A Format of Subsidiary Ledger for Ledger organizes detailed accounts related to a specific general ledger account, providing clarity and ease of reference. It typically includes columns for dates, particulars, debit, credit, and balance, ensuring accurate tracking of transactions. This format supports effective reconciliation and financial reporting by breaking down complex accounts into manageable sections.

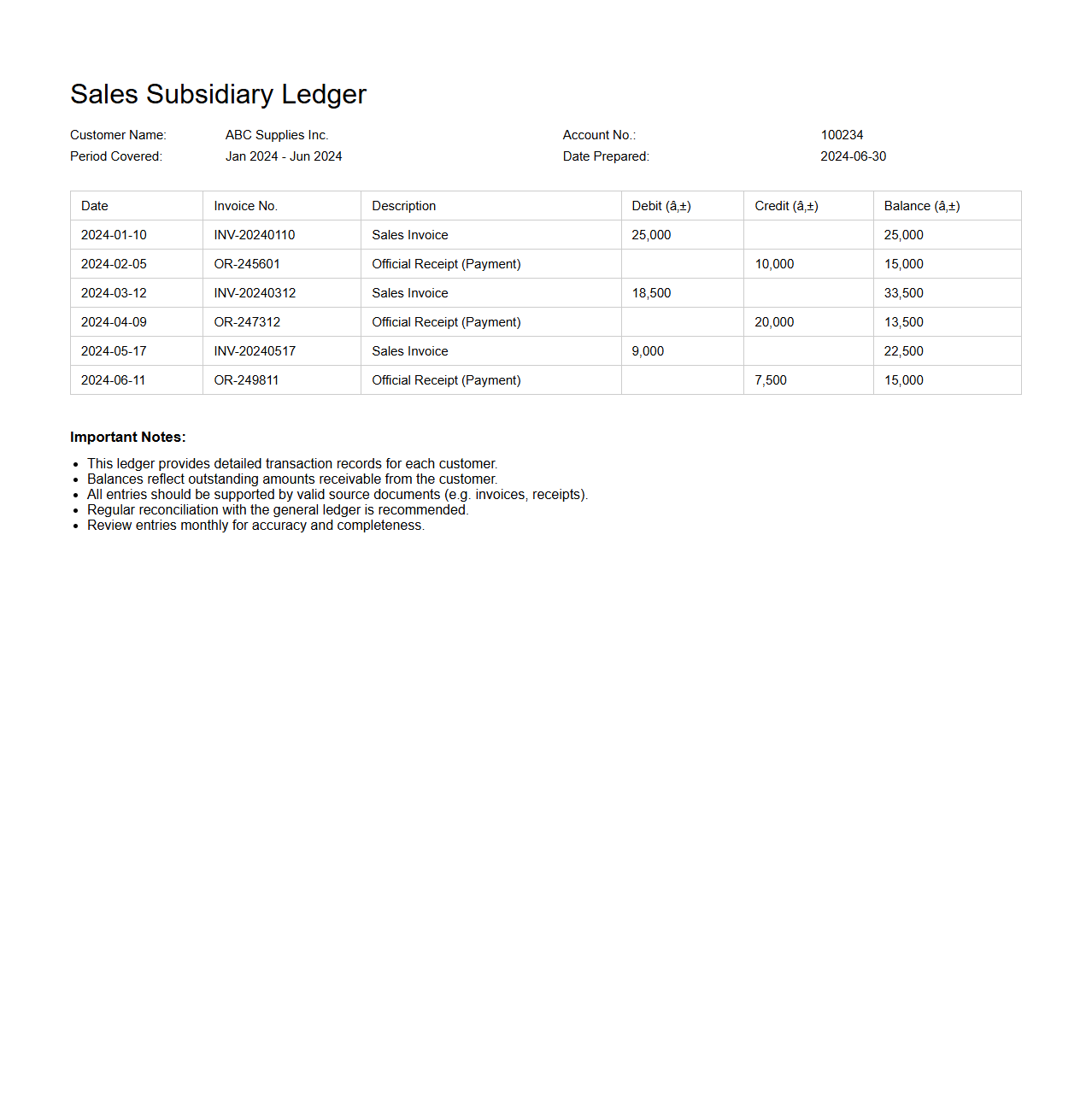

Sales Subsidiary Ledger Document Format

A

Sales Subsidiary Ledger Document Format is a standardized template used to record detailed sales transactions for individual customers or accounts, providing a clear and organized breakdown of sales activities. This document format ensures accurate tracking of invoices, payments, and outstanding balances, supporting efficient accounts receivable management. It facilitates transparency and reconciliation between the subsidiary ledger and the general ledger in financial accounting systems.

