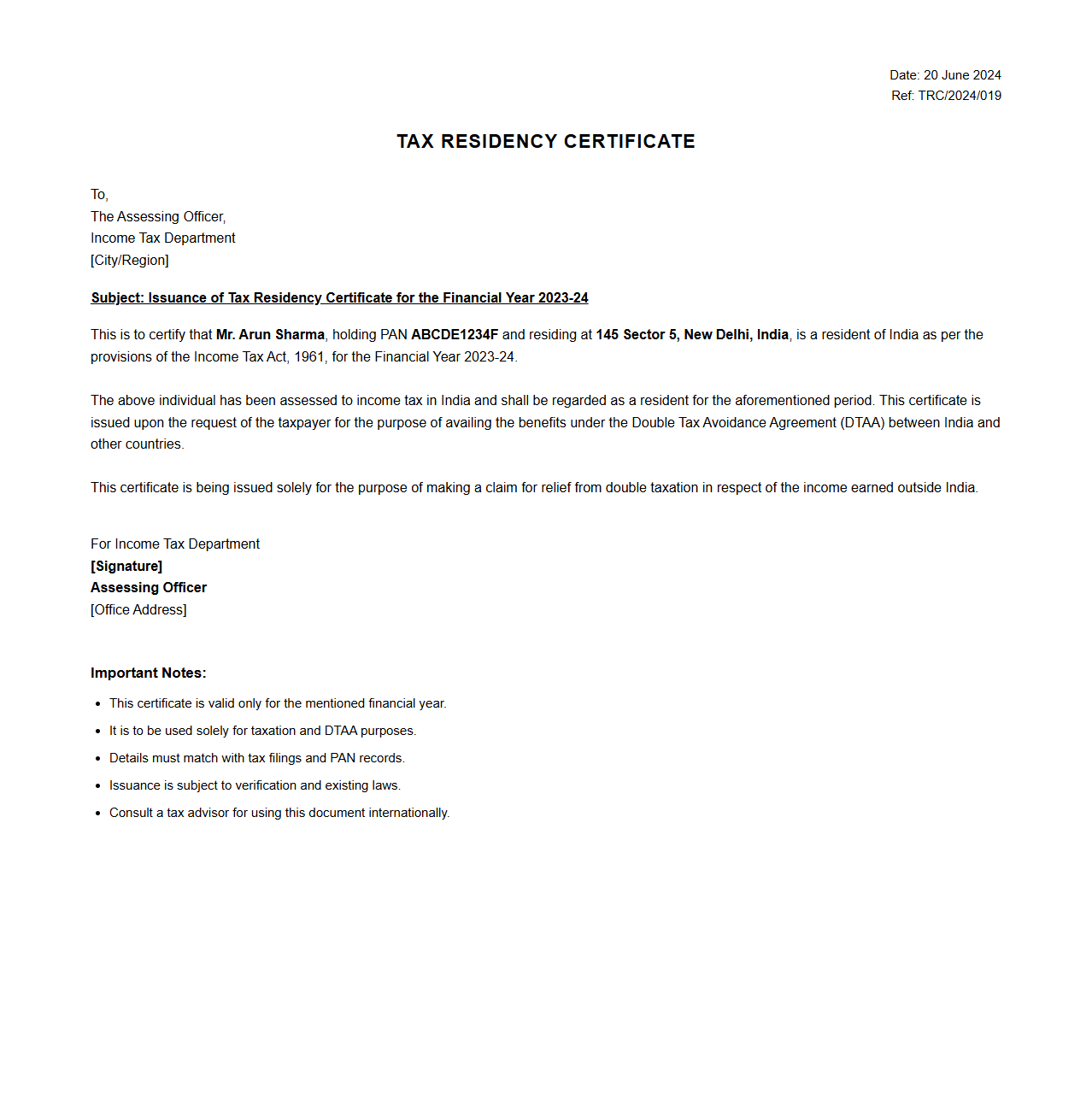

Tax Residency Certificate Format for Double Taxation Avoidance Agreement

A

Tax Residency Certificate (TRC) format is a standardized document issued by tax authorities to verify an individual or entity's tax residency status for a specific period, essential in applying for benefits under a Double Taxation Avoidance Agreement (DTAA). This certificate typically includes details such as the taxpayer's name, country of residence, tax identification number, and validity period, helping to prevent the taxpayer from being taxed twice on the same income in two different jurisdictions. The TRC format ensures compliance with the DTAA provisions, facilitating smooth tax administration and avoiding fiscal duplicity between countries.

