The Format of Capitalization Policy Document for an organization typically includes clear definitions of capital assets, criteria for capitalization thresholds, and guidelines for asset classification. It outlines procedures for asset acquisition, depreciation methods, and documentation requirements to ensure consistent financial reporting. This structured format helps maintain transparency and compliance with accounting standards.

Executive Summary of Capitalization Policy Document

The Executive Summary of a

Capitalization Policy Document provides a concise overview of the policy's key guidelines on asset capitalization thresholds, criteria for capitalizing expenditures, and procedures for recording and reporting capital assets. It highlights the purpose of establishing consistent practices to ensure accurate financial reporting and compliance with accounting standards such as GAAP or IFRS. This summary serves as a quick reference for stakeholders to understand the scope, objectives, and impact of the capitalization policy on the organization's financial management.

Purpose Statement for Capitalization Policy

A

Purpose Statement for a Capitalization Policy document defines the objectives and scope, clarifying how an organization identifies, classifies, and accounts for capital assets. It establishes the criteria for capitalizing expenditures to ensure consistent financial reporting and compliance with accounting standards. This statement guides employees in applying the policy effectively, supporting accurate asset management and financial transparency.

Scope and Applicability Section in Capitalization Policy

The

Scope and Applicability Section in a Capitalization Policy document defines the boundaries and determines which assets, transactions, or departments the policy covers. It clarifies the financial thresholds, asset categories, and organizational units subject to the capitalization rules. This section ensures consistent application of capitalization principles across the company, enabling accurate financial reporting and compliance.

Definitions and Terminology Segment for Capitalization

The

Definitions and Terminology Segment in a Capitalization document serves as a crucial reference section that clarifies specific terms and phrases used throughout the document. It ensures consistency and accuracy by providing precise meanings for technical jargon, accounting principles, and capitalization rules. This segment helps stakeholders understand the scope and application of capitalization policies without ambiguity.

