Format of Working Papers for Audit Evidence typically includes a clear heading, referencing system, and organized sections for audit procedures, findings, and conclusions. Each working paper should be concise, legible, and systematically arranged to ensure audit evidence is easily accessible and verifiable. Proper documentation enhances the reliability and effectiveness of the audit process.

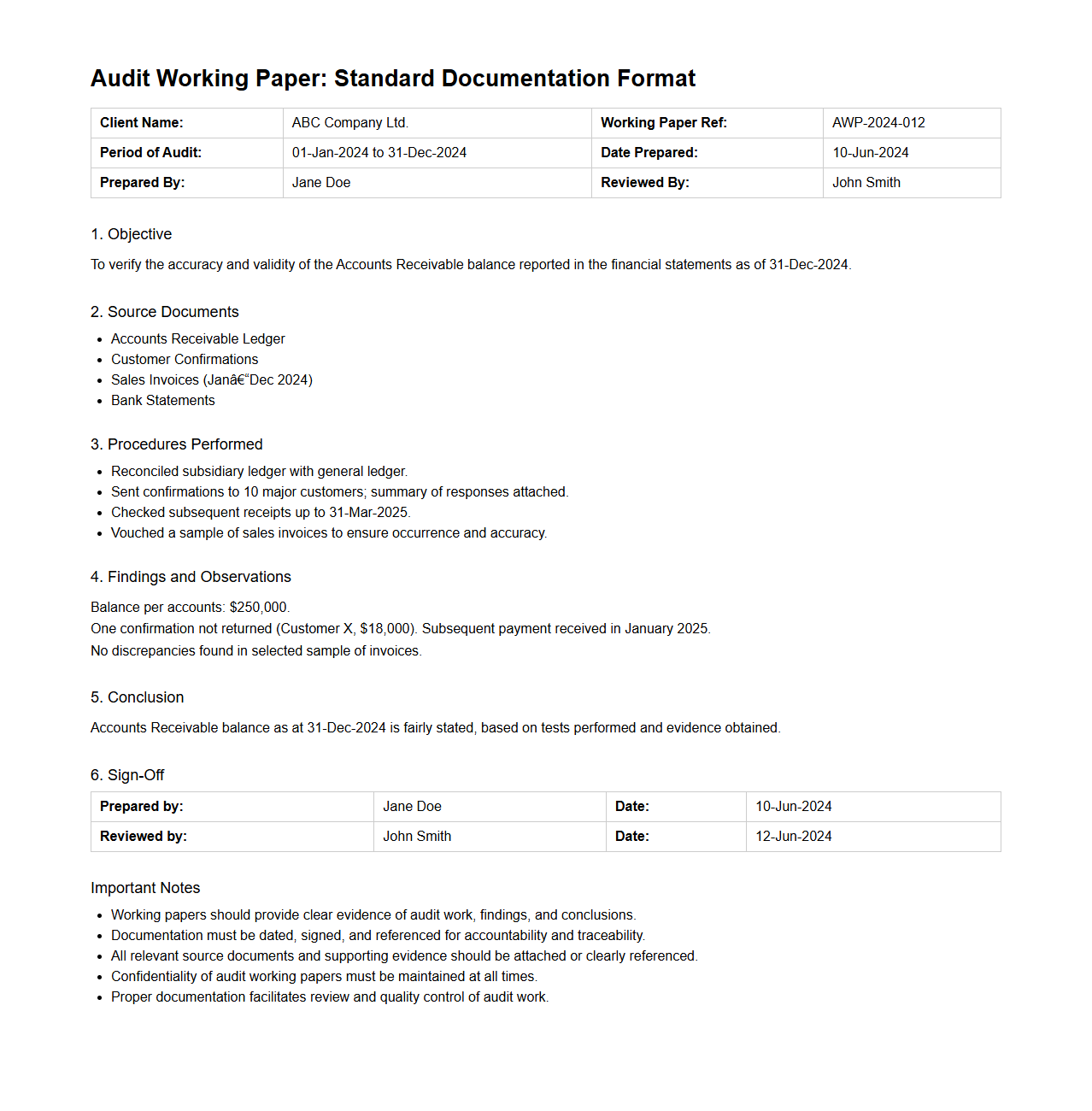

Audit Working Paper: Standard Documentation Format

Audit Working Paper: Standard Documentation Format document provides a systematic framework for organizing and presenting audit evidence and findings. It ensures consistency, clarity, and completeness in documenting audit procedures, supporting compliance with auditing standards. This format facilitates efficient review, enhances traceability, and strengthens the overall

audit quality and reliability.