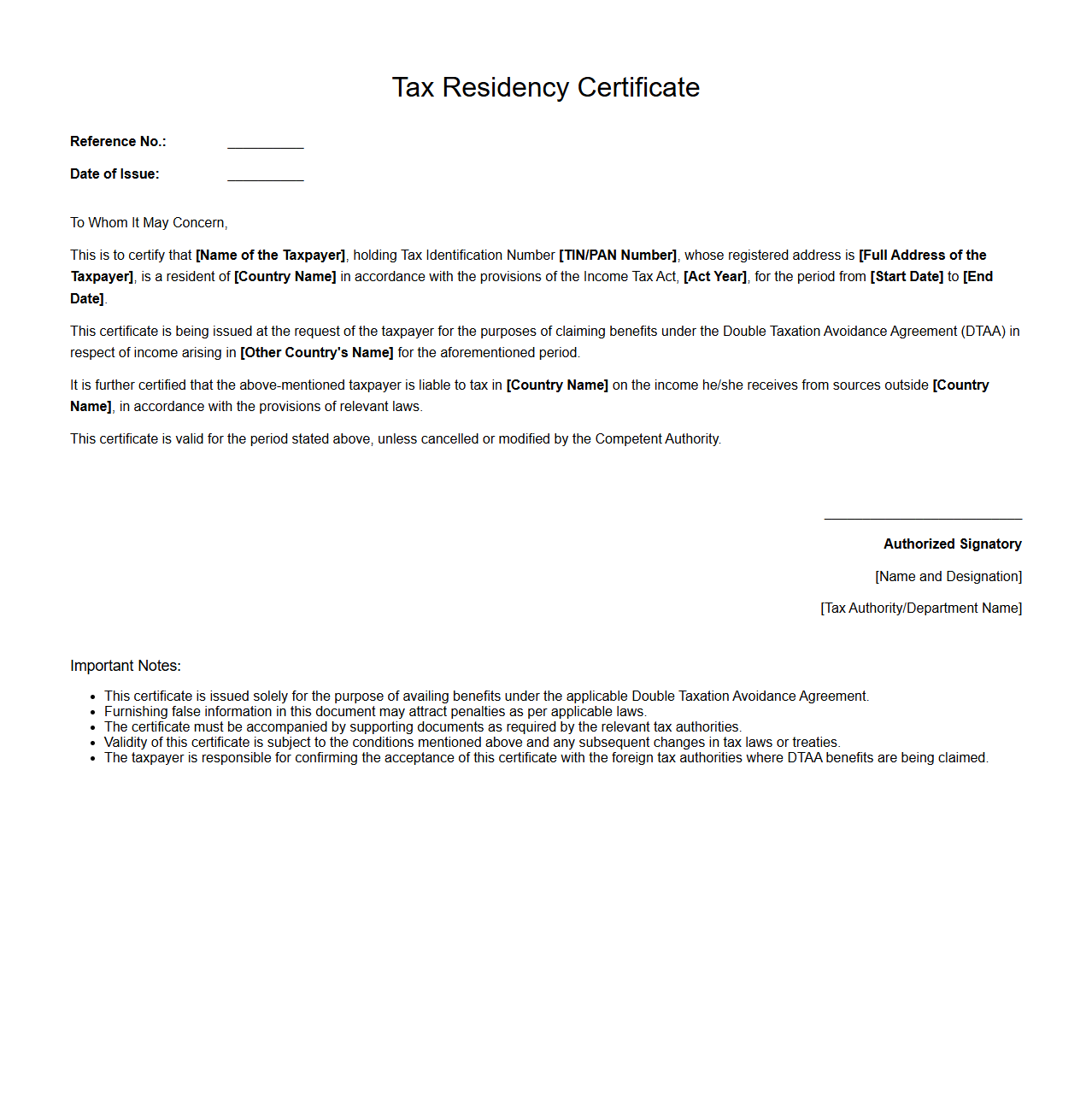

Tax Residency Certificate Sample Letter Format

A

Tax Residency Certificate Sample Letter Format is a template used to request or provide proof of an individual's or entity's tax residency status from tax authorities. It typically includes essential details such as the applicant's full name, tax identification number, period of residency, and a formal declaration stating the holder's tax residency in a specific jurisdiction. This document is crucial for avoiding double taxation and facilitating compliance with international tax treaties.

Notarized Tax Residency Certificate Format

A

Notarized Tax Residency Certificate Format document serves as an official proof verifying an individual's or entity's tax residency status in a specific country, certified by a notary public to ensure the document's authenticity. This format includes essential details such as the taxpayer's name, tax identification number, the period of residency, and confirmation that the person or entity is subject to tax laws in the issuing jurisdiction. It is commonly required for international tax compliance, treaty benefits, and avoiding double taxation between countries.

What specific information must a Tax Residency Certificate for non-residents include according to OECD guidelines?

A Tax Residency Certificate must clearly state the individual's or entity's residential status according to the tax laws of the issuing country. It should include the taxpayer's identifying details, such as name, taxpayer identification number, and fiscal year of residence. Additionally, the certificate must confirm the residency status for tax purposes, enabling relief under applicable Double Taxation Avoidance Agreements.

Which authority is authorized to issue a valid Tax Residency Certificate in a non-resident's home country?

The competent tax authority of the taxpayer's home country is authorized to issue a valid Tax Residency Certificate. This is typically the national or regional tax department responsible for income tax matters. Valid issuance ensures that the certificate is recognized for cross-border tax treaty benefits.

What is the ideal format for a digital Tax Residency Certificate accepted for cross-border tax treaties?

An ideal digital Tax Residency Certificate should be presented in a secure, tamper-proof PDF format incorporating a digital signature or official seal for authenticity. It must contain all key information plainly structured and easy to verify electronically. Adhering to international standards ensures acceptance in cross-border tax treaty scenarios.

Are notarization or apostille requirements mandatory for Tax Residency Certificate submission?

Usually, notarization or apostille is not mandatory for submitting a Tax Residency Certificate, especially if issued by a recognized tax authority. The digital signature or official certification by the tax authority typically suffices. However, specific jurisdictional requirements may apply based on the treaty partner's regulations.

How should the certificate reference applicable Double Taxation Avoidance Agreements (DTAAs) in its format?

The certificate should explicitly mention the Double Taxation Avoidance Agreement (DTAA) under which the residency status is certified. This includes referencing the relevant country pair and treaty date or article for clarity. Proper reference ensures smooth application of treaty benefits and reduces withholding tax disputes.