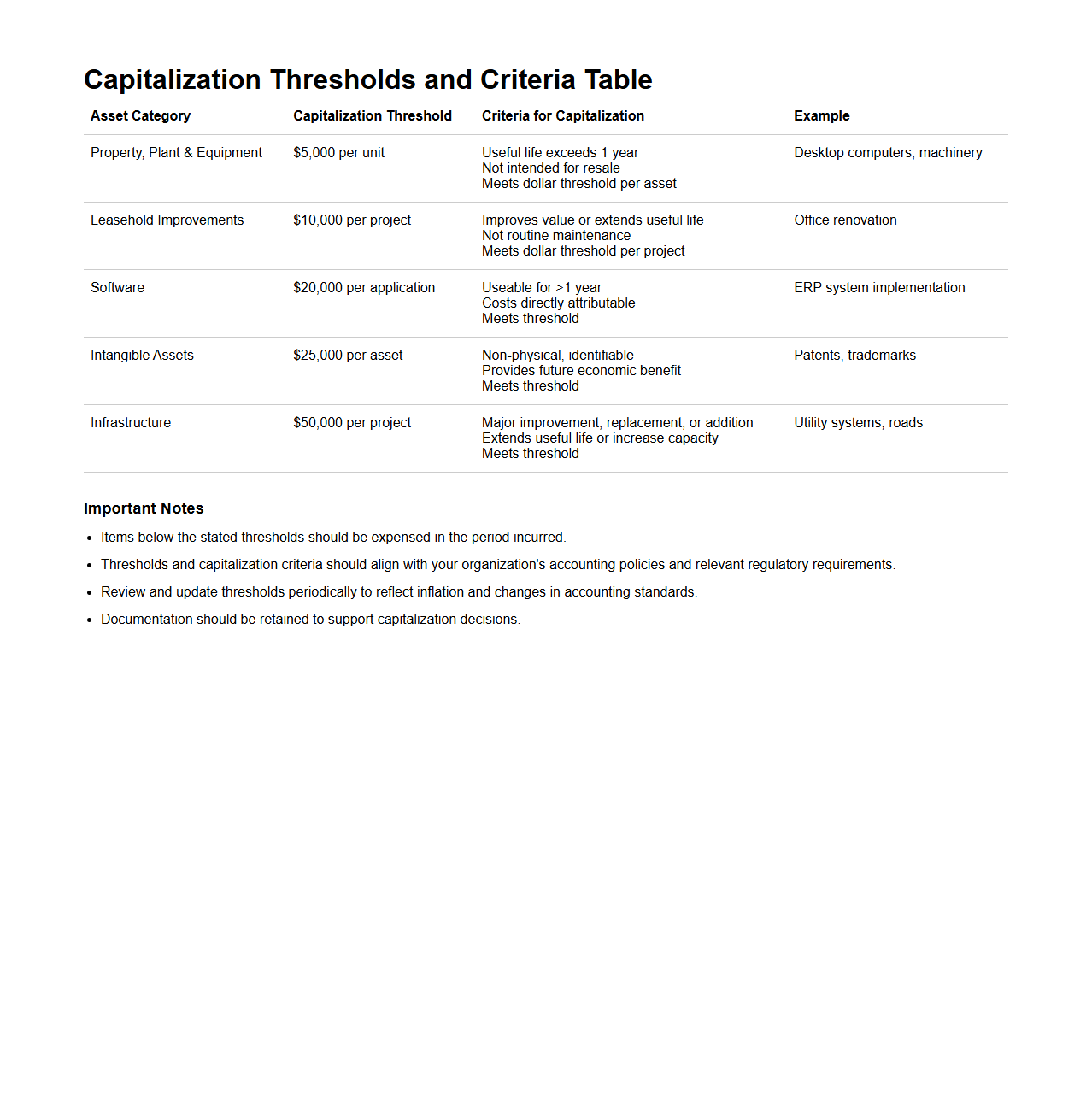

Capitalization Thresholds and Criteria Table

The

Capitalization Thresholds and Criteria Table document outlines specific financial limits and conditions a company uses to determine whether expenditures should be capitalized or expensed. It standardizes how assets are recorded on the balance sheet, ensuring consistent accounting treatment across departments and projects. This document is essential for compliance with accounting standards and aids in accurate financial reporting and asset management.

