The format of asset valuation for financial reporting typically includes the identification of assets, measurement of their fair value or historical cost, and the appropriate classification on the balance sheet. This format ensures consistency and transparency, aligning with accounting standards such as IFRS or GAAP. Proper documentation and disclosure of valuation methods enhance reliability and comparability in financial statements.

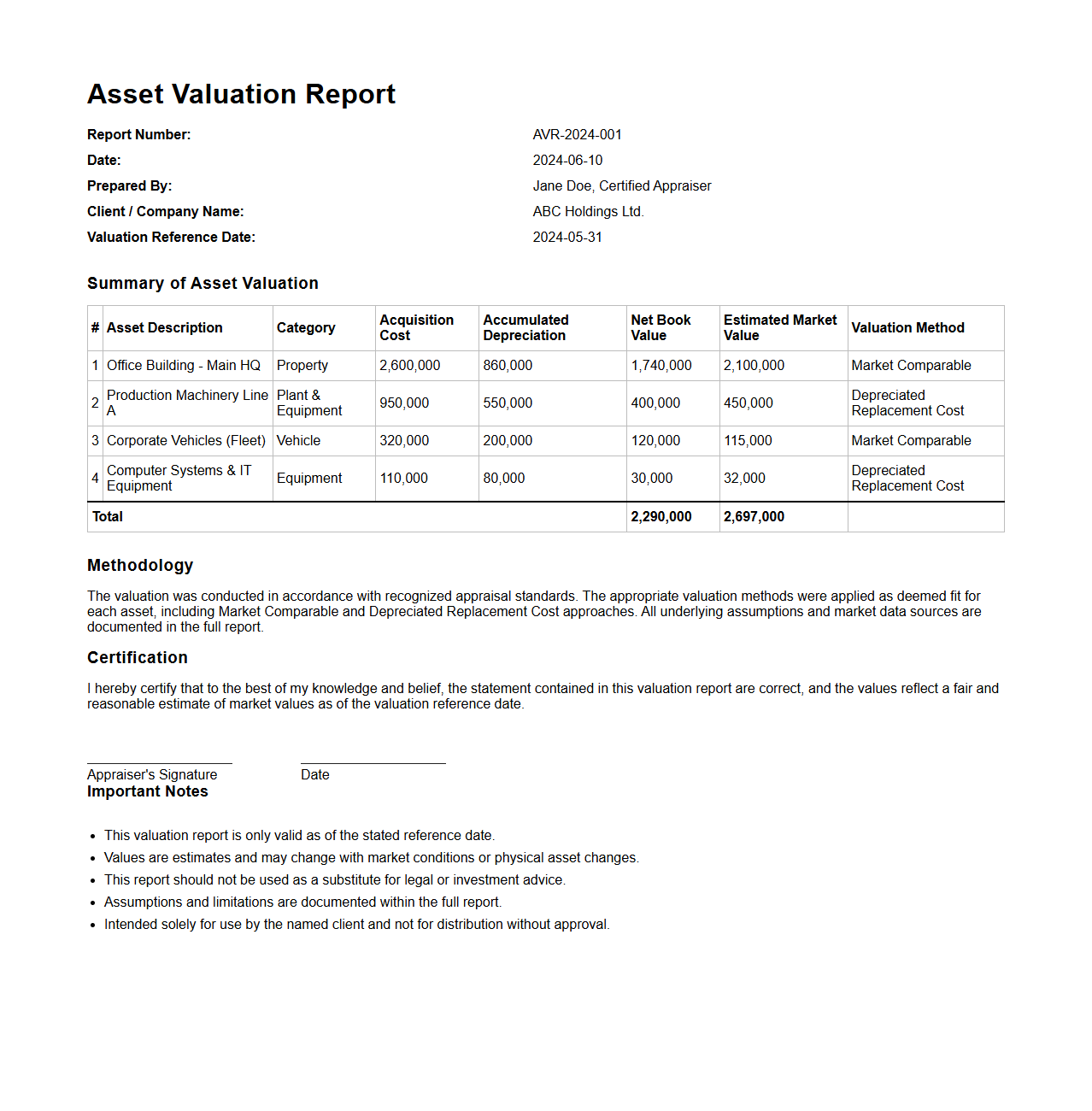

Asset Valuation Report Template – Financial Statement Format

An

Asset Valuation Report Template - Financial Statement Format document provides a structured framework for assessing and documenting the value of an organization's assets. It includes detailed sections for asset identification, valuation methods, market comparison, and depreciation calculations, ensuring accuracy and consistency in financial reporting. This template supports compliance with accounting standards and aids stakeholders in making informed financial decisions based on precise asset valuation data.