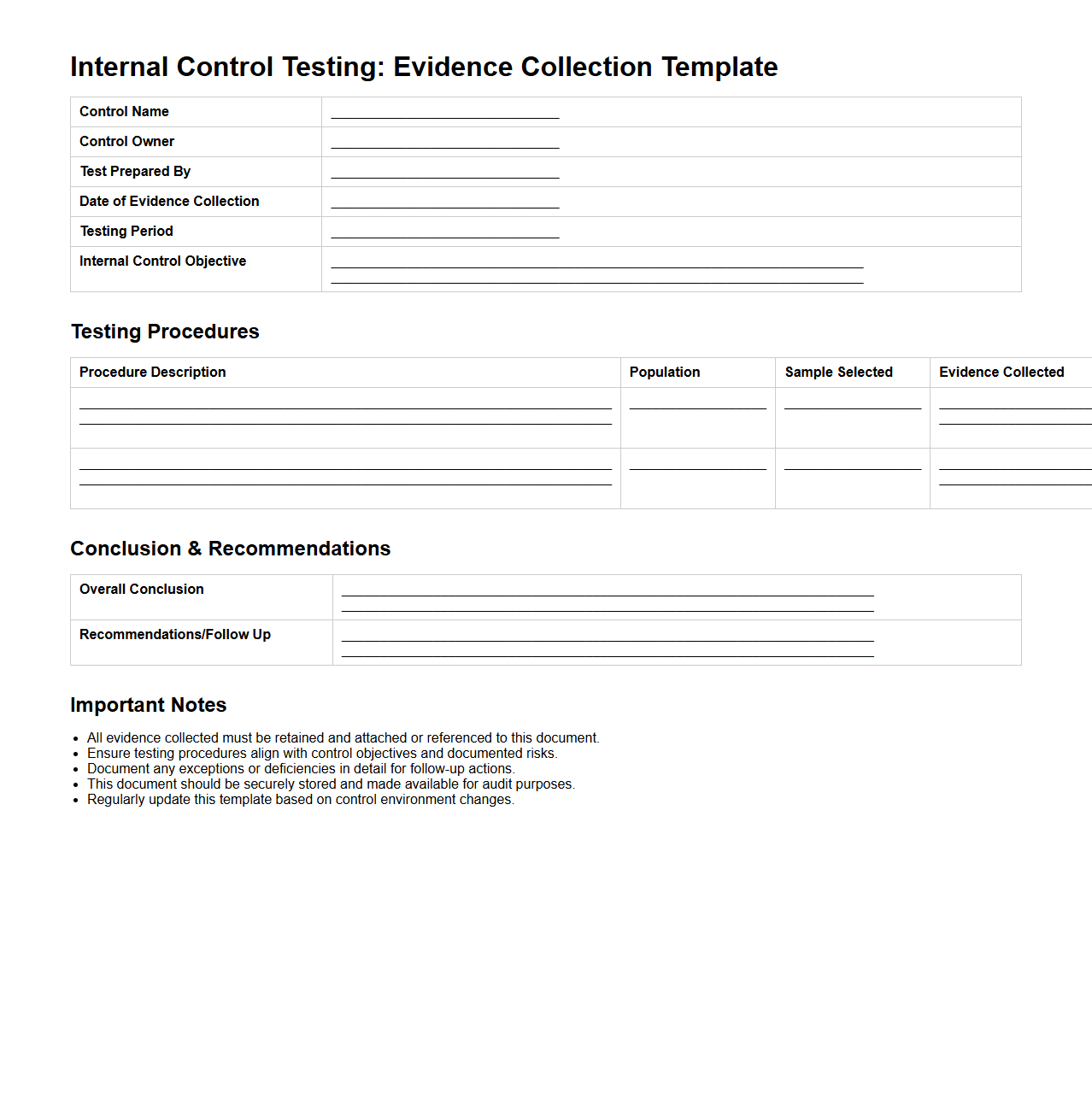

Internal Control Testing: Evidence Collection Template

The

Internal Control Testing: Evidence Collection Template document is a structured tool used to systematically gather and organize evidence during the assessment of internal controls within an organization. It facilitates the documentation of control activities, testing procedures, and results, ensuring compliance with regulatory standards and audit requirements. This template enhances accuracy and efficiency in evaluating the effectiveness of risk management and operational controls.