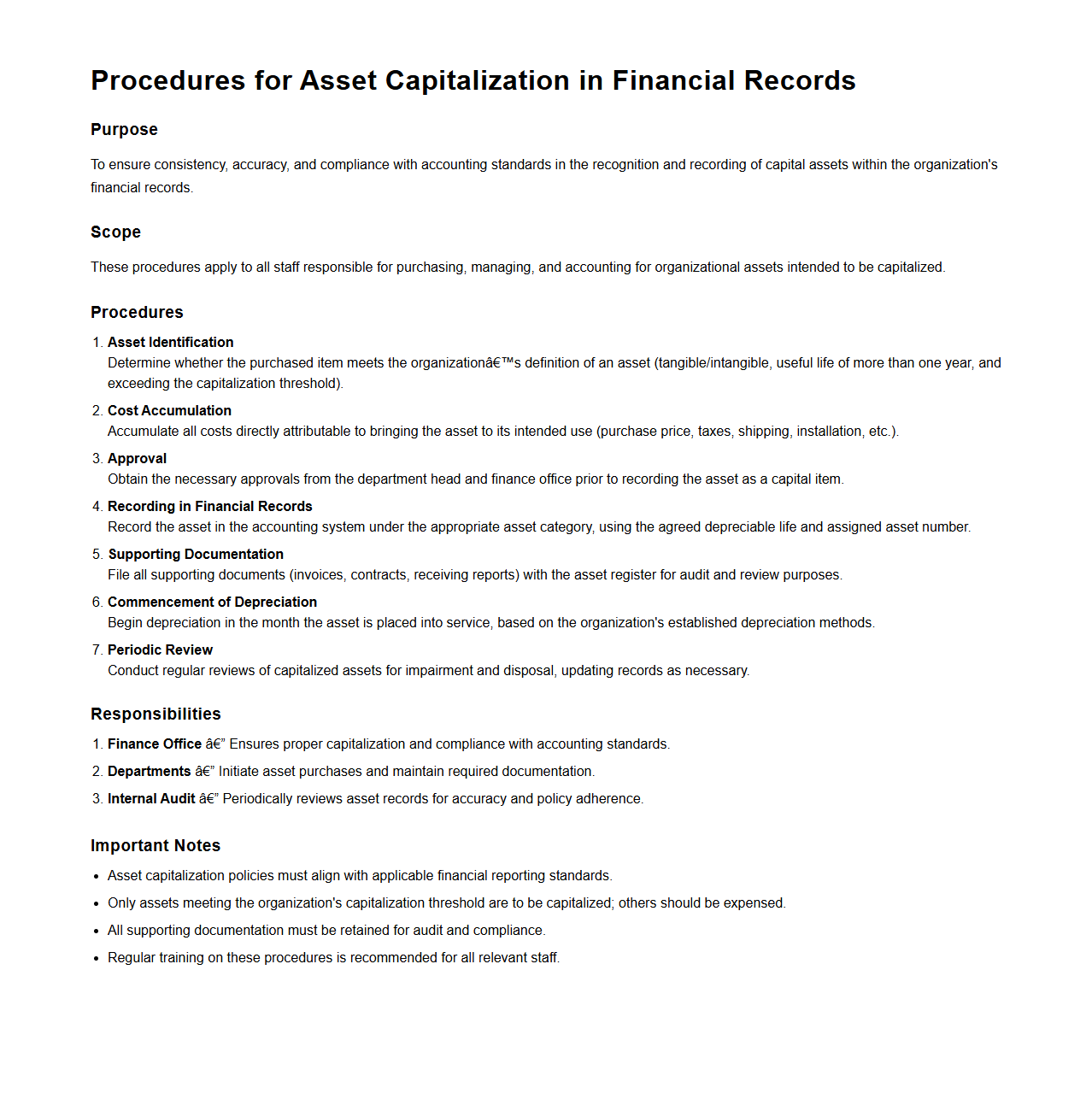

Procedures for Asset Capitalization in Financial Records

The

Procedures for Asset Capitalization in Financial Records document outlines systematic guidelines for identifying, classifying, and recording fixed assets to ensure accurate financial reporting and compliance with accounting standards. It specifies criteria such as asset cost thresholds, useful life estimations, and depreciation methods to determine which expenditures qualify as capital assets rather than expenses. This document supports consistent asset management, facilitates audit readiness, and enhances transparency in financial statements.