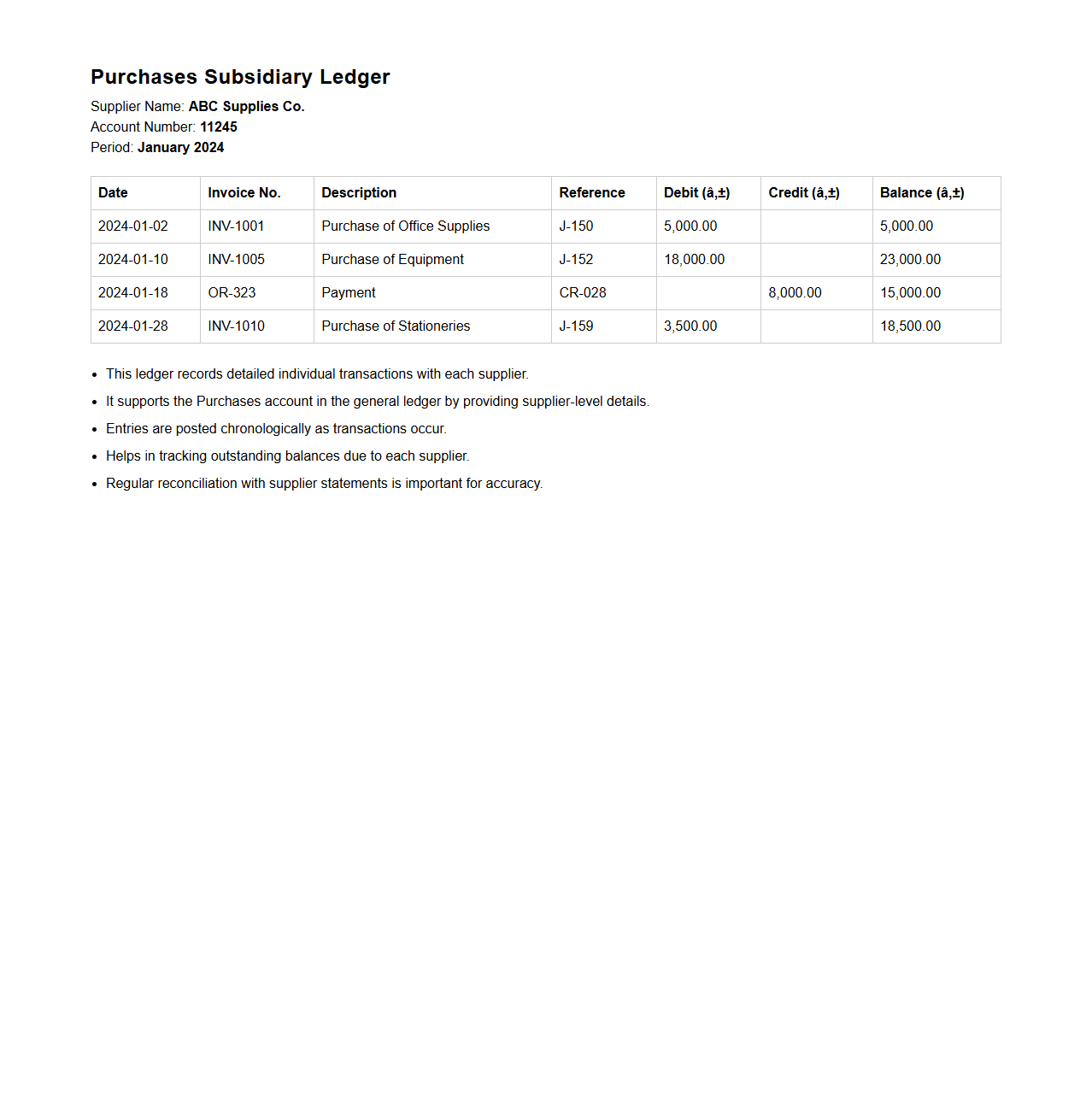

Purchases Subsidiary Ledger Document Format

The

Purchases Subsidiary Ledger Document Format is a structured template used to record and organize detailed transactions related to purchases made by a company. It captures essential data such as vendor information, invoice numbers, dates, amounts, and payment status, facilitating accurate tracking and reconciliation of accounts payable. This format enhances financial transparency and supports audit processes by maintaining a clear record of all purchase activities.