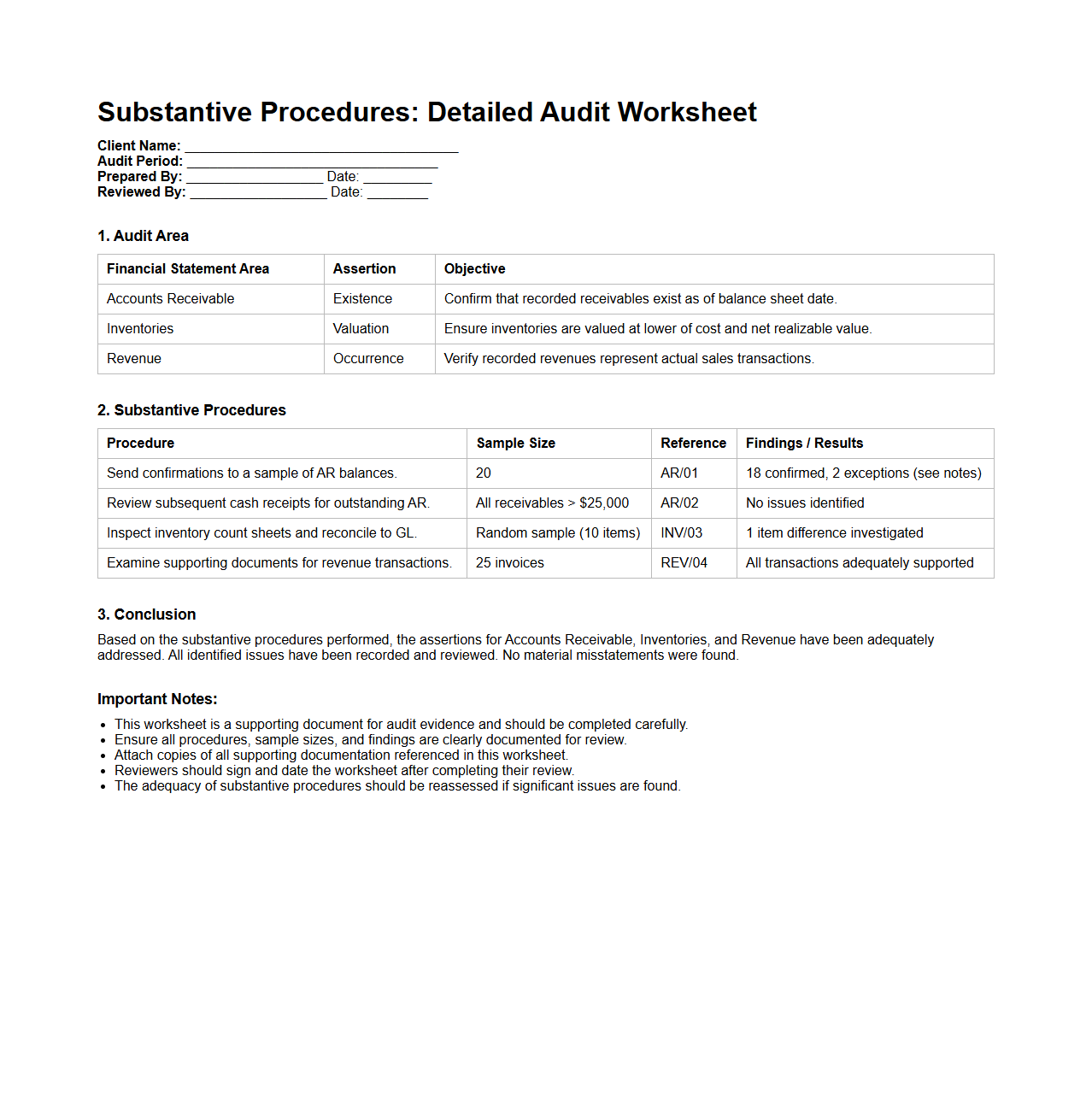

Substantive Procedures: Detailed Audit Worksheet

The

Substantive Procedures: Detailed Audit Worksheet document outlines specific audit tests and detailed procedures auditors perform to verify the accuracy and completeness of financial statement assertions. It serves as a comprehensive record of evidence collected through substantive tests, including inspection, observation, confirmation, and recalculation, ensuring compliance with auditing standards. This worksheet helps auditors identify discrepancies, quantify misstatements, and supports the final audit opinion on the entity's financial reporting.

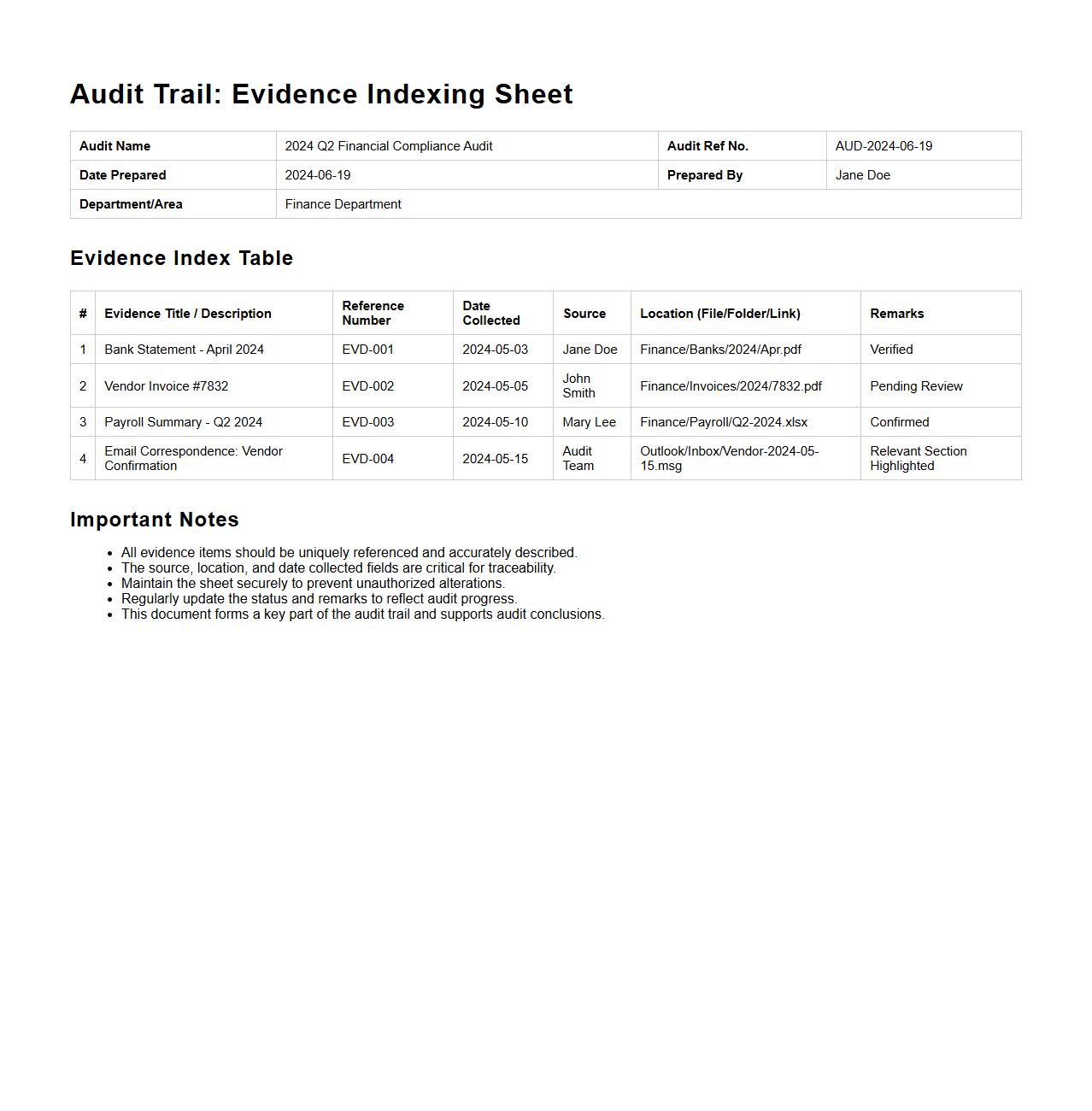

Audit Trail: Evidence Indexing Sheet

An

Audit Trail: Evidence Indexing Sheet document systematically records and organizes evidence related to audits, ensuring traceability and accountability throughout the audit process. It indexes each piece of evidence by date, source, and relevance, facilitating efficient retrieval and verification. This document supports compliance with regulatory standards and improves the integrity of audit findings.