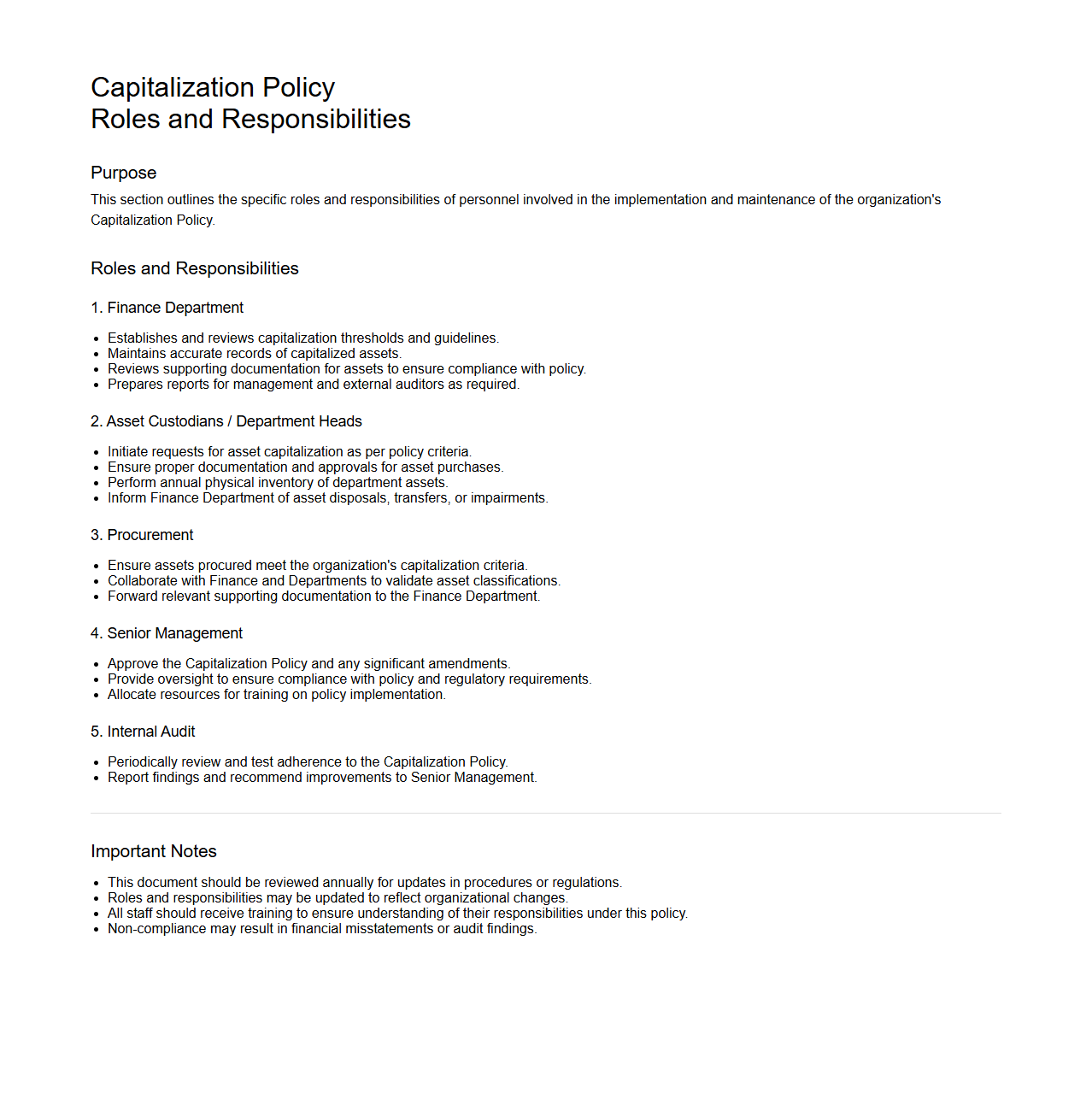

Roles and Responsibilities in Capitalization Policy

Roles and Responsibilities in a

Capitalization Policy document define the specific duties and accountability for individuals and departments involved in identifying, recording, and managing capital assets. This section clarifies who authorizes asset capitalization, ensures compliance with accounting standards, and maintains accurate asset tracking throughout its lifecycle. Clear delineation of these roles helps streamline processes, reduce errors, and support accurate financial reporting.