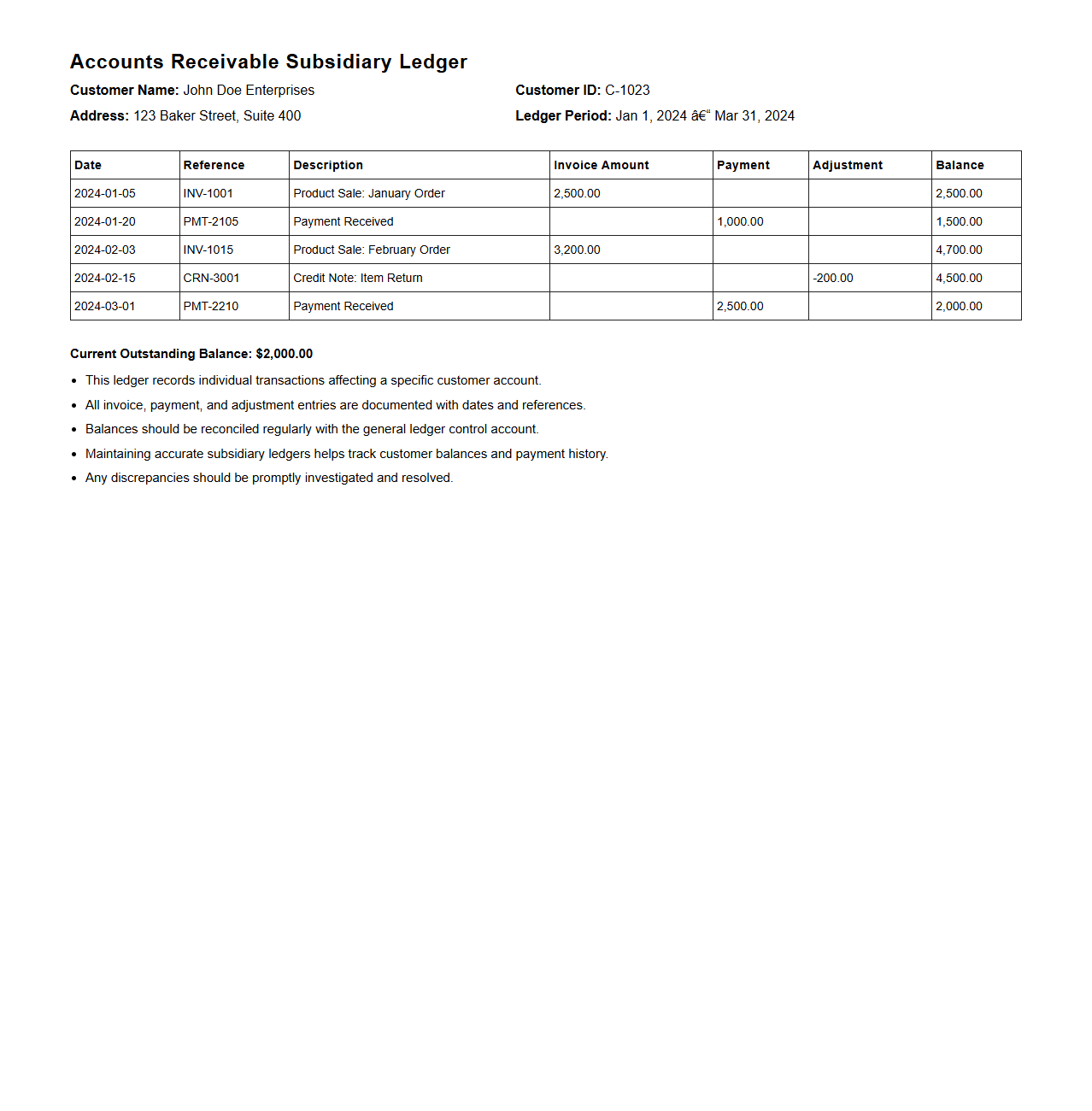

Accounts Receivable Subsidiary Ledger Document Format

The

Accounts Receivable Subsidiary Ledger Document Format is a structured template used to record detailed customer transactions, including invoices, payments, and credits. It provides a clear breakdown of individual account balances, ensuring accurate tracking of outstanding receivables and effective credit management. This document supports financial reconciliation by organizing data systematically, facilitating better accounts receivable control and reporting.

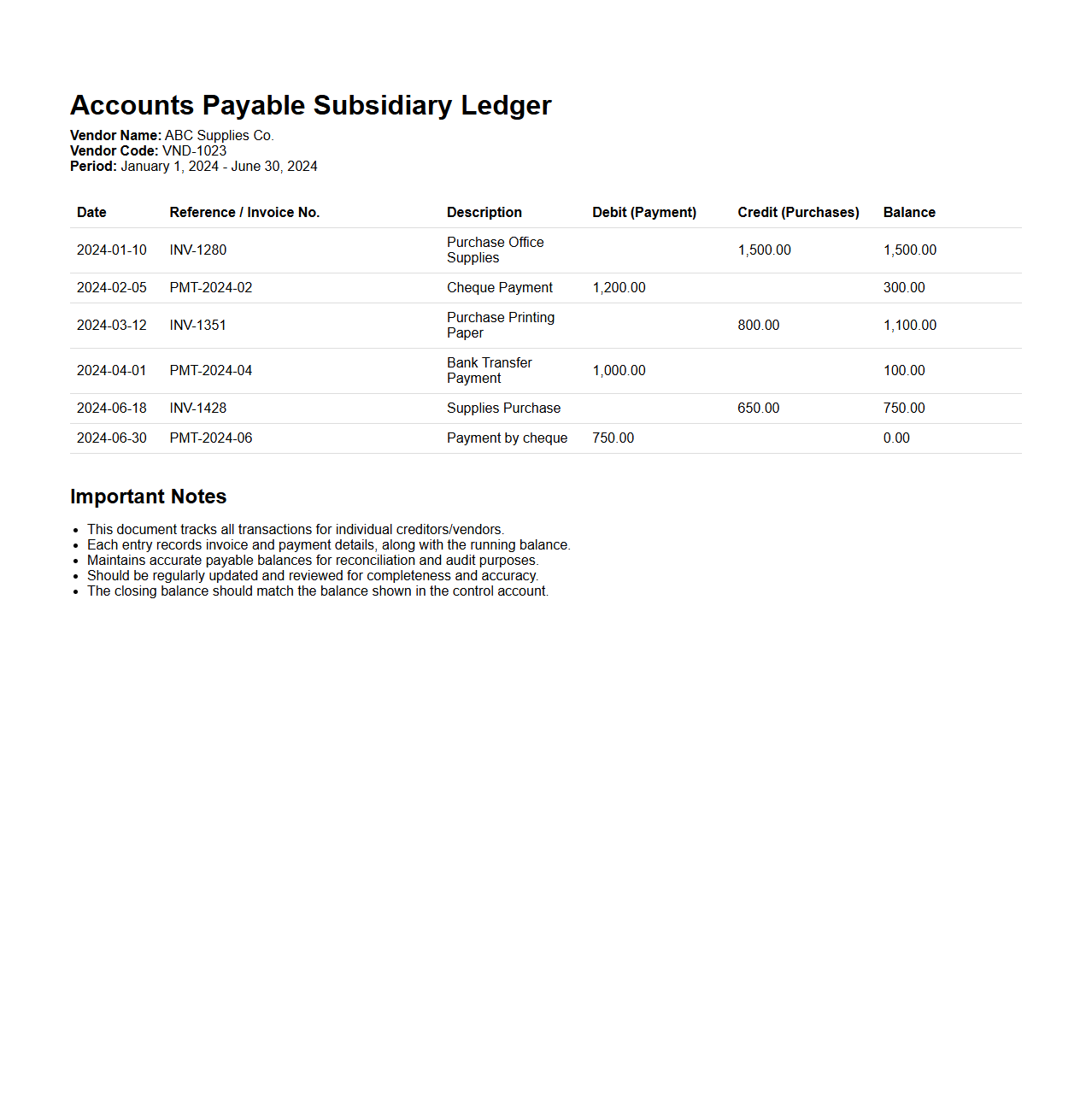

Accounts Payable Subsidiary Ledger Document Format

The

Accounts Payable Subsidiary Ledger Document Format is a standardized template used to record detailed vendor transaction information, ensuring accurate tracking of outstanding liabilities. This document format includes essential fields such as invoice numbers, payment dates, vendor names, and amounts payable, facilitating efficient reconciliation and audit processes. Its structured layout promotes transparency and helps maintain up-to-date financial records within the accounts payable system.