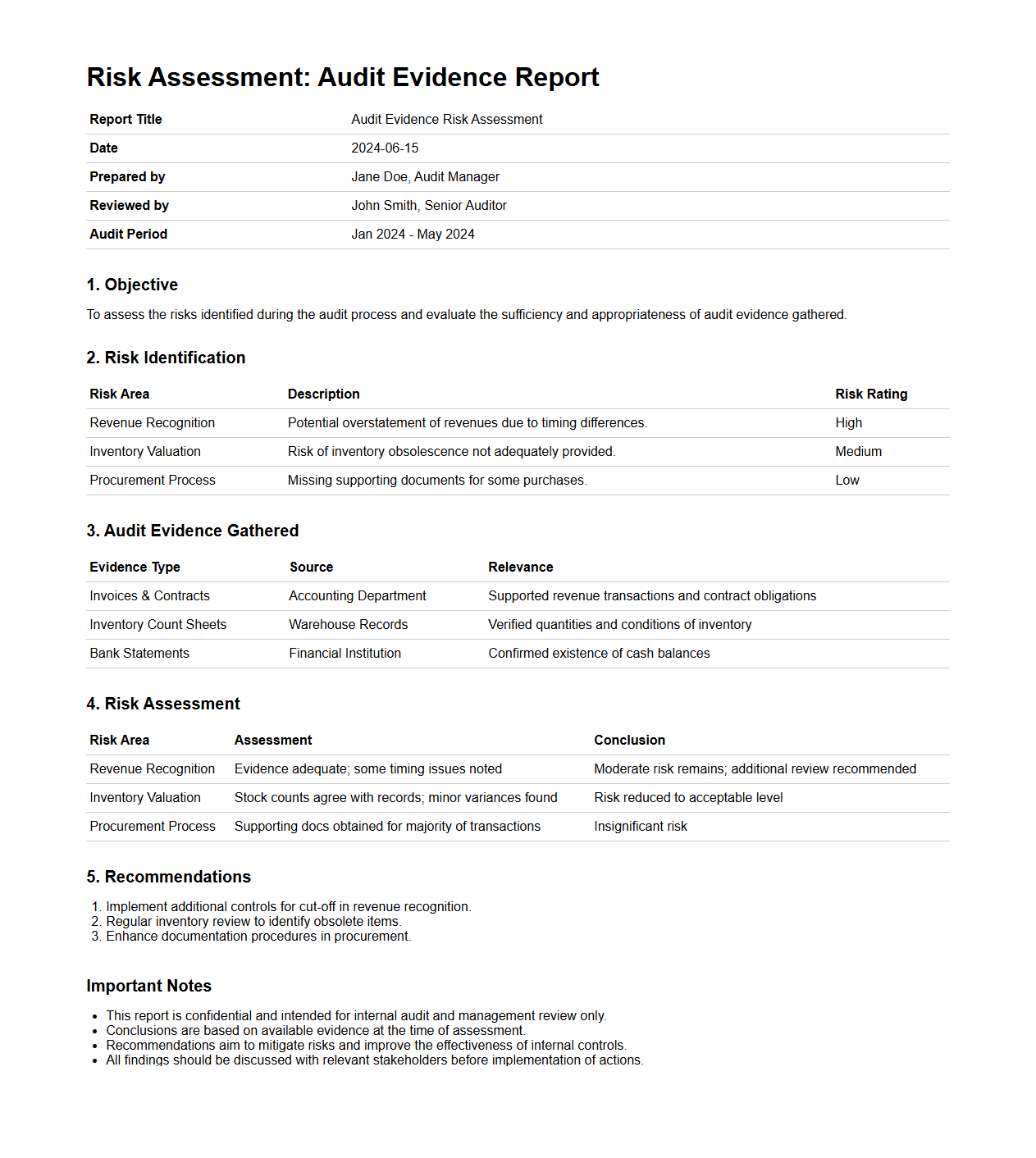

Risk Assessment: Audit Evidence Report Format

The

Risk Assessment: Audit Evidence Report Format document outlines a structured approach for collecting, analyzing, and documenting audit evidence related to identifying and evaluating risks within an organization. This format standardizes the way auditors capture findings, ensuring consistency and completeness in assessing potential threats to financial accuracy, compliance, and operational effectiveness. It facilitates clear communication among audit teams and stakeholders by providing a detailed, evidence-based framework to support risk mitigation strategies.