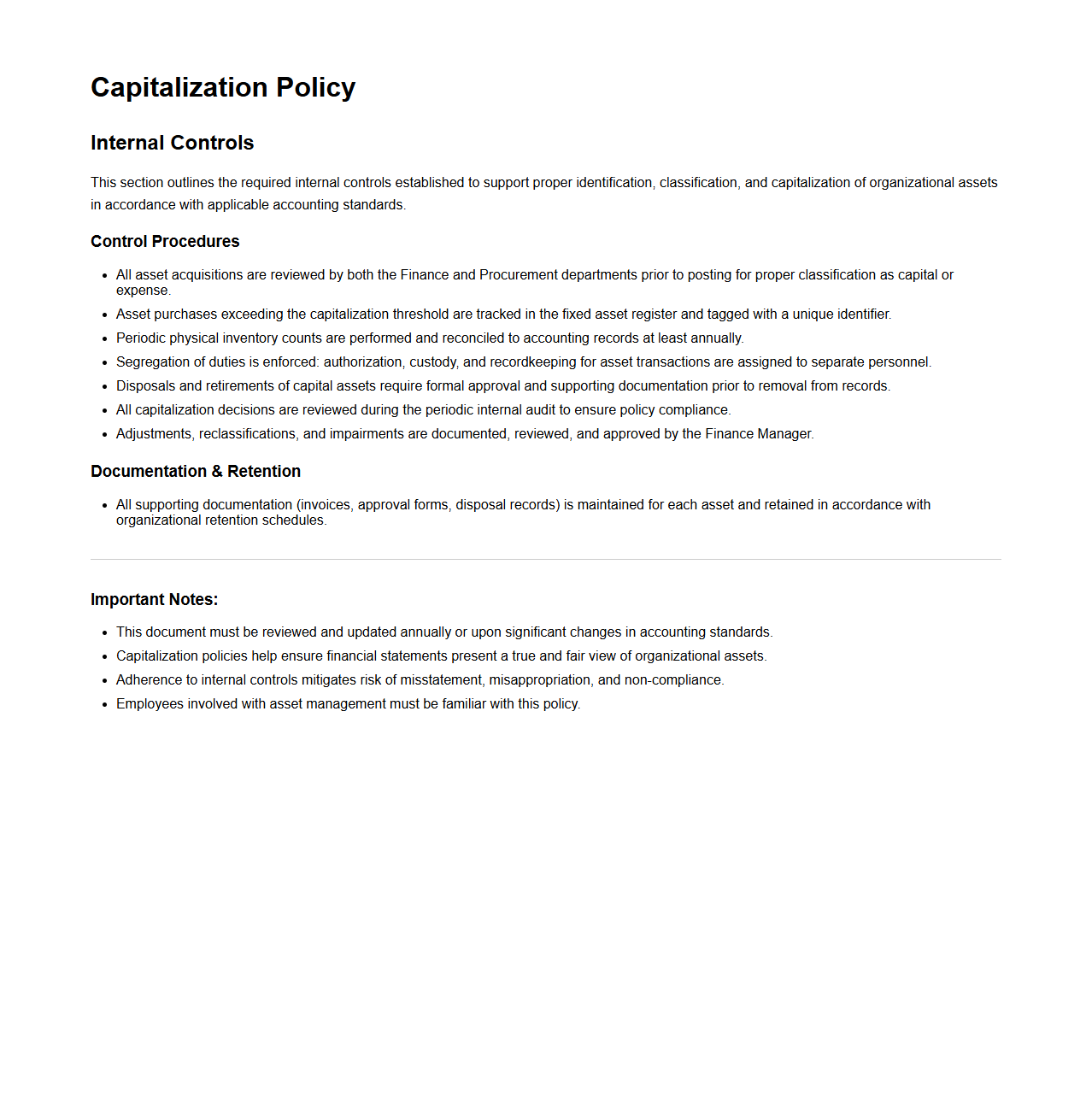

Capitalization Policy Internal Controls Section

The

Capitalization Policy Internal Controls Section document outlines the procedures and criteria for determining which assets should be capitalized versus expensed, ensuring consistent financial reporting and compliance with accounting standards. It includes guidelines on asset recognition, threshold limits, and periodic review processes to maintain accuracy in asset tracking and depreciation. This document is essential for safeguarding company assets and supporting audit readiness through established internal controls.