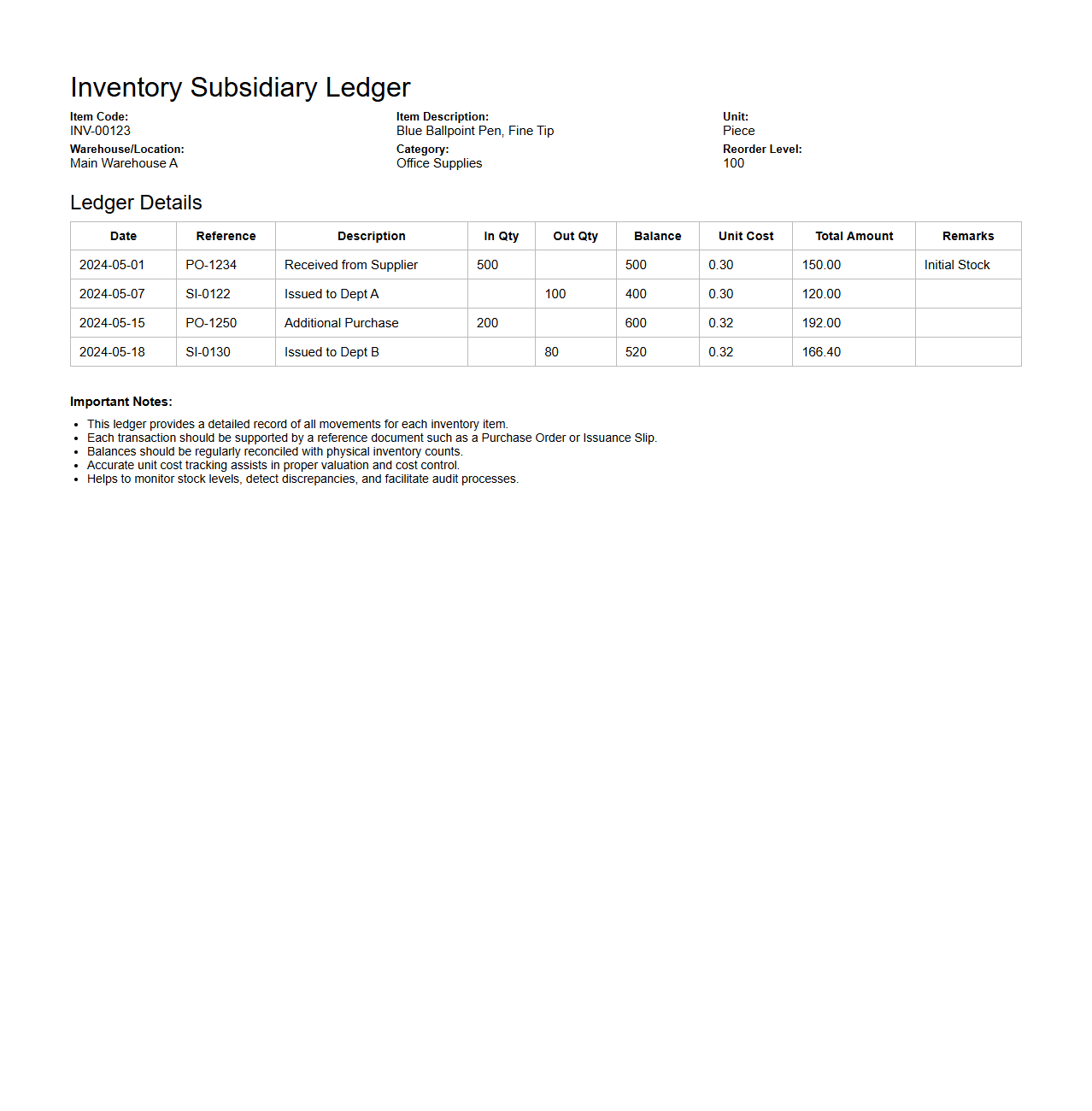

Inventory Subsidiary Ledger Document Format

An

Inventory Subsidiary Ledger Document Format is a structured record-keeping template used to detail individual inventory transactions within a subsidiary ledger. This document format helps track quantities, values, and movements of inventory items, ensuring accurate reconciliation with the general ledger. It plays a crucial role in inventory management by providing granular data for auditing, stock control, and financial reporting processes.