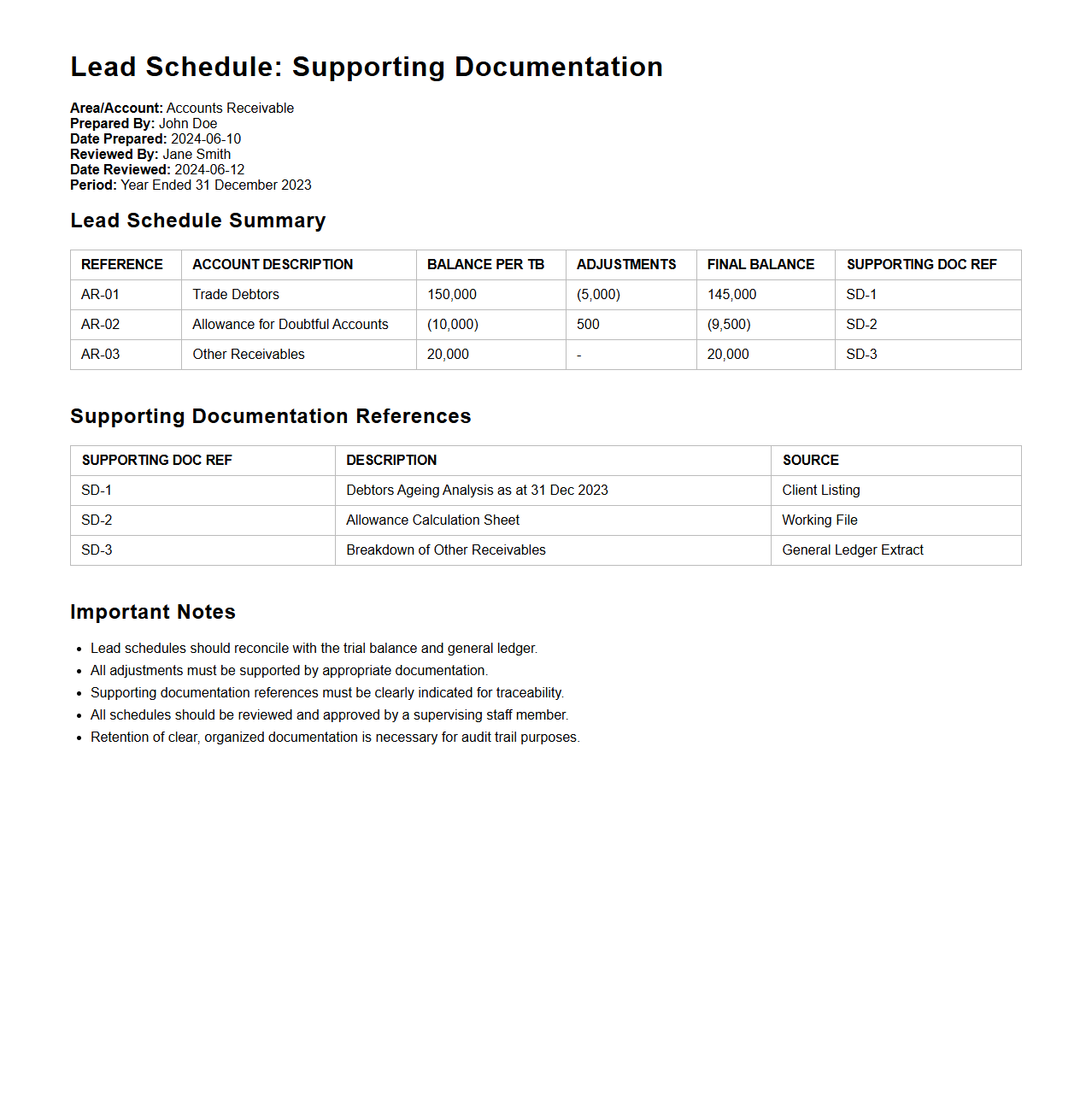

Lead Schedule: Supporting Documentation Format

Lead Schedule: Supporting Documentation Format document organizes and consolidates all relevant financial data, audit evidence, and working papers into a structured format for easy reference and review. This

key audit tool enhances accuracy, streamlines audit processes, and ensures compliance with regulatory standards by linking summary financial information directly to detailed supporting evidence. It serves as a critical resource for auditors to validate transactions and maintain transparency throughout the audit lifecycle.