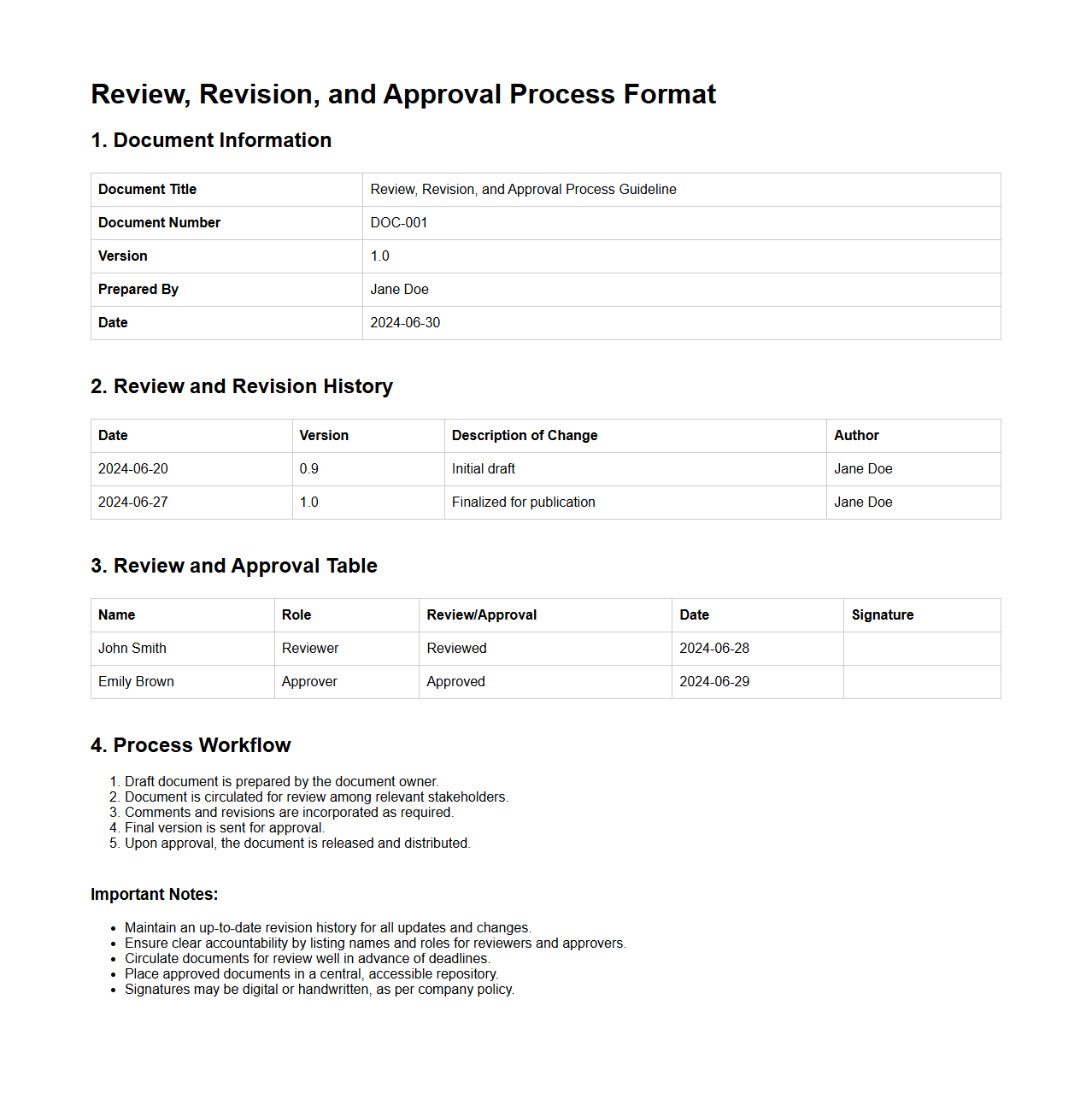

Review, Revision, and Approval Process Format

The

Review, Revision, and Approval Process Format document outlines a structured approach to evaluating, modifying, and authorizing important documents or projects to ensure quality and compliance. It specifies the roles and responsibilities of stakeholders involved in reviewing content, making necessary revisions, and granting final approval before implementation. This format enhances transparency, accountability, and traceability throughout the entire document lifecycle.