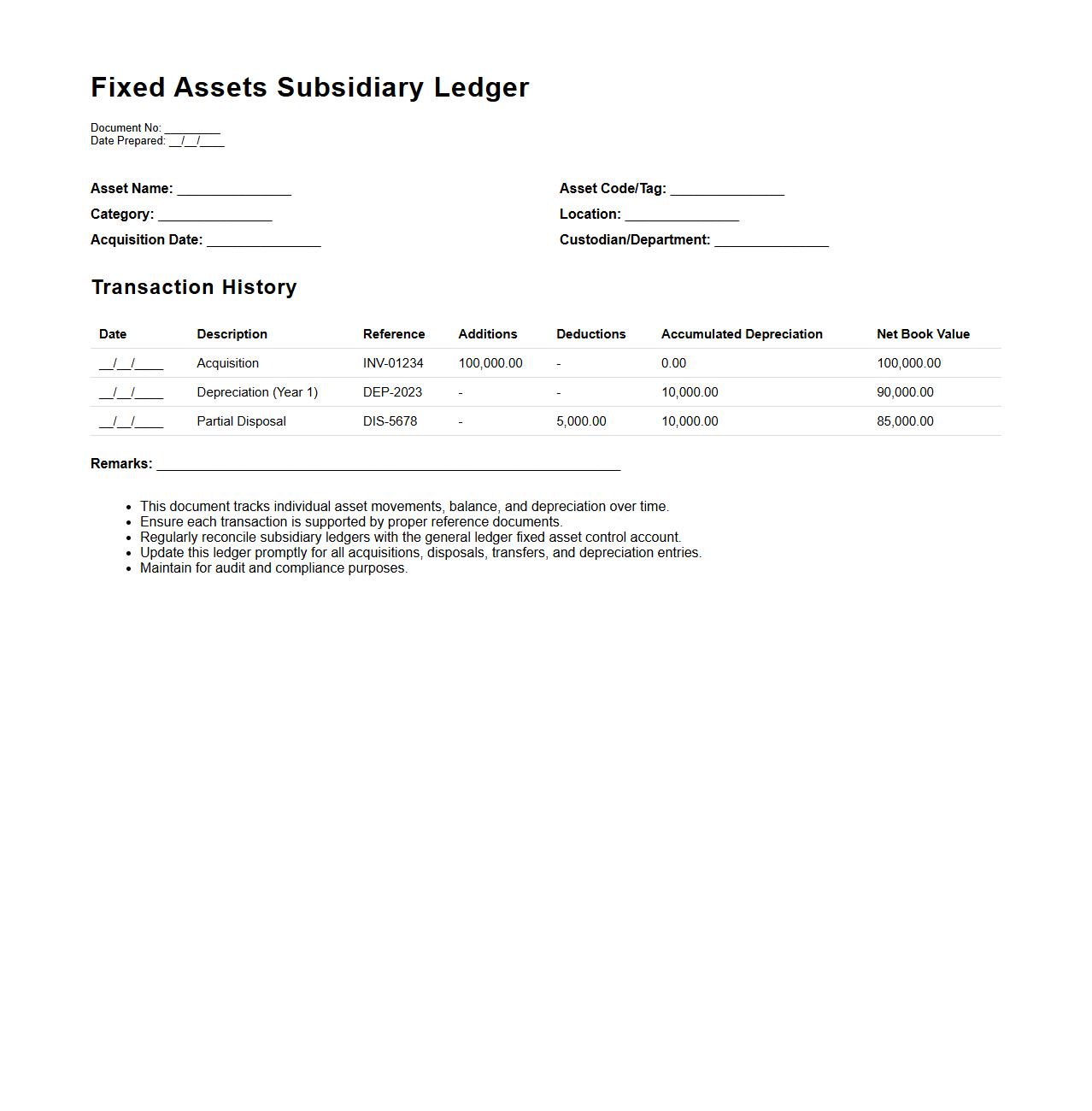

Fixed Assets Subsidiary Ledger Document Format

A

Fixed Assets Subsidiary Ledger Document Format is a structured template used to systematically record detailed information about an organization's fixed assets, such as acquisition dates, asset descriptions, locations, and depreciation values. This document ensures accuracy and consistency in tracking asset histories, facilitating efficient asset management and financial reporting. It integrates with the general ledger to provide a comprehensive view of fixed asset transactions and balances.