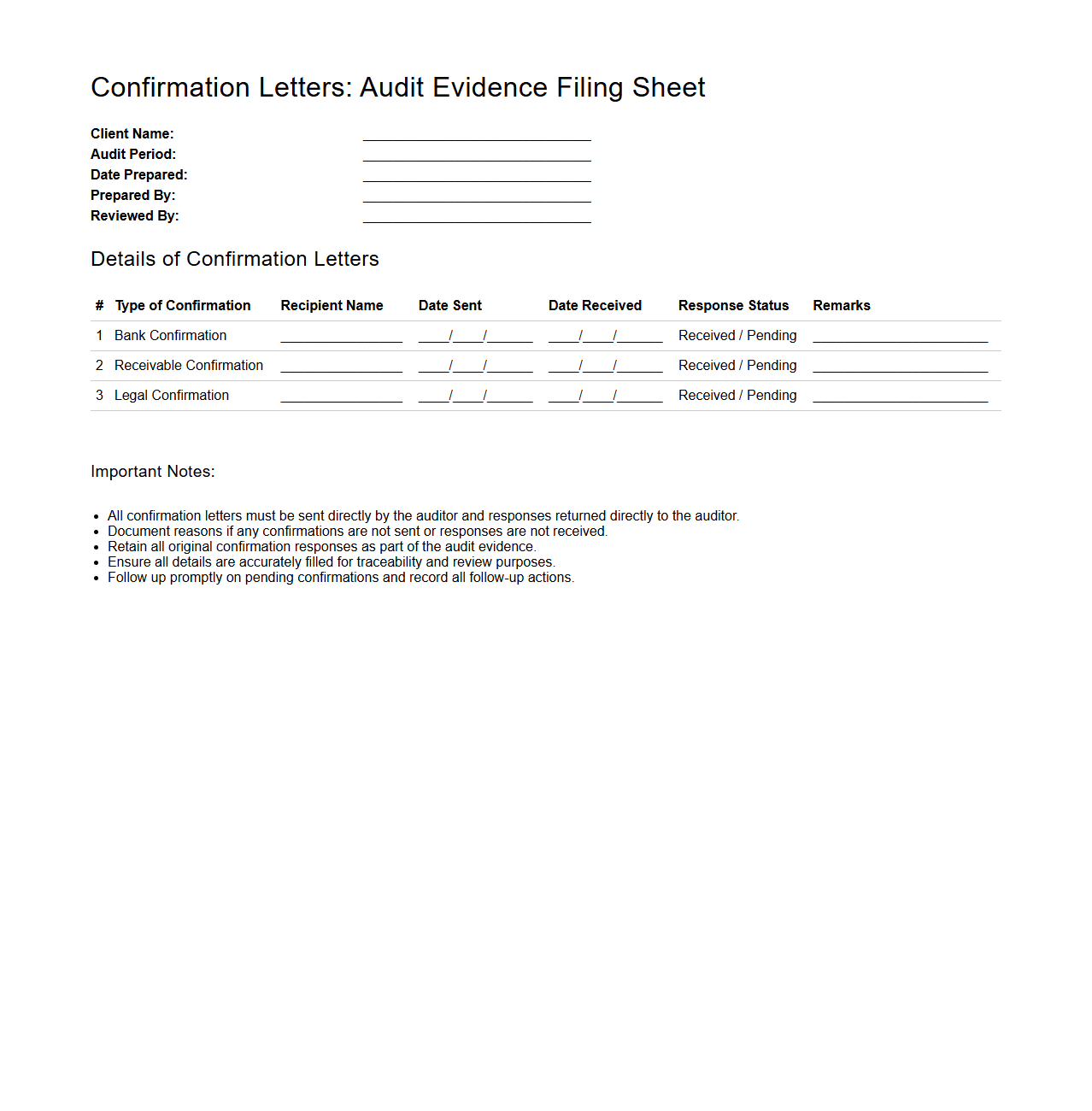

Confirmation Letters: Audit Evidence Filing Sheet

A

Confirmation Letters: Audit Evidence Filing Sheet document serves as an organized record compiling all confirmation letters obtained during an audit, providing crucial evidence to verify account balances and transactions. It helps auditors track the receipt, status, and responses of third-party confirmations, ensuring compliance with auditing standards and supporting the accuracy of financial statements. This document enhances the reliability of audit findings by systematically maintaining audit evidence for review and future reference.