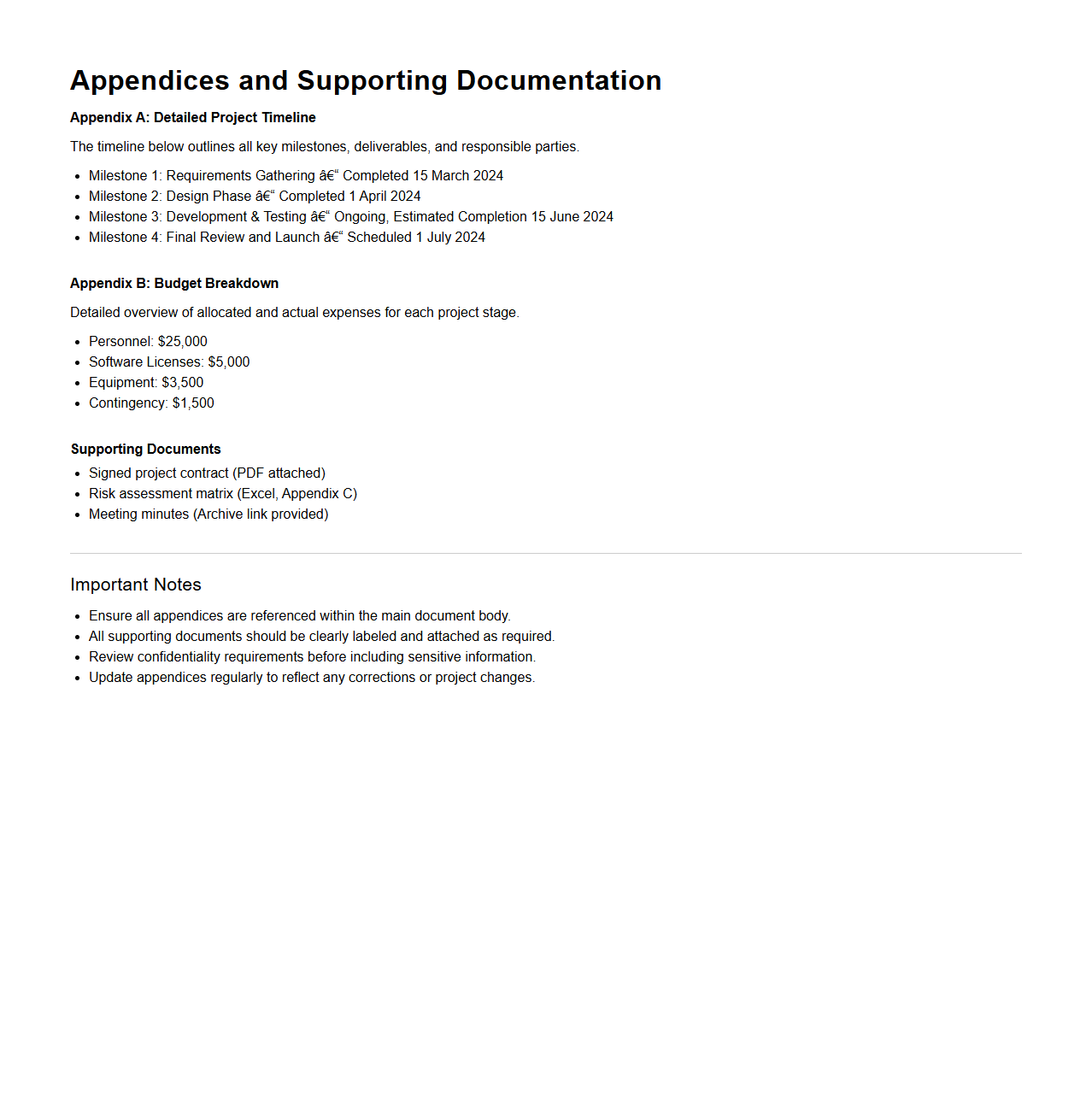

Appendices and Supporting Documentation Section

The

Appendices and Supporting Documentation Section of a document contains supplementary materials that provide essential background, detailed data, or additional explanations referenced in the main text. This section often includes charts, raw data, technical specifications, questionnaires, or legal documents that enhance the reader's understanding without interrupting the flow of the primary content. Properly organized appendices ensure transparency and allow verification of the information presented.

What financial threshold determines capitalization of assets in the organization's policy?

The organization's policy sets a financial threshold to determine which assets qualify for capitalization. Assets with a cost exceeding this threshold are recorded as capital assets rather than expenses. This ensures consistency in financial reporting and asset management.

Which types of purchases or expenditures are subject to capitalization under this policy?

The policy requires capitalization for purchases of tangible and intangible assets that meet the cost threshold and have a useful life extending beyond one year. Examples include equipment, buildings, and software development costs. Routine repairs and maintenance are excluded from capitalization.

What specific documentation is required to support asset capitalization decisions?

Supporting documentation must include purchase receipts, supplier invoices, and approval forms. Additionally, a detailed description of the asset and its estimated useful life is required. This documentation ensures transparency and facilitates audit compliance.

How does the policy address asset useful life and depreciation schedules?

The policy specifies estimated useful life ranges for different asset categories to standardize depreciation. Depreciation is recorded using approved methods such as straight-line or declining balance. Regular reviews are conducted to adjust useful life and depreciation as needed.

What approval processes are mandated for capitalizing assets according to the document?

Capitalization of assets requires prior approval from designated management or finance officers. Requests must be documented and reviewed to ensure compliance with the financial threshold and policy criteria. This process helps maintain control over asset recording and financial integrity.