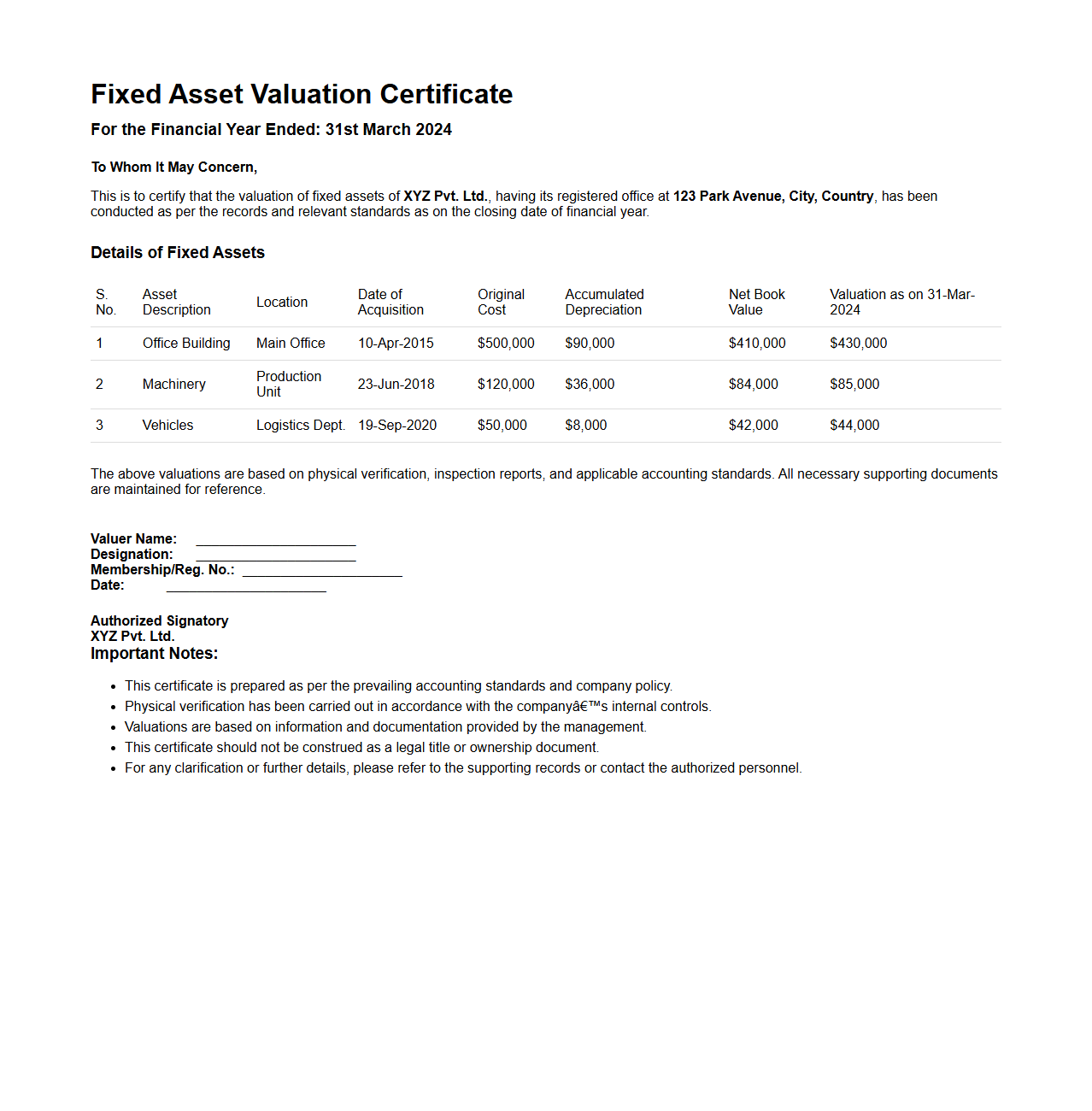

Fixed Asset Valuation Certificate Format for Annual Reporting

A

Fixed Asset Valuation Certificate Format for annual reporting is a standardized document used to verify and record the value of fixed assets owned by an organization at the end of the financial year. This certificate includes details such as asset descriptions, valuation methods, depreciation, and total asset value, ensuring accurate financial statements and compliance with accounting standards. It serves as critical evidence for auditors and stakeholders to assess the organization's capital investments and asset management.