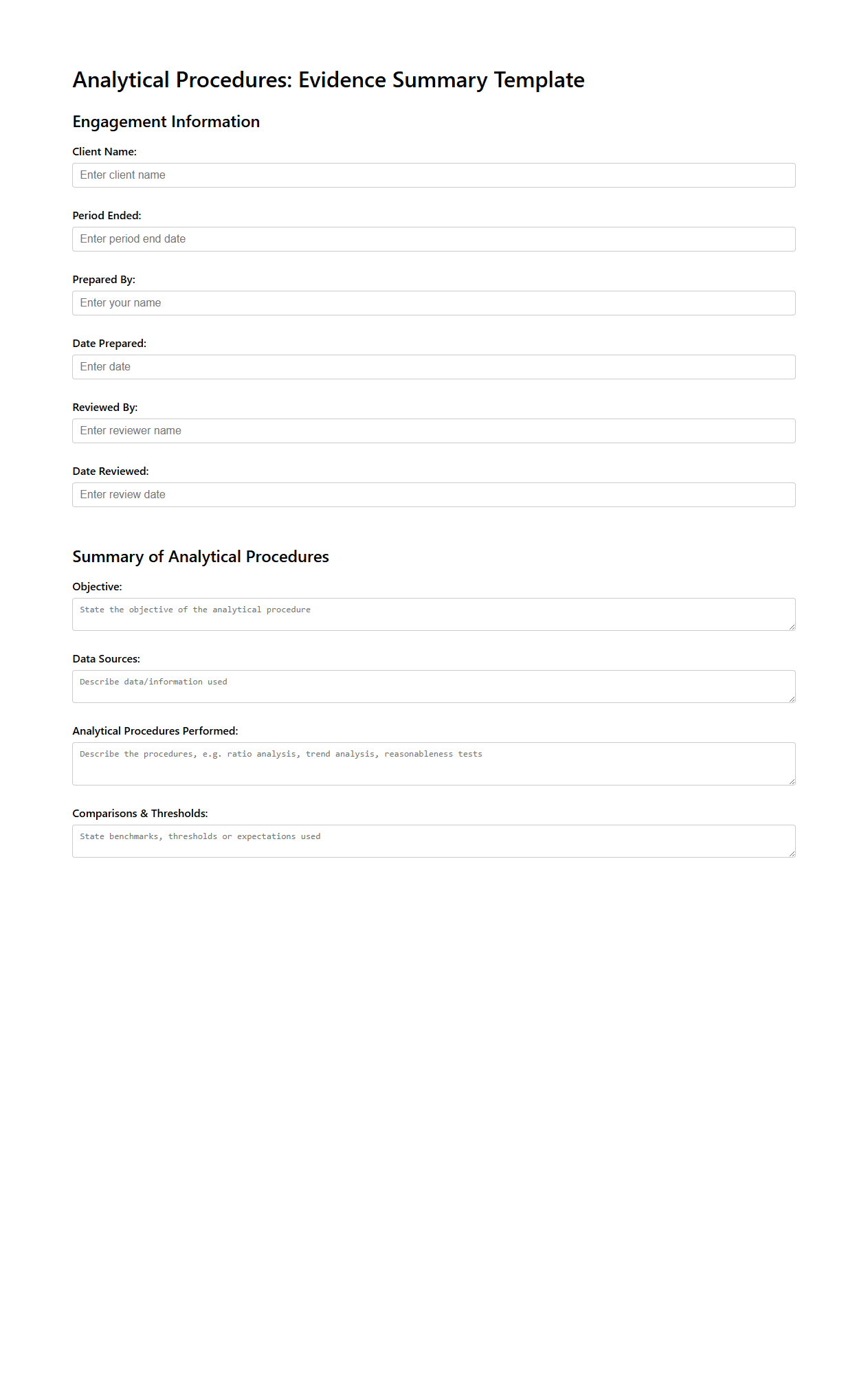

Analytical Procedures: Evidence Summary Template

The

Analytical Procedures: Evidence Summary Template document is a structured tool used by auditors to systematically collect and evaluate financial data during the audit process. It facilitates the identification of trends, inconsistencies, and anomalies by summarizing analytical evidence in a clear and concise manner. This template ensures comprehensive documentation that supports audit conclusions and compliance with auditing standards.

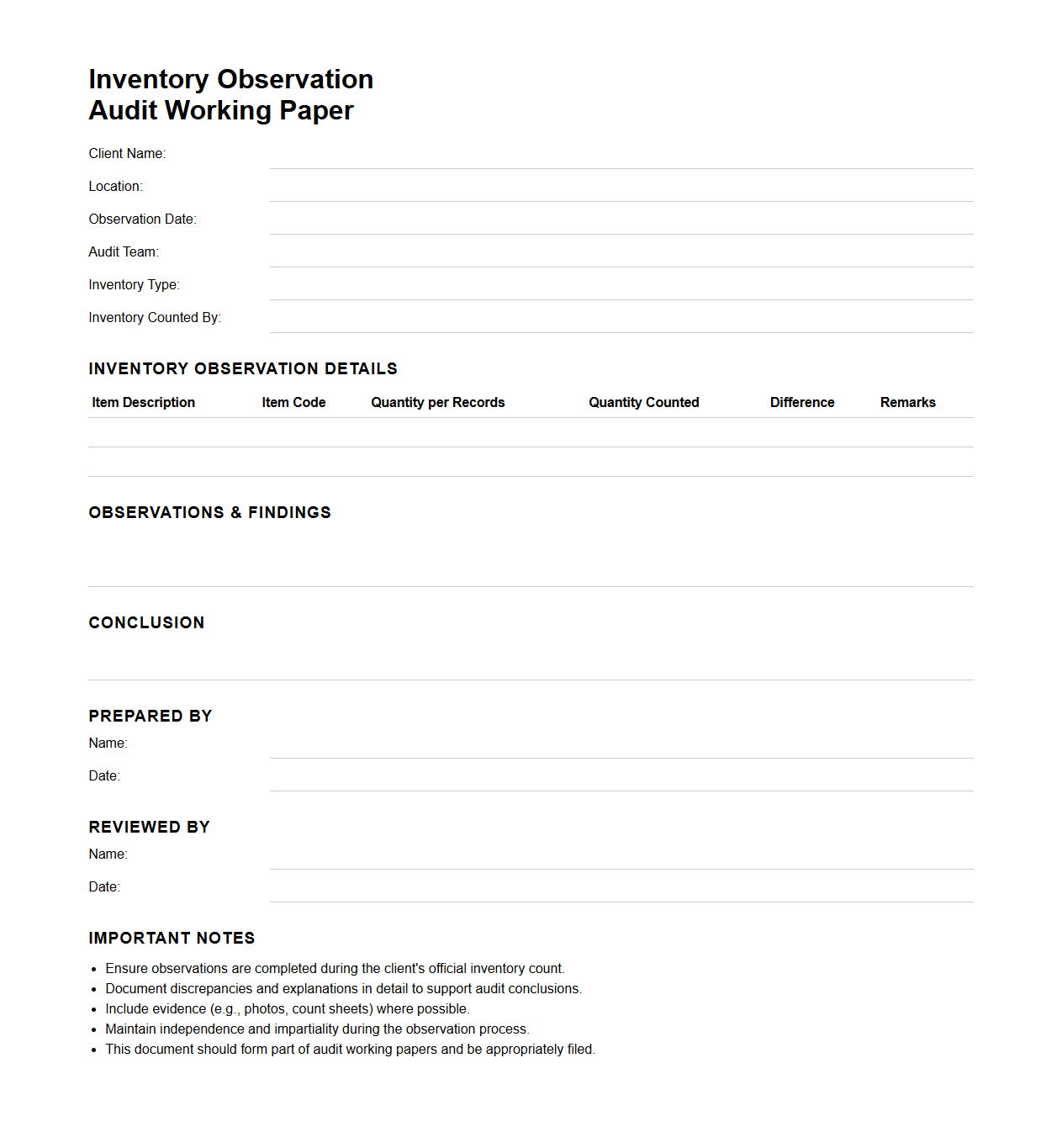

Inventory Observation: Audit Working Paper Format

The

Inventory Observation: Audit Working Paper Format document is a structured template used by auditors to systematically record and evaluate inventory observations during an audit. It ensures accurate documentation of stock quantities, conditions, and procedures, facilitating compliance verification and risk assessment. This format enhances transparency and supports audit conclusions by providing a clear, consistent framework for capturing inventory details.