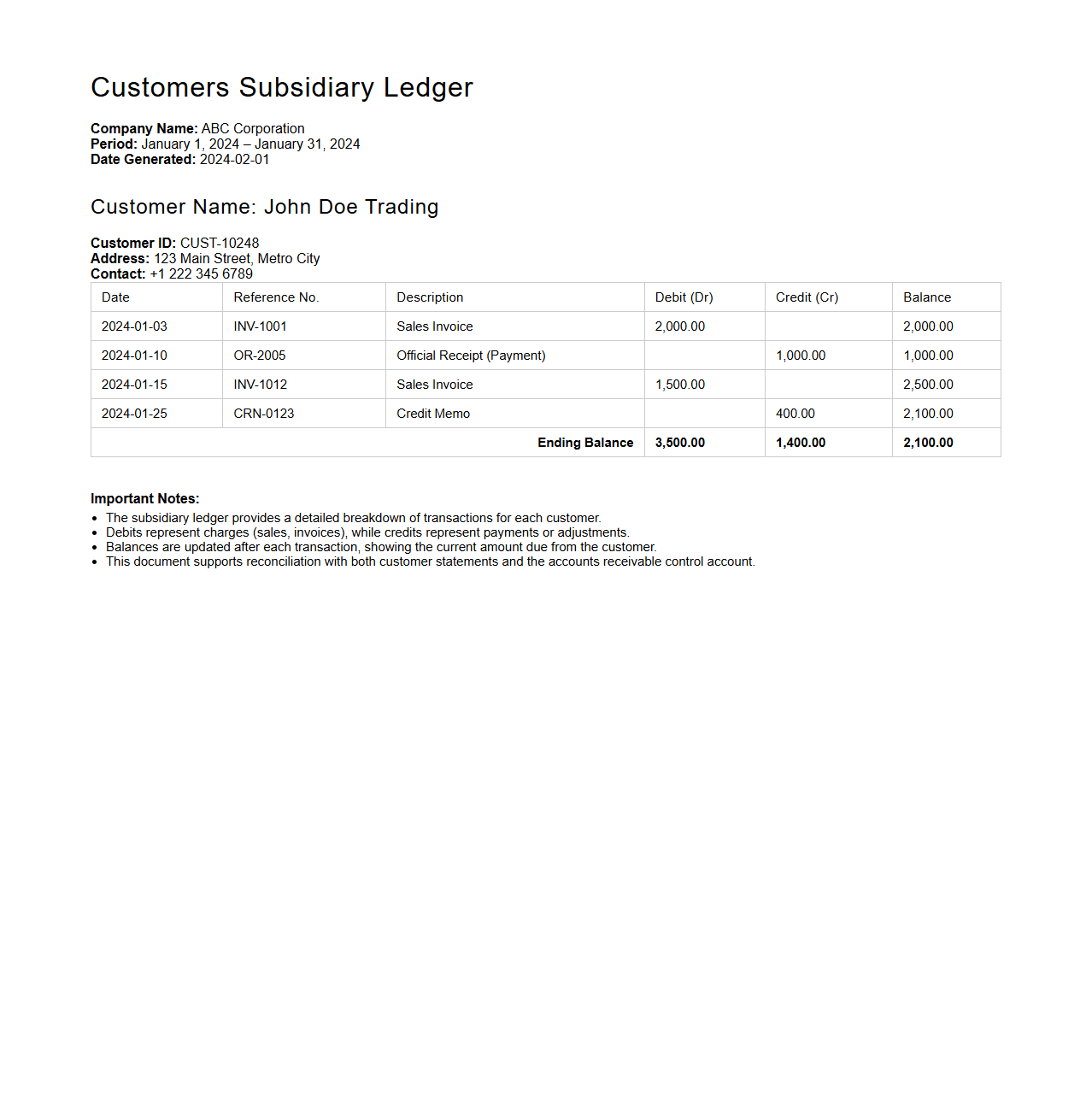

Customers Subsidiary Ledger Document Format

A

Customers Subsidiary Ledger Document Format is a structured financial record used to detail individual customer transactions within a company's subsidiary ledger. It organizes credit sales, payments, and outstanding balances, allowing for precise tracking of each customer's account activity. This document format enhances accuracy in accounts receivable management and supports efficient reconciliation with the general ledger.