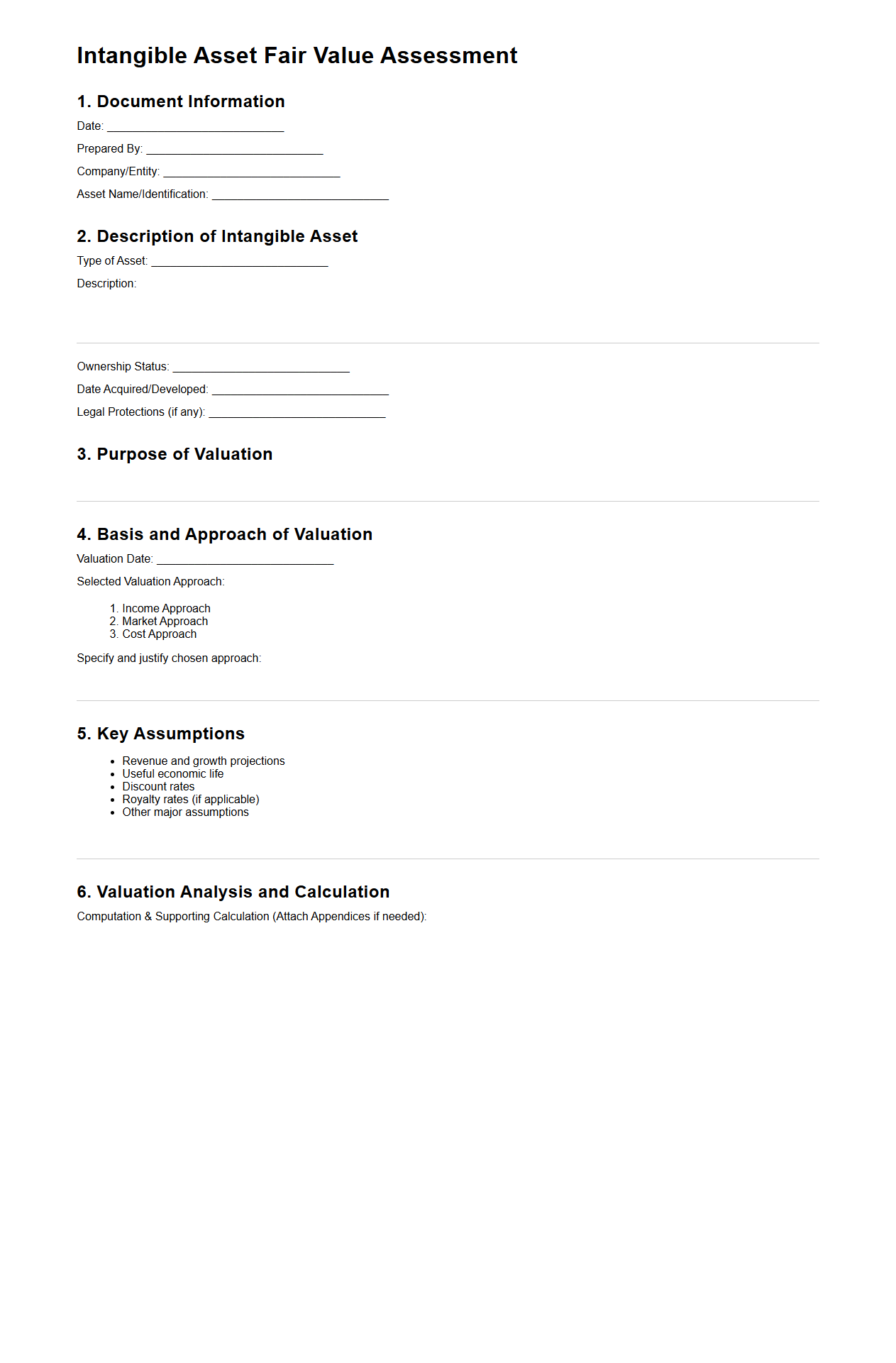

Intangible Asset Fair Value Assessment Document Format

The

Intangible Asset Fair Value Assessment Document Format is a structured template used to evaluate and report the fair value of intangible assets such as patents, trademarks, copyrights, and goodwill. This document typically includes detailed sections on asset identification, valuation methodology, market analysis, and financial projections to ensure compliance with accounting standards like IFRS or GAAP. It serves as a critical tool for auditors, accountants, and stakeholders in financial reporting, mergers, acquisitions, and investment decisions.

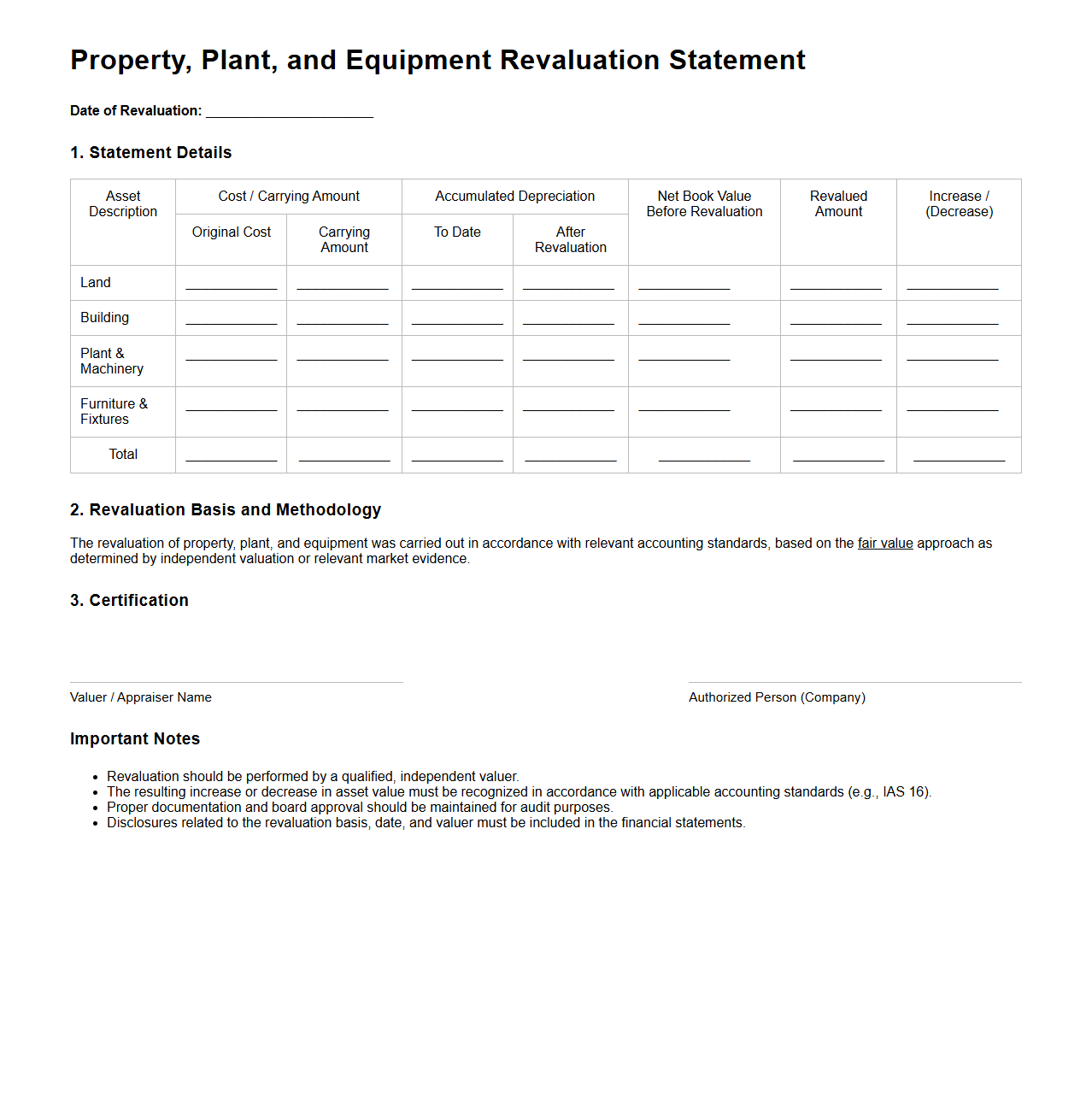

Property, Plant, and Equipment Revaluation Statement Format

The

Property, Plant, and Equipment Revaluation Statement Format document is a structured financial report used to record and present the updated values of an entity's fixed assets after revaluation. It includes details such as the asset description, original cost, accumulated depreciation, revalued amount, and the resulting revaluation surplus or deficit. This format ensures compliance with accounting standards and provides transparent information for stakeholders regarding changes in asset valuations.