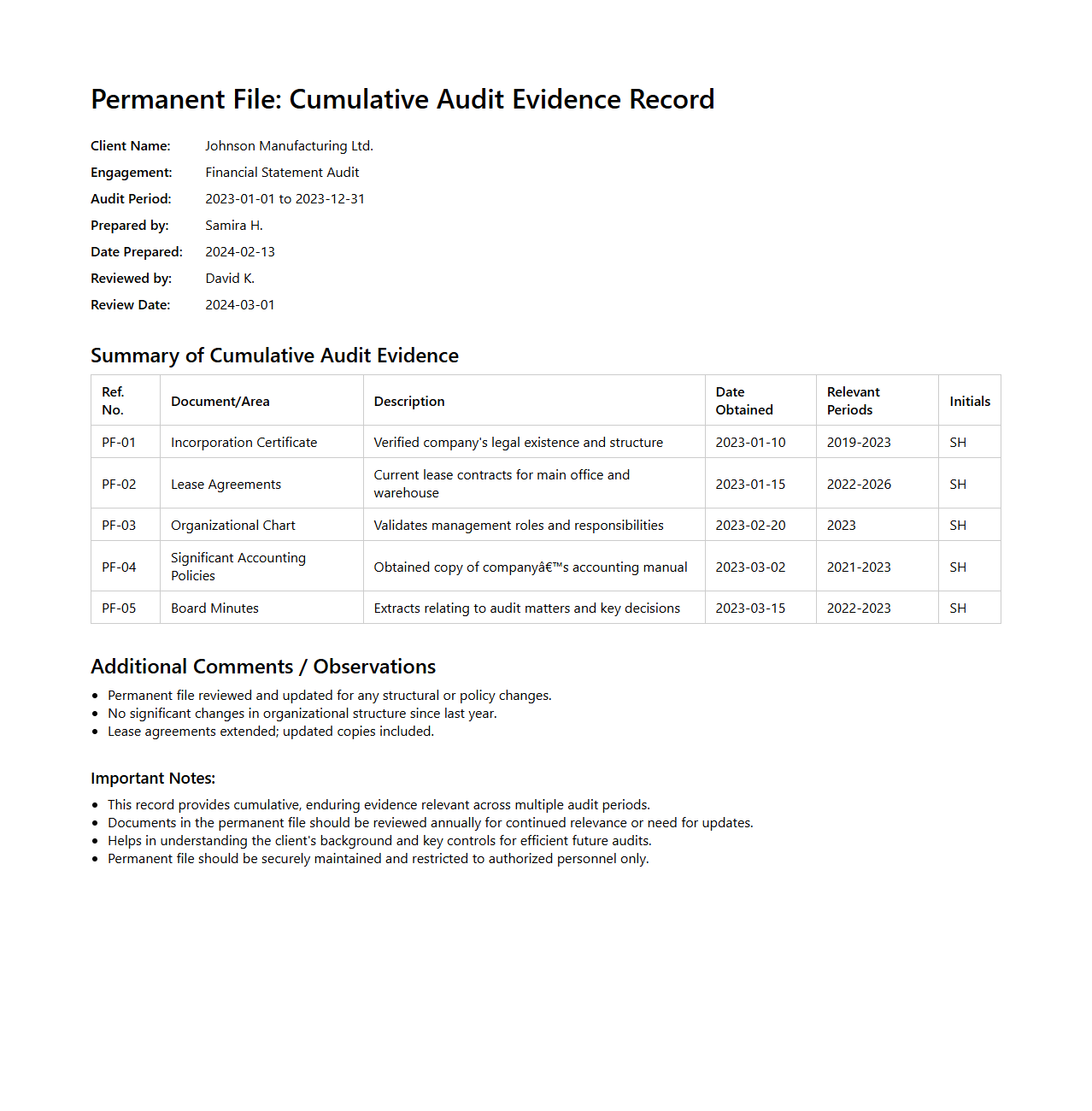

Permanent File: Cumulative Audit Evidence Record

The

Permanent File: Cumulative Audit Evidence Record document is a critical component in audit documentation, serving as a repository for ongoing and historical audit evidence that supports the auditor's understanding of the client's business and control environment over multiple periods. It includes key information such as organizational structure, accounting policies, significant contracts, and internal controls, which facilitate continuity and efficiency in audits year after year. This file helps auditors maintain a comprehensive record that informs risk assessment and audit planning processes.

What specific layout should audit working papers follow to comply with ISA standards?

The layout of audit working papers must adhere to the International Standards on Auditing (ISA) requirements to ensure clarity and completeness. Each working paper should be organized logically, featuring clear headings, dates, and reference codes for easy navigation. Proper layout facilitates audit trail integrity and supports the overall audit opinion.

How should electronic audit evidence be documented within digital working papers?

Electronic audit evidence must be documented within digital working papers with clear annotation and metadata to establish authenticity and reliability. Essential details such as source, date, and relevance to audit objectives must be recorded alongside the evidence. This ensures that digital files remain verifiable and accessible throughout the audit lifecycle.

What mandatory sections must be included in audit working paper formats for legal validity?

For legal validity, audit working papers must include mandatory sections such as purpose, procedures performed, findings, and conclusions. Additionally, reviewer sign-offs and date stamps are crucial to demonstrate accountability and the timeline of the audit process. These sections collectively ensure the working papers meet regulatory and professional requirements.

How are cross-referencing and indexing best structured in working paper formats?

Cross-referencing and indexing should be structured using a consistent coding system to link related documents and evidence seamlessly. Indexes must be detailed and organized to help auditors quickly locate supporting information within the audit file. Effective cross-referencing enhances the traceability and efficiency of audit reviews and oversight.

What audit evidence details are required in working papers for high-risk transactions?

Working papers for high-risk transactions should contain detailed descriptions, source documentation, and auditor's judgement to support risk assessment conclusions. Additional evidence such as recalculations, confirmations, and specific risk response activities must be fully documented. This thorough approach helps demonstrate due diligence and supports audit quality in complex areas.