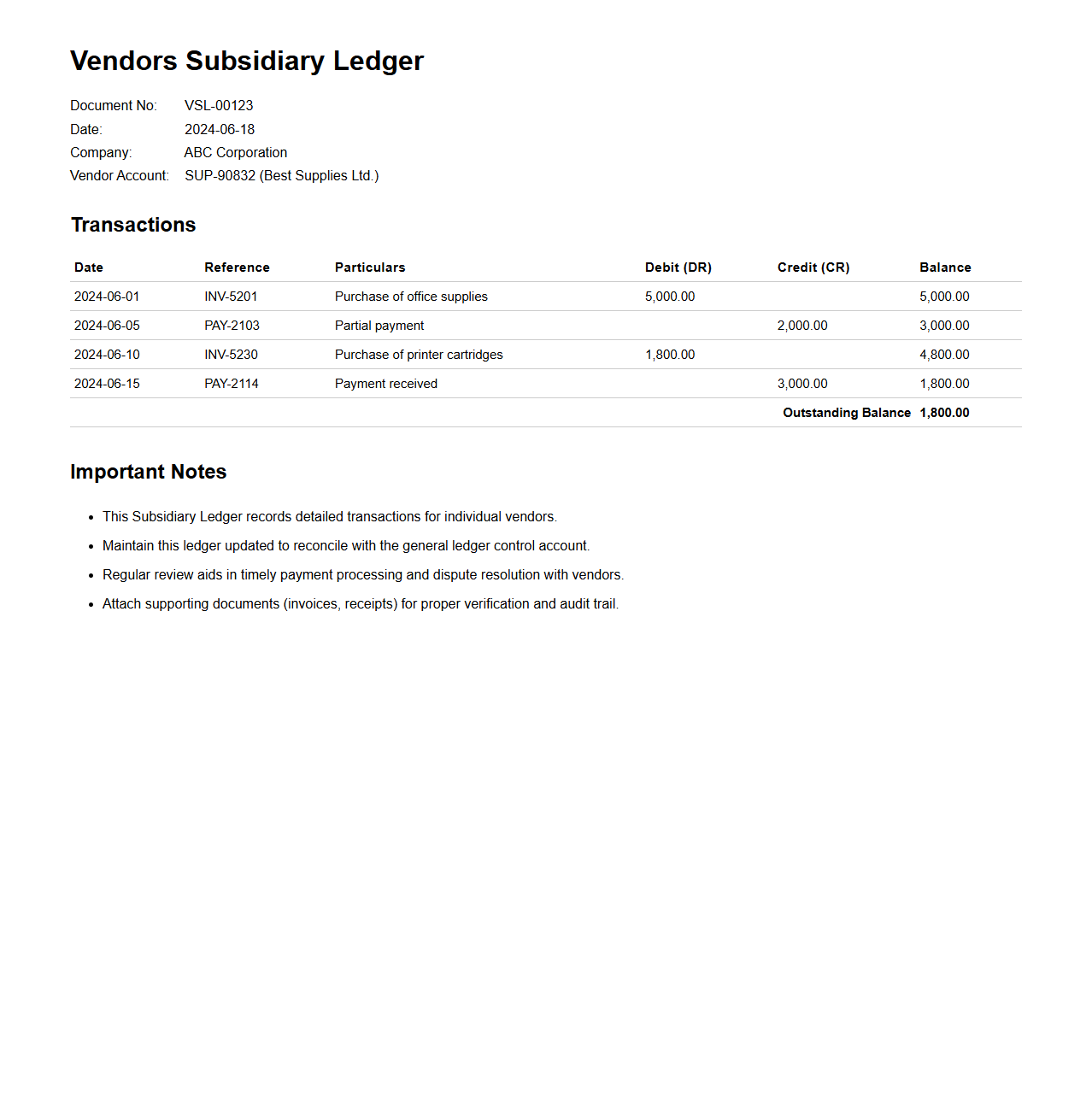

Vendors Subsidiary Ledger Document Format

The

Vendors Subsidiary Ledger Document Format is a structured template used to organize and present detailed transaction records between a company and its vendors. It includes vendor names, invoice numbers, payment dates, and outstanding balances, facilitating accurate tracking of payables and reconciliation with the general ledger. This document format enhances financial transparency and supports efficient accounts payable management.

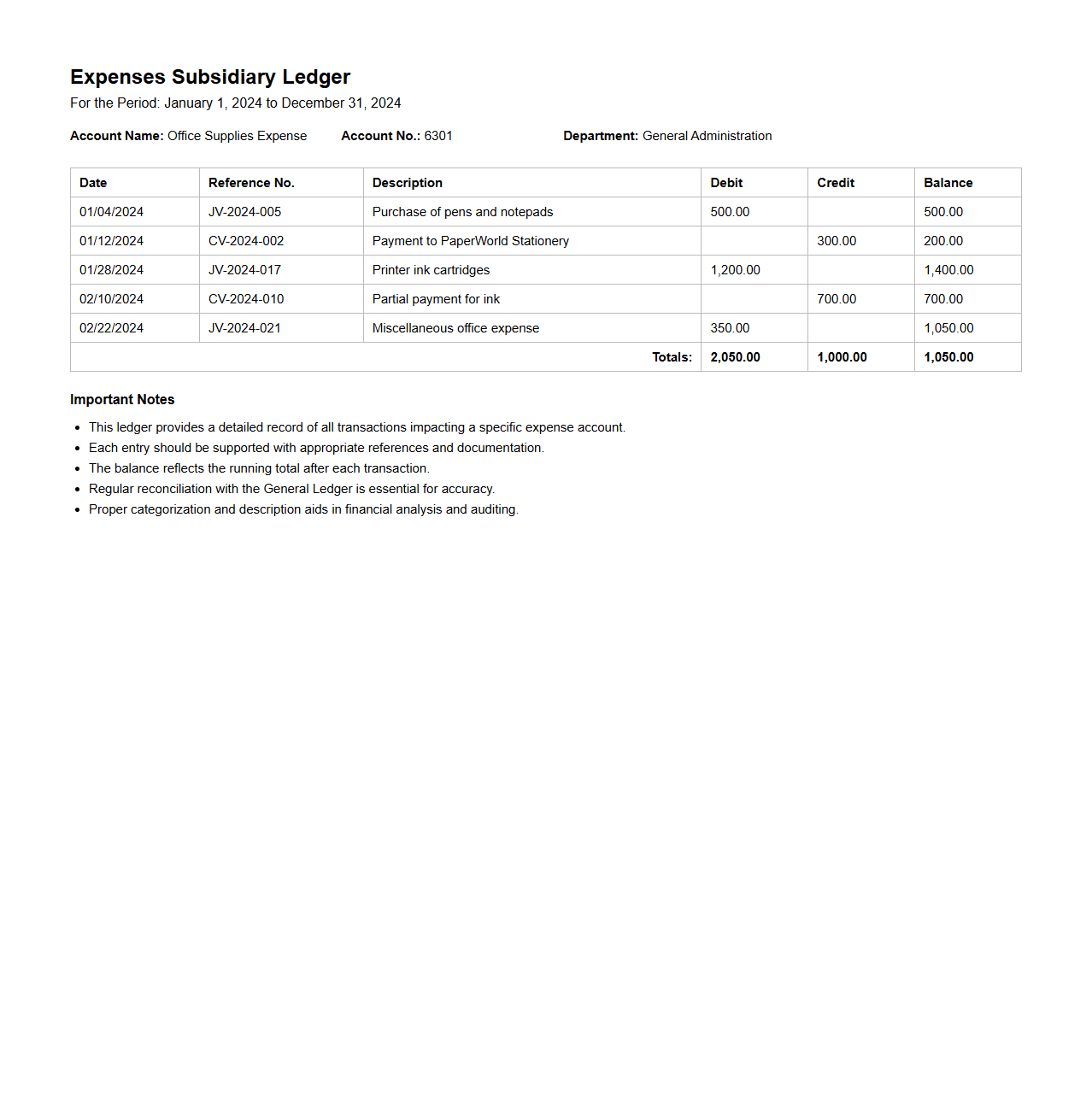

Expenses Subsidiary Ledger Document Format

An

Expenses Subsidiary Ledger Document Format is a structured template used to record detailed financial transactions related to a company's expenses. It organizes expense data by categories or individual accounts, facilitating accurate tracking, auditing, and reporting. This format ensures consistency and clarity in documenting expense details, supporting efficient financial management and compliance.