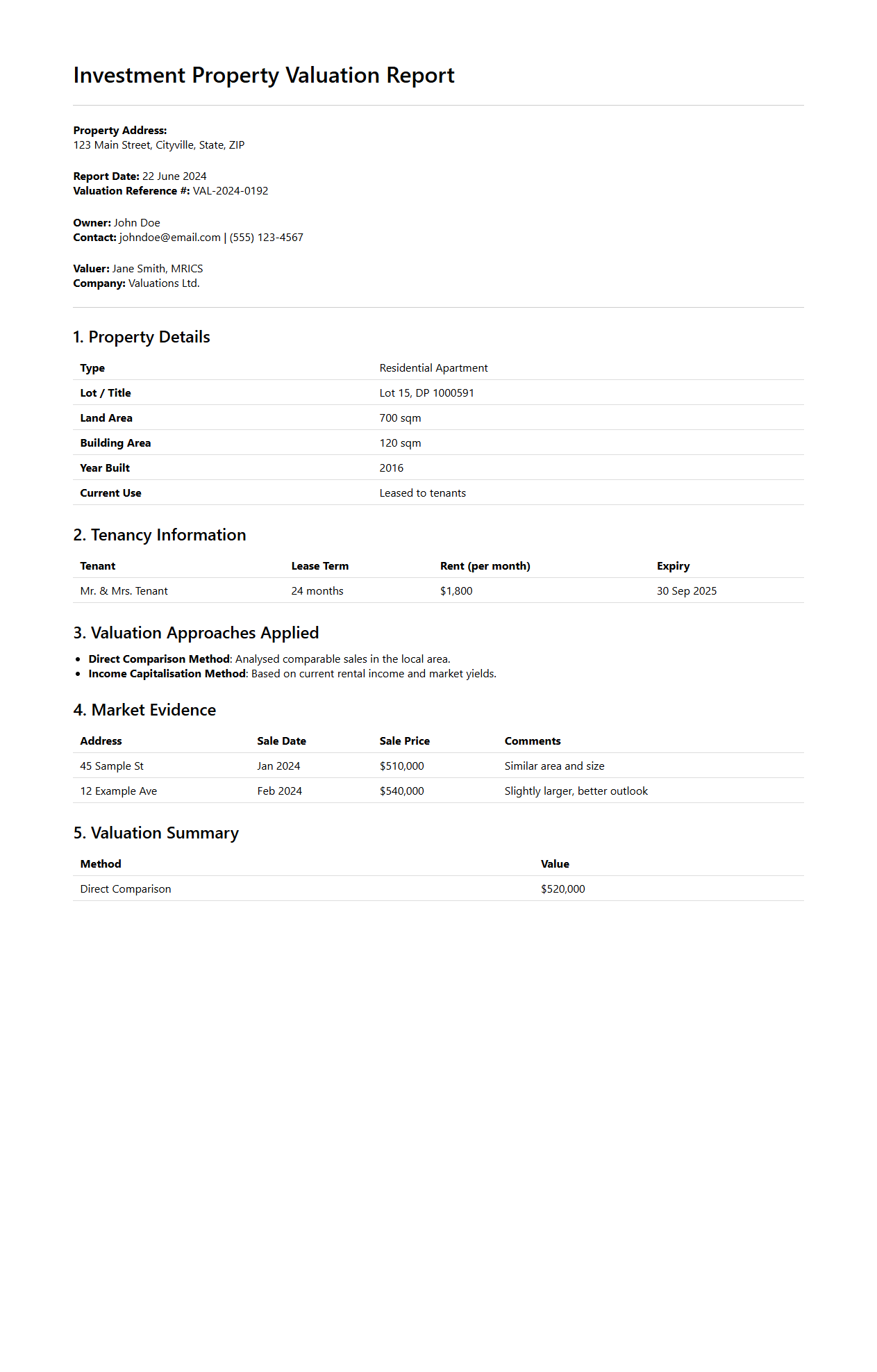

Investment Property Valuation Report Standard Format

An

Investment Property Valuation Report Standard Format document is a structured template used by real estate professionals to uniformly assess and present the market value of investment properties. It includes detailed sections on property description, financial analysis, market trends, and valuation methods to ensure consistency and transparency. This standardized format helps investors, lenders, and stakeholders make informed decisions based on reliable and comparable valuation data.

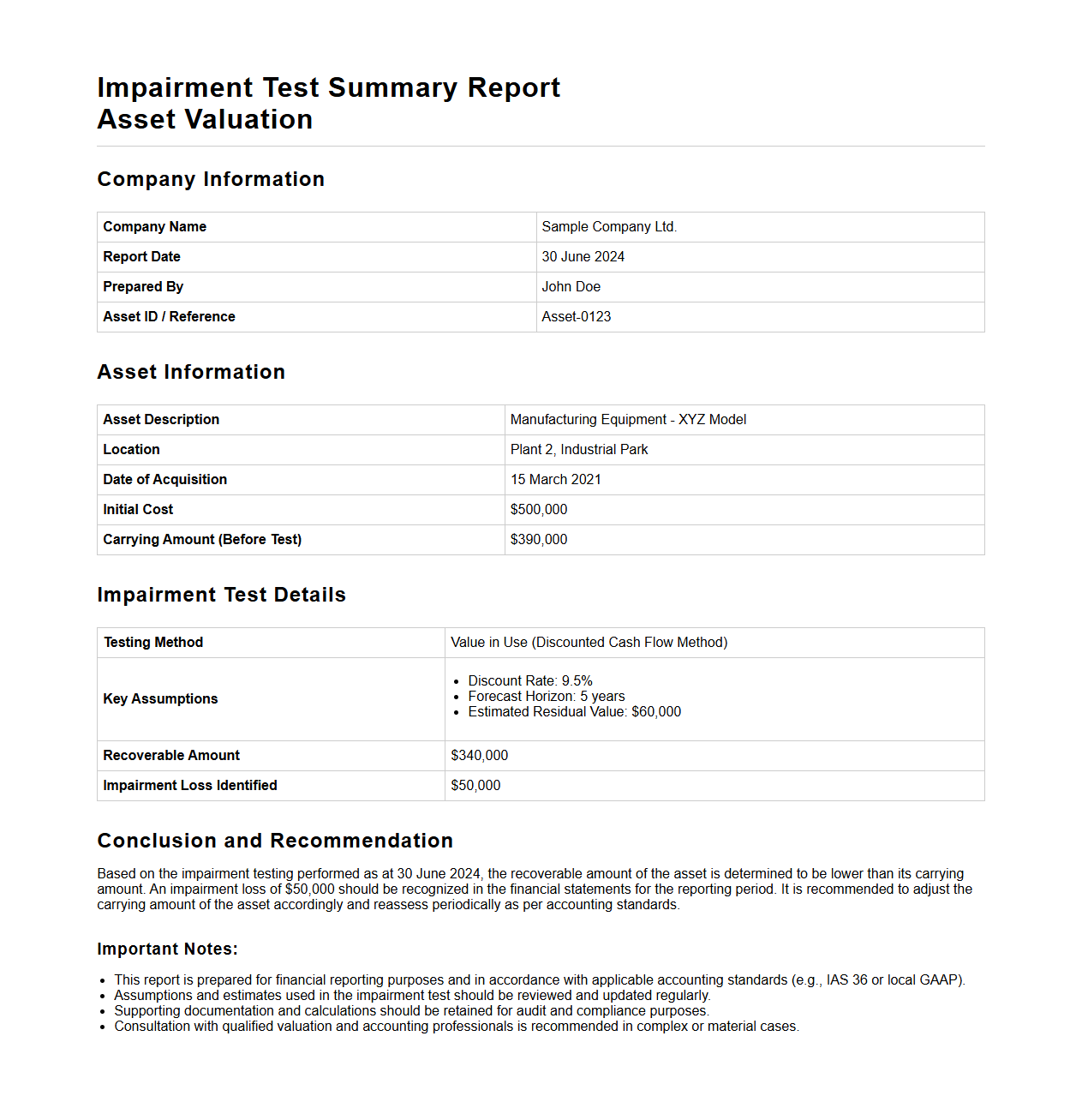

Impairment Test Summary Report Format for Asset Valuation

The

Impairment Test Summary Report Format for asset valuation is a standardized document that outlines the process and results of assessing whether an asset's carrying amount exceeds its recoverable amount. It includes key details such as asset identification, valuation methods used, assumptions applied, and calculations of recoverable amounts based on fair value or value in use. This report ensures compliance with accounting standards like IAS 36 and provides evidence for management's decision-making regarding potential asset write-downs.