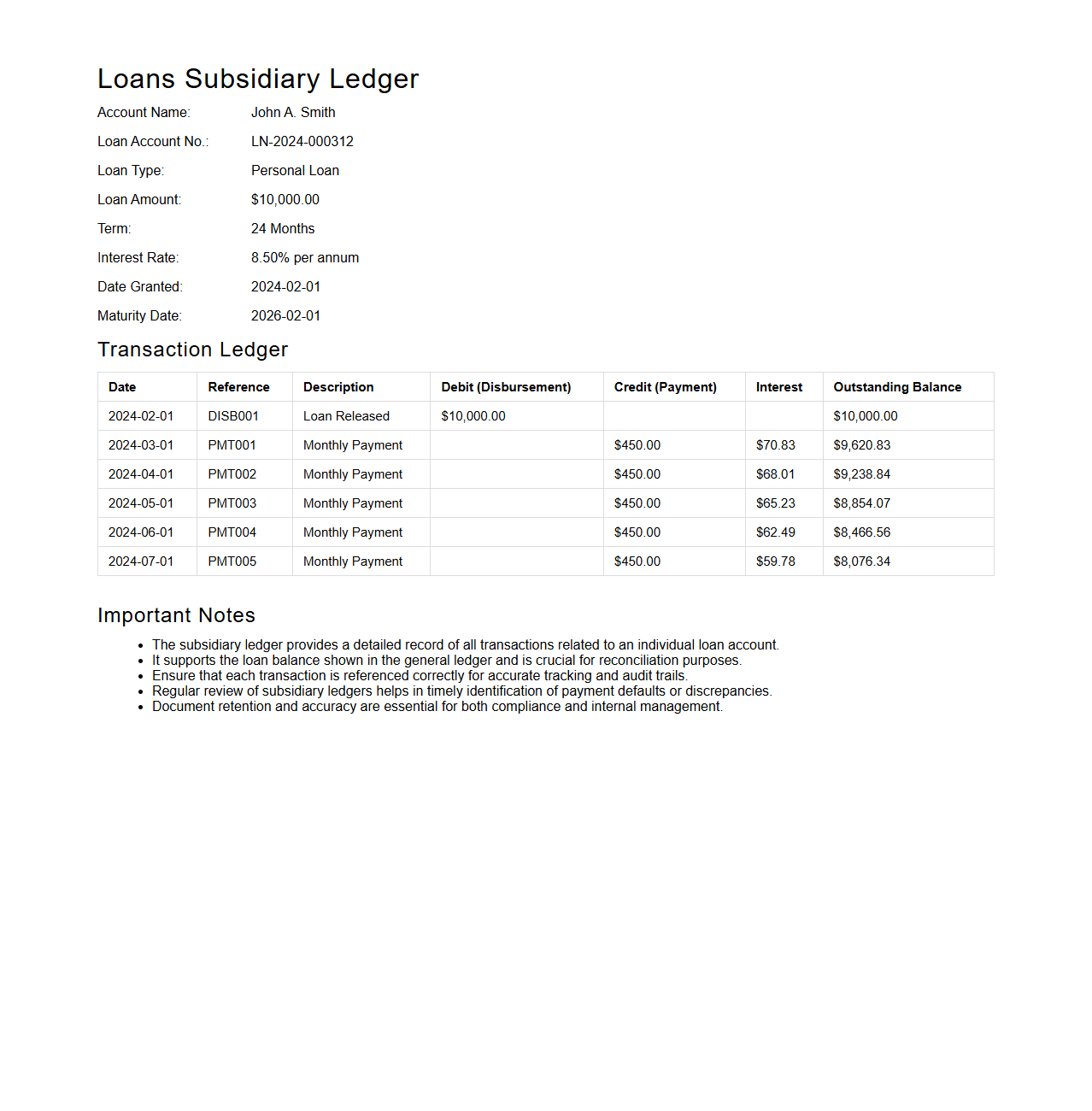

Loans Subsidiary Ledger Document Format

A

Loans Subsidiary Ledger Document Format is a structured financial record used to track individual loan transactions, balances, and payment histories separately from the general ledger. This format enables detailed monitoring of each loan account, ensuring accuracy in loan management and facilitating reconciliation with the general ledger. It typically includes fields such as loan amount, borrower details, payment dates, interest rates, and outstanding balances, making it essential for precise loan accounting and reporting.

What are the essential components included in the header of a subsidiary ledger document format?

The header of a subsidiary ledger document format must include critical identification details such as the customer or vendor name, account number, and the reporting period. It also typically features the subsidiary ledger's unique code, ensuring easy distinction from other ledgers. Including the date of document preparation enhances the accuracy and traceability of the ledger.

How should subsidiary ledger columns be structured for tracking accounts receivable and payable distinctly?

Subsidiary ledger columns must be organized separately for accounts receivable and accounts payable to maintain clarity. Typical columns include the transaction date, description, debit, credit, and the resulting balance for each account type. This distinct columnar structure facilitates efficient monitoring of outstanding amounts and timely reconciliations.

Which document numbering system is optimal for organized subsidiary ledger entries?

An alphanumeric sequential numbering system is optimal for subsidiary ledger entries, as it ensures uniqueness and easy reference. Incorporating prefixes indicating the ledger type (e.g., AR for accounts receivable) further enhances organization. This systematic approach promotes streamlined audits and quick retrieval of transactions.

What is the recommended referencing style for linking the subsidiary ledger to the main ledger?

The recommended referencing style involves using a cross-reference code or number in both the subsidiary and main ledgers. This code typically combines the subsidiary ledger entry number with the main ledger account number to enhance accuracy. Employing consistent linking references ensures seamless integration and reconciliation between ledgers.

How should adjustments and corrections be transparently formatted in a subsidiary ledger document?

Adjustments and corrections must be clearly annotated in the subsidiary ledger, usually by marking entries as "Adjustment" with the appropriate date and explanation. Using distinct colors or symbols can also improve transparency and prevent confusion. Proper documentation of these changes supports audit trails and financial integrity.