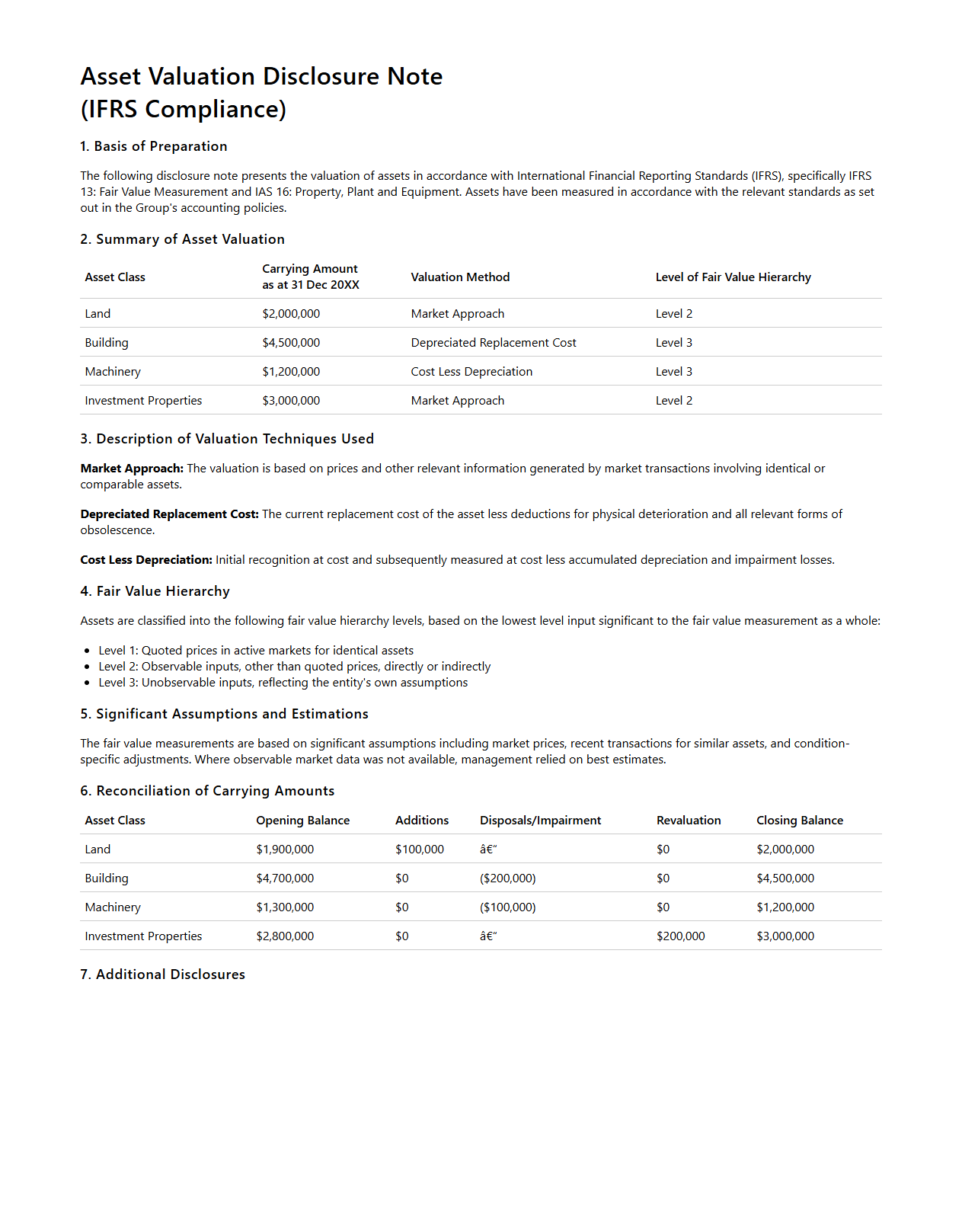

Asset Valuation Disclosure Note Format for IFRS Compliance

The

Asset Valuation Disclosure Note Format for IFRS compliance outlines the standardized presentation of asset values, including the basis of measurement, valuation techniques, and assumptions used in financial statements. This format ensures transparency and consistency, enabling stakeholders to understand how asset values were determined, whether by cost model, revaluation model, or fair value measurement. It also requires detailed disclosures on impairments, depreciation methods, and any revaluation surpluses or deficits, enhancing the credibility and comparability of financial reports.

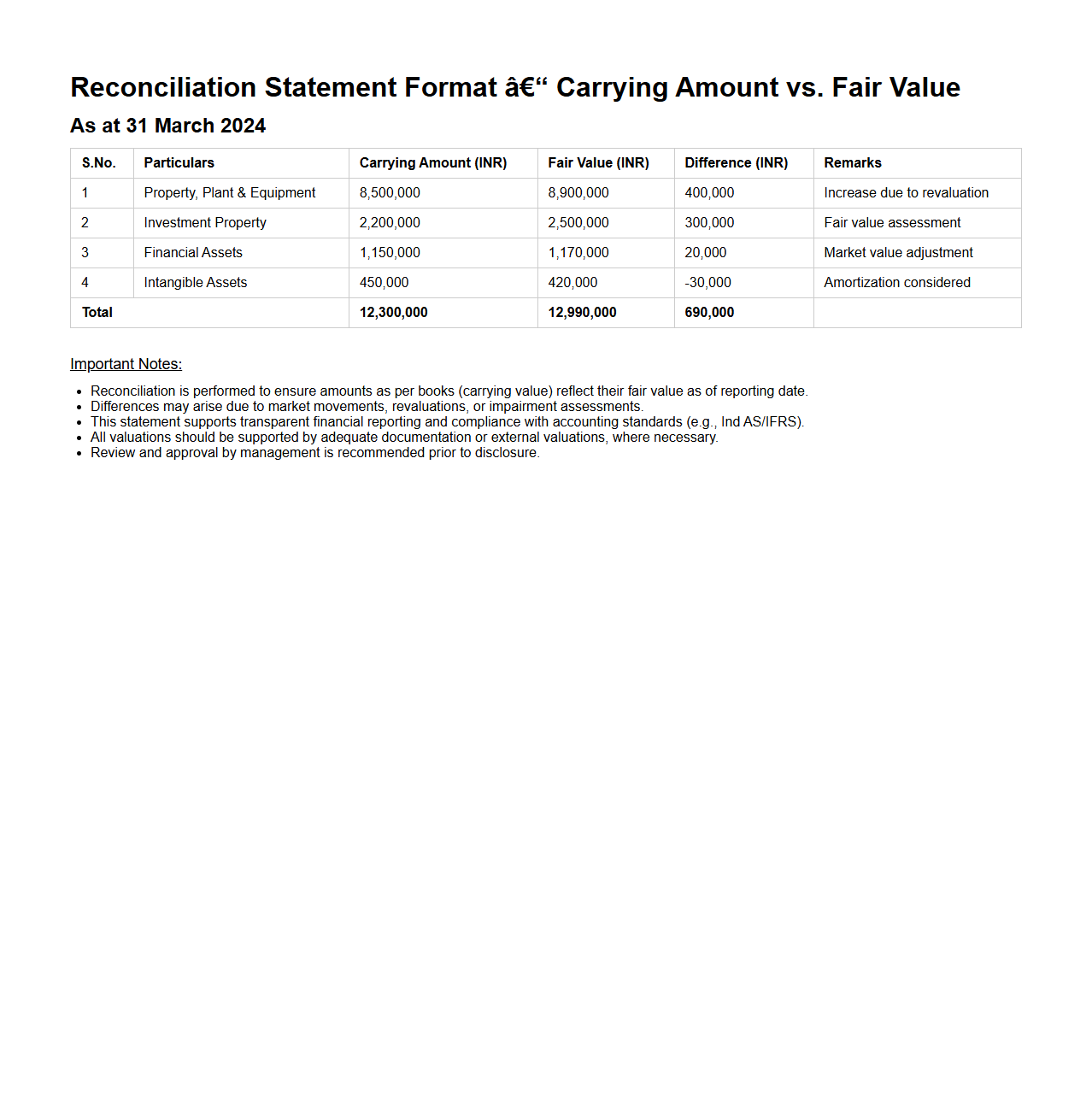

Reconciliation Statement Format – Carrying Amount vs. Fair Value

A

Reconciliation Statement Format - Carrying Amount vs. Fair Value document systematically compares the book value of an asset or liability with its market value to identify discrepancies. It highlights adjustments needed for accurate financial reporting and ensures compliance with accounting standards such as IFRS or GAAP. The format typically includes columns for carrying amount, fair value, and the resulting gain or loss, facilitating transparent asset valuation analysis.

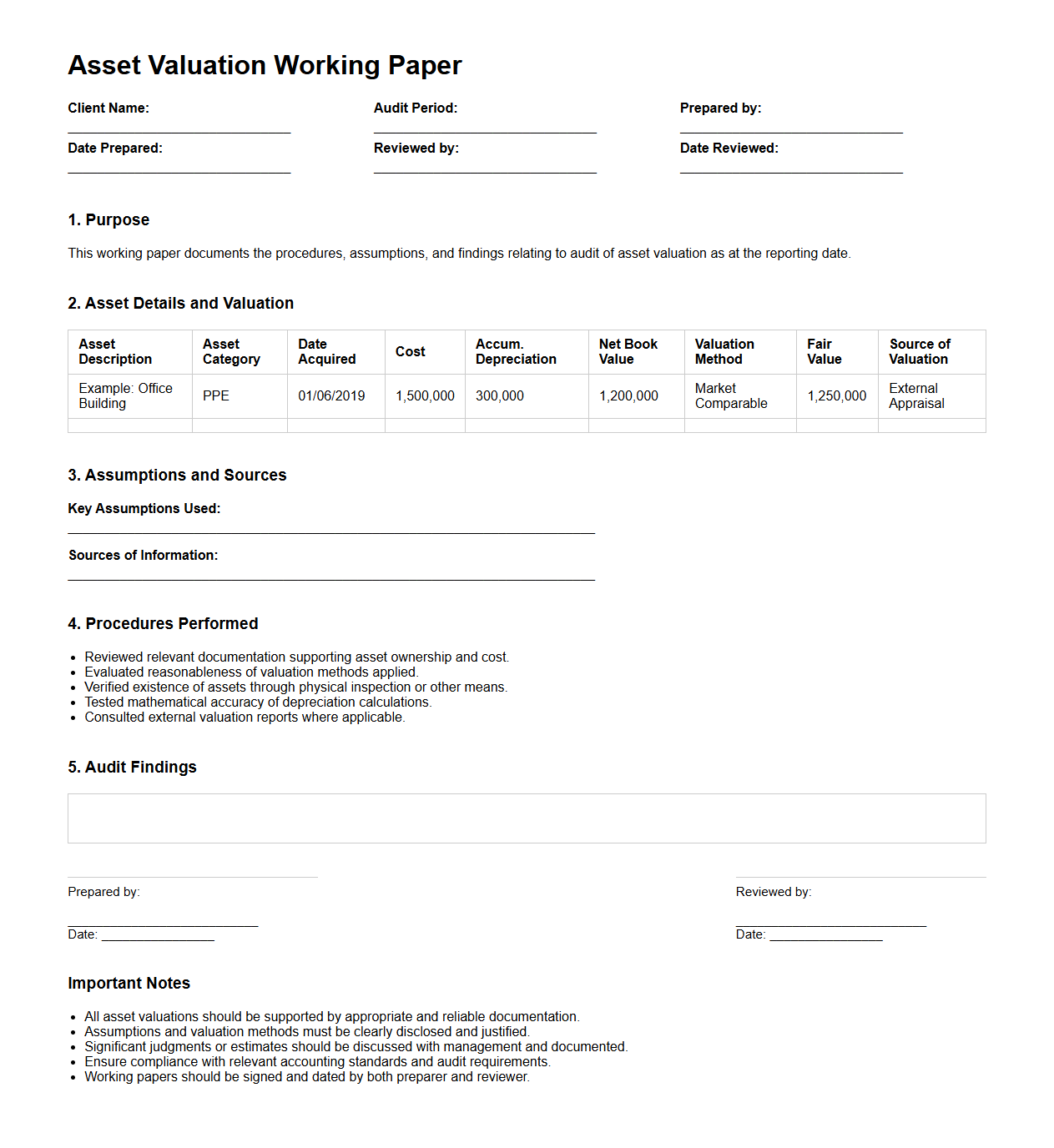

Asset Valuation Working Paper Format for Audit Purposes

The

Asset Valuation Working Paper Format for audit purposes is a structured document used by auditors to systematically record and assess the value of an organization's assets during the auditing process. It includes detailed schedules, valuation methods, supporting evidence, and reconciliations to ensure accuracy and compliance with accounting standards. This format helps maintain transparency, supports audit findings, and facilitates efficient review by audit teams and stakeholders.

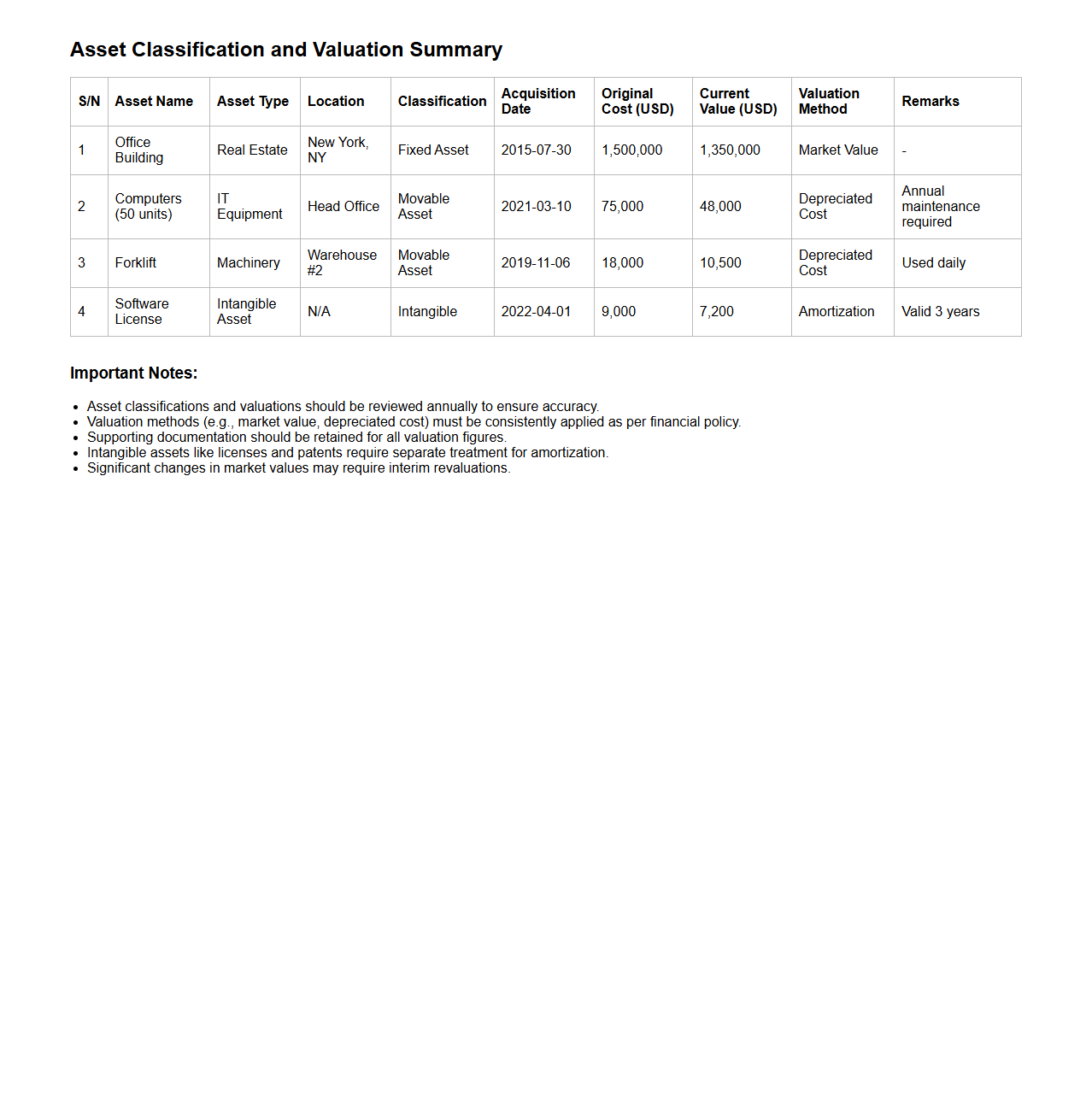

Asset Classification and Valuation Summary Table Format

The

Asset Classification and Valuation Summary Table Format document systematically organizes assets into categories based on type, condition, and usage, facilitating clear identification and management. It provides a structured layout for recording asset values, depreciation, and current worth, enabling accurate financial reporting and informed decision-making. This format streamlines asset tracking and supports compliance with accounting standards and regulatory requirements.

What are the key components required in the format of asset valuation for financial reporting?

The format of asset valuation for financial reporting must include the asset description, valuation method, and date of valuation to ensure transparency. Additionally, it should present the carrying amount and any accumulated depreciation or amortization. Inclusion of assumptions and estimation techniques used forms a vital part of the comprehensive valuation report.

How does the chosen valuation method impact the financial statement presentation of assets?

The chosen valuation method directly affects the asset's reported value and therefore the balance sheet totals. For example, fair value methods can introduce volatility due to market fluctuations, impacting profitability and equity figures. Historical cost methods typically result in more stable but potentially outdated asset values on financial statements.

In what ways are fair value and historical cost approaches disclosed in asset valuation documentation?

Asset valuation documentation must explicitly disclose whether fair value or historical cost approaches have been used. It should include detailed notes describing the measurement basis and the rationale behind using each approach. Furthermore, any significant changes in valuation methods over periods must be clearly communicated to stakeholders.

What supporting documents are necessary to validate the reported asset values for financial reporting purposes?

Supporting documents such as purchase invoices, appraisal reports, and market price quotations are essential to substantiate reported asset values. Additionally, internal records like depreciation schedules and impairment assessments provide further validation. These documents ensure reliability and compliance with accounting standards during audits.

How are impairment losses and reversals reflected in the format of asset valuation reports?

Impairment losses must be clearly identified and quantified within the asset valuation report, showing reductions in the carrying amount. Reversals of impairment, when applicable, are disclosed separately to indicate recovery in asset value. Both are presented with explanations of the triggering events and the impact on financial statements for full transparency.